Snack Pellets Market Report Scope & Overview:

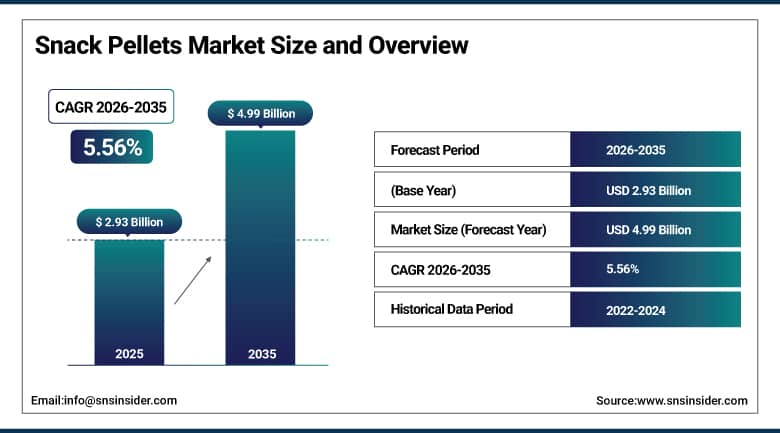

The Snack Pellets Market was valued at USD 2.93 Billion in 2025 and is expected to reach USD 4.99 Billion by 2035, growing at a CAGR of 5.56% from 2026–2035.

The global snack pellets market is undergoing a sustained commercial expansion driven by the convergence of consumer demand for convenient, ready-to-eat snacking formats and the food manufacturing industry’s growing preference for semi-finished intermediate products that offer production flexibility, extended shelf life, and formulation versatility unmatched by finished snack alternatives. Snack pellets are non-expanded, semi-finished products manufactured through extrusion from raw materials including potato, corn, rice, tapioca, mixed grains, and vegetable-based flours, which food manufacturers subsequently convert into ready-to-eat snacks through hot oil frying or hot air expansion processes that deliver the finished product texture, crunch, and flavor profile that consumers expect. Over 72% of global snack manufacturers now utilize pellets as a core intermediate due to their shelf life of up to 12 months versus four to six months for finished snacks, the operational flexibility they provide in adjusting output volume and flavor variants without retooling primary production, and their compatibility with both large-scale industrial processing and smaller artisan snack production environments that characterize the market’s long tail of branded and private label customers.

Tri-Snax launched a new multigrain protein-enhanced snack pellet line in early 2025, adding 60 SKUs across international markets, demonstrating the accelerating industry investment in nutritionally fortified pellet formulations that address the health-conscious consumer segment’s growing demand for snacks that combine the texture and convenience appeal of traditional extruded products with the macronutrient credentials of protein-enriched whole grain alternatives.

Market Size and Forecast

- Market Size in 2026E: USD 3.09 Billion

- Market Size by 2035: USD 4.99 Billion

- CAGR: 5.56% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

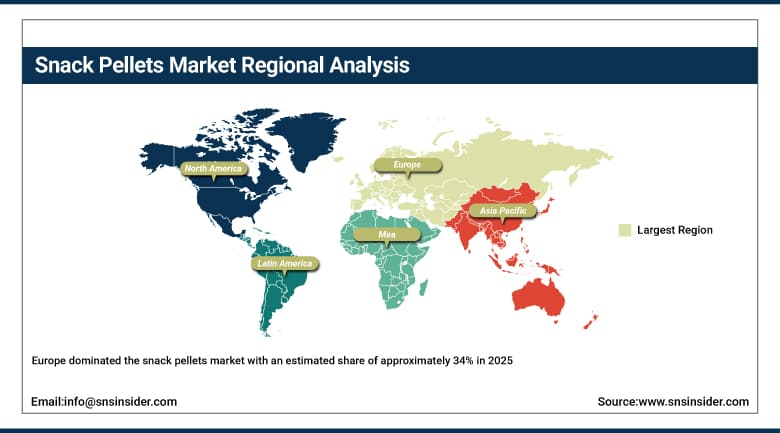

- Largest Region: Europe

To Get More Information On Snack Pellets Market - Request Free Sample Report

Snack Pellets Market Trends

- Rising consumer preference for healthier snacking is driving demand for air-expanded, low-fat, and multigrain pellet formulations across major markets.

- Growing adoption of twin-screw extrusion technology is enabling manufacturers to produce complex shapes, textures, and nutritionally enhanced pellet variants more efficiently.

- Increasing clean-label and organic product demand is compelling pellet manufacturers to develop formulations with minimal additives and traceable, sustainably sourced raw materials.

- Expanding organized snack retail and e-commerce distribution in Asia Pacific is significantly broadening consumer access to diverse pellet-based snack product categories.

- Rising private label snack production is creating growing B2B procurement demand for versatile pellet intermediates that food service and retail brands convert into proprietary finished products.

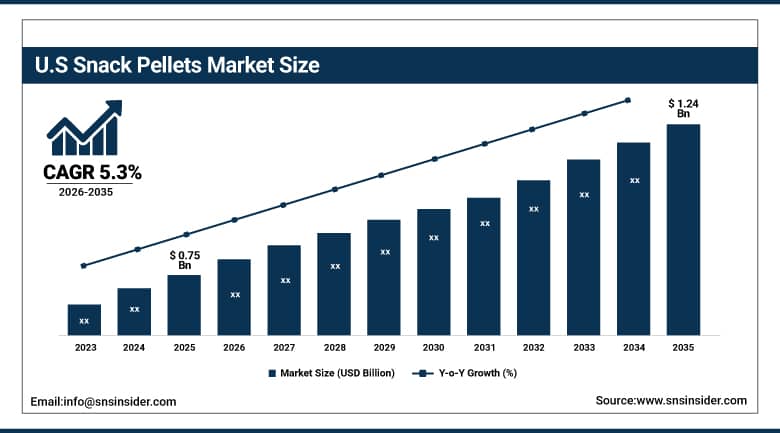

The U.S. Snack Pellets Market Outlook

The U.S. Snack Pellets Market was valued at approximately USD 0.75 Billion in 2025 and is expected to reach approximately USD 1.24 Billion by 2035, growing at a CAGR of approximately 5.3%.

Demand in the U.S. market is driven by the country’s well-established culture of snack consumption combined with rising consumer preference for healthier, lower-fat alternatives to traditionally fried snacks that hot air-expanded pellet-based products uniquely deliver. The U.S. benefits from advanced food extrusion manufacturing infrastructure, with twin-screw extruder adoption enabling producers including J.R. Short Milling and domestic pellet specialists to manufacture complex multi-ingredient pellets at the quality and consistency standards that major snack brands and private label retailers require. Multigrain and protein-enriched pellet formulations are growing fastest in the U.S. market, where new product development in the snack pellets segment has increased by approximately 29% in recent years, with multigrain and protein-enriched pellets accounting for over 22% of new launches as brands respond to consumer demand for snacks with meaningful nutritional credentials.

Snack Pellets Market Segment Analysis

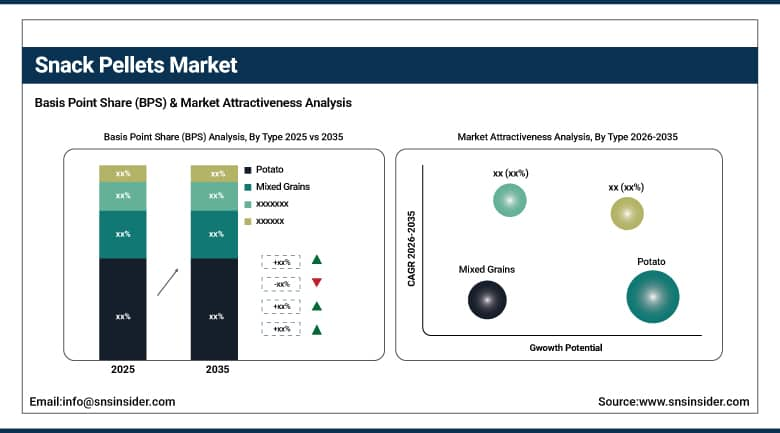

- By Type, potato-based pellets dominated with approximately 38% share in 2025, driven by their universal consumer familiarity and versatility across chip, stick, and ring snack formats. Mixed grains are the fastest-growing type, driven by health and nutrition positioning.

- By Form, laminated snack pellets dominated with approximately 46% share in 2025, supported by their compatibility with multiple snack formats and large-scale processing systems. Tridimensional pellets are the fastest-growing form segment at a CAGR of around 6.90% through the forecast period.

- By Flavor, flavored snack pellets dominated with approximately 61% share in 2025, driven by strong consumer demand for diverse savory and regional taste profiles. Nutritional pellets are the fastest-growing flavor segment at a CAGR of nearly 7.40% through the forecast period.

By Type, potato dominates, mixed grains grow fastest

Potato-based snack pellets retained the dominant type position with approximately 38% of the snack pellets market in 2025, a commercial dominance grounded in the potato’s universal consumer acceptance as a snacking ingredient, its established raw material supply chain across major agricultural producing regions in Europe, North America, and Asia Pacific, and the ingredient’s technical compatibility with the full range of extrusion, lamination, and expansion processes that snack pellet manufacturing employs. Potato pellets’ ability to deliver the familiar taste and texture characteristics that consumers associate with potato crisps and chips in formats ranging from flat chips to tubes and stars makes them the most commercially versatile pellet type for snack brands seeking to expand their product range with predictable consumer acceptance. The European market’s particular affinity for potato-based snacks has historically concentrated the largest potato pellet volumes in the region, where established potato crisp brands source pellets to produce private label and branded products across their retail distribution networks.

Mixed grains are the fastest-growing type in the snack pellets market, driven by the powerful structural trend toward health-positioned, nutritionally differentiated snack products whose multigrain formulations incorporating corn, rice, oats, quinoa, chickpea, lentil, and vegetable-based flours deliver the ingredient diversity and functional nutrition credentials that mainstream consumers are increasingly seeking in their everyday snacking choices. Mixed grain pellets command premium retail pricing relative to single-ingredient potato or corn alternatives, enabling manufacturers to improve revenue per kilogram while simultaneously responding to the consumer demand signals that are reshaping the snack category’s growth toward better-for-you formulations. The clean-label imperative is particularly commercially significant for mixed grain pellet development, as consumers scrutinizing ingredient lists respond most positively to recognizable whole grain and vegetable ingredients that communicate nutritional authenticity without requiring fortification claims.

By Flavour, flavoured snack pellets dominated, nutritional pellets grow fastest

Flavoured snack pellets dominated the market in 2025, accounting for the majority of commercial volume as manufacturers increasingly focused on regional, ethnic, spicy, cheese, and fusion flavour innovations to attract broader consumer demand across retail and food service channels. The segment’s dominance is supported by strong consumer preference for indulgent and ready-to-eat Savory snacks, alongside continuous product launches by major snack manufacturers seeking differentiated flavour portfolios and higher shelf appeal. Flavour-coated and seasoning-based pellet products continue to maintain significant demand across supermarkets, convenience stores, and quick-service food channels globally.

Nutritional pellets are the fastest-growing flavour segment, driven by rising consumer demand for clean-label, fortified, protein-rich, and functional snack products aligned with health and wellness trends. Manufacturers are increasingly incorporating ingredients such as whole grains, legumes, vegetable powders, plant proteins, and fiber-enriched formulations into snack pellet production to meet growing demand for healthier snacking alternatives. The rapid expansion of health-conscious consumer groups, particularly across North America, Europe, and Asia Pacific markets, is accelerating investment in nutritional snack pellet innovation and premium better-for-you snack categories.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

26.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

Europe Snack Pellets Market Insights

Europe dominated the snack pellets market with an estimated share of approximately 34% in 2025, driven by the continent’s deep-rooted culture of potato crisp and extruded snack consumption whose industrial production infrastructure depends heavily on potato and mixed grain pellet intermediates supplied by a well-developed regional pellet manufacturing ecosystem. Germany accounts for approximately 26.4% of European snack pellet revenues as the region’s largest national market, reflecting its position as both a major snack consumer market and a significant pellet manufacturing base where producers including Intersnack Group and specialized German pellet manufacturers supply both domestic brands and export markets across the EU with the high-volume conventional and premium pellet formulations that underpin European snack production.

The United Kingdom, France, Spain, and the Netherlands are significant secondary European markets where established crisp and extruded snack brands maintain large-scale pellet procurement relationships with regional suppliers, and where the growing demand for premium, health-positioned, and clean-label snack variants is driving active pellet formulation development investment. KP Snacks’ March 2024 introduction of a new Spicy Tomato Wheat Crunchies product demonstrates the continuous flavor innovation dynamic that characterizes European branded snack product development and sustains the flavored pellet category’s commercial primacy within the regional market.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Snack Pellets Market Insights

North America held a significant share of the global snack pellets market in 2025, with the United States accounting for approximately 82.5% of North American revenues through its combination of a highly developed snack manufacturing industry, sophisticated private label production ecosystem, and strong consumer demand for both conventional and health-positioned extruded snack formats. The U.S. market’s commercial depth reflects the presence of both major branded snack manufacturers who source pellets as intermediates for their production flexibility strategies and the growing direct-to-consumer snack brand segment whose small-batch, flavour-forward product strategies depend on the formulation versatility that pellet-based production enables without the capital investment required for proprietary finished snack manufacturing assets.

Canada contributes approximately 17.5% of North American snack pellet revenues through its organized grocery retail sector’s growing private label snack range, the country’s proximity to U.S. pellet manufacturing supply chains that enables efficient cross-border procurement, and a consumer health trend profile that mirrors U.S. demand for multigrain and air-expanded snack formats whose production depends on the type of nutritionally enhanced pellet formulations that both domestic and imported pellet suppliers are developing to serve the premium health snack tier.

Asia Pacific Snack Pellets Market Insights

Asia Pacific is the fastest-growing regional snack pellets market with a CAGR OF 7.80%, driven by rapidly expanding organized snack retail infrastructure, rising disposable incomes across China, India, and Southeast Asian markets, and the progressive adoption of Western-style convenience snacking formats among urban middle-class populations whose growing exposure to international snack brands is accelerating demand for the extruded and pellet-based snack formats that have historically characterized European and North American consumption. China accounts for approximately 44.8% of Asia Pacific revenues through its combination of a massive urban consumer population actively growing its snack category expenditure, a rapidly developing domestic pellet manufacturing industry, and the commercial pull of international snack brands whose China market entry strategies depend on local pellet supply to serve production volumes that import-dependent procurement models cannot cost-effectively support.

India represents the most commercially significant emerging market within Asia Pacific for snack pellets, as the country’s extraordinarily dynamic organized snack sector, whose growth is driven by urbanization, rising youth population, and the competitive innovation of domestic snack brands including ITC’s Bingo, Haldiram’s, and Balaji Wafers, creates growing structural demand for the diverse pellet formulations that support the product range breadth and launch velocity these brands require to maintain shelf presence across India’s expanding modern retail and e-commerce distribution networks. Noble Agro Food Products is among the domestic pellet manufacturers growing its capacity to serve this demand across Indian and export markets.

MEA & Latin America Snack Pellets Market Insights

Middle East and Africa and Latin America are growing snack pellets markets where urbanization, expanding organized grocery retail, and the rising consumption of convenience snacks among young and growing populations are creating incremental demand for pellet intermediates that support the production ambitions of regional snack manufacturers serving markets characterized by strong volume growth trajectories. UAE leads MEA revenues at approximately 31.2% of the regional total through its role as a regional food processing and distribution hub, the concentration of organized retail in Dubai and Abu Dhabi that sustains high-volume snack category consumption, and the active presence of international snack brands whose Gulf Cooperation Council manufacturing and distribution operations require pellet supply infrastructure aligned with regional taste preferences.

Brazil leads Latin American snack pellet revenues at approximately 44.2% of the regional total through its large domestic snack manufacturing industry, the country’s growing organized retail penetration driving snack category volume expansion, and the active participation of Brazilian food processors in the pellet-based snack category whose local raw material availability in corn and tapioca provides cost-competitive production economics that support both domestic consumption and regional export from Brazilian pellet manufacturing facilities serving the broader Latin American market.

Market Dynamics

Growth Drivers: Rising convenience snack consumption, health-positioned formulation innovation, and expanding Asia Pacific organized retail driving sustained pellet demand

The increasing consumer preference for convenient, ready-to-eat snack formats across all global markets is creating sustained structural demand for snack pellets as the semi-finished intermediate that underpins the commercial viability of the snack manufacturing industry’s most capital-efficient production model. Simultaneously, the growing consumer orientation toward healthier snacking, quantified by the 29% increase in new product development activity focused on healthier formulations, is expanding the addressable pellet market beyond conventional potato and corn variants into the premium multigrain, legume, and vegetable-enriched categories that command higher wholesale values and faster volume growth. The rapid expansion of organized snack retail in Asia Pacific’s emerging middle-class markets is adding an additional structural demand driver that reinforces the market’s growth trajectory independently of the more mature but still growing North American and European consumption dynamics.

Restraints: Raw material price volatility and supply chain disruptions affecting production cost predictability for pellet manufacturers and their snack brand customers

Snack pellet manufacturers face significant exposure to agricultural commodity price volatility across their primary raw material inputs, including potato starch, corn, rice, and tapioca, whose production volumes and wholesale prices are subject to weather event disruption, geopolitical trade policy impacts, and energy cost passthrough in the fertilizer and agricultural logistics supply chains that collectively determine the input cost environment within which pellet producers must manage their contract pricing obligations to snack brand customers whose own retail pricing constraints limit their tolerance for upstream cost increases. This raw material cost instability is particularly commercially challenging for smaller regional pellet manufacturers whose limited procurement scale prevents the forward contracting and diversified sourcing strategies that larger operators employ to stabilize their cost base against seasonal and cyclical commodity price movements.

Opportunities: Clean-label and protein-enriched product development, private label growth, and extrusion technology advancement creating new value-added pellet categories

The clean-label movement and protein enrichment trend are collectively creating a commercially significant premium product development opportunity for pellet manufacturers willing to invest in the raw material sourcing, formulation development, and certification infrastructure required to serve snack brands targeting the health-conscious consumer segment whose above-average willingness to pay premium snack prices supports the higher production costs of nutritionally enhanced pellet formulations. The rapid growth of private label snack production, as retailers priorities own-brand snack ranges that deliver higher margins than branded alternatives, is creating growing B2B procurement demand for versatile pellet intermediates at the consistent quality and volume levels that retail private label programmes require from their supply chain partners.

Recent Developments:

- 2025: Tri-Snax launched a new multigrain protein-enhanced snack pellet line in early 2025, adding 60 SKUs across international markets, reflecting the accelerating industry investment in nutritionally fortified pellet formulations targeting health-conscious consumers who seek snacks combining familiar extruded texture with meaningful protein and whole grain content credentials that standard potato or corn pellets cannot provide.

- 2024: KP Snacks introduced a new Spicy Tomato flavour for its Wheat Crunchies range in March 2024, available in multiple pack sizes and price points, demonstrating the sustained flavour innovation investment that major European snack brands directing to their wheat pellet-based product lines to maintain consumer engagement and capture emerging flavour trend demand across the convenience snack aisle.

- 2024: Noble Agro Food Products expanded its snack pellet manufacturing capacity in 2024 to serve growing demand from Indian and international snack brand customers for diverse pellet formulations including potato, corn, and multigrain variants, positioning the company to benefit from the rapidly expanding Asia Pacific pellet demand that urbanisation and organised retail growth in India and neighbouring markets are generating at an accelerating pace.

Snack Pellets Market Key Players are:

- Intersnack Group GmbH & Co. KG

- Limagrain Céréales Ingrédients

- J.R. Short Milling Company

- Bach Snacks S.L.

- Liven S.A.

- Noble Agro Food Products Pvt. Ltd.

- Le Caselle S.p.A.

- Leng d’Or S.A.

- Fiorentini Alimentari S.p.A.

- Tri-Snax International

- Calbee Inc.

- ITC Limited (Bingo!)

- Grupo Michel S.A. de C.V.

- Mafin s.r.l.

- Pellsnack Products Pvt. Ltd.

- Balance Foods Ltd.

- Snack Development Corporation

- KP Snacks Ltd.

- PepsiCo Inc. (Frito-Lay)

- Kellogg Company

Snack Pellets Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.93 Billion |

| Market Size by 2035 | USD 4.99 Billion |

| CAGR | CAGR of 5.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Potato, Corn, Rice, Tapioca, Mixed Grains, Others) •By Form (Laminated, Tridimensional, Die-Face, Gelatinized, Others) •By Flavor (Plain, Flavored, Nutritional) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intersnack Group GmbH & Co. KG, Limagrain Céréales Ingrédients, J.R. Short Milling Company, Bach Snacks S.L., Liven S.A., Noble Agro Food Products Pvt. Ltd., Le Caselle S.p.A., Leng d’Or S.A., Fiorentini Alimentari S.p.A., Tri-Snax International, Calbee Inc., ITC Limited (Bingo!), Grupo Michel S.A. de C.V., Mafin s.r.l., Pellsnack Products Pvt. Ltd., Balance Foods Ltd., Snack Development Corporation, KP Snacks Ltd., PepsiCo Inc. (Frito-Lay), Kellogg Company |

Frequently Asked Questions

Get in Touch