Aerosol Drug Delivery Devices Market Report Scope & Overview:

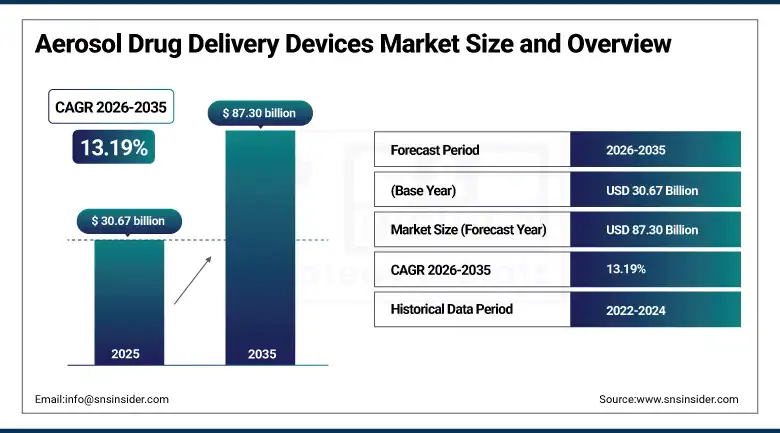

The Aerosol Drug Delivery Devices Market was valued at USD 30.67 Billion in 2025 and is expected to reach USD 87.30 Billion by 2035, growing at a CAGR of 13.19% from 2026 to 2035.

Medical devices known as aerosol drug delivery systems refer to the medical equipment which aerosolizes pharmaceutical formulations through particle generation of the optimum size and shape, and velocity parameters so that the drug delivery occurs via the deposition in the lungs, nasal passages, or oral pharynx. This device classification includes metered dose inhalers where actuation results in the delivery of accurate doses by aerosols due to the use of a propellant, dry powder inhalers with inspiratory aerosol deagglomeration of micronized drug, and nebulizers where aerosols result from ultrasound or jet atomization processes.

In January 2025, Aerogen planned to invest approximately USD 308.5 million to expand its manufacturing and development operations in Ireland, substantially increasing its production capacity for aerosol drug delivery solutions used in intensive care and hospital mechanical ventilation settings.

Market Size and Forecast

-

Market Size in 2025: USD 30.67 Billion

-

Market Size in 2026E: USD 34.71 Billion

-

Market Size by 2035: USD 87.30 Billion

-

CAGR: 13.19% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Aerosol Drug Delivery Devices Market - Request Free Sample Report

Aerosol Drug Delivery Devices Market Trends

-

Growing adoption of smart inhalers with digital monitoring, connectivity, and adherence tracking features.

-

Increasing development of inhaled biologics, insulin, and advanced therapies driving demand for specialized delivery devices.

-

Rising preference for breath-actuated inhalers that improve drug delivery accuracy and patient compliance.

-

Expanding use of nebulizers in hospital and homecare settings for chronic respiratory disease management.

-

Broadening applications of dry powder inhalers for vaccines, insulin, and systemic drug delivery.

The U.S. Aerosol Drug Delivery Devices Market Outlook

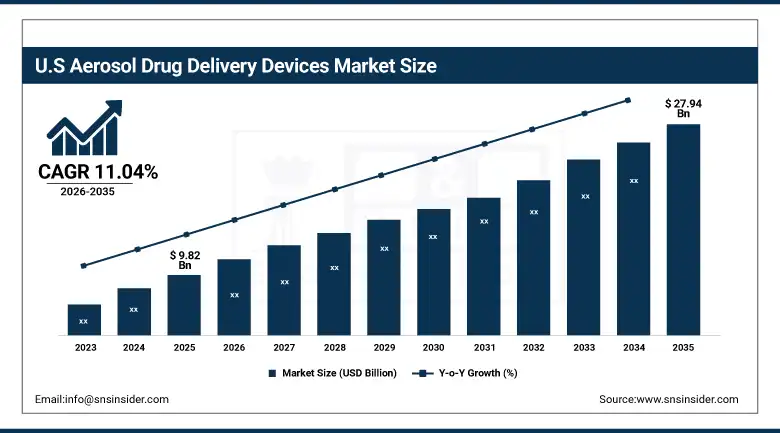

The U.S. Aerosol Drug Delivery Devices Market was valued at approximately USD 9.82 Billion in 2025 and is expected to reach approximately USD 27.94 Billion by 2035, growing at a CAGR of approximately 11.04%.

The United States is the world's most commercially significant aerosol drug delivery device market, driven by the world's largest pharmaceutical industry's investment in inhaled drug development, the FDA's established regulatory pathway for combination product inhaler and drug approval, the large domestic asthma and COPD patient population whose management under insurance-covered prescription benefit creates high device utilisation, and the commercial concentration of major aerosol device manufacturers including AstraZeneca, GSK, Boehringer Ingelheim, and specialty device companies whose U.S. operations define global development standards.

In October 2024, Aero Pump entered a collaboration with Resyca to market an ultra-soft nasal pump spray system designed to enhance nasal drug delivery through targeted and efficient administration with minimal mucosal trauma compared to conventional pump atomization.

Aerosol Drug Delivery Devices Market Segment Analysis

-

By Product Type, inhalers dominated the aerosol drug delivery devices market with 86.3% share in 2025, while nebulizers are growing steadily for hospital and complex respiratory care applications throughout the forecast period.

-

By Application, COPD dominated the aerosol drug delivery devices market with the largest application share in 2025, while asthma and allergic rhinitis collectively sustain high volume demand across all device categories during 2026 to 2035.

-

By End User, hospitals & clinics dominated the aerosol drug delivery devices market in 2025, while home care settings are the fastest growing end user driven by patient preference and healthcare system cost pressure to manage chronic respiratory conditions outside hospital settings.

By Product Type, inhalers dominate with 86.3% share, nebulizers serve hospital critical care

Aerosol inhalation products accounted for 86.3% of revenue earned from aerosol drug delivery devices in 2025, addressing the largest patient population in the world through the use of respiratory drug delivery applications such as asthma, COPD, and allergic rhinitis. Metered dose inhalers continue to be the leading form of inhalation product in the world due to their ability to ensure consistent delivery irrespective of breathing speed thanks to their propellant-based aerosol generation mechanism, supported by an evolution from CFC to HFA propellant, and subsequently from HFA to the next generation of propellants, which are less damaging to the environment owing to their low global warming potentials.

Nebulizers serve the most severely affected respiratory patient populations whose inspiratory effort limitation, acute exacerbation severity, or drug formulation requirement makes conventional inhaler use impractical, creating a clinically essential hospital and home nebuliser market whose growth is driven by the expanding inhaled antibiotic and antifungal treatment programmes for bronchiectasis and cystic fibrosis. Vibrating mesh nebuliser technology, which generates fine aerosol particles through piezoelectric mesh membrane vibration rather than compressed air jet atomization, delivers superior residual volume efficiency and smaller particle size distribution whose clinical performance advantages in critically ill patients sustain premium pricing despite higher unit cost than conventional jet nebulizers.

By End User, hospitals dominate, home care grows fastest

Institutions such as hospitals and clinics accounted for the largest end-user revenues in 2025, owing not only to the relatively high cost of each unit within the institutions where advanced nebulizer systems and smart inhalers are required but also to the clinical setting characterized by severe respiratory diseases that lead to a significantly higher amount of investment on pharmacotherapy per individual as compared to ambulatory care settings. It is critical care nebulization for ventilated individuals, bronchodilator treatment in hospital emergency departments, and inhaler device training within pulmonary rehabilitation programs that maintain purchasing of these devices within all product types.

Home care settings are growing fastest as the demonstrated clinical equivalence of home-based nebuliser therapy for stable chronic respiratory conditions with equivalent outcomes to clinic-based treatment, combined with patient preference and healthcare cost reduction motivations, is progressively shifting respiratory care management from clinic to home environments whose device requirements favor user-friendly, maintenance-simplified, and reliable systems.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

India |

32.84% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Aerosol Drug Delivery Devices Market Insights

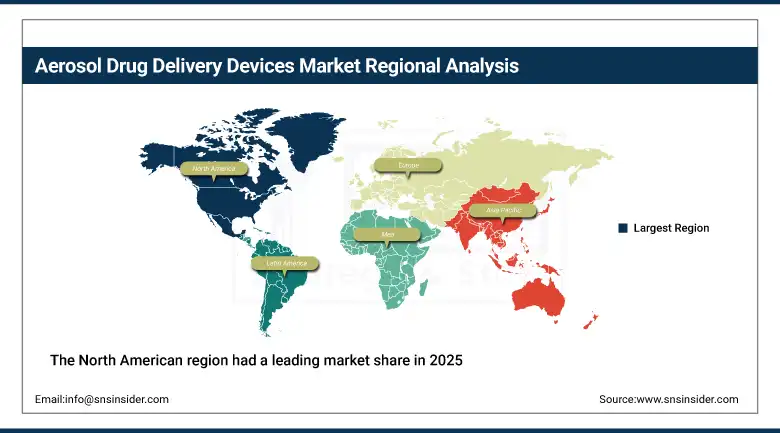

The North American region had a leading market share in 2025 due to its large contribution towards R&D efforts in the pharmaceutical sector for inhaled drugs, advanced healthcare infrastructure, higher awareness of respiratory diseases, and presence of key players dealing in inhalational drugs and devices in the country. The United States has a large share of around 82.47% of the regional revenue due to its large number of asthma and COPD patients, use of superior products owing to reimbursement policies, and FDA expertise that helps it approve combination products at a much quicker pace than any other market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Aerosol Drug Delivery Devices Market Insights

Europe was one of the largest revenue contributors to the global Aerosol Drug Delivery Devices industry in 2025. Some of the major countries include Germany, France, the United Kingdom, Sweden, and the Netherlands, which have a universal healthcare system and well-developed respiratory medicines clinic system, thereby resulting in constant demand for aerosol drug delivery devices. The regulatory approval route set out by the European Medicines Agency for combined inhaled drug and device development ensures continued development of inhaler technology in European pharmaceutical firms. The UK NHS respiratory initiative, German structured disease management program for asthma and COPD patients, and the adoption of digital health inhaler monitoring in Scandinavian countries provides Europe with regional references for innovation that shapes European market growth. Germany constitutes 28.47% of the total European revenue share owing to the presence of a large pharmaceutical industry.

Asia Pacific Aerosol Drug Delivery Devices Market Insights

Asia Pacific is the fastest-growing regional market for Aerosol Drug Delivery Devices due to having the largest disease burden in terms of respiratory diseases in the region, including China, India, and other Southeast Asian countries whose air pollution as a result of their urbanization process is causing high incidences of asthma and COPD, as well as due to the growth of healthcare infrastructure and insurance coverage that provide accessibility of medications and increasingly more sophisticated regulatory framework allowing for combination products. India, in turn, holds 32.84% of Asia Pacific revenues, thanks to the large patient base suffering from respiratory diseases, being the third-largest producer of generic pharmaceuticals worldwide with inhaled generics making a lot of device demand, and developing private healthcare sector adopting premium devices.

MEA & Latin America Aerosol Drug Delivery Devices Market Insights

ME and LA represent two emerging aerosol drug delivery devices markets which are seeing greater uptake of inhalers and nebulizers due to the increase in the respiratory disease disease load due to urbanization and industrialization, increased healthcare coverage, and expanded pharmaceutical market penetration. The UAE is the leader in MEA revenue accounting for about 22.84% of the total regional revenue because of its superior healthcare infrastructure, large expatriate population that consumes healthcare extensively, and medical tourism in the region which ensures the arrival of respiratory disease patients requiring devices. Brazil leads in LA revenue accounting for around 43.84% of the total regional revenue because of its large asthma patient base of around 20 million and the wide range of respiratory drugs covered under the Brazilian Public Health System and inhaled drugs produced locally.

Market Dynamics

Growth Driver: Rising prevalence of respiratory diseases and growing adoption of smart inhalers are driving demand for advanced aerosol drug delivery devices market

The structural factors driving the aerosol drug delivery devices market are made up of two demand drivers that are expanding concurrently. One of these drivers is the increasing number of patients requiring treatment of their respiratory diseases. The respiratory diseases burden in the global market is increasing due to air pollution arising from urbanization, cigarette smoking, exposure to workplace dust and chemicals, as well as increased vulnerability to COPD in the ageing population.

The second driver is represented by the maturity of the smart inhaler technology. This is marked by improvements in the health outcomes and reduction in costs associated with inhalers due to their ability to provide information regarding patient adherence, dosing and even environmental triggers of the respiratory diseases, which has increasingly been recognized by regulatory authorities and payers through reimbursement decisions. The adoption of smart inhalers continues to increase following every clinical study that provides evidence on their economic benefit.

Restraint: Regulatory complexities, propellant transition requirements, and high development costs can slow product commercialization.

The shift in regulation from HFA to ultra-low GWP HFO propellant, through the Kigali Amendment, necessitates the reformulation and resubmission of currently marketed MDI formulations in multiple countries each with its own requirements for clinical data, making this an ongoing process taking several years. The combined product development approach involving the collaboration between drug and device development that entails technical expertise in both domains is a challenge in itself limiting productivity in pipeline development for small pharma companies. The differing timelines and documentation requirements in each market add on to the high development costs for reformulation programs.

Opportunity: Expansion of inhaled biologics and digital health-enabled inhaler platforms is creating significant growth opportunities beyond traditional respiratory therapies.

The development of inhaled biologic agents is the biggest near-term frontier in the commercialization of aerosol drug delivery device technology, as this advance would create the largest potential market in the form of the world’s most rapidly growing market in the field of pharmaceuticals in which the monoclonal antibodies, fusion proteins, and nucleic acid therapies combined account for over USD 300 billion per year, and which can be partially replaced by the inhalation route using devices with superior patient convenience and possibly better pulmonary bioavailability.

Inhaled biologics for treating severe eosinophilic asthma, inhaled interferons for treating viral respiratory infection, and inhaled gene therapies to correct the lungs in cystic fibrosis patients are some examples of potential billion-dollar markets that will have to be made possible through advances in aerosol device technology.

Recent Developments:

-

2025: Aerogen announced an investment of approximately USD 308.5 million to expand its manufacturing and development operations in Ireland, substantially increasing production capacity for vibrating mesh nebuliser aerosol drug delivery solutions serving hospital mechanical ventilation and critical care patient populations globally.

-

2024: Aero Pump collaborated with Resyca to commercialise an ultra-soft nasal pump spray system for targeted intranasal drug delivery, addressing the growing market for intranasal administration of pain, migraine, CNS, and vaccine drug formulations whose nasal absorption advantages support development beyond conventional allergy treatment applications.

Aerosol Drug Delivery Devices Market Key Players are:

-

AstraZeneca PLC

-

GlaxoSmithKline PLC

-

Boehringer Ingelheim GmbH

-

Novartis AG

-

Teva Pharmaceutical Industries Ltd.

-

3M Company

-

Philips Respironics (Philips Healthcare)

-

Omron Healthcare Co. Ltd.

-

PARI Medical Holding GmbH

-

Aerogen Ltd.

-

Cipla Ltd.

-

Vectura Group PLC

-

Trudell Medical International

-

Aptar Pharma

-

Gerresheimer AG

-

Presspart Manufacturing Ltd.

-

Bespak (Consort Medical)

-

Aero Pump GmbH

-

Hovione SA

-

Catalent Inc.

Aerosol Drug Delivery Devices Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 30.67 Billion |

| Market Size by 2035 | USD 87.30 Billion |

| CAGR | CAGR of 13.19% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Metered Dose Inhalers, Dry Powder Inhalers, Nebulizers, Nasal Sprays, Others) • By Application (Asthma, Chronic Obstructive Pulmonary Disease, Cystic Fibrosis, Allergic Rhinitis, Others) • By End User (Hospitals & Clinics, Ambulatory Care Settings, Home Care Settings, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AstraZeneca PLC, GlaxoSmithKline PLC, Boehringer Ingelheim GmbH, Novartis AG, Teva Pharmaceutical Industries Ltd., 3M Company, Philips Respironics (Philips Healthcare), Omron Healthcare Co. Ltd., PARI Medical Holding GmbH, Aerogen Ltd., Cipla Ltd., Vectura Group PLC, Trudell Medical International, Aptar Pharma, Gerresheimer AG, Presspart Manufacturing Ltd., Bespak (Consort Medical), Aero Pump GmbH, Hovione SA, and Catalent Inc. |

Frequently Asked Questions

North America dominated the Aerosol Drug Delivery Devices Market in 2025.

The inhaler segment dominated the Aerosol Drug Delivery Devices Market with 86.3% share in 2025.

Rising global respiratory disease burden from urbanization and ageing populations, smart inhaler digital health platform adoption improving adherence and outcomes, expanding healthcare infrastructure in Asia Pacific enabling treatment access.

The Aerosol Drug Delivery Devices Market was valued at USD 30.67 Billion in 2025.

The Aerosol Drug Delivery Devices Market is expected to grow at a CAGR of 13.19% from 2026 to 2035.

Get in Touch