Server Market Report Scope & Overview:

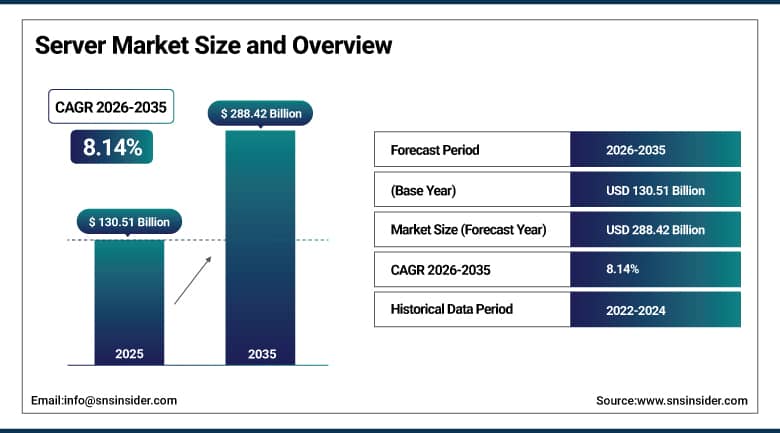

The Server Market was valued at USD 130.51 Billion in 2025 and is expected to reach USD 288.42 Billion by 2035, growing at a CAGR of 8.14% from 2026 to 2035.

The global server market is undergoing a period of dynamic transformation driven by the explosive growth of cloud computing, the rapid expansion of AI and machine learning workloads, the proliferation of edge computing architectures, and the extraordinary capital investment flowing into hyperscale data centre infrastructure. Servers are the foundational computing hardware underpinning virtually every digital service, enterprise application, cloud workload, and AI inference or training task across modern technology infrastructure.

In February 2025, Hewlett Packard Enterprise introduced its next generation ProLiant server family engineered for advanced security, AI automation, and higher performance across hybrid cloud environments. The ProLiant servers deliver cloud native experiences and intelligent operations through HPE GreenLake, incorporating integrated security silicon, AI driven workload optimisation, and energy efficiency improvements that address data centre operators’ dual mandate to maximise compute density while meeting sustainability commitments.

Market Size and Forecast

-

Market Size in 2026E: USD 141.13 Billion

-

Market Size by 2035: USD 288.42 Billion

-

CAGR: 8.14% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Server Market - Request Free Sample Report

Server Market Trends

-

Growing adoption of AI accelerator servers equipped with GPUs and custom AI chips is driving demand for high-performance computing infrastructure to support generative AI, machine learning, and advanced analytics workloads

-

Increasing implementation of Open Compute Project (OCP) server designs is enabling hyperscale data centers and enterprises to improve efficiency, reduce vendor dependence, and optimize infrastructure costs

-

Rising deployment of liquid cooling technologies is addressing the thermal management requirements of high-density AI and HPC servers, improving energy efficiency and system performance

-

Expansion of edge computing is driving demand for distributed server infrastructure that supports low-latency processing for 5G, industrial automation, smart retail, and real-time analytics applications

-

Growing adoption of ARM-based server processors is improving performance-per-watt efficiency and encouraging diversification beyond traditional x86 server architectures in cloud and enterprise environments

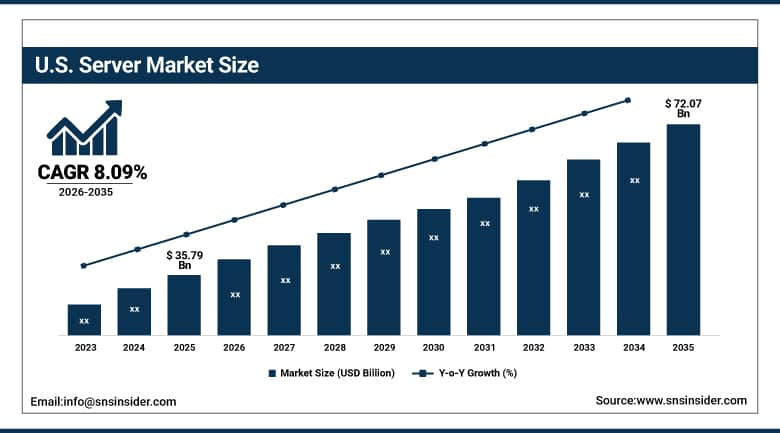

U.S. Server Market Outlook

The U.S. Server Market was valued at approximately USD 35.79 Billion in 2025 and is expected to reach approximately USD 72.07 Billion by 2035, growing at a CAGR of approximately 8.09%.

The U.S. is the world’s most commercially significant server market, hosting the global headquarters of Dell Technologies, Hewlett Packard Enterprise, IBM, Cisco Systems, Supermicro, and the hyperscale cloud providers whose combined server procurement defines global demand patterns. The extraordinary concentration of hyperscale data centre capacity in Northern Virginia, Phoenix, Dallas, Chicago, and the Pacific Northwest creates server procurement at a scale that no other geography can match. Federal government investment in digital infrastructure, AI computing for national security applications, and the enterprise sector’s systematic digital transformation create consistent structured procurement across all server product categories.

In September 2025, Dell Technologies introduced the PowerEdge XR8720T, a high performance server designed specifically for cloud radio access network deployments. The server delivers the computational power and low latency performance required for 5G infrastructure, enabling telecom operators to consolidate distributed radio unit processing in virtualised network functions that reduce infrastructure cost while improving network flexibility. The launch reflects the deepening intersection of the server and telecommunications infrastructure markets where 5G virtualisation creates substantial server procurement driven by network architecture transformation rather than conventional IT workload growth.

Server Market Segment Analysis

-

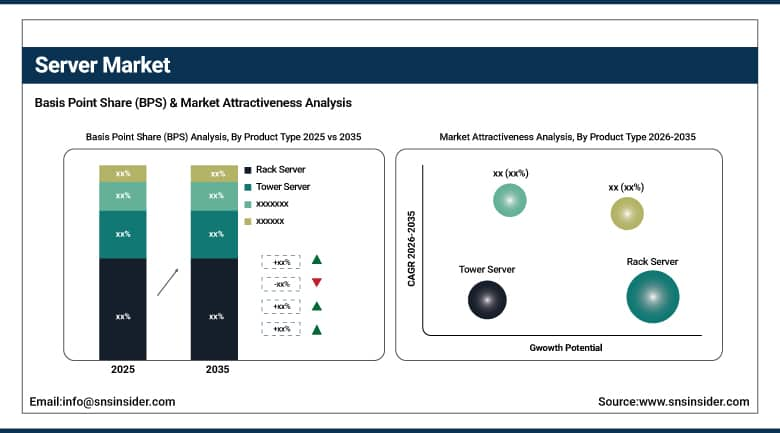

By Product Type, the Rack Server segment dominated the Server Market with approximately 51% share in 2025, while the Open Compute Project Server segment is the fastest growing.

-

By Channel, the Direct segment dominated the Server Market with approximately 44% share in 2025, while the Reseller segment is the fastest growing at a CAGR of approximately 9.77%.

-

By End Use, the IT & Telecom segment dominated the Server Market in 2025, while the BFSI segment is the fastest growing at approximately 10.71% CAGR.

By Product Type, rack servers dominate, OCP grows fastest

Rack servers retained the dominant product type position with approximately 51% of the server market in 2025. Their commercial primacy reflects the technology’s unmatched combination of versatility, density, and operational manageability that makes it the default server specification for data centres ranging from single rack enterprise deployments to hyperscale facilities housing tens of thousands of units. Rack servers’ modular design that allows independent CPU, memory, storage, and networking component specification creates procurement flexibility that tower and blade alternatives cannot match across diverse workload requirements. Each new data centre construction project, each capacity expansion at an existing facility, and each server refresh cycle creates rack server procurement as the statistically dominant product type whose installed base concentration sustains revenue leadership across forecast periods. Dell Technologies’ PowerEdge rack family, HPE’s ProLiant DL series, and Supermicro’s high density rack portfolio collectively define the commercial landscape.

Open Compute Project servers are the fastest growing product type because hyperscale operators’ convergence on open hardware standards, combined with large enterprise data centre operators’ adoption of OCP designs to eliminate proprietary vendor lock in, creates above average adoption growth across the most commercially significant server procurement categories. Each hyperscale operator that standardises on OCP server designs for a new data centre generation creates procurement at scale that sustains OCP ecosystem investment. Microsoft’s Project Olympus, Meta’s Open Rack standard, and Google’s participation in OCP collectively demonstrate the commercial commitment of the world’s largest server buyers to open hardware architectures.

By Channel, direct dominates, reseller grows fastest

The direct channel retained the dominant position with approximately 44% of the server market in 2025. Large enterprises’ preference for direct OEM engagement reflects the customisation requirement, performance guarantee, and long term support relationship that complex enterprise server deployments create. Each hyperscale cloud operator whose custom server specification requires direct engineering collaboration with OEM manufacturers creates direct channel procurement whose per order commercial value can represent hundreds of millions of dollars in annual commitments that no reseller channel alternative can service at equivalent capability. The direct channel’s ability to provide integrated technical support, rapid field service response, and configuration management at enterprise scale sustains its commercial dominance across the most valuable customer segments.

Resellers are the fastest growing channel at approximately 9.77% CAGR because SME digitalisation, regional market expansion in Asia Pacific and Latin America, and the bundled value added service model that resellers provide create above average procurement growth from customer segments that direct OEM engagement cannot efficiently serve. Each SME that purchases a server with bundled configuration, deployment, and support services from a trusted local reseller creates procurement that direct OEM channels’ minimum order and support model economics cannot accommodate profitably. Resellers’ ability to offer competitive pricing across multiple OEM brands, flexible financing, and localised technical support creates commercial advantages that sustain the channel’s fastest growing designation across the forecast period.

By End Use, IT & telecom dominates, BFSI grows fastest

IT and telecom retained the dominant end use position in 2025 through the enormous server deployment required to support cloud infrastructure, telecommunications network functions, and digital service platforms whose combined computing requirement represents the single largest server procurement category. Each cloud service provider that adds data centre capacity creates server procurement at extraordinary scale. Telecom operators’ 5G network virtualisation, whose replacement of proprietary network hardware with software running on commodity server platforms creates sustained procurement cycles, adds substantial commercial volume above conventional enterprise IT server demand. Content delivery networks, online gaming platforms, and streaming services whose continuous traffic growth creates consistent capacity addition requirements collectively sustain IT and telecom’s dominant end use position throughout the forecast period.

BFSI is the fastest growing end use at approximately 10.71% CAGR because the intersection of digital banking adoption, real time transaction processing requirements, regulatory compliance data management, and the extraordinary cybersecurity investment of financial institutions creates structured above average server procurement growth. Each financial institution that transitions from batch to real time core banking processing creates server infrastructure investment whose latency and availability requirements justify premium server configuration. Fintech platform growth and the digital banking competitive pressure on established institutions creates systematic IT modernisation investment that sustains BFSI server procurement growth above overall market average through the forecast period.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

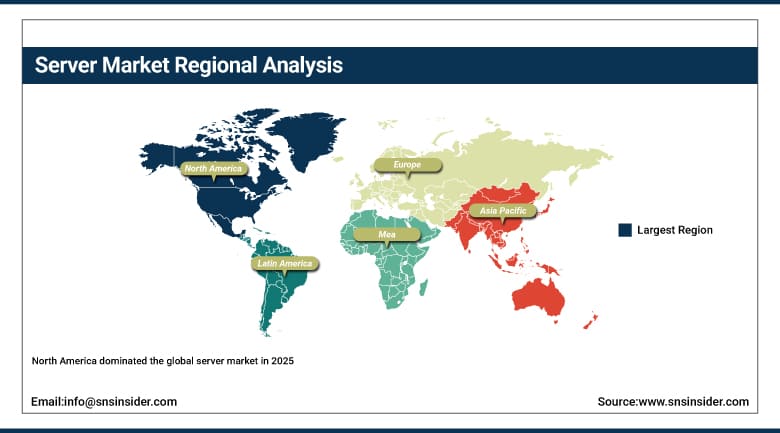

North America Server Market Insights

North America dominated the global server market in 2025, driven by advanced data centre infrastructure, the concentration of hyperscale cloud providers, early AI infrastructure adoption, and the presence of Dell Technologies, Hewlett Packard Enterprise, IBM, Cisco Systems, and Supermicro. The United States accounts for approximately 87.4% of North American revenues through its extraordinary hyperscale data centre investment concentration and enterprise IT spending scale.

Canada contributes approximately 12.6% of North American revenues through its growing data centre sector, the financial services industry’s server investment, and government digital transformation programmes that sustain consistent server procurement across federal and provincial agencies.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Server Market Insights

Europe is a technically sophisticated server market where the EU’s digital sovereignty initiative, data localisation requirements under GDPR, and the growing enterprise cloud adoption create consistent structured procurement. Germany accounts for approximately 22.3% of European revenues through its manufacturing industry’s digital transformation server investment, the financial sector’s infrastructure spending, and the hyperscale cloud provider data centre development in Frankfurt.

The United Kingdom, Netherlands, and France are significant secondary markets where London’s financial district server infrastructure, Amsterdam’s hyperscale data centre cluster, and Paris’s growing cloud region create consistent above average server procurement. Lenovo’s European operations and Fujitsu’s regional server division sustain complementary commercial supply.

Asia Pacific Server Market Insights

Asia Pacific is the fastest growing regional server market, driven by China’s extraordinary data centre construction investment, India’s digital infrastructure expansion, Japan’s enterprise IT modernisation, South Korea’s semiconductor and cloud sector growth, and Southeast Asia’s accelerating digital transformation. China accounts for approximately 44.8% of Asia Pacific revenues through Alibaba Cloud, Tencent, Baidu, and Huawei Cloud’s combined data centre investment whose server procurement scale rivals the largest Western hyperscale operators.

India represents the most commercially dynamic emerging server market within Asia Pacific where the government’s Digital India initiative, the extraordinary IT services export sector’s data centre investment, and the rapidly growing domestic cloud services market create above average server procurement growth that compounds with India’s digital economy expansion.

MEA & Latin America Server Market Insights

The UAE leads MEA revenues at approximately 31.2% through its hyperscale data centre investment at Dubai Internet City and Abu Dhabi’s emerging technology hub, Microsoft and Google’s UAE cloud region launches, and ADNOC’s high performance computing investment. Saudi Arabia’s NEOM smart city server infrastructure adds substantial complementary demand. Brazil leads Latin American revenues at approximately 44.2% through its hyperscale data centre development in Sao Paulo, the financial sector’s server investment, and AWS, Microsoft, and Google’s Brazilian cloud region expansion. Mexico’s IT sector and Colombia’s cloud adoption collectively sustain regional growth through 2035.

Market Dynamics

Growth Drivers: AI workload explosion and hyperscale data centre capacity expansion creating extraordinary server demand

The artificial intelligence workload explosion is the server market’s most commercially transformative structural growth driver, creating a premium GPU server market whose per unit commercial value is approximately 10 to 50 times that of conventional CPU servers. Each large language model training run, each AI inference deployment, and each enterprise AI application that requires dedicated GPU compute creates server procurement whose commercial scale compounds with the extraordinary pace of AI adoption across all industry verticals. NVIDIA’s H100 and H200 server allocation constraints through 2024 and 2025 demonstrated that AI GPU server demand significantly exceeded supply from the most commercially capable manufacturers, creating a demand backlog that sustains elevated revenue growth.

Hyperscale data centre capacity expansion programmes from Amazon Web Services, Microsoft Azure, Google Cloud, and Meta represent the most commercially certain long duration server demand driver whose multi year capital expenditure commitments create structured procurement pipelines that sustain consistent server OEM revenue independent of short term macroeconomic fluctuations. Microsoft’s USD 80 billion data centre investment commitment for fiscal year 2025 alone created server procurement at a scale that substantially elevates the entire market’s revenue growth trajectory.

Restraints: Supply chain constraints for advanced semiconductor components and data centre power availability limits

Supply chain constraints for advanced semiconductor components, particularly AI GPU processors, high bandwidth memory, and custom networking ASICs, create server production bottlenecks that limit the pace at which manufacturers can fulfil demand from hyperscale and enterprise customers. Each new GPU server product generation whose component supply is constrained by semiconductor fabrication capacity at TSMC creates procurement delays that moderate revenue recognition timing even when end customer demand substantially exceeds available supply.

Data centre power availability limits are becoming a binding constraint on server deployment growth in the most commercially significant markets. Northern Virginia’s Loudoun County, the world’s largest data centre market, has experienced power grid capacity constraints that delay new data centre energisation by 12 to 24 months, creating server deployment timing that moderates the pace at which procured servers can be commissioned into service and revenue generating operations.

Opportunities: Edge computing server deployment and sustainable liquid cooled server architecture

Edge computing server deployment represents the most geographically distributed near term server market expansion opportunity whose decentralisation of computing from centralised cloud to proximity locations creates server procurement across manufacturing facilities, retail locations, telecommunications network sites, and transportation infrastructure. Each 5G base station that adds mobile edge computing creates server procurement whose commercial aggregate across global 5G deployment sustains substantial incremental server demand beyond conventional data centre procurement.

Sustainable liquid cooled server architecture represents the most commercially premium near term product innovation opportunity whose immersion and direct liquid cooling technology enables the AI GPU server power densities that hyperscale AI infrastructure requires at economics that conventional air cooled alternatives cannot achieve. Each hyperscale operator that converts a data centre hall from air to liquid cooling creates a server replacement cycle whose liquid cooling compatibility requirement sustains premium server procurement and shortens effective refresh cycles.

Recent Developments:

-

2025: Hewlett Packard Enterprise introduced its next generation ProLiant server family in February 2025, engineered for advanced security, AI automation, and higher performance across hybrid cloud environments, delivering cloud native experiences and intelligent operations through HPE GreenLake.

-

2025: Dell Technologies introduced the PowerEdge XR8720T high performance server in September 2025 designed for cloud radio access network deployments, delivering computational power and low latency performance required for 5G infrastructure virtualisation at telecom operators.

-

2024: Supermicro expanded its liquid cooled AI server portfolio in 2024 with new direct liquid cooling configurations supporting NVIDIA H100 and H200 GPU clusters, targeting hyperscale AI training infrastructure operators requiring above standard thermal management for 10 kW per rack AI server deployments.

-

2024: Lenovo launched its ThinkSystem V3 server portfolio update in 2024 incorporating fourth generation Intel Xeon Scalable and AMD EPYC processor support with enhanced AI inference acceleration and improved energy efficiency for enterprise data centre and cloud service provider deployment.

-

2023: IBM launched its Power10 Scale Up server family in 2023 targeting mission critical enterprise workloads requiring the highest memory bandwidth, RAS characteristics, and database performance, reinforcing IBM’s BFSI and government sector server position against x86 incumbent competition.

Server Market Key Players

-

Dell Technologies Inc.

-

Hewlett Packard Enterprise Company

-

IBM Corporation

-

Cisco Systems Inc.

-

Lenovo Group Limited

-

Supermicro

-

Huawei Technologies Co. Ltd.

-

Inspur Electronic Information Industry Co. Ltd.

-

Oracle Corporation

-

Fujitsu Limited

-

ASUSTeK Computer Inc.

-

Gigabyte Technology Co. Ltd.

-

H3C Technologies Co. Ltd.

-

NEC Corporation

-

Hitachi Ltd.

-

Atos SE

-

SGI

-

Cray Inc.

-

QCT

-

Wiwynn Corporation

Server Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 130.51 Billion |

| Market Size by 2035 | USD 288.42 Billion |

| CAGR | CAGR of 8.14% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product Type (Rack Server, Blade Server, Tower Server, Micro Server, Open Compute Project Server) • by Channel (Direct, Reseller, Systems Integrator, Others) • by End Use (IT & Telecom, BFSI, Government & Defence, Healthcare, Energy & Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Dell Technologies Inc., Hewlett Packard Enterprise Company, IBM Corporation, Cisco Systems Inc., Lenovo Group Limited, Supermicro, Huawei Technologies Co. Ltd., Inspur Electronic Information Industry Co. Ltd., Oracle Corporation, Fujitsu Limited, ASUSTeK Computer Inc., Gigabyte Technology Co. Ltd., H3C Technologies Co. Ltd., NEC Corporation, Hitachi Ltd., Atos SE, SGI, Cray Inc., QCT, Wiwynn Corporation |

Frequently Asked Questions

The explosion of AI and machine learning workloads requiring GPU accelerated server platforms, and hyperscale data centre capacity expansion programmes from cloud providers committing tens of billions of dollars annually to infrastructure investment that creates the most commercially certain long duration server demand in the market’s history.

Rack Server dominated the Server Market with approximately 51% share in 2025, while the Open Compute Project Server segment is the fastest growing.

North America dominated the Server Market in 2025, while Asia Pacific is the fastest growing region driven by China’s hyperscale data centre construction and India’s digital infrastructure expansion.

Get in Touch