File Integrity Monitoring Market Report Scope & Overview:

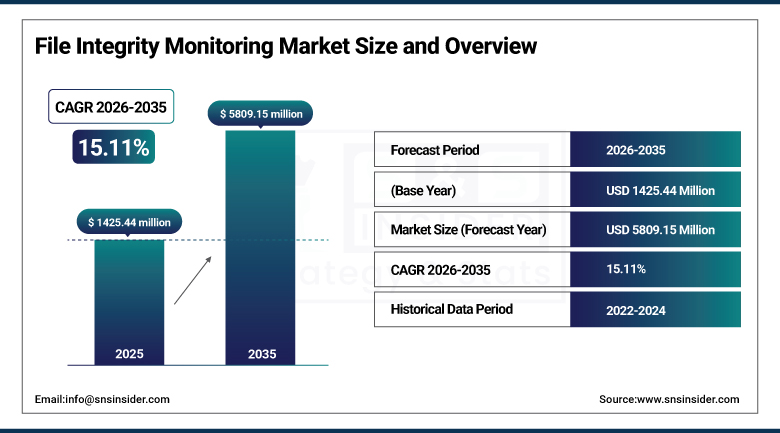

The File Integrity Monitoring Market was valued at USD 1,425.44 Million in 2025 and is expected to reach USD 5,809.15 Million by 2035, growing at a CAGR of 15.11% from 2026–2035.

The global file integrity monitoring market is experiencing exceptional growth driven by growing needs for real-time detection of threats, increasing adoption of FIM solutions as an integral part of cybersecurity strategies, and mounting regulatory compliance requirements that mandate file change auditing across critical infrastructure. File integrity monitoring solutions continuously audit and validate file states against established baselines, detecting unauthorized changes to operating system files, configuration files, application binaries, and sensitive data files that indicate malware infection, insider threat activity, or ransomware encryption in progress. FIM is a fundamental component of PCI DSS, HIPAA, SOX, GDPR, and NIST cybersecurity framework compliance whose mandatory control requirement creates structured procurement motivation across financial services, healthcare, government, and retail industries maintaining regulated data. The growing sophistication of supply chain attacks and zero-day exploits that evade perimeter security defenses creates above-average demand for host-based file change detection capability whose early threat identification prevents catastrophic breach impact.

In 2024, CrowdStrike expanded its Falcon platform with enhanced file integrity monitoring capabilities integrating AI-powered anomaly detection that distinguishes legitimate software updates from malicious file modifications using behavioral pattern analysis. The enhancement reflects the commercial direction of enterprise FIM toward AI-native monitoring platforms whose automated threat correlation eliminates the manual alert investigation burden that conventional change-detection-only FIM systems create when generating high-volume file change notifications from normal system activity.

Market Size and Forecast

-

Market Size in 2026E: USD 1,640.78 Million

-

Market Size by 2035: USD 5,809.15 Million

-

CAGR: 15.11% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on File Integrity Monitoring Market - Request Free Sample Report

File Integrity Monitoring Market Trends

-

AI-powered FIM solutions are improving threat detection accuracy by automatically distinguishing legitimate system changes from potentially malicious file modifications

-

Growing adoption of cloud-native infrastructure is driving demand for FIM platforms designed to monitor cloud workloads, containers, and dynamic computing environments

-

Agentless FIM deployments are gaining popularity as organizations seek simplified monitoring with lower system resource requirements and reduced management complexity

-

Integration of FIM capabilities into Extended Detection and Response (XDR) platforms is enabling more comprehensive threat visibility and streamlined security operations

-

Increasing implementation of zero trust security architectures is driving demand for continuous file integrity verification to ensure systems remain aligned with approved security baselines and compliance requirements

U.S. File Integrity Monitoring Market Outlook

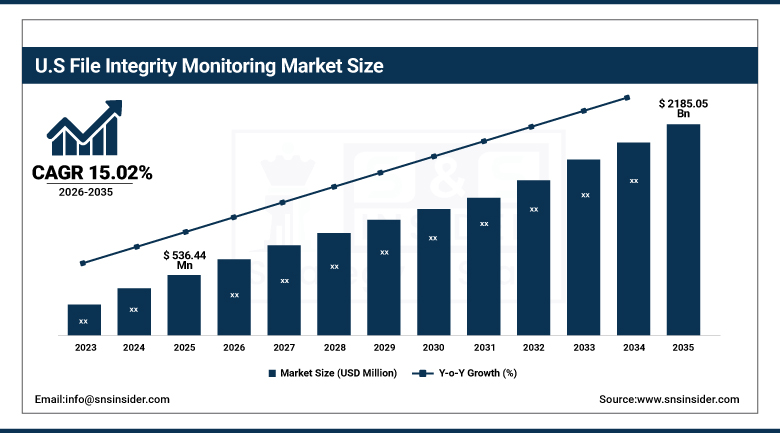

The U.S. File Integrity Monitoring Market was valued at approximately USD 536.44 Million in 2025 and is expected to reach approximately USD 2,185.05 Million by 2035, growing at a CAGR of approximately 15.02%.

The U.S. is the most commercially sophisticated file integrity monitoring market within North America's dominant revenue position. CrowdStrike, Qualys, Tripwire (HelpSystems), SolarWinds, and IBM Security define the domestic FIM commercial landscape whose combined portfolio covers enterprise, cloud, and compliance-focused FIM use cases. The U.S. financial services sector’s PCI DSS and SOX compliance requirements, the healthcare sector’s HIPAA security rule mandate, and the federal government’s FISMA and NIST cybersecurity framework requirements collectively create structured institutional FIM procurement across the most commercially concentrated regulated industry environment globally. The SEC’s cybersecurity incident disclosure rule effective December 2023 creates board-level security investment motivation that sustains FIM specification as a foundational threat detection capability.

In 2023, Qualys launched its VMDR-integrated File Integrity Monitoring module that combines vulnerability assessment with file change monitoring in a unified cloud platform, enabling security teams to correlate file changes with known vulnerability exploitation patterns and priorities response based on threat severity rather than treating every file change as an equivalent security event. The launch demonstrates the commercial evolution of FIM from standalone compliance checkboxes toward integrated security operations capabilities whose threat context enrichment creates investigation efficiency improvements measurable in mean-time-to-detect reduction.

File Integrity Monitoring Market Segment Analysis

-

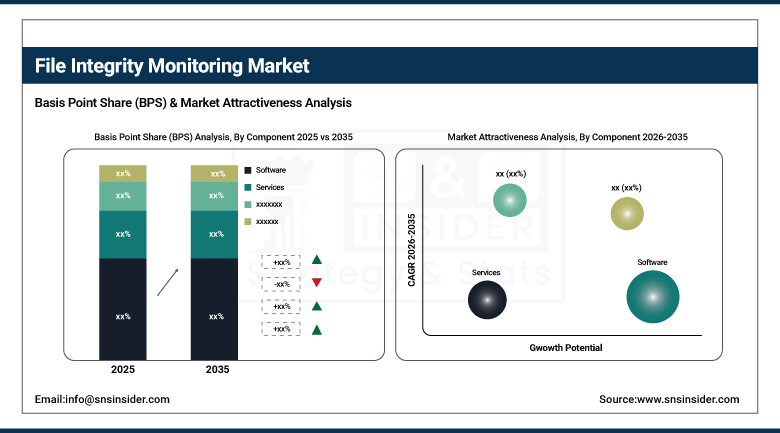

By Component, the Software segment dominated the File Integrity Monitoring Market with approximately 68% share in 2025, while the Services segment is the fastest growing.

-

By Installation, the Agent-based segment dominated the File Integrity Monitoring Market with approximately 62% share in 2025, while the Agentless segment is the fastest growing.

-

By Deployment, the Cloud segment dominated the File Integrity Monitoring Market with approximately 58% share in 2025, while the On-premise deployment segment is the fastest growing.

-

By End Use, the BFSI segment dominated the File Integrity Monitoring Market with approximately 26% share in 2025, while the Healthcare segment is the fastest growing.

By Component, software dominates, services grow fastest

Software retained the dominant component position with approximately 68% of the file integrity monitoring market in 2025. FIM software’s commercial primacy reflects the market’s fundamental purchase decision structure where the monitoring engine, alert management console, compliance reporting, and threat intelligence integration capabilities are delivered through software whose subscription or perpetual license procurement defines the primary commercial relationship. Each enterprise FIM software deployment creates a long-duration subscription relationship whose annual renewal, capability expansion, and user count growth sustains recurring revenue that compounds with the enterprise’s infrastructure scale. The integration of FIM software with SIEM, SOAR, and XDR platforms creates expanded deployment scope whose file change telemetry enriches enterprise security operations beyond standalone FIM use cases.

Services are the fastest-growing component because FIM implementation complexity, whose scope encompasses baseline establishment, policy tuning to reduce false positives, compliance framework mapping, and integration with existing security infrastructure, creates professional services demand that sustains multi-month engagement timelines per deployment. Managed FIM service adoption by resource-constrained organizations whose security teams lack FIM specialist expertise creates recurring managed service revenue whose commercial momentum compounds with the growing demand for outsourced security operations capability.

By Installation, agent-based dominates, agentless grows fastest

Agent-based FIM retained the dominant installation position with approximately 62% of the file integrity monitoring market in 2025. The installed endpoint agent’s real-time file change detection capability, whose kernel-level hooks can intercept file operations before they complete, creates detection latency that agentless alternatives monitoring file states through API polling cannot match. Each server whose FIM agent detects a malware-created file before the malware establishes persistence creates threat remediation opportunity whose time advantage directly translates into breach impact reduction. PCI DSS and HIPAA’s FIM control requirements’ expectation of real-time detection capability sustains agent-based specification across compliance-driven procurement.

Agentless FIM is the fastest-growing installation type because the enterprise infrastructure’s migration toward cloud workloads, containers, serverless functions, and IoT devices creates monitoring environments where agent installation either creates performance impact incompatible with resource-constrained devices or requires container image modification that DevSecOps workflows prefer to avoid. Each cloud workload running in ephemeral container environments creates agentless FIM demand whose API-based file state polling provides compliance-required change documentation without modifying the monitored workload.

By End Use, BFSI dominates, healthcare grows fastest

BFSI retained the dominant end-use position with approximately 26% of the file integrity monitoring market in 2025. The financial services sector’s commercial dominance reflects PCI DSS Requirement 11.5’s explicit mandate for file integrity monitoring as a cardholder data environment security control whose regulatory enforcement creates non-discretionary FIM procurement across payment processors, banks, and financial institutions handling credit card data. SOX’s IT general control requirements for financial reporting system integrity create additional FIM procurement motivation for public company finance system file monitoring. The financial sector’s above-average cybersecurity investment intensity creates premium FIM solution specification that sustains above-average per-organization commercial relationships.

Healthcare is the fastest-growing end use because the convergence of HIPAA Security Rule’s access control and audit control requirements for electronic PHI systems, the healthcare sector’s extraordinary ransomware exposure whose 2023 average ransom demand exceeded USD 1.5 million per healthcare incident, and the FDA’s medical device software integrity requirement collectively create structured and growing FIM procurement motivation. Each hospital network, health insurance company, and pharmaceutical manufacturer whose electronic PHI systems require HIPAA audit control compliance creates FIM procurement that compounds with the healthcare sector’s growing cybersecurity investment following high-profile ransomware incidents.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America File Integrity Monitoring Market Insights

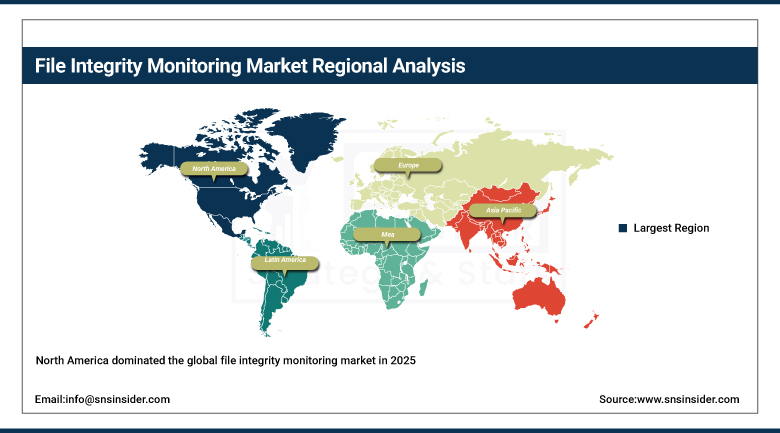

North America dominated the global file integrity monitoring market in 2025 through its stringent regulatory requirements including PCI DSS, HIPAA, SOX, and FISMA, high cybersecurity investment intensity, and the commercial presence of CrowdStrike, Qualys, Tripwire, SolarWinds, and IBM Security. The United States accounts for approximately 87.4% of North American revenues through its concentrated regulated industry investment and the SEC’s cybersecurity disclosure rule creating board-level security procurement motivation.

Canada contributes approximately 12.6% of North American revenues through its financial services sector’s PCI DSS compliance investment, the federal government’s cybersecurity framework, and the healthcare sector’s provincial health data security requirement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe File Integrity Monitoring Market Insights

Europe is a technically sophisticated FIM market where GDPR’s data protection requirements, NIS2 Directive’s expanded critical infrastructure cybersecurity mandate, and the financial sector’s EBA guidelines create structured regulatory FIM demand. Germany accounts for approximately 22.3% of European revenues through its financial services sector’s regulatory compliance investment, the industrial sector’s OT security programme, and BSI’s IT baseline protection catalogue FIM requirements.

The United Kingdom and France are significant secondary markets where NCSC guidance, financial regulatory compliance, and government critical infrastructure cybersecurity investment create consistent FIM demand.

Asia Pacific File Integrity Monitoring Market Insights

Asia Pacific is the fastest-growing regional FIM market, driven by China’s cybersecurity law compliance requirements, India’s Digital Personal Data Protection Act, Japan’s financial sector cybersecurity investment, and Southeast Asia’s growing financial services digitalization creating FIM demand. China accounts for approximately 44.8% of Asia Pacific revenues through its Cybersecurity Law’s critical information infrastructure protection requirements and the financial sector’s growing security compliance investment.

India represents the most commercially dynamic emerging market within Asia Pacific where the Digital Personal Data Protection Act’s data breach prevention requirements, the BFSI sector’s RBI cybersecurity framework, and the IT services industry’s security compliance investment create above-average FIM procurement growth.

MEA & Latin America File Integrity Monitoring Market Insights

UAE leads MEA revenues at approximately 38.4% through its financial sector’s CBUAE cybersecurity framework, the government’s critical infrastructure protection programme, and the growing technology sector’s security compliance investment. Brazil leads Latin American revenues at approximately 44.2% through its LGPD data protection law compliance, the financial sector’s BACEN cybersecurity resolution requirements, and the growing enterprise cybersecurity investment. Saudi Arabia’s NCA cybersecurity framework and South Africa’s POPIA data protection law create significant MEA secondary FIM demand sustaining regional market development through 2035.

Market Dynamics

Growth Drivers: Regulatory compliance mandates and ransomware threat elevation creating non-discretionary FIM procurement

Regulatory compliance mandates are the FIM market’s most commercially certain structural growth driver. PCI DSS 4.0’s enhanced file integrity monitoring requirements, HIPAA’s audit control mandate, SOX’s IT general control requirements, and NIS2 Directive’s expanded critical infrastructure security obligations collectively create legally mandated FIM procurement whose compliance motivation is independent of cybersecurity ROI calculation. Each regulatory standard revision that strengthens FIM requirements creates compliance upgrade procurement across the regulated industry’s installed base, creating procurement cycles that sustain market growth independently of new regulation adoption.

The ransomware threat landscape’s escalation, whose healthcare sector average demand exceeding USD 1.5 million per incident and critical infrastructure attacks creating national security implications, creates financial and reputational motivation for FIM investment that sustains premium solution specification. Each high-profile ransomware incident that demonstrates file encryption detection as the critical intervention point creates peer-organization FIM procurement motivation whose aggregate across industry sectors sustains market demand.

Restraints: High false positive rates in legacy FIM systems and integration complexity with existing security infrastructure

Legacy FIM systems’ high false positive alert rates, where normal system update and application patch activity generates thousands of file change notifications requiring manual investigation, create security operations team alert fatigue that reduces FIM monitoring effectiveness and moderates’ enterprise confidence in FIM solution investment value. Each security analyst hour spent investigating false positive FIM alerts creates operational cost that sustains pressure toward advanced AI-powered FIM alternatives whose machine learning classification reduces false positives.

Integration complexity between FIM solutions and existing SIEM, vulnerability management, and endpoint security platforms creates implementation engineering investment whose timeline and cost moderate the pace of FIM deployment across complex enterprise security infrastructures.

Opportunities: AI-powered FIM threat correlation and cloud workload FIM for DevSecOps

AI-powered FIM threat correlation represents the most commercially premium product direction whose ability to automatically classify file changes as authorized system updates or suspicious modifications, correlate FIM alerts with vulnerability exploitation patterns, and priorities investigation based on threat severity creates security operations efficiency improvement that sustains premium platform pricing. CrowdStrike’s 2024 AI-powered FIM enhancement and Qualys’s VMDR-integrated FIM demonstrate the commercial direction whose AI capability creates measurable detection quality improvement.

Cloud workload FIM for DevSecOps represents the most commercially dynamic emerging opportunity whose integration with CI/CD pipeline file integrity validation, container image verification, and infrastructure-as-code configuration integrity monitoring creates new FIM procurement categories that conventional on-premise FIM solutions cannot address.

Recent Developments:

-

2024: CrowdStrike expanded its Falcon platform with enhanced file integrity monitoring capabilities in 2024 integrating AI-powered anomaly detection that distinguishes legitimate software updates from malicious file modifications using behavioral pattern analysis.

-

2024: Tripwire (HelpSystems) launched its Tripwire Enterprise 9.1 with enhanced cloud integration and containerized environment FIM support in 2024, extending its established enterprise FIM platform to cover hybrid cloud and Kubernetes workload file integrity monitoring requirements.

-

2024: Qualys expanded its File Integrity Monitoring capabilities within the Cloud Agent platform in 2024 with new real-time file change detection for Linux and Windows cloud instances, enabling agentless-equivalent FIM coverage through the Qualys unified agent without separate FIM deployment.

-

2023: Qualys launched its VMDR-integrated File Integrity Monitoring module in 2023 that combines vulnerability assessment with file change monitoring in a unified cloud platform, enabling security teams to correlate file changes with known vulnerability exploitation patterns.

-

2023: IBM Security QRadar SIEM enhanced its FIM integration in 2023 with automated file change event correlation against threat intelligence feeds, enabling security analysts to immediately identify when file change patterns match known attack toolchains without manual threat intelligence lookup.

File Integrity Monitoring Market Key Players

-

CrowdStrike Holdings Inc.

-

Qualys Inc.

-

Tripwire Inc.

-

SolarWinds Corporation

-

IBM Security

-

Broadcom Inc.

-

McAfee Enterprise

-

Trend Micro Incorporated

-

LogRhythm Inc.

-

AlienVault

-

Netwrix Corporation

-

Varonis Systems Inc.

-

ManageEngine

-

Rapid7 Inc.

-

Tenable Holdings Inc.

-

Carbon Black

-

Illumio Inc.

-

Fortra LLC

-

NNT (Fortra)

-

FileAudit

File Integrity Monitoring Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,425.44 Million |

| Market Size by 2035 | USD 5,809.15 Million |

| CAGR | CAGR of 15.11% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Software, Services) • Installation (Agent-based, Agentless) • Deployment (Cloud, On-premise) • End Use (Healthcare, BFSI, Government, Retail, Telecom & IT, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | CrowdStrike Holdings Inc., Qualys Inc., Tripwire Inc. SolarWinds Corporation, IBM Security, Broadcom Inc., McAfee Enterprise, Trend Micro Incorporated, LogRhythm Inc., AlienVault, Netwrix Corporation, Varonis Systems Inc., ManageEngine, Rapid7 Inc., Tenable Holdings Inc., Carbon Black, Illumio Inc., Fortra LLC, NNT (Fortra), FileAudit |

Frequently Asked Questions

The File Integrity Monitoring Market is expected to grow at a CAGR of 15.11% from 2026 to 2035.

The File Integrity Monitoring Market was valued at USD 1,425.44 Million in 2025.

Regulatory compliance mandates including PCI DSS 4.0, HIPAA, SOX, and NIS2 creating legally mandated FIM procurement, and the ransomware threat landscape's escalation creating financial and reputational motivation for file change detection capability investment.

Software dominated the File Integrity Monitoring Market with approximately 68% share in 2025, while the Services segment is the fastest growing.

North America dominated the File Integrity Monitoring Market in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch