Semiconductor Supply Chain Market Size Analysis:

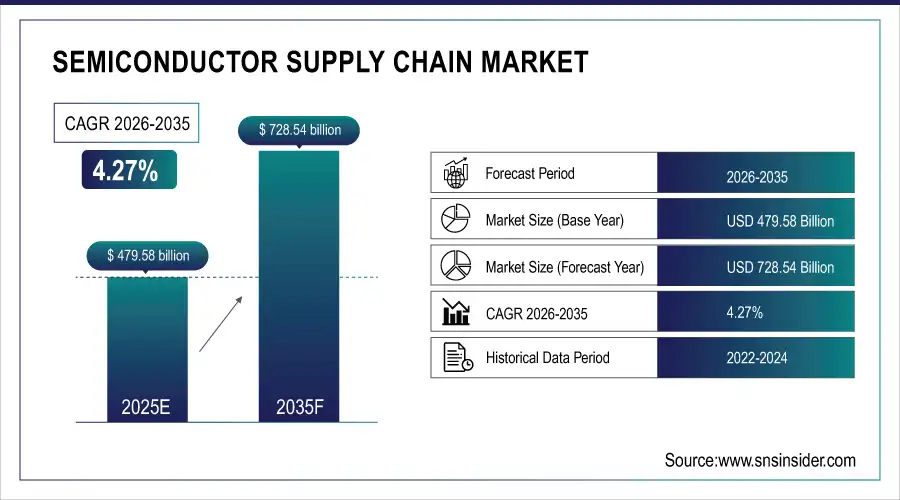

The Semiconductor Supply Chain Market Size is valued at USD 479.58 Billion in 2025 and is projected to reach USD 728.54 Billion by 2035, growing at a CAGR of 4.27% during the forecast period 2026–2035.

The Semiconductor Supply Chain Market analysis report provides a comprehensive overview of industry trends, highlighting technological advancements, supply chain optimization and increasing semiconductor demand across automotive, consumer electronics and industrial sectors. Rising digitalization, IoT adoption and electronics manufacturing expansion are expected to drive market growth.

Semiconductor Supply Chain handled 1.2 trillion units in 2025, driven by electronics, automotive, and industrial demand.

Market Size and Growth Projection:

-

Market Size in 2025: USD 479.58 Billion

-

Market Size by 2035: USD 728.54 Billion

-

CAGR: 4.27% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Semiconductor Supply Chain Market - Request Free Sample Report

Semiconductor Supply Chain Market Trends:

-

Rising demand for consumer electronics, EVs and IoT devices is driving growth across the semiconductor supply chain.

-

Adoption of advanced manufacturing technologies, AI and automation is streamlining supply chain efficiency.

-

Increasing focus on supply chain resilience and risk mitigation is shaping logistics and sourcing strategies.

-

Expansion of cloud-based and software-driven supply chain solutions is enhancing real-time monitoring and optimization.

-

Growth in emerging markets is boosting semiconductor consumption across industrial, automotive and telecommunication sectors.

-

Sustainable and energy-efficient manufacturing practices are trending, reflecting emphasis on eco-friendly production and responsible sourcing.

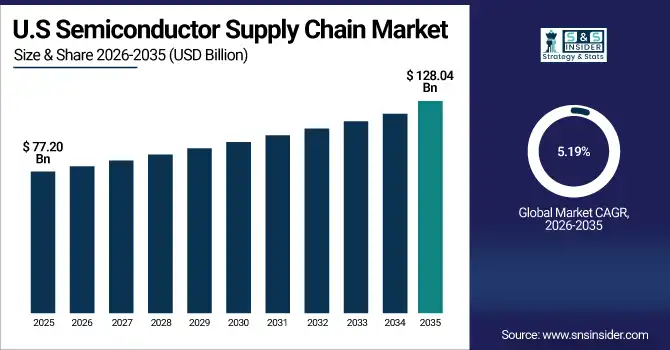

U.S. Semiconductor Supply Chain Market Size Outlook:

The U.S. Semiconductor Supply Chain Market is projected to grow from USD 77.20 Billion in 2025 to USD 128.04 Billion by 2035, at a CAGR of 5.19%. Growth is driven by rising semiconductor demand across automotive, AI, data centers and consumer electronics, alongside strong investments in domestic manufacturing and supply chain resilience.

Semiconductor Supply Chain Market Growth Drivers:

-

Surging demand for semiconductors in automotive, consumer electronics and IoT accelerating supply chain market growth.

Surge in the semiconductor demand, is one of the key factors fuelling the growth of Semiconductor Supply Chain Market. Dramatic growth across consumer electronics, electric vehicles and IoT devices is driving manufacturers to implement efficient and robust supply chain solutions. Advanced technology integration that includes AI, automation and cloud-based monitoring is streamlining production, testing and distribution. As this demand for capable, high-performing semiconductors grows, it is changing logistics strategies, increasing supply chain visibility and driving market growth in several industries.

Semiconductor shipments grew 8.5% in 2025, driven by rising demand from consumer electronics, automotive and IoT sectors.

Semiconductor Supply Chain Market Restraints:

-

Supply chain disruptions, chip shortages and geopolitical tensions are restricting consistent semiconductor market growth.

Supply chain tumult, chip shortages and geopolitical tensions are prominent constraints for Semiconductor Supply Chain Market. The reliance on a few production facilities, scarce minerals and complicated logistics is what can make scaling up expensive. Trade barriers, export controls and regulatory requirements also limit frictionless running of business. Those limitations add sourcing risk for manufacturers, affect production schedules, raise prices and put up barriers to new entrants they're looking to penetrate high-demand, technology-intensive semiconductor areas.

Semiconductor Supply Chain Market Opportunities:

-

Growing adoption of AI, IoT and electric vehicles presents significant opportunities for advanced semiconductor supply solutions.

Widespread implementation of AI, IoT and electric vehicles is the massive opportunity for Semiconductor Supply Chain Market. Demand for high-quality, high-performance semiconductors is leading to the growth of advanced supply chain solutions such as AI-based logistics and cloud-mediated monitoring and automation. Firms are maximizing production, testing and delivery to accommodate tech-driven demands. The move toward these smarter, more efficient supply chains drives increased operational resilience, market differentiation and long-term growth in a range of industry sectors.

Advanced semiconductor supply chain solutions accounted for 28% of new technology investments in 2025, driven by rising AI, IoT, and EV adoption.

Semiconductor Supply Chain Market Segmentation Analysis:

-

By Component, Semiconductors held the largest market share of 42.76% in 2025, while Software & Services is expected to grow at the fastest CAGR of 6.15% during 2026–2035.

-

By Supply Chain Stage, Manufacturing accounted for the highest market share of 38.21% in 2025, while Assembly & Packaging is projected to expand at the fastest CAGR of 5.48% during the forecast period.

-

By End-User Industry, Consumer Electronics dominated with a 34.88% share in 2025, while Automotive is anticipated to record the fastest CAGR of 5.63% through 2026–2035.

-

By Deployment Type, On-Premises held the largest share of 71.24% in 2025, while Cloud-Based is expected to grow at the fastest CAGR of 6.08% during 2026–2035.

-

By Logistics Type, In-House accounted for the largest share of 64.33% in 2025, while Third-Party Logistics are forecasted to register the fastest CAGR of 5.92% during 2026–2035.

By Component, Semiconductors Dominates While Software & Services Expands Rapidly:

Market Dynamics The semiconductors segment is leading the market owing to its key applications in consumer electronics, automotive, and industrial sectors. Its leadership is buttressed by high-volume manufacturing and substantial R&D, as well as vital demand for chips it’s the only one on record with any flexibility at scale (such as AI and IoT devices). The number of semiconductor units processed in 2025 were over 520 billion.

Software & Services is the most rapidly expanding segment, where AI-powered supply chain optimisation, predictive analytics and cloud-based supervision are leading product launches. By the end of 2025 over 1.2 billion instances of software-supported supply chain network processes were deployed, indicating adoption on an massive scale to increase both efficiency and resilience.

By Supply Chain Stage, Manufacturing Dominates While Assembly & Packaging Expands Rapidly:

Manufacturing was the most prominent market segment because of high capital investment, complicated fabrication and strategic value for semiconductors. Leading foundry and fab companies accounted for most of the production, meanwhile wafer processing exceeded 620 million in 2025.

The Assembly & Packaging segment is the fastest growing and is driven by advanced packaging technologies, 3D stacking and miniaturization requirements. 2025 Cumulative units filed surpassed 140 million units, a fast uptake of new technologies to service high performance applications.

By End-User Industry, Consumer Electronics Dominates While Automotive Expands Rapidly:

Based on End-User Industry, consumer electronics segment held the largest market share as thousands of smartphones, laptops and wearables have been manufactured. There were more than 450 billion semiconductor units used in electronics in 2025, which is a good indicator: high demand. Strong uptake of smart devices is contributing to market expansion.

The automotive segment is the fastest growing on the back of electric vehicle (EV) penetration, advanced driver-assistance systems (ADAS) and connected car growth. The load factor for automotive semiconductors to be installed in cars peaked at 85 billion units in 2025, indicating a strong growth potential and dependence on high-performance chips for cars.

By Deployment Type, On-Premises Dominates While Cloud-Based Expands Rapidly:

On-Premises held the dominant position in this market, as this has been the traditional way of working with in-house IT environment, security and closed & protected supply chain management systems. More than 3500 firms employed on premise technology in semiconductor operations, in 2025. Powerful data control, along with flexibility of customization, is still driving industry adoption.

Fastest growing segment is Cloud-Based with real time monitoring, AI based analytics and scalability benefits. These cloud-based supply chain solutions were increasingly selected by 1,250 companies in 2025 due to their speed of deployment in a digital transformation-focused and inter-connected world.

By Logistics Type, In-House Dominates While Third-Party Logistics Expands Rapidly:

In-House segment was the leading type as major semiconductor companies possess their own control over warehousing, transportation and inventory planning. In 2025, 1,750 firms organized their own logistics and maintained quality and reliability. Improved operational visibility further reinforces supply chain efficiency and success.

The fastest growing segment is Third-Party Logistics resulting from the needs of outsourcing, cost-effectiveness and distribution complexities. By 2025, a total of 980 companies used the services of a third-party logistics company suggesting that shippers increasingly turned to dedicated providers for dynamic demand fulfillment. Agility and scale are what keep the wheels turning in regard to market uptake.

Semiconductor Supply Chain Market Regional Analysis:

Asia-Pacific Semiconductor Supply Chain Market Insights:

The Asia-Pacific Semiconductor Supply Chain Market dominated with a market share of 46.82% in 2025. Growth is driven by high demand for consumer electronics, automotive and industrial applications across China, Japan, South Korea and Taiwan. Rapid adoption of IoT, AI and electric vehicles is fueling semiconductor consumption, while investments in advanced manufacturing and supply chain optimization enhance operational efficiency. The region remains the largest and most influential market in semiconductor supply chain operations.

Get Customized Report as per Your Business Requirement - Enquiry Now

China Semiconductor Supply Chain Market Insights:

There has been also a large and escalating demand in Chinese market for both consumer electronics (e.g. smart phones, TVs), electric vehicles (EV) or industrial applications that must increasingly rely on imported ICs. China plays a significant role in the APAC semiconductor supply chain market as it has rapidly embraced technologies such as AI, IoT, and smart manufacturing and is being backed by government support for locally produced chips.

North America Semiconductor Supply Chain Market Insights:

The Semiconductor Supply Chain Market in North America grows the fastest with a CAGR of 5.42% over the next nine years. Growth is fueled by increased demand for semiconductors in electric vehicles, artificial intelligence, data centers and advanced consumer electronics. Significant investments in domestic manufacturing, supply chain resiliency efforts and rapid penetration of cloud-based and automated solutions establishes North America as a booming center for innovation, capacity growth and critical supply chain development.

U.S. Semiconductor Supply Chain Market Insights:

U.S. semiconductor supply chain market is gaining traction due to increasing demand for high-performance chips in AI, electric vehicles and data centers. Tamayo added that aggressive government support for in-country fab, increasing uptake of automation and cloud-based supply chain systems and renewed emphasis on supply resiliency are all driving the country’s leadership in the North American semiconductor supply chain market.

Europe Semiconductor Supply Chain Market Insights:

Expansion of Europe Semiconductor Supply Chain Market can be associated with increasing demand for semiconductors in automotive, industrial automation & renewables. Germany, UK, France and Italy are all contributing strongly on the back of robust automotive manufacturing and uptake of Industry 4.0. Growing investment into local chip fabrication, focus on supply chain resiliency and roll-out of advanced manufacturing infrastructure further establish Europe as a future growth market within the semiconductor ecosystem.

Germany Semiconductor Supply Chain Market Insights:

Germany is Important Semiconductor Supply Chain Market driven by its robust automotive industry fabrication, industrial automation and Industry 4.0 development. Increased demand for semiconductors in electric vehicles, smart manufacturing and renewable energy applications as well as investment in domestic chip production and supply chain robustness are also strengthening Germany’s position within the European semiconductor landscape.

Latin America Semiconductor Supply Chain Market Insights:

The Latin America Semiconductor Supply Chain Market is growing at a moderate pace on account of increasing demand for consumer electronics, automotive parts and industrial automation in Brazil, Mexico and Argentina. Moreover the development of electronics manufacturing, improvements to logistics infrastructure and greater adoption of digital technologies are fuelling supply chain growth and boosting the region’s status in the semiconductor ecosystem.

Middle East and Africa Semiconductor Supply Chain Market Insights:

Middle East & Africa Semiconductor Supply Chain Market size is increasing as demand for consumer electronics, connected infrastructure and industrial automation accelerates. Expansion in investments being made by various companies is expected cater to the growth of the semiconductor supply chain across GCC, with considerable penetration within Saudi Arabia, the UAE and South Africa focusing much on this momentum.

Semiconductor Supply Chain Market Competitive Landscape:

TSMC, based in Hsinchu, Taiwan, is the world’s biggest and most important contract maker of computer chips. The firm controls the entire supply chain, from manufacturing (the most advanced globally) to massive fabrication capacity and superior R&D investments in innovative process nodes. Such a vertically integrated ecosystem enables chip design enablement, wafer fabrication and high-volume production for fabless to best serve customers." A well-established R&D commitment and leading-edge lithography and manufacturing results in consistently high-performance, low-power chips for the consumer electronics, AI, automotive and HPC markets guarantee TSMC’s leading position

-

In April 2025, TSMC launched its 2nm process technology, enabling higher performance and energy efficiency for AI, automotive and high-performance computing chips, strengthening its leadership in advanced semiconductor manufacturing and supply chain dominance.

Based in Santa Clara, Calif., NVIDIA is the leading designer of advanced semiconductor units that cater for a diverse range of end markets which include its GPU, AI and accelerated computing offerings. As a fabless company NVIDIA has substantial power regarding manufacturing, packaging and distribution through cooperation with various leading foundries and ecosystem players. The company’s leadership in those categories — A.I., data centers, automotive computing and high performance graphics — has fueled enormous demand for semiconductors. This has made NVIDIA a major force in the semiconductor supply chain, with its relentless innovation efforts, software-hardware integration and platform-driven approach ensuring that the demand dynamic is in its favour.

-

In March 2025, NVIDIA introduced its Blackwell AI platform, expanding GPU offerings for data centers and generative AI workloads, driving increased semiconductor demand and reinforcing its dominant role within the semiconductor supply chain ecosystem.

Samsung Electronics, based in Suwon, South Korea and known for its large position in the semiconductor supply chain from design to manufacturing of memory chips, logic semiconductors and advanced packaging. Large production capacity, advanced process technology as well as good management of fabrication, package and testing issues make the company to be the world-class leader. Memory Samsung’s strength in memory semiconductors and increased investments in foundry have enabled the company to quickly respond to demand for a wide variety of applications spanning consumer electronics, data centers and automotive devices. Strong R&D, manufacturing and supply chain robustness have strengthened Samsung’s status as a leading semiconductor industry player.

-

In February 2025, Samsung Electronics unveiled enhanced 3nm Gate-All-Around technology, improving yield and performance for mobile, AI and automotive chips, supporting its foundry expansion and strengthening supply chain resilience and manufacturing leadership.

Key Semiconductor Supply Chain Companies are:

-

NVIDIA

-

Samsung Electronics

-

Intel

-

Broadcom

-

SK Hynix

-

AMD

-

ASML Holding

-

Applied Materials

-

Micron Technology

-

Texas Instruments

-

STMicroelectronics

-

Infineon Technologies

-

Sony Semiconductor Solutions

-

Marvell Technology

-

KLA Corporation

-

Entegris

-

Amkor Technology

-

Sumco Corporation

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 479.58 Billion |

| Market Size by 2035 | USD 728.54 Billion |

| CAGR | CAGR of 4.27% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Semiconductors, Wafers, Packaging & Testing Equipment, Materials, Software & Services) • By Supply Chain Stage (Design, Manufacturing, Assembly & Packaging, Testing & Distribution, Aftermarket Services) • By End-User Industry (Consumer Electronics, Automotive, Telecommunications, Industrial, Healthcare, Aerospace & Defense, Others) • By Deployment Type (On-Premises, Cloud-Based) • By Logistics Type (In-House, Third-Party Logistics) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | TSMC, NVIDIA, Samsung Electronics, Intel, Qualcomm, Broadcom, SK Hynix, AMD, ASML Holding, Applied Materials, Micron Technology, Texas Instruments, STMicroelectronics, Infineon Technologies, Sony Semiconductor Solutions, Marvell Technology, KLA Corporation, Entegris, Amkor Technology, Sumco Corporation. |

Frequently Asked Questions

Asia-Pacific dominated the market with a 46.82% share in 2025, while North America is the fastest-growing region, projected to expand at a CAGR of 5.42% during 2026–2033.

Semiconductors dominated the market with a 42.76% share in 2025, while Software & Services is projected to grow at the fastest CAGR of 6.15% during 2026–2033.

Growth is driven by rising semiconductor demand across electronics, automotive, AI and IoT, supported by automation and cloud-based supply chain adoption.

The market is valued at USD 479.58 Billion in 2025E and is projected to reach USD 668.40 Billion by 2033.

The Semiconductor Supply Chain Market is expected to grow at a CAGR of 4.27% during the forecast period 2026–2033.

Get in Touch