Service Bureau Market Report Scope & Overview:

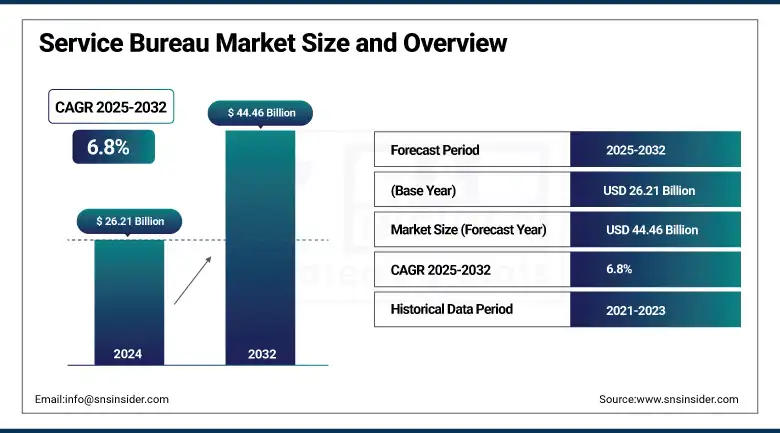

The Service Bureau Market Size was valued at USD 26.21 billion in 2024 and is expected to reach USD 44.46 billion by 2032 and grow at a CAGR of 6.8% over the forecast period 2025-2032.

The Service Bureau Market includes companies that provide outsourced services such as data processing, IT support, printing, and analytics to businesses in various industries. These service bureaus allow organizations to save on operational costs, improve the function of their processes, and gain access to specialized skills without the need to invest heavily in in-house infrastructure. Increasing digital transformation, cloud services adoption, and necessity for compliance and data security solutions to fuel the market growth. Healthcare, finance, and manufacturing are some of the key sectors that drive demand for AI systems in a sector that needs operational efficiency and regulatory compliance.

To Get more information On Service Bureau Market - Request Free Sample Report

According to a study, computer support specialists are expected to grow 6% between 2023 and 2033, which is faster than the average for all jobs. This increase accounts for about 62,740 job openings each year, due to the need to replace workers leaving the labor force and the growing demand for help desk services. Likewise, the professional, scientific, and technical services industry, which includes IT outsourcing, is expected to grow at 10.5% over the same period, more than twice the growth rate for total employment of 4.2%. All of these trends highlight how important service bureaus are for specialized IT and support functions.

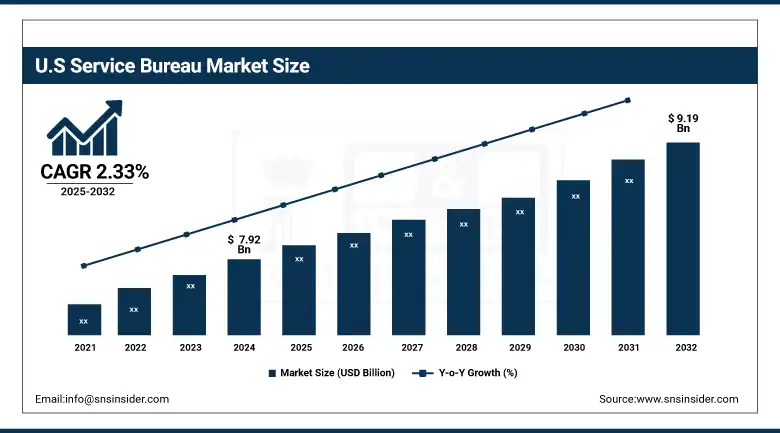

The U.S. Service Bureau Market size was USD 7.92 billion in 2024 and is expected to reach USD 9.19 billion by 2032, growing at a CAGR of 2.33% over the forecast period of 2025–2032. The rapid digital transformation across industries in the U.S. market has led to greater demand for outsourced IT, data processing, and compliance services. High technological infrastructure, high cloud computing adoption, and the presence of major service providers make the U.S. a high revenue-generating region in North America. These dynamics create a unique space for the U.S. to lead outsourcing solutions and managed services in the region.

Market Dynamics:

Key Drivers:

-

Increasing Global Demand for Outsourcing and Managed Services Drives the Growth of the Market

One of the primary drivers of the global service bureau market growth demand for outsourcing and managed services across industries globally. As companies strive to reduce operational costs and focus on core business areas, they increasingly delegate functions, such as data processing, IT support, payroll, and document management to a service bureau. The notable expansion of these trends in the Asia–Pacific and Latin America regions come from the fact that labor and technology adoption are generally cheaper in these regions compared to the East.

Likewise, big organizations also want to build lean operations across geographies and are finding service bureaus to be an efficient and centralized solution. In addition, both small businesses and corporations including service bureaus because they have scalable and customizable services. The global proliferation of digital business models, e-commerce, and work-from-home accelerates the need for flexible outsourced solutions even more. With companies across the world focusing on agility, efficiency, and digital transformation.

Restraints:

-

Lack of Standardization in Service Delivery Across Countries Restrains the market

A major restraint in the global Service Bureau Market is the lack of standardized service delivery models and regulatory frameworks across different regions. Unlike in the more regulated markets such as the U.S. and Europe, something that can dramatically taint the quality of services and compliance with laws and regulations, all of which impede transparency into the operations. This inconsistency affect multinationals that want the same level of service, data protection, and response time.

Furthermore, variations in labor laws, data privacy regulations, and technical infrastructure complicate service deployment and management. Clients may also face difficulties in enforcing contracts and ensuring accountability in regions with weaker legal enforcement. Such factors decrease the confidence that businesses have in moving mission-critical operations across borders and restrict global service bureaus from both penetrating and expanding in markets. Consequently, this non-standardization continues to be the primary barrier for smooth, international service bureau solution growth.

Opportunities:

-

Expanding Adoption of Digital Technologies in Emerging Economies Creates Substantial Growth Opportunities for the Market

The opportunities in the market is driven by the rapid digitalization of emerging economies. With most Asian-Pacific, African, and Latin American countries pumping money into IT infrastructure, cloud computing, and automation technologies, outsourced service solutions have a huge marketplace. With the rise of digitalisation among SMEs in those regions, they typically do not have the in-house expertise or a big budget to develop firm foundations for support systems. Additionally, given rising labor costs in some traditional outsourcing centers, providers are also looking at emerging regions as new places to diversify their portfolios. The digital upsurge in developing countries, along with budding entrepreneurship, makes the emerging economies a hotspot for future growth in the global Service Bureau Market.

Challenges:

-

Intense Global Competition and Pricing Pressure Pose a Critical Challenge for International Service Bureau Providers

The market expansion is challenged by the rising level of competition and pricing pressure across regions. With new players entering the market and established firms expanding their international presence, service providers are often forced to compete on cost rather than value-added services. This price-driven competition can erode profit margins, reduce service quality, and hinder investments in innovation.

Additionally, geopolitical risks, economic instability, and fluctuating foreign exchange rates make it difficult for global service bureaus to maintain consistent pricing models across different countries. The need to localize services while keeping costs under control further adds to operational complexity. Smaller firms may find it particularly difficult to compete against large global outsourcing companies with greater resources and scale.

Segmentation Analysis:

By Type

Data Processing Service Bureaus held the largest revenue share of 47% in 2024, driven by rising enterprise demand for efficient data management and automation. Industry adoption has been fueled by improved major offerings, such as the AI-Powered Data Services from IBM or Accenture Cloud-Native Processing Platforms. These improvements enable real-time analytics, regulatory compliance, and business intelligence. Due to growing volumes of data globally, this segment has remained a pillar of the service bureau market industry as it provides solutions for data-intensive industries, such as financial services, healthcare, and manufacturing, at a considerable scale and in a cost-effective, secure manner.

Payroll Service Bureaus are projected to grow at the highest CAGR of 12.05% during the forecast period, fueled by the rising need for automated, compliant payroll processing. Such enterprises as ADP, Paychex, and similar enterprises have unveiled a plethora of sophisticated AI-based platforms and mobile-ready services aimed at no-touch payroll, minimizing mistakes, and complying with the law. With the ever-increasing regulatory complexities and expansion of the global workforce, companies are forced to opt for outsourced payroll solutions.

By Industry

The Government segment held the largest revenue share of 28% in 2024, driven by increasing reliance on outsourced IT, data processing, and compliance management. Governments are collaborating with service bureaus for secure cloud migration & digitization. Examples of communications detailing these recent developments include those appearing from Accenture, through its public sector modernization tools, and CGI, through the delivery of advanced e-governance platforms. These efforts will ensure better citizen services and cybersecurity. As public agencies digitize operations, the demand for trusted, scalable service bureau solutions positions this segment as a dominant force in the market.

The Finance segment is projected to grow at the highest CAGR of 12.06% during the forecast period, fueled by the industry’s urgent need for secure, real-time data processing and regulatory compliance. Companies, such as ADP and FIS developed AI-embedded financial services platforms and global cloud-native solutions to serve banking and insurance organisations. The increasing use of fintech, complex reporting requirements, and demands for fraud prevention continue to compel financial institutions to utilize a service bureau, making this segment the fastest-growing component of the ever-evolving Service Bureau Market.

By Enterprise Size

The Medium-Sized Enterprises (100–499 employees) segment accounted for the largest revenue share of 35% in 2024, driven by its growing dependence on service bureaus to provide cheap IT, payroll, and data management. The enterprises provides scaled solutions for mid-size firms, without them having to spend on a complete in-house infrastructure. Such digital maturity and resource constraints classify this segment as a consistent revenue driver in the Service Bureau Market Outlook.

The Small Offices (1–9 employees) segment is projected to grow at the highest CAGR of 8.5% during the forecast period, as microbusinesses increasingly adopt outsourced services to improve efficiency without expanding headcount. The growth in this segment is indicative of the potential of the Service Bureau Market analysis in serving even the smaller business units across the globe, as rising entrepreneurial activity coupled with increased demand for low-cost, high-impact support drives the growth of this segment.

Regional Analysis:

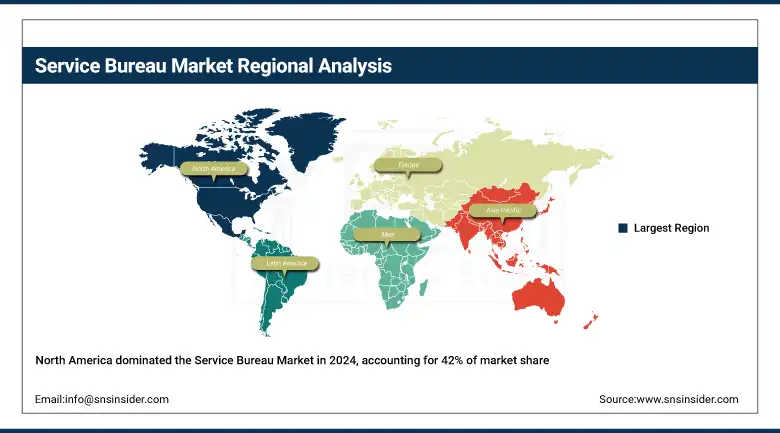

North America dominated the Market in 2024 with an Estimated Service Bureau Market Share of 42%. Market dominance is attributed to high digital transformation, modern IT infrastructure, and rising outsourcing trends in the target industries. The North American market is very much powered by the U.S., which has a very mature technology ecosystem, a large enterprise base, and a growing demand for specialized outsourced services. The country is called a leader in the Market due to government digital initiatives, cloud-first approaches, and massive implementation of AI by service delivery.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Region fastest fastest-growing region with an estimated CAGR of 12.11% in 2024. Rapid industrialization, increasing SME digitization, and low-cost service bureau offerings are propelling market growth in Asia-Pacific. Asia-Pacific Service Bureau Market is dominated by India, aided by an enormous IT human resource reservoir, lower service costs, and hyper-digital adoption among SMEs and enterprises. India is a preferred destination for service bureaus, based on government efforts including Digital India and growing global outsourcing demand across industry sectors.

In 2024, Europe showed a steady growth in the Service Bureau Market, with Germany holding the dominant share due to its advanced industrial base and ongoing digitalization in the manufacturing and finance sectors. Demand for streamlined outsourced service bureau solutions is being driven by Germany's robust manufacturing sector and emphasis on digital innovation. European firms are progressively offshoring information preparation, finance, and analysis to enhance consistency and diminishment costs. Further adoption is driven by the EU's attention to data protection (GDPR) and cloud computing.

The Middle East & Africa region is gradually emerging in the Service Bureau Market as governments push for digital transformation and smart services. The UAE leads regional growth due to strong investments in smart city initiatives, IT modernization, and paperless governance. Latin America’s Service Bureau Market Trends is expanding steadily, led by Brazil and Mexico. Brazil’s growing fintech sector, complex regulatory environment, and rising startup ecosystem create high demand for outsourced payroll and compliance services. Service bureaus are key for SMEs seeking operational efficiency.

Key Players:

The Service Bureau Market companies are Iron Mountain Incorporated, Ricoh Company, Ltd., Xerox Corporation, Canon Business Process Services, Exela Technologies, Inc., HP Inc., Konica Minolta, Inc., Kodak Alaris, ARC Document Solutions, Inc., Kyocera Document Solutions Inc., and others.

Recent Developments:

-

February 2025 – Iron Mountain reported significant growth across its global Records and Information Management (RIM), data center, and Asset Lifecycle Management (ALM) services. This performance highlights Iron Mountain’s expanded role in outsourced document and data management services, directly aligning with the Service Bureau Market.

-

January 2025 – Ricoh was named a Leader in the IDC MarketScape: Worldwide Cloud Managed Print and Document Services Vendor Assessment. This recognition underscores Ricoh’s leadership in cloud-based document services, supporting its influence in the evolving Service Bureau Market.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 26.21 Billion |

| Market Size by 2032 | USD 44.46 Billion |

| CAGR | CAGR of 6.8 % From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Data Processing Service Bureaus, Payroll Service Bureaus, Printing and Mailing Service Bureaus, IT Service Bureaus, Others) • By Enterprise Size (Small Offices [1–9 employees], Small Enterprises [10–99 employees], Medium-Sized Enterprises [100–499 employees], Large Enterprises [500–999 employees], Very Large Enterprises [1,000+ employees]) • By Industry Type (Finance, Healthcare, Retail, Manufacturing, Government, Education, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Taiwan, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Iron Mountain Incorporated, Ricoh Company, Ltd., Xerox Corporation, Canon Business Process Services, Exela Technologies, Inc., HP Inc., Konica Minolta, Inc., Kodak Alaris, ARC Document Solutions, Inc., Kyocera Document Solutions Inc., and Others |

Frequently Asked Questions

Ans: North America dominated the Service Bureau Market in 2024.

Ans: The Data Processing Service Bureaus segment dominated the Service Bureau Market.

Ans: The major growth factor of the Service Bureau Market is the increasing demand for cost-effective, outsourced digital and data processing services.

Ans: The Service Bureau Market size was USD 26.21 billion in 2024 and is expected to reach USD 44.46 billion by 2032.

Ans: The Service Bureau Market is expected to grow at a CAGR of 6.8% during 2025-2032.

Get in Touch