Veterinary Anti-infectives Market Report Scope & Overview:

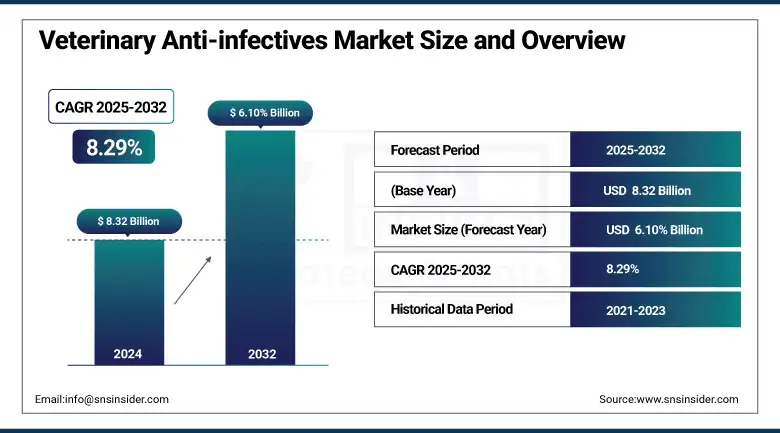

The veterinary anti-infectives market size was valued at USD 8.32 billion in 2024 and is expected to reach USD 13.27 billion by 2032, growing at a CAGR of 6.10% over the forecast period of 2025-2032.

The global veterinary anti-infectives market is growing significantly, due to massive dependency in livestock and companion animals, increasing demand for meat and dairy products, expansion of urban population, and pet ownership, especially in the Asia Pacific region, are fueling the consumption of anti-infectives. The North American and European markets are driven by the presence of a strong regulatory framework, along with antimicrobial stewardship initiatives, which act as a catalyst for veterinary anti-infectives market growth.

To Get more information On Veterinary Anti-infectives Market - Request Free Sample Report

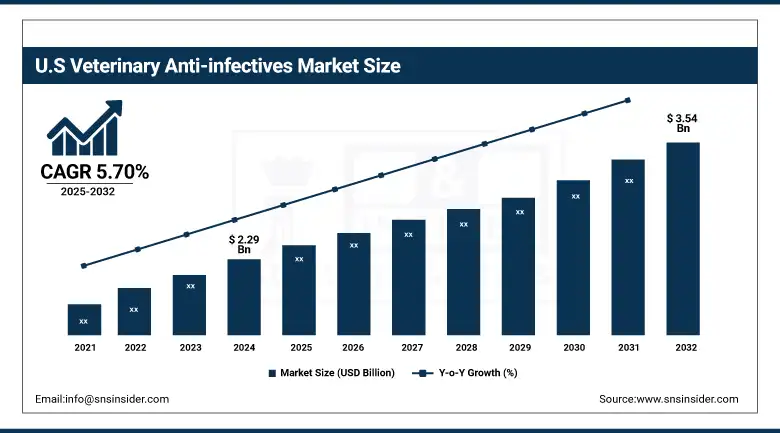

The U.S. veterinary anti-infectives market size was valued at USD 2.29 billion in 2024 and is expected to reach USD 3.54 billion by 2032, growing at a CAGR of 5.70% over the forecast period of 2025-2032.

The U.S. dominated the North American veterinary anti-infectives market due to its highly developed veterinary healthcare infrastructure, R&D capabilities, and high demand for effective treatment of livestock and companion animals. The early adoption of antimicrobial stewardship and top players from large industry players also support the dominance in the country.

May 2025 — FDA approval of Otiserene (Dechra): A single-dose, long-acting otic suspension for the treatment of canine otitis externa. The combination is a combination of marbofloxacin, terbinafine, and dexamethasone with a wide spectrum of antimicrobial and anti-inflammatory activity. In clinical trials, dogs treated with the drug experienced a 71.3% improvement rate, significantly better than the 26.3% improvement rate seen in control groups.

Market Dynamics:

Drivers:

- Increasing Animal Infectious Disease Incidence is Driving the Market Growth

The rising prevalence of infectious diseases in livestock and companion animals is one of the key factors driving the growth of the global veterinary anti-infectives market. In addition, diseases, such as bovine respiratory disease, swine dysentery, mastitis, and avian influenza can spread rapidly in intensive farming systems, making cattle, poultry, and swine all particularly vulnerable. The same goes for pets that may suffer bacterial skin infections, upper respiratory tract infections, and urinary tract infections, particularly in aging or immunocompromised animals. Such conditions necessitate prompt, targeted therapy, thereby contributing to an increased need for antibiotics, antifungals, antiparasitics, and antivirals. As the population of animals increases and the international commerce of animal goods increases, disease control becomes even more necessary, which induces an increased use of anti-infective therapies.

The outbreaks in mammals were over two times higher than those in the last 20 years, 1,022 outbreaks in 55 countries, an increase of nearly 123% compared to the 459 cases reported in 2023, by the World Organisation for Animal Health (WOAH). These events highlight the escalating risks driven by zoonotic and livestock infections, contributing to increased demand for antimicrobials, antivirals, and vaccines. In the 15 months between January 2024 and April 2025 alone, the global community reported more than 6,800 outbreaks of African swine fever, 3,500 of HPAI, and 3,600 of bluetongue disease, underscoring the ongoing need for animal disease control.

- New Veterinary Diagnostics and Drug Discovery is Propelling the Market Growth

Advancements in technology related to veterinary diagnostics are allowing practitioners to identify infectious agents faster and more accurately, resulting in timely, effective treatment decisions. PCR (polymerase chain reaction), ELISA kits, and rapid point-of-care tests have become commonplace in veterinary practices to differentiate between bacterial, viral, and parasitic infections. Such precision in diagnostics is beneficial for targeted anti-infective therapies, better treatment outcomes, and decreased reliance on inappropriate antibiotics, a significant driver for AMR (antimicrobial resistance). Additionally, advances in creating new formulations of drugs, including long-acting injectables, species-specific drugs, and combination products, are improving compliance and therapeutic effectiveness. These trends ensure the efficient, safe, and specific application of anti-infectives for unique veterinary needs, which is further propelling market growth.

Restraints:

- Stringent Regulatory Policies are Restraining the Market from Growing

Stringent regulatory requirements act as one of the major deterrent factors for the veterinary anti-infectives market analysis, as the approval, manufacturing, and marketing of all animal health drugs are governed by stringent regulatory guidelines. Regulatory authorities, such as the U.S. FDA (Food and Drug Administration) and EMA (European Medicines Agency) impose rigorous safety, efficacy, and environmental standards to confirm that no veterinary medicines jeopardize animals, humans (via residues in food), or the environment.

Such stringent regulations typically require extensive and costly clinical trials, rigorous documentation, and compliance with good manufacturing practices (GMP). That can slow the release of products greatly and discourage smaller businesses from participating in the first place. Additionally, increasing focus on antimicrobial stewardship and restricted use policies, particularly in Europe and North America, imposes further constraints on the development and marketing of anti-infective products, especially antibiotics. Although these regulations are an important tool in the fight against antimicrobial resistance (AMR), they add a significant financial and operational burden to the manufacturer's operations.

Segmentation Analysis:

By Animal Type

In 2024, the livestock animals segment led the veterinary anti-infectives market share with a 68.5% due to the high utilization of anti-infective agents among food-producing animals, including cattle, poultry, and swine. Given growing requirements for meat, milk, and additional products of pet sources (especially in developing and export areas), and justifications for illness control, there is a high need for the solution of many classes of animal products by using antimicrobials, antiparasitics, and other treatments concerning disease control. Additionally, increased governmental health and biosecurity regimes across the globe for livestock, followed by fears of zoonotic disease essentially disrupting the food supply chain, have solidified this segment.

The companion animal segment is expected to exhibit the fastest growth over the forecast period. This growth is anticipated to occur during the given period due to rising pet ownership, increased spending on pet health, and increased awareness of the well-being of animals. As a result of urbanization and lifestyle changes, the demand for veterinary care for dogs, cats, and other household animals has increased significantly. As the human-animal relationship bonds more and more tightly, pet owners are now increasingly going for early and preventive treatment, including antibiotics and antifungals. This segment is also witnessing a rapid expansion owing to the advances provided in diagnostic services, along with the availability of targeted therapies.

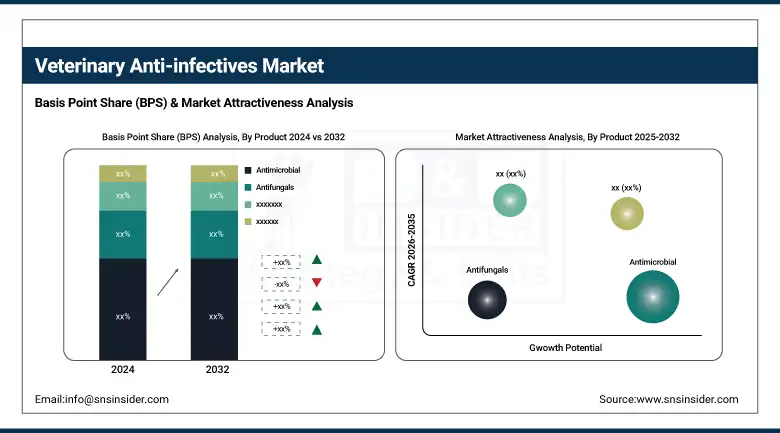

By Product

In 2024, the antimicrobial segment held the highest veterinary anti-infectives market share with 52.14% due to the medicines being used for the treatment of bacterial infections in both livestock and companion animals. A variety of common and economically important diseases, such as respiratory tract infections, mastitis, and enteric disorders, have a first-line therapy with antimicrobials. Due to their crucial role in the prevention and control of outbreaks in industrial-scale herds and flocks, well-established patterns of use and regulatory acceptance for therapeutic use, they remain the single largest product class in veterinary medicine.

The antivirals segment is expected to be the fastest growing during the forecast period, with the increasing prevalence of viral infections in livestock (such as Feline leukemia virus, canine parvovirus, and swine influenza). The increasing investment spends on targeted antiviral therapies and vaccines, coupled with rising awareness regarding zoonotic viral threats, is driving the market growth. Furthermore, the development of improved veterinary diagnostics is enhancing the detection of viral pathogens, thus allowing for the timely administration of antiviral treatments, thereby driving the demand for this nascent but rapidly evolving segment.

By Route of Administration

The oral segment dominated the veterinary anti-infectives market trends in 2024 with a 72.26% market share, owing to its convenient and easy administration route for medications, covering both food-producing animals and companion animals. Cost-effective and mass treatable, especially with the poultry and swine, the most widely used and effective forms of the recommended alternative are oral, such as tablets, powders, and feed additives. For home-based care, pet owners also prefer orally administered, enteral routes, such as finely sized food doses in companion animals. Coupled with the fact that oral anti-infectives can often be administered without the need for veterinary supervision, this has helped to reinforce their dominance in the market.

The other segment is expected to grow at the highest CAGR during the forecast period due to increased usage in targeted therapies and emerging treatment technology. Topical anti-infectives continue to be a growing trend in dermatological infections, while intramammary treatments are indispensable in mastitis control in dairy cattle. New advances in formulation science, including long-acting delivery systems and localized delivery, are improving both the efficacy and acceptability of these routes, especially for certain disease states where systemic delivery is less effective and/or not preferred.

By Type

In 2024, the OTC (Over-the-Counter) segment dominated the veterinary anti-infectives market with 73.10% market share, owing to its easy availability, affordability, and high accessibility, especially in emerging countries. OTC products are often used by livestock owners and pet parents for minor infections or preventive care, so no repeated visits to the vet are necessary. In rural and agricultural settings, over-the-counter (OTC) anti-infectives, such as feed additives and oral antibiotics are regularly utilized in order to maintain herd health. In addition, their accessibility through retail and agrovet stores has strengthened them in maintaining their market dominance in the livestock and the companion animal segments.

During the forecast period, the fastest-growing segment is related to prescription, which is attributed to the rising regulatory focus on antimicrobial resistance (AMR) and a global change toward the restricted use of anti-infectives. In the U.S. and EU members, numerous nations are developing extreme plans preparing for veterinary prescriptions for key anti-infection agents and different medications. This movement is encouraging more precision and accountability in medication utilization. An increase in complicated infections, the need for specific treatment, and increasing numbers of companion animals visiting clinics are further aiding the rapid surge of the prescription-based anti-infectives market.

By Distribution Channel

In 2024, the veterinary anti-infectives market was dominated by the retail pharmacies segment, with 76% market share, which has a large penetration, reliable distribution channels, and a long-standing presence in the urban and rural markets. Retail pharmacies are often a go-to source for farmers, pet owners, and animal caregivers seeking quick access to widely used anti-infectives, particularly OTC products. They are major suppliers of livestock medicines in farming areas and basic pet care in urban centers. Also, the availability of trained professionals with their basic guidelines supplements this segment’s market growth.

The e-commerce segment is expected to be the fastest-growing segment during the forecast period, owing to the ongoing digitalization of veterinary services and increasing adoption of home delivery of pet and livestock medicines. They provide a more convenient shopping experience, a vast selection of available products, competitive pricing, and an opportunity to find hard-to-find or specialty drugs. Additionally, an increase in pet ownership along with tele-veterinary services is driving this market, which is leading to a rise in online prescription-store-comparison services.

Regional Analysis:

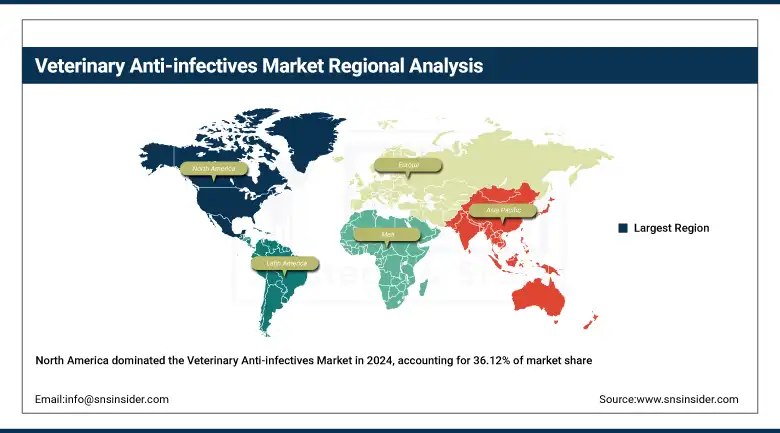

The North America Region holds the largest share of the veterinary anti-infectives market with a 36.12% market share in 2024, owing to the well-defined veterinary care standards, regulatory policies, and high adoption of animal health. Demand for anti-infective products is consistent in the region, driven by an established livestock industry and increasing companion animals. Furthermore, the presence of leading veterinary pharmaceutical firms, including Zoetis, Merck Animal Health, and Elanco, further augments the market. Widespread utilization of treatment based on prescriptions, strong investment portfolio on R&D, and significant disease surveillance programs are some of the factors responsible for North America holding a leadership position in this regard.

Get Customized Report as per Your Business Requirement - Enquiry Now

February 2024, Merck Animal Health, a subsidiary of Merck & Co., Inc., Rahway, N.J., U.S. (known as MSD Animal Health outside of the U.S. and Canada) has announced that it has entered into a definitive agreement to acquire the aquaculture business of Elanco Animal Health Incorporated for USD 1.3 billion in cash. The purchased asset consists of more than 200 unique formulas covering medicines, vaccines, nutritionals, and supplements intended for finfish and shellfish species, two manufacturing sites in Canada and Vietnam, and a research facility in Chile.

Asia Pacific is the fastest-growing region in the veterinary anti-infectives market with 6.67% CAGR over the forecast period due to an expanded livestock population, the increasing consumption of meat and dairy-related products, and the rising awareness of zoonotic diseases. Emerging economies, such as China and India are undergoing swift urbanization and sustaining a healthy growth rate, owing to which they are investing more in animal healthcare. In addition, the demand for veterinary anti-infectives is increasing due to government initiatives to facilitate the modernization of animal farming practices and outbreaks of infectious diseases.

The European veterinary anti-infectives market is growing substantially owing to the strict regulatory norms, growing awareness of antimicrobial stewardship, and surging demand for quality animal-sourced food products in the region. Sufficient guidelines have been executed in this region to manifest the responsible endeavor of the use of antibiotics in animals, and have resulted in the high acceptance of targeted therapies along with prescription-based anti-infectives. Moreover, the rising pet population, along with increasing zoonotic disease prevention awareness and animal welfare, are propelling the need for companion animal anti-infective products in major markets, such as Germany, France, and the U.K.

Latin America and the Middle East & Africa (MEA) exhibit moderate growth in the veterinary anti-infectives market, which can be attributed to expanding livestock farming and growth in initiatives for the enhancement of animal health infrastructure. The MEA growth is driven by the increasing zoonotic disease awareness and gradual improvement of veterinary services. The slower growth is still more restrictive access to advanced treatments, regulatory challenges, and less spending on veterinary healthcare compared to developed regions.

Key Players:

The veterinary anti-infectives market companies are Zoetis, Boehringer Ingelheim Animal Health, Merck Animal Health, Elanco Animal Health, Bayer Animal Health, Ceva Santé Animale, Virbac, Vetoquinol S.A., Phibro Animal Health Corporation, Norbrook Laboratories, and other players.

Recent Developments:

- February 2025 – Zoetis revealed that it has acquired marketing rights to Loncor 300 (florfenicol) from Elanco. The strategic acquisition augments Zoetis' cattle anti-infective portfolio by adding an amphenicol-class antibiotic, further solidifying its position as a leader in the livestock health market.

- November 2024 – Boehringer Ingelheim opened its newly expanded research and development center in Athens, Georgia. With the state's largest animal health company, this state-of-the-art facility reflects Boehringer's ongoing commitment to investment in innovation and to accelerating animal health and well-being.

Veterinary Anti-infectives Market Report Scope:

Report Attributes Details Market Size in 2024 USD 8.32 Billion Market Size by 2032 USD 13.27 Billion CAGR CAGR of 6.10% From 2025 to 2032 Base Year 2024 Forecast Period 2025-2032 Historical Data 2021-2023 Report Scope & Coverage Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook Key Segments • By Animal Type (Livestock Animal, Companion Animal)

• By Product (Antimicrobial, Antifungals, Antivirals, Antiparasitic, Others)

• By Route of Administration (Oral, Injectable, Topical)

• By Type (OTC, Prescription)

• By Distribution Channel (Hospital/Clinic Pharmacy, Retail Pharmacies, E-commerce)Regional Analysis/Coverage North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) Company Profiles Zoetis, Boehringer Ingelheim Animal Health, Merck Animal Health, Elanco Animal Health, Bayer Animal Health, Ceva Santé Animale, Virbac, Vetoquinol S.A., Phibro Animal Health Corporation, Norbrook Laboratories, and other players.

Frequently Asked Questions

North America dominated the Veterinary Anti-infectives Market in 2024.

Zoetis, Boehringer Ingelheim Animal Health, Merck Animal Health, Elanco Animal Health, Bayer Animal Health, Ceva Santé Animale, Virbac, Vetoquinol S.A., Phibro Animal Health Corporation, Norbrook Laboratories, and other players.

New veterinary diagnostics and drug discovery are propelling the market growth.

The Veterinary Anti-infectives Market was USD 8.32 billion in 2024 and is expected to reach USD 13.27 billion by 2032.

The Veterinary Anti-infectives Market is expected to grow at a CAGR of 6.10% from 2025 to 2032.

Get in Touch