Smart Ward Market Report Scope & Overview:

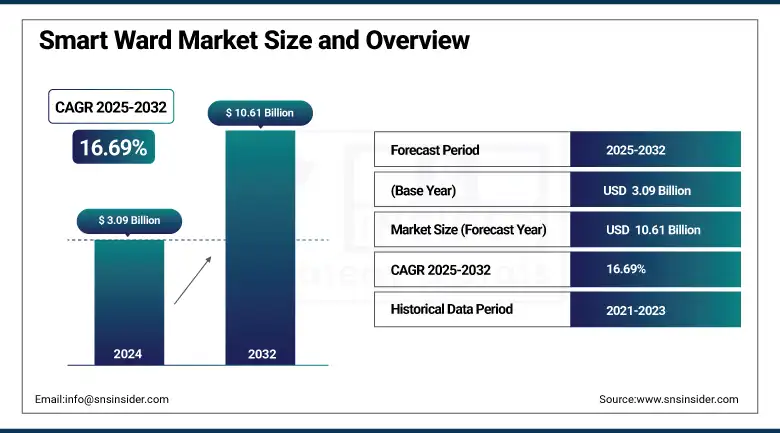

The Smart Ward Market size was valued at USD 3.09 billion in 2024 and is expected to reach USD 10.61 billion by 2032, growing at a CAGR of 16.69% over 2025-2032.

The global smart ward market is gaining traction with the increasing requirement for connected solutions in healthcare, real-time patient monitoring, and better workflow systems in hospitals. With an increasing adoption of IoT-capable devices, RFID tags, RTLS systems, and AI-based support tools for clinical decisions, old-style wards are becoming digitally smart areas.

Smart wards have been shown to reduce nurse workload by 20%, to improve medication tracking, and to increase bed management efficiency by more than 30%, increase patient safety, and hospital efficiency. More and more hospitals, especially in Asia Pacific and Europe, are adopting 8–12 times more smart devices and connected systems than five years ago. Government-led initiatives in digital health infrastructure, such as the EU’s “Digital Health and Care” strategy and India’s Ayushman Bharat Digital Mission, make up the additional demand. Share in patient monitoring and workflow automation due to the growing R&D investments by leading smart ward companies (such as GE HealthCare, Siemens Healthineers, and Philips.

To Get more information On Smart Ward Market - Request Free Sample Report

In June 2024, GE HealthCare introduced a smart ward solution, powered by AI technology, which combines patient tracking, predictive analytics, and automated alerts across hospital networks, with the aim of reducing patient deterioration events by 15–20%.

Regulatory progress, like the U.S. FDA’s embrace of digital health tech and the EU’s MDR regulations for connected devices, is also easing approvals and hastening the pace of product release. Rising investments towards AI and IoT in healthcare, exceeding USD 4 billion globally by 2024, also contribute to the uptake of the smart ward market growth.

In May 2024, Qatar and Belarus join forces to enhance regional smart wards with the deployment of an RFID and RTLS-enabled smart ward system to provide the best care during health emergencies and optimize hospital logistics, and signify robust regional as well as increasing global smart ward market share.

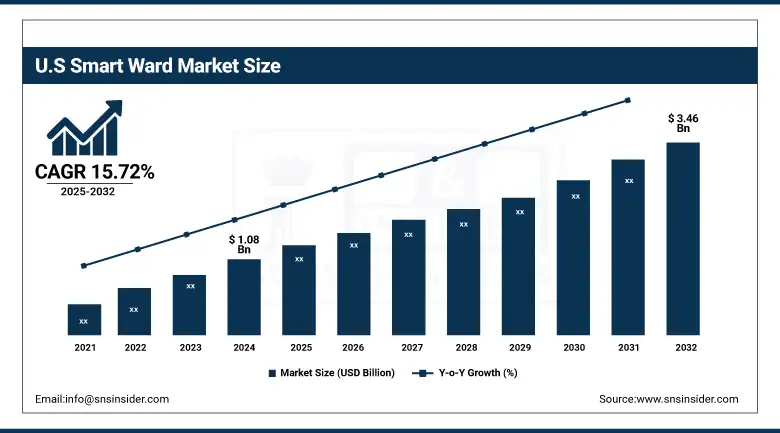

The U.S. smart ward market size was valued at USD 1.08 billion in 2024 and is expected to reach USD 3.46 billion by 2032, growing at a CAGR of 15.72% over 2025-2032. The U.S. commands the highest market share in the region on account of well-established hospital networks, massive government spending on initiatives such as the HITECH Act, and substantial expenditure on R&D, with the U.S. healthcare IT industry size estimated to surpass USD 130 billion by 2024. There are also more than 85% of U.S. hospitals combining smart monitoring and automated workflow. Canada is also growing, mostly in Ontario and British Columbia, especially because of federal smart healthcare initiatives. In private hospitals in Mexico, the adoption of digital health tools is slowly making headway, but there continues to be a gap with public-sector deployment.

Table: Recent Partnerships and Launches (2023–2024)

|

Company/Organization |

Partner/Initiative |

Purpose |

Date |

Region |

|

Philips Healthcare |

Smart Ward Integration in the EU |

Multi-center patient monitoring |

Aug 2023 |

Europe |

|

Lifesigns + Amala Hospital |

Wireless Smart Ward Deployment |

Real-time vitals tracking |

Mar 2023 |

India |

|

Sancheti Hospital |

AI-Driven Smart Ward Launch |

Continuous patient monitoring |

Jun 2024 |

India |

|

GE Healthcare |

Smart ICU + Ward Systems |

Predictive alert systems |

Sep 2023 |

U.S. |

|

Samsung Medison |

Smart Bed Connectivity System |

Remote fetal/maternal tracking |

Nov 2023 |

South Korea |

Market Dynamics:

Drivers:

-

The Major Factors Fueling the Smart Ward Market Growth, Supported by Advancements in Technology, Rising Healthcare Demand, and Digitalization Initiatives

The smart ward market growth is primarily driven by the growing healthcare digitization, increasing inpatient caseloads, and growing focus on improving operational efficiency and patient safety. Global shortages of healthcare workers are forecast to exceed 10 million by 2030 (WHO). This is driving the widespread adoption of automated ward solutions in hospitals that can help to streamline clinical work processes and cut down on time spent on administrative tasks. Real-time location systems (RTLS), RFID-based asset tracking, and automated dispensing cabinets are being used to enhance visibility of the supply chain and increase medication accuracy.

Key capital investments by healthcare companies into IT infrastructure are also driving the demand, with over USD 21 billion invested into digital health in 2024 globally, much of this into inpatient care automation. Moreover, increasing regulatory backing, such as the US FDA’s Digital Health Software Precertification Program and the UK NHS’s “What Good Looks Like” framework, is assuring health services that they can deploy AI-driven solutions on the ward. Smart beds and wired monitors are already driving 30% fewer adverse outcomes, increasing market confidence. Also, healthcare tech powerhouses, including Medtronic and Hillrom, are spending more on R&D, pushing forward innovation in smart beds, wearables, and patient monitoring, creating the terrain for the smart hospital rooms industry landscape of the next-gen global smart ward market.

Restraints:

-

The Key Limitations Hindering Smart Ward Market Growth Include Cost Barriers, System Integration Issues, And Regulatory Complexities

The smart ward market still has to address major challenges, including high initial fees and interoperability within legacy systems. Thousands of hospitals, particularly in low-to-mid income economies, cannot justify such investment, estimated at USD 2-5 million per hospital, for full deployment in the absence of a clear and fast ROI. Custom middleware is commonly needed for integration (e.g., infusion pumps, monitors, and EMRs), which can introduce latency and inefficiency into a system. In addition, data security and adherence to regulations are crucial. According to an HIMSS 2024 CIO survey, more than 60% of healthcare CIOs reported cybersecurity risks and burdensome regulations as the leading barriers to implementing smart ward.

The lack of standardization of data formats between vendors is one of the contributors to the inability to scale the system. Additionally, the shortage of computer-literate IT staff within hospitals is a bottleneck to the useful deployment and maintenance of smart solutions. There are a number of regulatory barriers to adoption that further challenge this dynamic, such as a lagging approval on the digital health side in certain parts of the world, and overlaid authorities or requirements on the medical device and data protection fronts (e.g., HIPAA, GDPR). Without well-defined frameworks and affordable integration, market share may be limited for smart wards, particularly for resource-limited providers, and a broad adoption will be delayed despite demonstrated value.

Segmentation Analysis:

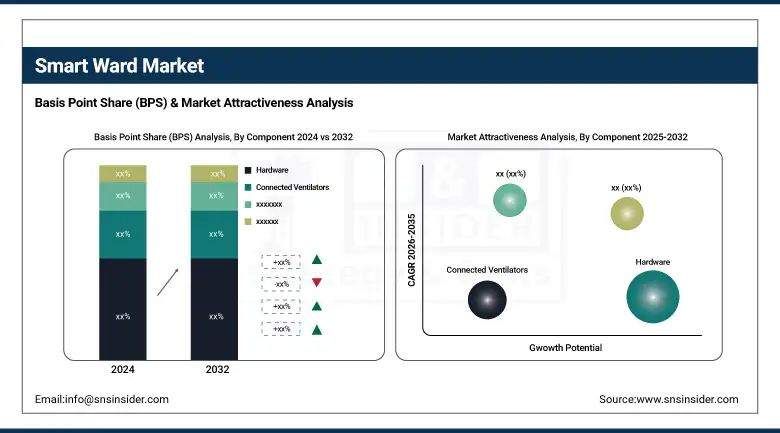

By Component

The hardware dominated the market in 2024, with 59.03 of % smart ward market share in the market. This predominance is due to the widespread use of smart beds, RFID tags, sensors, and real-time location tracking devices that constitute the role of smart ward infrastructure. Continuing demand for hardware system devices that interface directly with software systems and with human patients provides an ongoing source of demand for such hardware.

The top growth dynamic remains the software category, driven by AI-enhanced platforms, cloud-based EHR systems, and interoperability solutions, which optimize data sharing and clinical decisions. The move towards digital-first healthcare architecture and predictive analytics in patient care is driving up the adoption of software in smart wards.

By Application

Patient monitoring & management was the largest smart ward market held in 2024, due to the rising demand for real-time vital sign monitoring, automated alerts, and continuous patient engagement systems. Hospitals are moving toward smarter monitoring to diminish negative events and increase the probability of improving outcomes, as we see increased prevalence of chronic disease and an aging population.

The fastest-growing application is workflow automation, as more and more healthcare provider organizations are investing in automated scheduling, digital handovers, and clinical task management systems. These solutions help enhance productivity among staff and reduce burnout, enhancing care coordination, particularly in high-volume hospital environments.

By Technology

The Internet of Things (IoT) segment led the smart ward market in 2024 and accounted for a share of 36.2% as it is the basic requirement to connect devices, share real-time data, and communicate efficiently between devices, patients, and clinical support. IOT is necessary for the live monitoring and automation in a smart ward as we know it today.

The fastest-growing technology is AI & ML (Artificial Intelligence and Machine Learning). Such tools are being widely circulated to support predictive analytics, alert automation, patient-centered care, and resource allocation at the ward level. Investments in AI integration across hospital systems are one factor spurring the smart ward market trend.

By End User

Hospitals led the end-user segment in terms of smart ward market share in 2024, as they are equipped with extensive facilities and have high budget reserves, plus a high demand for integrated systems to improve patient care and operational excellence. This dominance is further driven by the high adoption of connected devices in tertiary and quaternary hospitals.

The long-term care facilities are the fastest-growing end-user segment for which the smart ward technologies play a significant role in coping with the aging population, continuous monitoring, and staff reduction. Demand for customized, long-term care plans is also driving the smart ward market trend.

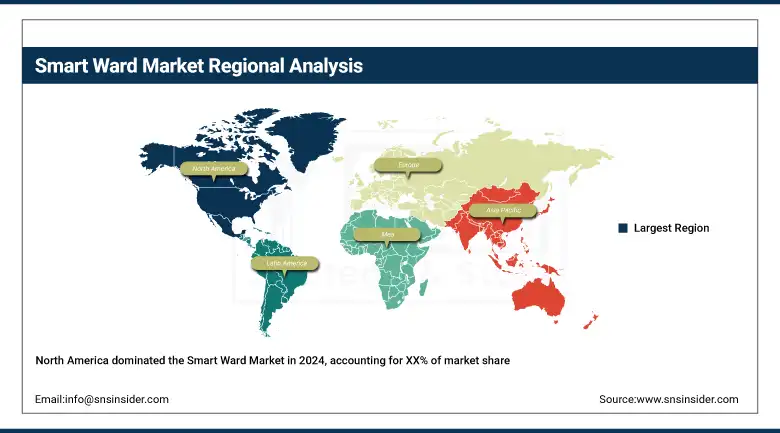

Regional Analysis:

North America held a major position in the global smart ward market analysis in 2024 due to excellent healthcare infrastructure, large digital health adoption, and high R&D expenditure. The region is an early adopter of AI, IoT, and RTLS in healthcare and has favorable reimbursement policies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe secures the second position in the market owing to harmonized regulation (for example, MDR, GDPR) and digital changes accepted in most of the leading economies. Germany and Britain are among the countries implementing AI-based hospital automation and smart wards in a big way. Germany is the strongest market in the area due to more than €4.3 billion invested in digital infrastructure improvements within the framework of the “Hospital Future Act,” leading to many hospitals deploying RTLS and patient monitoring projects. The UK, driven by its NHShas devised a “What Good Looks Like” digital roadmap to rapidly digitize inpatient care and installed AI systems in more than 150 hospital trusts. France and Italy are also making smart inroads on infrastructure, particularly on public health networks. Eastern Europe and Turkey are up next in line, but at a slower pace, amid cost and infrastructure challenges.

The Asia Pacific is expected to be the fastest-growing region in the smart ward market analysis, owing to increasing healthcare expenditure, urbanization, and government healthcare digitalization policies.

China leads the region, spurred by its “Smart Hospital” initiative and large-scale IoT projects, and more than 2,000 hospitals will implement smart ward technologies by 2024. Last year, China’s public-private investments in hospital automation totaled over USD 6.5 billion. India is a burgeoning market, smart ward tests in Tier-1 hospitals have been facilitated by the Ayushman Bharat Digital Mission, and cloud-based hospital systems are also receiving larger investments. Some hospitals in Japan and Korea are applying robotics and AI to elderly care in smart wards. Australia is also experiencing growth in remote patient monitoring, with the federal telehealth expansion driving uptake across its expansive geography.

Table: Regulatory and Policy Landscape Impacting Smart Wards

|

Country |

Key Regulation/Policy |

Impact on Smart Ward Deployment |

Implementation Year |

|

U.S. |

FDA Digital Health Software Precert Program |

Accelerates the clearance of AI-driven tools |

2023 |

|

Germany |

Hospital Future Act (KHZG) |

Fund smart infrastructure in hospitals |

2022 |

|

UK |

NHS "What Good Looks Like" Framework |

Standardizes digital transformation goals |

2021 |

|

India |

Ayushman Bharat Digital Mission |

Promotes digital health records and smart care |

2022 |

|

UAE |

Smart Hospital Program (Dubai Health Authority) |

Pilots smart ward technologies |

2023 |

Key Players:

Leading smart ward companies operating in the market include Philips Healthcare, Siemens Healthineers, GE Healthcare, IBM Watson Health, Medtronic, Honeywell, Cisco Systems, Johnson & Johnson, Cerner, Oracle, Allscripts, Baxter International, Boston Scientific, Samsung Medison, and Nuance Communications.

Recent Developments:

-

In June 2024, Sancheti Advanced Orthocare Hospital launched Pune’s first AI-powered Smart Ward, integrating real-time patient monitoring to enhance clinical decision-making and improve patient outcomes.

-

In April 2024, the Enugu State Government initiated the "One Ward One Smart Farm Estate" project, promoting smart infrastructure development, which reflects growing regional support for smart technology integration across sectors, including healthcare.

-

In March 2023, Lifesigns partnered with Amala Hospital to roll out a Smart Ward solution featuring continuous wireless patient monitoring to enhance clinical efficiency and care quality.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.09 billion |

| Market Size by 2032 | USD 10.61 billion |

| CAGR | CAGR of 16.69% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware (Smart Beds & Mattresses, Wearable Devices, Medical Devices (Connected Ventilators, Infusion Pumps, and Others), RFID & Tracking Systems, Others), Software (Patient Data Management Systems, Hospital Management Systems, Remote Monitoring Platforms, and Others), Services (Consulting, Implementation, and Others)) • By Application (Patient Monitoring & Management, Asset & Inventory Management, Workflow Automation, Infection Control & Hygiene Monitoring, and Others) • By Technology (Internet of Things, Artificial Intelligence (AI) & Machine Learning (ML), Cloud Computing, Big Data Analytics, Augmented Reality (AR) & Virtual Reality (VR) (Training & diagnostics), and Blockchain, etc.) • By End User (Hospitals, Clinics, Long-term Care Facilities, Home Care Settings, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Philips Healthcare, Siemens Healthineers, GE Healthcare, IBM Watson Health, Medtronic, Honeywell, Cisco Systems, Johnson & Johnson, Cerner, Oracle, Allscripts, Baxter International, Boston Scientific, Samsung Medison, and Nuance Communications. |

Frequently Asked Questions

North America dominated the Smart Ward market.

The smart ward market still has to address major challenges, including high initial fees and interoperability within legacy systems.

The smart ward market growth is primarily driven by the growing healthcare digitization, increasing inpatient caseloads, and growing focus on improving operational efficiency and patient safety.

The market is expected to reach USD 10.61 billion by 2032, increasing from USD 3.09 billion in 2024.

The Smart Ward market is anticipated to grow at a CAGR of 16.69% from 2025 to 2032.

Get in Touch