Smokeless Tobacco Market Report Scope & Overview:

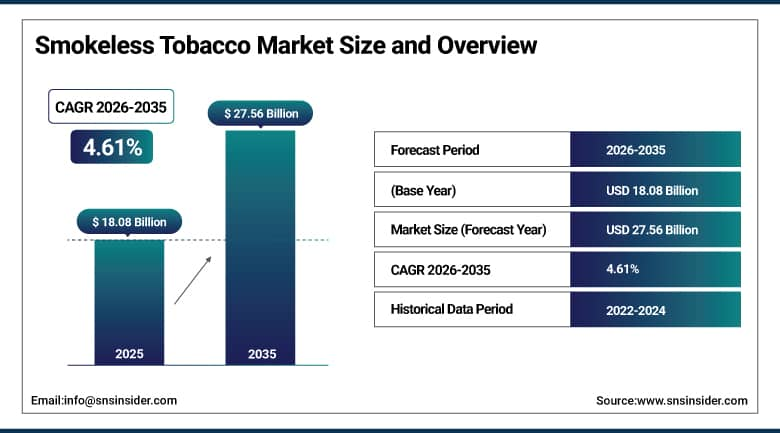

The Smokeless Tobacco market was valued at USD 18.08 billion in 2025. It is expected to reach USD 27.56 billion by 2035, growing at a CAGR of 4.61% from 2026–2035.

Nicotine products that do not involve combustion can be used via chewing, dipping, sniffing, and dissolving. Some of the key forms are moist snuff, dry snuff, snus, chewing tobacco, and dissolving strips. More than 60% of consumers in 2025 reported that discretion and convenience were major factors influencing their purchasing decision. Smoke bans imposed by 60+ nations are helping increase the adoption of smokeless tobacco products. Introduction of innovative flavors and controlled quantities of portions is widening the target customer base considerably. High level of acceptance of such products among South Asians and Nordic populations is keeping consumption practices strong. Modern nicotine pouch brands are being introduced in new territories with increasing frequency.

In 2025, over 60% of smokeless tobacco users chose snus, pouches, or dissolvable formats. Discretion and ease of use in public and workplace settings were the primary reasons cited.

Market Size and Forecast

-

Market Size in 2026E: USD 18.91 Billion

-

Market Size by 2035: USD 27.56 Billion

-

CAGR: 4.61% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Smokeless Tobacco Market - Request Free Sample Report

Smokeless Tobacco Market Trends

-

Nicotine pouches are the fastest-growing smokeless product format globally. Brands like ZYN and Velo deliver tobacco-free, discreet oral nicotine without spitting or visible residue.

-

Flavour diversification is attracting younger adult consumers to the smokeless category. Mint, berry, citrus, and menthol variants are driving consistent trial and repeat purchases.

-

E-commerce is becoming a critical distribution pathway for smokeless tobacco products. Subscription models and digital age verification are enabling geographic expansion beyond traditional retail.

-

Stricter packaging regulations are reshaping brand presentation across global markets. Standardized packaging and enlarged health warnings are being mandated in more countries annually.

-

Premium snus and pouch segments are consistently outgrowing standard commodity formats. Consumers are trading up to higher-priced, portion-controlled, and better-flavored smokeless products.

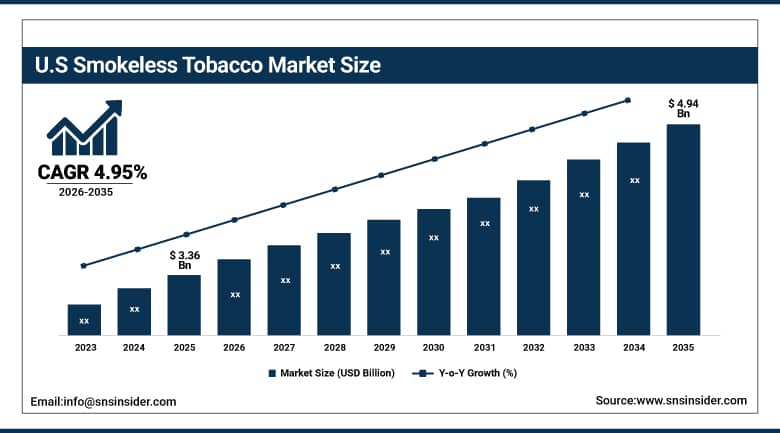

The U.S. Smokeless Tobacco Market Outlook

The U.S. Smokeless Tobacco Market was valued at approximately USD 3.36 billion in 2025. It is expected to reach approximately USD 4.94 billion by 2033, growing at a CAGR of 4.95%.

The U.S. is the most commercially advanced smokeless tobacco market in the world. Regarding market share, the leading companies are USSTC owned by Altria and American Snuff Company owned by Reynolds American Inc. FDA's approval on a product basis for marketing brings certainty in regulation and commerciality for investors. The nicotine pouches have been gaining quick access to retail distribution channels since their introduction into the market in 2020. Convenience stores remain the main retail channel for the distribution of smokeless tobacco in the United States. The online retail distribution channels are steadily growing as a result of development of technology in age verification during the digital era. Average spending per person has been increasing due to increased consumption of premium and flavored products.

FDA's marketing authorization framework for select moist snuff products has set a meaningful commercial precedent. It enables confident long-term investment in smokeless harm-reduction product development.

Smokeless Tobacco Market Segment Analysis

-

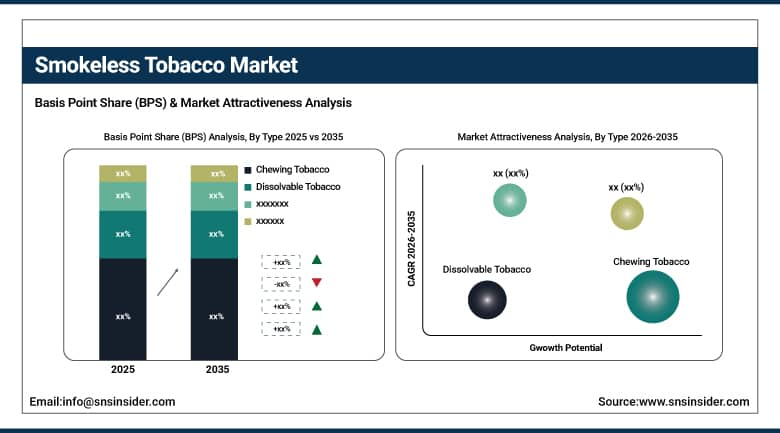

By Type, Chewing Tobacco led with approximately 45.27% share in 2025; Dissolvable Tobacco is the fastest-growing at a CAGR of 9.50%, driven by nicotine pouch convenience and discretion.

-

By Form, Dry Smokeless Tobacco dominated with approximately 55.32% share in 2025; Moist formats are growing rapidly through snus, dip, and modern nicotine pouch adoption.

-

By Route, Oral consumption dominated across chewing tobacco, snus, dip, and dissolvable categories; Nasal snuff holds a stable niche in select traditional European markets.

-

By Distribution Channel, offline dominated through convenience stores and tobacco shops; Online is the fastest-growing at a CAGR of 9.30% through subscription and direct-to-consumer models.

By Type, Chewing Tobacco dominates, Dissolvable Tobacco is expected to grow fastest

The market share of chewing tobacco is approximately 45.27% in the category of smokeless tobacco products in 2025. It has deep historical significance in the South Asian and North American marketplaces. The khaini form, gutka type, and loose leaf type products continue to maintain a huge volume of sales in their traditional markets. Low pricing along with rural distribution contributes to its category supremacy. Innovation in this category is less compared to other categories.

Dissolvable tobacco is the fastest-growing type at a CAGR of 9.50% through 2035. Nicotine pouches, strips, and lozenges define this commercially dynamic and innovative category. They require no spitting and leave no visible residue on the user. This makes them ideal for indoor, workplace, and public consumption environments. Brands including ZYN, On!, Velo, and Lucy have achieved strong penetration in the U.S. and Europe. Adoption is expanding well beyond traditional smokeless tobacco user demographics globally.

By Distribution Channel, offline dominates, online is expected to grow fastest

Offline retail represents 70% of channel revenue in 2025. Conveniences stores, tobacconists, and supermarkets allow consumers quick and wide-ranging access. Offline channels allow products to be discovered, compared with competing brands, and promotional offers redeemed. Age verification at the point of sale is a reliable way to ensure regulatory compliance. Relationships with existing retailers confer considerable advantage over new market entrants.

Online is the fastest-growing distribution channel at a CAGR of 9.30% through 2035. Direct-to-consumer subscription platforms are gaining significant commercial traction globally. Digital channels provide access to premium and niche products unavailable in local retail networks. Improved digital age-verification systems enable broader regulatory compliance for online sales. Loyalty and subscription programmes on digital platforms improve customer retention and lifetime value substantially.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.7% |

|

Europe |

Sweden |

27.3% |

|

Asia Pacific |

India |

48.6% |

|

Middle East & Africa |

South Africa |

29.8% |

|

Latin America |

Brazil |

43.4% |

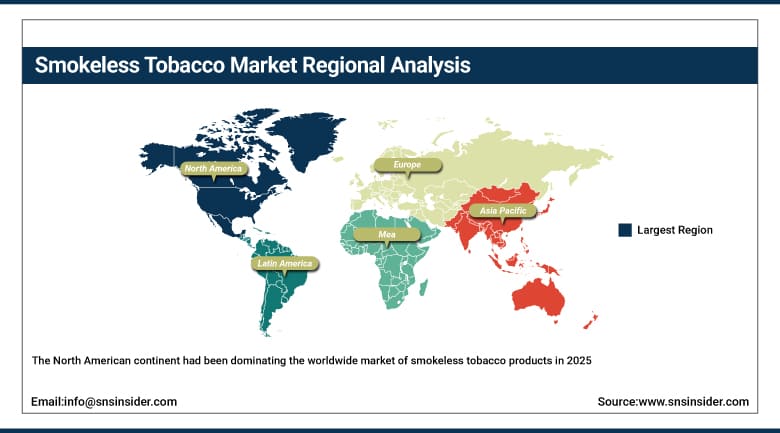

North America Smokeless Tobacco Market Insights

The North American continent had been dominating the worldwide market of smokeless tobacco products in 2025. The USA generates about 84.7% of the revenues earned by the continent as a whole. The major commercial companies in this market include Altria, Reynolds American, and Swedish Match. The FDA regulatory structure ensures very clear regulation on the products for investment. The use of nicotine pouches has helped open up the market beyond traditional consumers of tobacco products. The moist snuff is the highest revenue-generating product in this industry in the USA.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Smokeless Tobacco Market Insights

Europe is an advanced smokeless tobacco market with unique geographical attributes. Sweden contributes about 27.3% to European sales thanks to its well-entrenched snus culture. Similarly, Norway enjoys high per capita snus usage compared to other countries within Europe. There is also the effect of the ban of snus products across EU member states excluding Sweden and Finland. The emergence of nicotine pouches has seen them emerge commercially in countries where the use of tobacco snus is limited. Germany, Denmark, and the United Kingdom are among the leading nicotine pouch adopting markets in the region. Regulations continue to evolve on product classification in harm reduction across EU member states.

Asia Pacific Smokeless Tobacco Market Insights

Asia Pacific is leading among all regional segments, being the fastest-growing market for smokeless tobacco products worldwide. India represents around 48.6% of the Asia Pacific market based on its huge number of consumers. Khaini, gutka, and pan masala remain deeply rooted in many Indian states. Increasing incomes in urban areas are contributing to premium product usage among the country's increasing urban population. Stringent rules by the government continue to have an impact on product compositions and packaging designs. Other important markets in terms of volume include China, Bangladesh, and Pakistan. Young and growing populations are maintaining healthy future demand prospects.

MEA & Latin America Smokeless Tobacco Market Insights

South Africa leads MEA revenues at approximately 29.8% of the regional share. Algeria has seen rising chewing tobacco advertising and commercial investment in recent years. Brazil leads Latin American revenues at approximately 43.4% through established domestic tobacco culture. Regulatory frameworks across both regions are progressively aligning with WHO tobacco control guidelines. Growing health awareness is beginning to moderate consumption growth in major urban centers. Emerging market income growth is simultaneously enabling premium product adoption across both regions. International brands are selectively expanding distribution in high-potential urban markets. Rising smartphone penetration is supporting e-commerce channel growth across both regions significantly. Government tobacco tax revenues create a dual dynamic of fiscal dependency and health policy tension.

Market Dynamics

Growth Drivers: Rising smoking bans, growing health awareness, and nicotine pouch innovation are driving global smokeless tobacco market growth.

Indoor public smoking bans have been introduced in more than 60 countries since 2020. These policies are progressively driving adult users of nicotine towards discreet smokeless alternatives. Pouches have become the most commercially exciting innovation in the product category currently. They resonate well with consumers who have never used tobacco products before in their life. Introduction of flavors in these products is creating opportunities for even greater uptake. Harm reduction products, which are FDA approved, are proving their worth in the U.S. market. The growth in incomes among the middle classes in Asia and Africa regions is driving expenditure on higher-end smokeless products.

Restraints: Strict government regulations, growing health concerns, and excise tax increases are restraining smokeless tobacco market growth and expansion.

Government regulation of packaging, labeling, and market access in major markets is becoming much tighter. Mandatory standardized packaging policies are making it difficult to use differentiation in branding by major companies. Tax hikes are elevating pricing levels in various regulated countries. Awareness of the health concerns associated with smokeless tobacco among consumers is steadily rising globally. Regulation banning flavors restricts the key growth area of the business. Regulations in more than 100 countries mean very high costs related to regulatory compliance. Prevention of youth access means continual training and checking for retailers. Marketing restrictions limit brand communication.

Opportunities: Nicotine pouch expansion into new markets and harm-reduction regulatory authorizations create substantial smokeless tobacco growth opportunities globally.

The nicotine pouches that are free from tobacco can be promoted in regions where there is very little freedom concerning the use of traditional tobacco products. This ensures that the consumer base for the products is significantly increased beyond the current user base. In emerging economies in Asia, Africa, and Latin America, there exists a very large untapped demand pool. E-commerce helps to ensure the promotion of the products far beyond what physical retail outlets allow. High-end product categories continue to perform better margin-wise when compared to commodity-based products. The presence of harm reduction policies in the US, UK, and Sweden provides commercial security for investments in such products. Digital marketing allows targeted campaigns against the most lucrative consumer groups. There exists a rising wellness consumer trend globally, making people receptive towards harm reduction messages.

Recent Developments:

-

2025: Philip Morris International expanded ZYN nicotine pouch distribution across European and Asian markets. The brand leveraged its smoke-free product strategy and retail infrastructure for rapid geographic rollout.

-

2025: Altria Group launched new snus and nicotine pouch variants under its own! and Skoal brand portfolios. The launches targeted smoking switchers in high-regulation U.S. state markets specifically.

-

Q2 2025: India enacted stricter smokeless tobacco packaging regulations mandating larger health warnings. Standardized packaging is now required for all products sold in the Indian domestic market. These changes are already influencing product design and labelling strategies for domestic and international manufacturers.

Smokeless Tobacco Market Key Players are:

-

Altria Group Inc. (USSTC, on!)

-

British American Tobacco plc (Velo, Lyft)

-

Philip Morris International Inc. (ZYN)

-

Swedish Match AB

-

Japan Tobacco International

-

Reynolds American Inc. (American Snuff)

-

Imperial Tobacco Group plc

-

Universal Corporation

-

Dharampal Satyapal Limited

-

MacBaren Tobacco Company A/S

-

Dholakia Tobacco Pvt. Ltd.

-

Star Scientific Inc.

-

Standard Commercial Corporation

-

North Atlantic Trading Company

-

Kretek International Inc.

-

Swisher International Group

-

Rocky Mountain High Brands

-

Rogue Nicotine

-

Lucy Goods

-

Zyn (Philip Morris International)

Smokeless Tobacco Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.08 Billion |

| Market Size by 2035 | USD 27.56 Billion |

| CAGR | CAGR of 4.61% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Chewing Tobacco, Dipping Tobacco, Dissolvable Tobacco, Snuff, Others) • By Form (Dry, Moist) • By Route (Oral, Nasal) • By Distribution Channel (Online, Offline) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Altria Group Inc. (USSTC, on!), British American Tobacco plc (Velo, Lyft), Philip Morris International Inc. (ZYN), Swedish Match AB, Japan Tobacco International, Reynolds American Inc. (American Snuff), Imperial Tobacco Group plc, Universal Corporation, Dharampal Satyapal Limited, MacBaren Tobacco Company A/S, Dholakia Tobacco Pvt. Ltd., Star Scientific Inc., Standard Commercial Corporation, North Atlantic Trading Company, Kretek International Inc., Swisher International Group, Rocky Mountain High Brands, Rogue Nicotine, Lucy Goods, Zyn (Philip Morris International). |

Frequently Asked Questions

North America dominated the Smokeless Tobacco Market in 2025.

Chewing Tobacco dominated with approximately 45.27% of revenues in 2025.

Rising shift from combustible tobacco to smokeless alternatives is the primary growth driver. Nicotine pouch innovation is expanding market access to entirely new consumer segments globally. The global harm-reduction movement is further legitimising smokeless tobacco as a viable long-term category.

The Smokeless Tobacco Market was valued at USD 18.08 billion in 2025.

The Smokeless Tobacco Market is expected to grow at a CAGR of 4.61% from 2026 to 2035.

Get in Touch