Silicon Photonics Market Size Analysis:

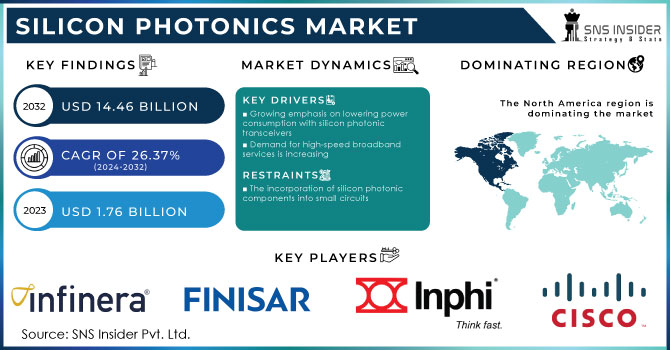

The Silicon Photonics Market size is expected to be valued at USD 1.76 Billion in 2023. It is estimated to reach USD 14.46 Billion by 2032, growing at a CAGR of 26.37% during 2024-2032.

The Silicon Photonics Market is witnessing significant growth on the back of technological advancements and an increasing need for high-speed data transfer. Due to the increasing popularity of cloud computing, big data, and the Internet of Things (IoT), data centers must now manage large volumes of data quickly. The exponential rise in data traffic is a major factor fueling the growth of the silicon photonics market. Silicon photonics provides a high-bandwidth optical communication solution on silicon chips, which can boost the performance of data centers and telecommunications infrastructure. In the year 2023, there was a significant rise in worldwide data usage due to different technological progress and changes in digital consumption trends. Global IP traffic reached around 6.7 zettabytes (ZB) at the end of the year, showing a 26% rise from the previous year's 5.3 ZB. There was a significant surge in mobile data traffic, with a 26% increase, totaling about 109 exabytes (EB) monthly.

Silicon Photonics Market Size and Forecast

-

Market Size in 2023: USD 1.76 Billion

-

Market Size by 2032: USD 14.46 Billion

-

CAGR: 26.37% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2023

Get More Information on Silicon Photonics Market - Request Sample Report

Silicon Photonics Market Trends (with Stats):

-

Surging data center traffic is accelerating adoption of silicon photonics for high-speed interconnects, with over 70% of hyperscale data centers transitioning to optical links above 400G.

-

Rising deployment of AI and HPC workloads is driving demand for low-latency optical transceivers, improving bandwidth density by 40–50% compared to traditional copper interconnects.

-

Expansion of 5G and edge networks is increasing need for high-speed optical modules, with telecom optical port shipments growing at over 18% annually.

-

Integration of photonics with CMOS fabrication is reducing production costs by 30–40%, enabling scalable mass manufacturing.

-

Growing use in sensing, LiDAR, and biomedical applications is expanding market scope, with non-data-com applications projected to grow at a CAGR above 20%.

Silicon photonics is used in the telecommunications industry to develop optical transceivers and modulators for data transmission that is faster and more efficient over long distances. This has become necessary to meet the increasing demand for higher access speeds of the internet and other access systems. Apart from this, owing to decreased consumption of power and reduced cost when compared to the conventional methods of telecommunication, telecom operators have started adopting silicon photonics technology. The Bipartisan Infrastructure Law has allotted USD 65 billion for upgrading the broadband infrastructure throughout the United States. This law has included the Broadband Equity, Access, and Deployment (BEAD) Program as one of the main projects and has allotted USD 42.45 billion to the states and territories to expand broadband access. Apart from these, the Digital Equity Act has allotted USD 2.75 billion to achieve digital equity and USD 1.44 billion has been made available to build state capacity for addressing the digital divide.

Silicon Photonics Market Dynamics:

Drivers

-

Growing emphasis on lowering power consumption with silicon photonic transceivers

The need to reduce power consumption continues to drive the silicon photonics market. This trend is mostly prominent in the development and outfitting of silicon photonic transceivers. In practical terms, with data centers and telecommunication networks continuing to grow and meeting the demand for higher data rates and bandwidth sizes, the performance pressure is growing. Additionally, the equipment must be energy-efficient to address sustainability considerations, attracting a higher demand for such devices. In this context, silicon photonic transceivers provide a clear benefit since they use the natural power advantage of silicon-based optical equipment to transmit data faster and with less power waste compared to traditional electronic transceivers.

-

Demand for high-speed broadband services is increasing

The market for silicon photonics is booming due to the increasing demand for ultra-fast broadband services. As the demand for data is growing at a rapid pace across the globe, high-speed internet has become the need of the hour. With the prevalent use of cloud services, streaming platforms, and other online services, the demand for data transmission services has surged. In addition, the rapid increase in smartphone and portable device users is making it tougher for traditional copper-based networks to withstand the data consumption demands. The older networks are restricted by their limitations in terms of both bandwidth and distance. However, silicon photonics technology is providing the ultimate solutions to the growing demand for data with its capability of data transmission over larger distances and that too at high speeds. In addition, the technology is highly sustainable as it uses photonic technology to transmit the data. The telecommunication companies across the globe are striving to implement silicon photonics technology to improve their network infrastructure and provide highly efficient ultra-fast broadband services.

Restraints

-

The incorporation of silicon photonic components into small circuits

Although silicon photonics technology is promising for faster data transfer and enhanced performance, it faces serious issues with further integrating optical components into small chips. The main problem arises from the inherent size mismatch of classical electronic elements and usually much larger photonic devices. Their alignment requires substantial engineering and extremely high-quality manufacturing, which is costly and complex. Moreover, silicon is not very efficient as a light source, so lasers also cannot be put on silicon chips. This prevents efficient coupling of mont silicon circuits with lasers, let alone processing the laser on the same chip. Proper location of the circuit in relation to the laser requires appropriate packaging, which adds to the cost. Consequently, it is quite difficult to introduce silicon photonic circuitry at the scale of miniaturized low-cost consumer electronics, thus limiting the growth of the market concerning small highly demanded devices.

Silicon Photonics Market Segment Overview:

By Product

The active optical cables segment dominated in 2023 with a market share of over 35%. These cables facilitate a high volume of data transfer to a great distance as compared to copper cables. They minimize the cost of integration concerning traditional optical modules. In addition, these cables are also anticipated to provide streamlined installation processes for HPC projects and data centers, along with other storage applications.

The optical multiplexer segment is anticipated to grow with the fastest CAGR during the forecast period. As the optical multiplexer is crucial for WDM systems, it enables different wavelengths to transfer the data over an optical fiber, thereby reducing the congestion of fibers required in such devices. In addition, the optical multiplexers enable the integration of multiple channel counts, compressing the chip design with minimal power loss. Hence, the advancement in multiplexers aids in enhancing the capacity and efficiency of optical communication systems throughout the forecast period.

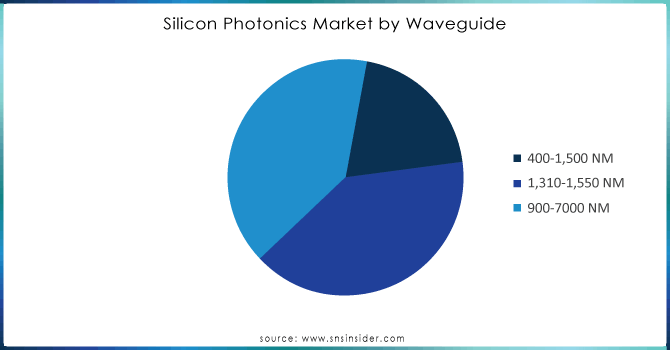

By Waveguide

The 1,310-1,550 NM led the market in 2023 with a market share of over 40%, as the range is widely used in telecommunications and data center applications because it offers optimal performance for long-distance data transmission with minimal attenuation. These wavelengths are ideal for fiber optic communications, which is a major application area for silicon photonics technology. The 1,310-1,550 NM range is also witnessing rapid growth due to increasing demand for high-speed data communication, cloud computing, and data centers. The expansion of internet infrastructure and the rise of 5G networks are further driving this growth. Additionally, advancements in silicon photonics technology are enhancing the performance and cost-effectiveness of devices operating in this wavelength range.

Get Customized Report as per your Business Requirement - Request For Customized Report

Silicon Photonics Market Regional Analysis:

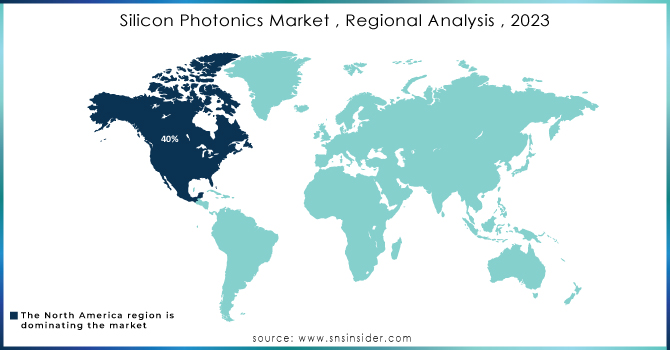

North America held a major market share of around 40% in 2023. Increased investments by the Canadian government in SiPh chip provider, One Silicon Chip Photonics will also fuel market growth in the region. This, in turn, would result in the development of technology that would speed up driverless cars and drones. Furthermore, during the forecast period, the product demand is also driven by the presence of a large number of silicon photonics technology providers in countries, such as the U.S. and Canada.

Asia Pacific is expected to see the highest CAGR during the forecast period 2024-2032. Increased no of 5G users and the expanded use of smartphones and other smart devices in countries including China, India, and Japan would be one of the prominent factors propelling the product demand. The huge volumes of data are increasing in the region on account of substantial network capabilities. Therefore, to meet the increasing demand for SiPh, the demand for high-capacity data communication solutions will be on the rise. Thus, the Asia particular market will grow during the forecast period.

KEY PLAYERS:

The key players in the Silicon Photonics market are Cisco Systems, Infinera, Finisar, GlobalFoundries, InPhi, IBM, Rockley Photonics, Intel, IPG Photonics, MACOM Technology, NeoPhotonics, II-VI, STMicroelectronics & Other Players.

Recent Development

-

In March 2024, Intel unveiled advanced 400G DR4 and 800G DR8 Silicon Photonics Optical Engines, designed for high-bandwidth data center interconnects. These engines support data rates of 100G per wavelength and offer improved power efficiency and integration, making them ideal for hyperscale cloud environments.

-

In March 2024, Marvell launched its 3D Silicon Photonics Engine which is the industry’s first 200G 3D Silicon Photonics Engine, providing 2x the bandwidth and 30% lower power consumption per bit compared to 100G interfaces. It integrates numerous components into a single device, optimizing it for high-density AI clusters and cloud data centers.

| Report Attributes | Details |

| Market Size in 2023 | USD 1.76 billion |

| Market Size by 2032 | USD 14.46 billion |

| CAGR | CAGR of 26.37% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Transceivers, Switches, Optical Multiplexers, Variable Optical Attenuators, Optical Engines, Active Optical Cable, Sensors) • By Component (Photo Detectors, Lasers, Modulators) • By Waveguide (400-1,500 NM, 1,310-1,550 NM, 900-7000 NM) • By Application (Military, Defense And Aerospace, IT And Telecommunication, Medical And Life Science, Data Centers And High-Performance Computing, Other) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cisco Systems, Infinera, Finisar, GlobalFoundries, InPhi, IBM, Rockley Photonics, Intel, IPG Photonics, MACOM Technology, NeoPhotonics, II-VI, STMicroelectronics |

| Key Drivers | • Growing emphasis on lowering power consumption with silicon photonic transceivers. • Demand for high-speed broadband services is increasing. |

| RESTRAINTS | • The incorporation of silicon photonic components into small circuits. |

Frequently Asked Questions

Ans: Asia Pacific is the fastest-growing region in the Silicon Photonics Market in 2023.

Ans: The transceivers segment dominated the Silicon Photonics Market.

Ans: Growing emphasis on lowering power consumption with silicon photonic transceivers is a major growth factor for the Silicon Photonics Market.

Ans: Silicon Photonics Market size was USD 1.76 billion in 2023 and is expected to Reach USD 14.46 billion by 2032.

Ans: The Silicon Photonics Market is expected to grow at a CAGR of 26.37% during 2024-2032.

Get in Touch