Shipping Container Market Report Scope & Overview:

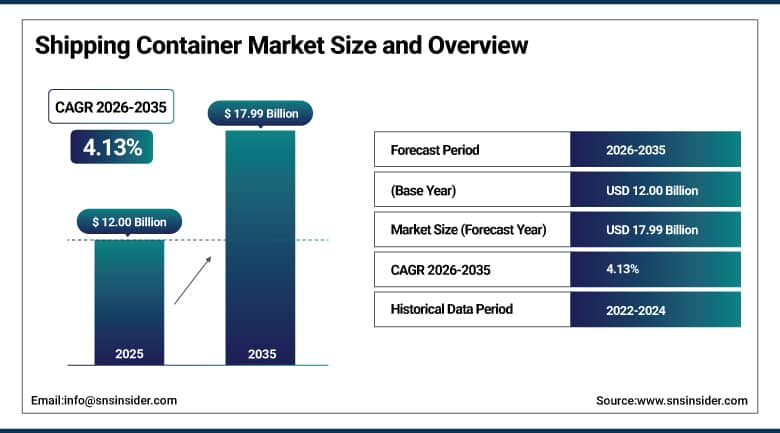

The Shipping Container Market was valued at USD 12.00 Billion in 2025 and is expected to reach USD 17.99 Billion by 2035, growing at a CAGR of 4.13% from 2026–2035.

The global shipping container market is a foundational component of world trade infrastructure. Standardised steel containers underpin approximately 90% of global maritime cargo movement, enabling the cost-effective, secure, and intermodal transport of manufactured goods, agricultural commodities, and industrial materials across thousands of trade routes. The market’s growth is driven by expanding global trade volumes, rising e-commerce cross-border shipments, and increasing investment in port infrastructure modernisation. Container manufacturers are investing in smart container technologies, lightweight materials, and AI-integrated tracking systems that improve fleet utilisation, cargo security, and supply chain visibility for shipping lines and logistics operators. The secondary container economy is also growing as retired containers are repurposed for modular construction, storage, and emergency housing, creating additional market activity beyond the primary manufacturing and leasing cycle.

In 2025, Hapag-Lloyd completed the rollout of smart real-time tracking devices across its entire combined dry and reefer container fleet of approximately 1.6 million units, establishing one of the world’s largest IoT-connected container fleets and demonstrating the commercial direction of intelligent container technology adoption by major shipping lines whose fleet visibility and predictive maintenance investments are becoming competitive differentiators in the global container logistics market.

Market Size and Forecast

-

Market Size in 2026E: USD 12.50 Billion

-

Market Size by 2035: USD 17.99 Billion

-

CAGR: 4.13% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get More Information On Shipping Container Market - Request Free Sample Report

Shipping Container Market Trends

-

Growing integration of IoT sensors and AI-driven tracking across global container fleets is improving real-time cargo visibility, predictive maintenance scheduling, and fleet utilisation rates for major shipping lines and leasing companies.

-

Rising demand for refrigerated containers driven by expanding global cold chain logistics for pharmaceuticals, perishable food, and temperature-sensitive cargo is creating above-average growth in the reefer container segment relative to standard dry freight alternatives.

-

Increasing adoption of high cube containers for e-commerce logistics is driven by the higher volumetric cargo density of packaged retail goods whose cube efficiency requirements favour the additional internal height that high cube formats provide over standard 40-foot containers.

-

Growing alternative use applications for retired shipping containers, including modular construction, portable storage, and emergency housing, are creating secondary market demand that extends the commercial lifecycle of container assets beyond their primary shipping service.

-

Expanding investment in port automation and intermodal logistics infrastructure across Asia Pacific, North America, and Europe is increasing container throughput efficiency and driving demand for standardised container formats compatible with automated handling systems.

U.S. Shipping Container Market Outlook

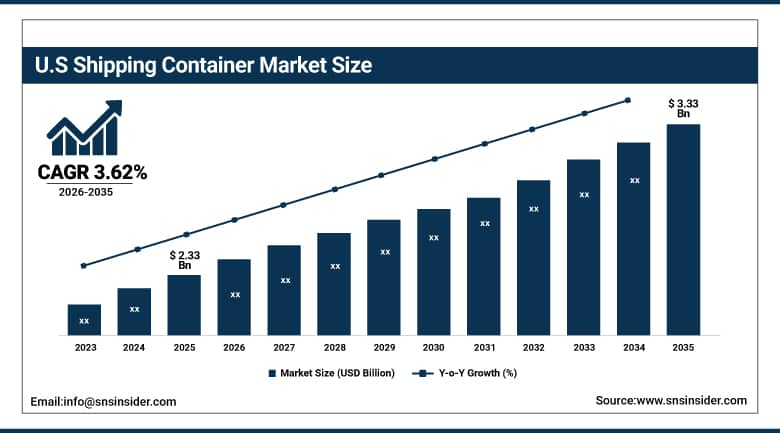

The U.S. Shipping Container Market was valued at approximately USD 2.33 Billion in 2025 and is expected to reach approximately USD 3.33 Billion by 2035, growing at a CAGR of approximately 3.62%.

The United States is a major participant in the global shipping container market both as the world’s largest import destination and as a significant node in the North American intermodal logistics network whose container handling volumes sustain substantial procurement and leasing activity across U.S.-flagged and internationally-operated container fleets. The U.S. market’s commercial dynamics are shaped by the volume asymmetry between inbound and outbound container flows, where the U.S.’s import-heavy trade balance creates structural demand for container repositioning that sustains leasing market activity across the Pacific trade lane. Major port infrastructure investment programmes at the Port of Los Angeles, Port of Long Beach, and East Coast ports including Port of New York and New Jersey are expanding container handling capacity and implementing automated stacking crane and truck appointment systems that improve throughput efficiency and reduce container dwell times.

CMA CGM’s March 2025 announcement of a USD 20 billion four-year investment programme to upgrade U.S. maritime infrastructure reflects the commercial significance that major global carriers assign to U.S. port capacity development for their long-term service competitiveness on the world’s highest-volume trade routes.

Shipping Container Market Segment Analysis

-

By Container Type, Dry Containers led the market with approximately 45.8% share in 2025 due to their versatility, robustness, and widespread use in transporting non-perishable goods across virtually all general cargo trade routes; Refrigerated Containers are the fastest-growing segment at a CAGR of approximately 6.2%.

-

By Container Size, 20-Foot containers led the market in 2025 as the most widely used standard shipping unit whose TEU-based measurement defines global container fleet capacity accounting and whose compact dimensions make them suitable for a broader range of cargo types, port facilities, and intermodal transport configurations; High Cube containers are the fastest-growing size segment.

-

By Ownership, Leasing dominated the shipping container market in 2025 as shipping lines and logistics operators prefer to lease containers to manage fleet size flexibility, reduce capital expenditure, and maintain asset utilisation rates during trade cycle fluctuations; Owned containers are growing as major shipping lines with strong balance sheets invest in owned fleet expansion to reduce long-term leasing costs on high-volume, predictable trade routes.

-

By End Use, Sea Freight dominated the shipping container market in 2025 as the primary commercial purpose for which standardised containers were designed and for which global shipping line fleets are almost entirely deployed; Intermodal Logistics is the fastest-growing end use.

By Container Type, dry containers dominate, refrigerated grows fastest

Dry containers retained the dominant container type position with approximately 45.8% of the shipping container market in 2025, reflecting their role as the universal standard for general cargo trade whose versatility across manufactured goods, consumer products, industrial components, building materials, and agricultural commodities makes them applicable to the broadest range of trade lanes and cargo categories of any container type. The dry container segment’s market leadership is structurally sustained by the composition of global trade, where the majority of containerised cargo by volume and value is non-perishable general merchandise whose packaging and handling characteristics are well-suited to the standard dry container’s-controlled environment and cargo securing provisions. CIMC’s dominant position in dry container manufacturing, with approximately 30% global market share, reflects the commercial scale advantages that the world’s largest container manufacturer achieves through vertically integrated steel sourcing, standardised production processes, and global customer relationships with major shipping lines whose fleet procurement contracts create predictable manufacturing volume at the scale that sustains CIMC’s cost leadership in the global container manufacturing market.

Refrigerated containers are the fastest-growing segment at a CAGR of approximately 6.2% through 2033, propelled by the expansion of global cold chain logistics networks that are serving the growing international trade in temperature-sensitive cargo including fresh and frozen food, pharmaceutical products, vaccines, and biotechnology materials whose handling requirements demand the consistent temperature control that reefer container technology provides regardless of ambient conditions along the maritime route. CIMC’s 2024 launch of the Smart Reefer 2.0 with AI-driven temperature and humidity control reducing energy consumption by up to 18%, and Maersk Container Industry’s RCM 3.0 cloud-based remote container management platform for refrigerated containers, collectively demonstrate the technology investment acceleration that is simultaneously improving reefer container performance and reducing operational cost, making the cold chain logistics value proposition more commercially compelling for shippers across the pharmaceutical and perishable food categories whose trade volumes are growing fastest.

By End Use, sea freight dominates, intermodal logistics grows fastest

Sea freight retained the dominant end use position in the shipping container market in 2025, representing the foundational commercial purpose of the standardised container ecosystem whose design, dimensions, and handling specifications have been optimised over six decades of global maritime trade to enable the efficient ship loading, stowage, and discharge operations that define the commercial productivity of containerised shipping. The sea freight end use encompasses the full spectrum of containerised maritime trade from trans-Pacific and trans-Atlantic major lane operations through intra-Asian feeder services to emerging trade corridors between Southeast Asia, Africa, and Latin America whose growing manufacturing and consumer goods trade volumes are progressively joining the global container shipping network. Major shipping line investment in new vessel capacity including Evergreen’s November 2024 order of 60,500 new containers, ZIM’s USD 2.3 billion fleet expansion commitment in May 2025, and DP World’s USD 1.3 billion London Gateway expansion with two fully electric berths announced in March 2025 collectively demonstrate the sustained capital investment that global maritime trade growth is generating across the container shipping ecosystem.

Intermodal logistics is the fastest-growing end use in the shipping container market, driven by the progressive development of inland container transportation networks that extend the container’s utility beyond the port-to-port maritime journey into integrated multimodal supply chains that use rail and road transport to move loaded containers directly from origin production facilities to destination distribution centres without intermediate transloading of cargo. The intermodal growth is particularly commercially significant in North America where the double-stack rail network’s expansion enables cost-effective container movement between Pacific gateway ports and interior distribution markets, in Europe where rail freight corridors are progressively extending containerisation into Central and Eastern European manufacturing regions, and in Asia Pacific where the China-Europe rail network and Southeast Asian rail investment programmes are creating new inland container connectivity that supplements maritime trade lane capacity.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Shipping Container Market Insights

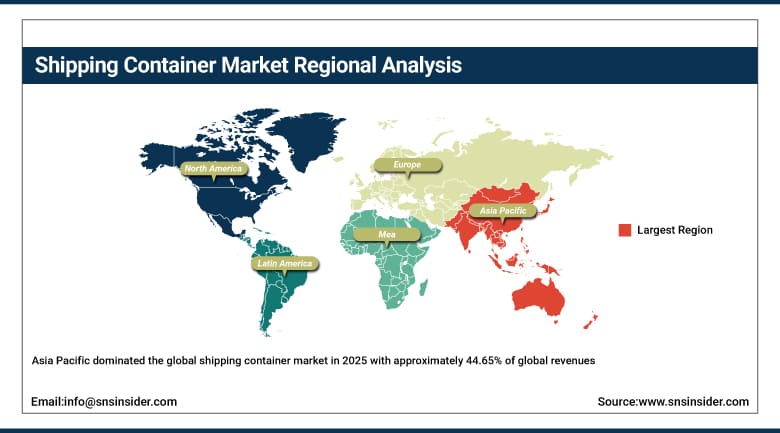

Asia Pacific dominated the global shipping container market in 2025 with approximately 44.65% of global revenues, a commercial leadership reflecting the region’s unparalleled concentration of container manufacturing capacity, export manufacturing activity, and port throughput that collectively define the global container industry’s operational centre of gravity. China accounts for approximately 61.7% of Asia Pacific revenues through the world’s largest concentration of container manufacturers, led by CIMC, CXIC Group, Dong Fang International Container, and Singamas, whose combined output represents approximately 85 to 90% of global new container production annually. China’s manufacturing and export sector simultaneously generates the world’s largest single-country demand for export container capacity, creating a domestic market context where manufacturing supply and trade demand both reinforce the container industry’s Asia Pacific dominance.

Japan, South Korea, Taiwan, and the ASEAN economies contribute secondary Asia Pacific container market activity through their significant manufacturing export sectors, major port operations, and growing intra-regional trade, whose container throughput volumes are expanding as regional supply chains become more integrated and as Southeast Asian manufacturing growth displaces some production from higher-cost East Asian locations. The Asia Pacific container leasing market is also substantial, with major leasing companies including Triton International, Textainer, and Seaco maintaining large container fleets that are deployed primarily on trans-Pacific and intra-Asian trade routes whose lease rates and fleet utilisation levels directly influence the commercial performance of the global container leasing industry.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Shipping Container Market Insights

North America is the fastest-growing regional shipping container market, with the United States accounting for approximately 87.4% of North American revenues through the world’s largest single-country import market whose container demand is driven by the volume and value of consumer goods, industrial components, and agricultural imports that sustain the U.S. economy’s trade-dependent supply chains. The U.S. market’s above-average growth rate reflects accelerating port infrastructure investment, the intermodal logistics network’s expansion into new inland markets, and the increasing adoption of container-based domestic storage and alternative use applications that are creating secondary demand beyond the primary maritime trade channel. Canada contributes approximately 12.6% of North American revenues through its role as both a significant container import and export market, particularly for resource commodities and manufactured goods, and as a participant in the continental intermodal logistics network that moves containers between U.S. and Canadian production and consumption regions.

Europe Shipping Container Market Insights

Europe is a sophisticated shipping container market characterised by advanced port infrastructure in Rotterdam, Hamburg, Antwerp, and Felixstowe, a well-developed intermodal logistics network connecting major seaports to Central and Eastern European manufacturing and distribution regions, and growing regulatory pressure for decarbonisation of maritime logistics that is influencing container design, fleet management, and port operations. Germany accounts for approximately 22.3% of European revenues as the region’s largest national market, anchored by its position as Europe’s largest manufacturing export economy whose export container demand sustains significant freight volumes through Hamburg and Bremerhaven, the country’s primary container gateway ports. The European container market is also at the forefront of the container technology sustainability agenda, with CIMC and Maersk Container Industry’s joint initiative to produce 200,000 TEUs using steel with 50% less embodied carbon by 2027 directly responding to European shipping line and regulatory sustainability requirements.

MEA & Latin America Shipping Container Market Insights

The Middle East and Africa and Latin America are growing shipping container markets where expanding manufacturing export activity, commodity trade growth, and port infrastructure investment are increasing container throughput and procurement demand. Saudi Arabia leads Middle East and Africa container revenues at approximately 38.4% of the regional total through its position as the region’s largest trade hub, with the King Abdullah Port and Jeddah Islamic Port collectively handling substantial container volumes for both Saudi imports and regional transshipment. Ocean Network Express’ December 2025 acquisition of a minority stake in the Dalian Container Terminal to gain access to a Northeast China hub with 6.6 million TEU capacity signals the strategic container infrastructure investment that global shipping lines are making to secure throughput access at high-growth container handling facilities. Brazil leads Latin American revenues at approximately 44.2% of the regional total through the scale of its agricultural export sector, its manufacturing import demand, and the development of expanded container terminal infrastructure at Santos, the region’s largest container port.

Market Dynamics

Growth Drivers: Expanding global trade volumes and e-commerce cross-border shipments driving container demand, rising cold chain logistics investment increasing reefer container procurement

The primary structural growth driver for the shipping container market is the sustained expansion of global trade whose volume growth generates consistent demand for new container procurement and fleet capacity maintenance. E-commerce’s rapid growth as a cross-border retail channel is creating above-average incremental container demand as international parcel and packaged consumer goods shipments require containerised air and sea freight capacity at rates that grow faster than bulk commodity trade. Cold chain logistics investment driven by the globalisation of food supply chains and pharmaceutical trade is simultaneously creating specific demand for the higher-value refrigerated container segment whose growth rate exceeds the overall market average. Port infrastructure investment across Asia Pacific, North America, and the Middle East is expanding container handling throughput capacity and improving the operational efficiency that sustains container fleet utilisation economics.

Restraints: Volatility in steel prices affecting container manufacturing cost, trade cycle fluctuations creating demand variability, and geopolitical trade tensions creating route and volume uncertainty

Container manufacturing economics are significantly affected by steel price volatility, as steel represents approximately 75 to 80% of a standard container’s production cost and its price movements directly translate into new container price fluctuations that affect both manufacturer margins and leasing rate economics. Geopolitical trade tensions including tariff disputes, shipping lane disruptions, and sanctions create route and volume uncertainty that affects container demand forecasting and fleet investment planning for both manufacturers and leasing companies whose multi-year asset investment horizons require relative stability in trade flow assumptions to justify capital deployment decisions.

Opportunities: Smart container IoT technology improving fleet utilisation and cargo visibility, container repurposing economy creating secondary market demand, and emerging trade corridors in South Asia and Africa creating new container procurement markets

The smart container technology opportunity represents a commercially significant product innovation pathway for container manufacturers whose IoT-integrated tracking, condition monitoring, and AI-driven temperature management capabilities are commanding premium pricing in the refrigerated and specialised container segments while progressively becoming standard specifications in the dry container market as shipping lines increasingly require real-time visibility across their entire owned and leased fleets. The container repurposing market for modular construction, retail pop-up installations, data centre cooling, and emergency infrastructure is creating a growing secondary demand category whose commercial activity is extending the revenue lifecycle of container assets beyond their primary shipping service and creating a new application market for container manufacturers capable of producing purpose-designed containers for non-maritime applications.

Recent Developments:

-

2025: Hapag-Lloyd achieved its goal of equipping its entire combined dry and reefer container fleet of approximately 1.6 million units with smart real-time tracking devices, establishing one of the world’s largest IoT-connected container fleets and demonstrating the commercial viability of fleet-wide intelligent container technology deployment at scale.

-

2025: CMA CGM announced a USD 20 billion four-year investment programme to upgrade United States maritime infrastructure, including terminal capacity expansion, vessel efficiency improvement, and digital logistics integration that positions the company for sustained volume growth on the trans-Atlantic and trans-Pacific trade lanes that represent its highest commercial priority routes.

-

2025: DP World began a USD 1.3 billion expansion at London Gateway in March 2025, introducing two fully electric berths that represent one of the most significant port electrification investments in European maritime infrastructure and demonstrate the commercial commitment of major port operators to decarbonisation of container handling operations.

-

2025: October 2025 saw India launch the Bharat Container Shipping Line with an initial fleet of 51 ships and a USD 6.9 billion government investment, creating a national container carrier intended to reduce India’s dependence on foreign shipping lines for its rapidly growing export and import container trade volumes.

-

2024: CIMC launched the Smart Reefer 2.0 refrigerated container featuring AI-driven temperature and humidity control that reduces energy consumption by up to 18%, and Maersk Container Industry launched RCM 3.0, a major cloud-based Remote Container Management platform upgrade that improves real-time monitoring and predictive maintenance for reefer container fleets globally.

Shipping Container Market Key Players

-

China International Marine Containers Co. Ltd. (CIMC)

-

Maersk Container Industry A/S

-

Singamas Container Holdings Ltd.

-

CXIC Group Containers Co., Ltd.

-

Dong Fang International Container (Hong Kong) Co., Ltd.

-

Triton International Limited

-

Textainer Group Holdings Ltd.

-

Seaco Global Ltd.

-

Hapag-Lloyd AG

-

Mediterranean Shipping Company (MSC)

-

CMA CGM SA

-

Evergreen Marine Corporation

-

Ocean Network Express (ONE)

-

ZIM Integrated Shipping Services

-

Sea Box Inc.

-

CARU Containers B.V.

-

Storstac Inc.

-

China Eastern Containers Co., Ltd.

-

BSL Containers Ltd.

-

W&K Container Inc.

Shipping Container Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.00 Billion |

| Market Size by 2035 | USD 17.99 Billion |

| CAGR | CAGR of 4.13% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Container Type (Dry Containers, Refrigerated Containers, Tank Containers, Open Top Containers, Others) • By Container Size (20-Foot, 40-Foot, High Cube Containers, Others) • By Ownership (Leasing, Owned) • By End Use (Sea Freight, Intermodal Logistics, Storage, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | China International Marine Containers Co. Ltd. (CIMC), Maersk Container Industry A/S, Singamas Container Holdings Ltd., CXIC Group Containers Co., Ltd., Dong Fang International Container (Hong Kong) Co., Ltd., Triton International Limited, Textainer Group Holdings Ltd., Seaco Global Ltd., Hapag-Lloyd AG, Mediterranean Shipping Company (MSC), CMA CGM SA, Evergreen Marine Corporation, Ocean Network Express (ONE), ZIM Integrated Shipping Services, Sea Box Inc., CARU Containers B.V., Storstac Inc., China Eastern Containers Co., Ltd., BSL Containers Ltd., W&K Container Inc. |

Get in Touch