Semiconductor Market Report Scope and Overview:

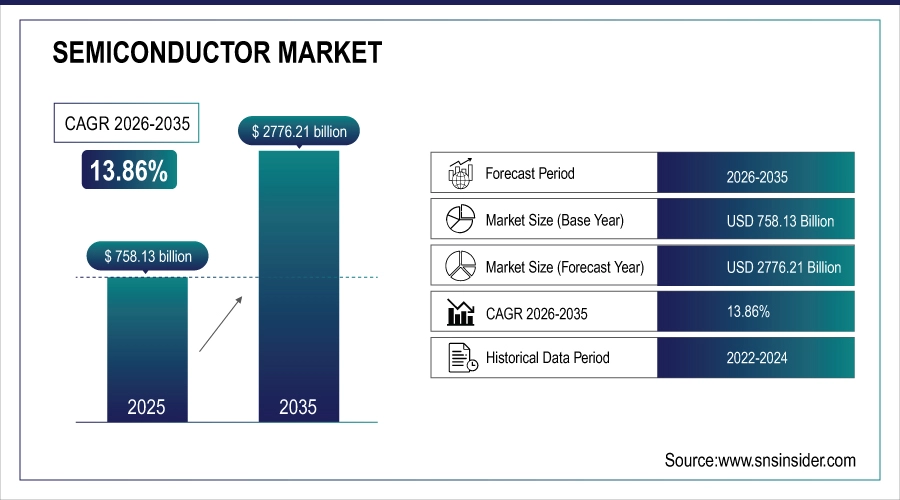

The Semiconductor Market size was valued at USD 758.13 Billion in 2025 and is projected to reach USD 2776.21 Billion by 2035, growing at a CAGR of 13.86 % during 2026-2035.

Semiconductors have continuously advanced rapidly, moving to smaller technology nodes, like 5nm and 3nm, which should allow higher performance and energy efficiency. With demand from AI, IoT, and automotive growing, manufacturers are balancing between production volume and capacity utilization. It is important to leverage supply chain efficiencies–strategic sourcing, inventory management, and more–to avoid disruption in supply output. As chip design focuses on sustainable and high-performance computing solutions that demand less power and efficient thermal management, power efficiency metrics are emerging as critical metrics.

Semiconductor Market Size and Forecast:

-

Market Size in 2025 USD 758.13 Billion

-

Market Size by 2035 USD 2776.21 Billion

-

CAGR 13.86% from 2026 to 2035

-

Base Year 2025

-

Forecast Period 2026–2035

-

Historical Data 2022–2024

Get More Information on Semiconductor Market - Request Sample Report

Semiconductor Market Highlights:

-

Indian semiconductor manufacturing is advancing as domestic players invest in advanced chip packaging and system-in-package capabilities, strengthening local assembly and testing infrastructure.

-

India’s fabless semiconductor design ecosystem is gaining momentum, supported by successful delivery of custom SoCs for space and defense applications, boosting investor confidence.

-

Global memory capacity expansion is accelerating, with major players acquiring fabs to secure long-term DRAM supply amid rising AI, data center, and high-performance computing demand.

-

Strategic cross-border semiconductor acquisitions are reinforcing supply chain resilience and increasing cleanroom and advanced manufacturing capacity in Asia.

-

US–Taiwan semiconductor cooperation is deepening through large-scale investment commitments, aiming to secure AI-focused chip supply chains and reduce geopolitical risk exposure.

-

Overall, the semiconductor market is witnessing strong consolidation, localization efforts, and geopolitical realignment, shaping long-term growth and capacity planning.

The U.S. Semiconductor market size was valued at an estimated USD 285.40 billion in 2025 and is projected to reach USD 1013.43 billion by 2035, growing at a CAGR of 13.51% over the forecast period 2026–2035. The market is being driven by increasing demand for advanced chips in computing, AI (artificial intelligence), automotive electronics, communications as well as consumer electronics. Semiconductor consumption continues to grow as AI, 5G, cloud computing and Internet of Things (IoT) adoption increases. Moreover, robust government support for the development of native semiconductor manufacturing capabilities, an escalation in fabrication facilities and continued innovations being made to chip design and process nodes will continue to provide traction to the U.S. semiconductor market over the course of next few years.

Semiconductor Market Drivers:

-

Surging Semiconductor Demand Driven by Consumer Electronics IoT Electric Vehicles Data Centers and 5G

The rapid growth of the consumer electronics market with increasing demand for smartphones, tablets, and wearable devices has been also driving the semiconductor market as these devices need advanced chips for better performance and efficiency. Also powering the demand for memory and logic devices is the growth of data centers and cloud computing. In addition, the rise of the Internet of Things (IoT) and the expanding connected device base, from smart homes to industrial automation, is driving up demand for sensors and microcontrollers, also registering strong double-digit growth. The growing electric vehicle (EV) market subsequently boosts the need for power electronics and semiconductor elements with battery management systems and advanced driver assistance systems (ADAS) being the prime targets. In addition, the demand for high-speed processors and communication chips caused by the promotion of 5G continues.

Semiconductor Market Restraints:

-

The Semiconductor Market Faces Challenges with Complex Manufacturing Supply Chain Disruptions Environmental Regulations and IP Theft

The complexity of manufacturing processes that require advanced equipment and precision is one of the key restraints for the semiconductor market. Chip architectures shrink and increase in complexity to deliver greater performance but there is a greater challenge in maintaining yield and process control. Matsubara said the industry also is experiencing supply chain disruptions from geopolitical tensions, export restrictions, and its reliance on a small number of regions for raw materials and manufacturing. Another major challenge is a lot of environmental regulations and sustainability issues because semiconductor manufacturing requires the use of hazardous chemicals and high volumes of energy. Additionally, high-tech markets are also shot at by a reputable risk, since the theft of intellectual property (IP) (Cyberwar) has become the new war.

Semiconductor Market Opportunities:

-

Growth Opportunities in Advanced Semiconductor Materials AI Automotive Edge Computing and Smart City Solutions

Advanced semiconductor materials, providing increased efficiency and power handling capabilities (i.e., gallium nitride [GaN], silicon carbide [SiC]) represent another area with considerable growth potential. Growing demand for artificial intelligence (AI) and machine learning (ML) applications could provide a boost to high-performance computing chips and chipsets with dedicated processors. automotive semiconductor will be the fastest-growing segment thanks to the transition to autonomous vehicles and in-vehicle infotainment systems. Furthermore, the growth in demand for edge computing as well as smart cities opens up opportunities for innovation around low-power chips and also connectivity solutions.

Semiconductor Market Segment Analysis:

By Application

Networking & Communications was the largest semiconductor end-use market in 2025, accounting for 28.8% of the semiconductor market, as the deployment of 5G technology accelerates, internet penetration continues to expand, and demand for data centers grows. This segment will benefit from the use of wireless communication technology and/or the requirement for high-speed data access.

The automotive sector is slated to grow at a rapid CAGR during 2026 – 2035, driven by the increasing adoption of electric vehicles (EVs), advanced driver assistance systems (ADAS), and autonomous driving technology. This segment is propelled by the increasing use of power management chips and sensors in smart vehicles.

By Component

Memory Devices dominated the semiconductor market with a 33.4% share in 2025 and are expected to grow at the fastest CAGR from 2026 to 2035. Such growth is supported by the growing need for HPC, data storage solutions, and increased adoption in consumer electronics, data centers, and artificial intelligence. Cloud computing and 5G technology further increase the demand for high-performance memory solutions. Meanwhile, the electrical vehicle (EV) market, which is gradually increasing, also needs suitable memory devices for battery management (BMS) and infotainment systems. Memory Devices are poised to continue as a critical building block in the evolving semiconductor landscape, supported by continued innovation within NAND and DRAM, as well as the promise of emerging memory technologies such as MRAM and ReRAM to stimulate the market, reads the report.

Semiconductor Market Regional Analysis:

Asia-Pacific Semiconductor Market Trends:

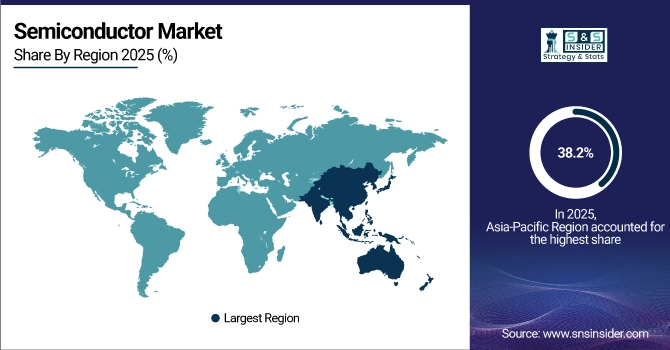

The semiconductor market was led by Asia-Pacific and accounted for 38.2% of the total market share in 2025 owing to the major manufacturing hubs and increased consumption of consumer electronics. Focal nations are China, South Korea, and Taiwan as of organizations like TSMC, Samsung Electronics, and SK Hynix. Powering the world's smartphones, laptops, and data centers, these companies are at the top of the advanced chip manufacturing chain. Japan's Sony and Renesas have also been key in sensor and semiconductor chips for cars, respectively.

Need any customization research on Semiconductor Market - Enquiry Now

North America Semiconductor Market Trends:

North America is expected to experience the highest CAGR growth rate from 2026-2035, fueled by the progress of artificial intelligence, cloud computing, and self-driving cars. Flagship corporations such as Intel, NVIDIA, and Qualcomm are spearheading the progress for high-performance computing, graphical processing, and 5G. This growth is also aided by the U.S. government's efforts to increase domestic semiconductor production through acts like the CHIPS Act. Demand in North America is also being boosted by advanced chips used for electric vehicles and autonomous driving features from North American automakers, including Tesla.

Europe Semiconductor Market Trends:

Semiconductor Market Growth in Europe Propelled by Automotive Electronics, Industrial Automation, and IoT Adoption. Germany, France and the Netherlands are key players with advanced manufacturing, automotive chip production and R&D hubs. The automotive and power sectors are the target applications of choice in this region, where companies are seeking automotive-grade semiconductors, power management ICs and industrial sensors to serve these growing markets. The move towards electric vehicles, smart manufacturing and AI-backed industry solutions is reinforcing Europe’s semiconductor requirement.

Latin America Semiconductor Market Trends:

The growth of the Latin America semiconductor market is driven by growing automotive electronics, consumer electronics, and industrial automation in the region. Brazil and Mexico are two of the biggest exporters, with automotive semiconductors, memory devices and power management ICs as the key product categories. Regional consumption growth is driven by increasing demand for smartphones, electric vehicles and data centers, as well as government insulation for domestic electronics manufacturing.

Middle East & Africa Semiconductor Market Trends:

ME&A semiconductor industry is growing due to rising investments in digital infrastructure, smart cities and telecom. The UAE, Israel and South Africa are the major market boosters; with IoT solution & electronics manufacturing growing significantly in these regions. Government efforts to increase tech innovation, along with increasing penetration of smartphones and consumer electronic devices, are helping drive demand for memory chips, processors and sensors.

Semiconductor Market Competitive Landscape:

Intel a leader in the semiconductor industry, is shaping the data-centric future with computing and communications technology that is the foundation of the world's innovations. In January 2025, its Intel Foundry Services entered into defense partnerships with Trusted Semiconductor Solutions and Reliable MicroSystems as part of the U.S. DoD's RAMP-C program

-

In January 2025, Intel Foundry Services secured new defense clients, Trusted Semiconductor Solutions and Reliable MicroSystems, for its advanced 18A process under the U.S. DoD's RAMP-C program.

Semiconductor Market Key Players:

-

Intel

-

Samsung Electronics

-

TSMC

-

Qualcomm

-

NVIDIA

-

Broadcom

-

SK Hynix

-

Micron Technology

-

Texas Instruments

-

AMD

-

MediaTek

-

Applied Materials

-

ASE Technology Holding

-

Infineon Technologies

-

Sony

-

ON Semiconductor

-

NXP Semiconductors

-

STMicroelectronics

-

Renesas Electronics

-

Marvell Technology

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 758.13 Billion |

| Market Size by 2035 | USD 2776.21 Billion |

| CAGR | CAGR of 13.86% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Memory Devices, Logic Devices, Analog IC, MPU, Discrete Power Devices, MCU, Sensors, Others (DSP)) • By Application (Data Processing, Industrial, Networking & Communications, Consumer Electronics, Automotive, Government) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intel, Samsung Electronics, TSMC, Qualcomm, NVIDIA, Broadcom, SK Hynix, Micron Technology, Texas Instruments, AMD, MediaTek, Applied Materials, ASE Technology Holding, Infineon Technologies, Sony, ON Semiconductor, NXP Semiconductors, STMicroelectronics, Renesas Electronics, Marvell Technology |

Frequently Asked Questions

Ans: Asia Pacific dominated the Semiconductor Market in 2025.

Ans: The Memory Devices segment dominated the Industrial battery market in 2025.

Ans: The major growth factor of the Semiconductor market is the rising demand for advanced chips driven by digital transformation, AI, IoT, and electric vehicles.

Ans: The Semiconductor Market size was valued at USD 758.13 Billion in 2025 and is projected to reach USD 2776.21 Billion by 2035, growing at a CAGR of 13.86 % during 2026-2035.

Ans: The Semiconductor Market is expected to grow at a CAGR of 13.86% during 2026-2035.

Get in Touch