Sodium Sulfate Market Report Scope & Overview:

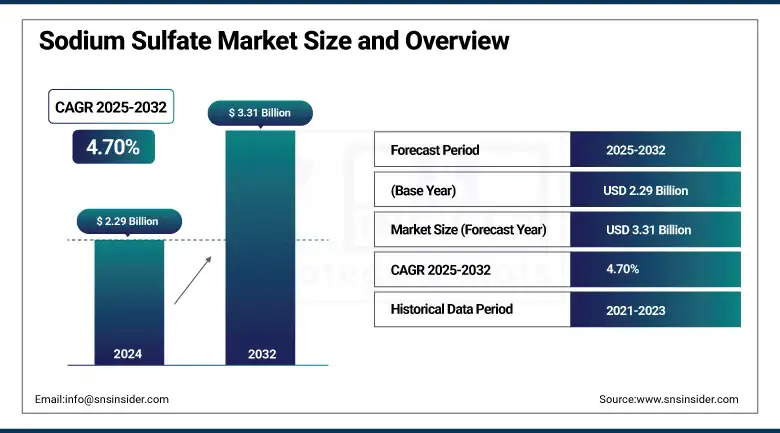

The sodium sulfate market size was valued at USD 2.29 billion in 2024 and is expected to reach USD 3.31 billion by 2032, growing at a CAGR of 4.70% over the forecast period of 2025-2032.

The sodium sulfate market is rapidly evolving in favor of sustainability and industrial innovation. North American sodium sulfate industry companies such as Searles Valley Minerals are scaling brine mining to saturate the market for detergents and glass. Synthetic sodium sulfate is more common in sustainable detergents, whereas Anhydrous Sodium Sulfate is more popular with manufacturing glass and recycling lithium-ion batteries byproducts. Sodium sulfate market trends highlight the increasing adoption of circular processes and clean manufacturing in the industry.

To Get more information On Sodium Sulfate Market - Request Free Sample Report

The U.S. Geological Survey (2023) reported that brine sources represented 33% of total U.S. salt consumption, a reflection of substantial natural sodium sulfate availability. Domestic sodium sulfate market share had likely been stable as of September 2022, when the U.S. International Trade Commission ruled no injury from Canadian imports of anhydrous sodium sulfate. Such developments are the manifestation of stable regulatory frameworks along with process innovation that is driving the sodium sulfate market growth.

Market Dynamics

Drivers

-

Expansion of Sustainable Brine Mining by Key Producers Accelerates Supply Growth

Leading sodium sulfate suppliers have increased the sustainable brine extraction of California dry-lake operations and incorporated a closed-loop evaporation process that reduces water and energy usage. This strategic repositioning will meet increased demand for natural sodium sulfate in detergents and glass and support a generalised expansion in the sodium sulfate market based on environmental sensitivity. Moreover, on the circular business front, by way of recycling lithium-ion battery byproducts and byproducts from rayon manufacture, customers can achieve higher purity of sodium sulphate with higher resource utilisation efficiency as well as supply source diversification. Consequently, brine-derived capacity in the North American sodium sulfate industry is expected to increase by 12% during 2022-24, helping to defend the market against raw material shortages

-

Rising Demand for High-Purity Synthetic Sodium Sulfate Fuels Specialty Applications

Pharmaceutical, electronics, and food-grade end-user industries have strict requirements for anhydrous sodium sulfate product purity, so Synthetic Sodium Sulfate manufacturers are innovating powder detergent formulation and specialty-grade anhydrous products to meet those specifications. Over the past few years, the developments in crystallization and drying technologies have kept the impurities below 0.05%, which have opened up new applications of high-purity material such as pH buffer, crystallization aid, and moisture-control desiccant. It is visible in a 9% annual growth from 2022 to 2024 in U.S. shipments of anhydrous sodium sulfate for specialty applications. These trends highlight the need for Sodium Sulfate Market Trends- segmentation, premium products, and chemical-firm and end-user partnerships.

Restraints

-

Climatic Variability Undermines Brine Lake Yield, Constraining Natural Supply

Production of Natural Sodium Sulfate via solar evaporation of brine is highly sensitive to precipitation and temperature; the 2023 unusually wet summer caused a 30,000-ton drop (-7%) in New York's Syracuse Basin output. Unfavourable weather conditions lower evaporation rates, prolong crystallization duration, and oblige producers to use more expensive synthetic methods. According to the U.S. Geological Survey, in 2022, domestic salt production was based in seven states, and 94% of salt was produced from this crop; such regional climate events may disproportionately affect the global Sodium Sulfate Market Size. This volatility increases the risk of supply and is hampering future capacity planning.

-

Heightened Water-Quality Regulations Increase Treatment and Compliance Costs

Stricter discharge limits for sulfate in industrial effluent, such as the EPA’s advisory to maintain drinking water sulfate below 250 mg/L and aquatic toxicity thresholds, necessitate advanced treatment systems at production sites. Retrofitting crystallizers and effluent treatment plants to meet these standards can add 8–12% to capital expenditures and drive-up operating costs. For instance, a Midwest facility incurred $1.2 million in treatment upgrades in 2023 to comply with state-mandated sulfate limits. This regulatory burden constrains profit margins and slows Sodium Sulfate Market Growth in regions with rigorous environmental policies.

Segment Analysis

By Nature

Natural Sodium Sulfate accounted for 55.3% of the market share in 2024, driven by its abundant reserves and lower production cost. Major producers like Saskatchewan Mining and Minerals in Canada supply to global detergent and glass manufacturers, ensuring steady demand. It is widely used in powder detergents as a filler and in glass production to remove air bubbles. According to the U.S. Geological Survey (USGS), the majority of natural Sodium Sulfate production is exported, highlighting its global acceptance and reliability in diverse industrial applications.

Synthetic Sodium Sulfate is the fastest-growing segment due to its consistent quality and purity, which are crucial for specialized uses in textiles and food processing. China leads in synthetic production through chemical processes involving hydrochloric acid and sodium chloride. As global industries emphasize precision formulations and environmental control, synthetic variants are gaining traction. Government incentives for advanced chemical production in Asia further fuel this growth. According to China’s Ministry of Industry and Information Technology (MIIT), synthetic Sodium Sulfate exports have increased by over 7% year-over-year.

By Application

Detergents dominate with 38.5% market share, primarily due to the essential use of Sodium Sulfate as a filler in laundry powders and cleaners. Global leaders like Procter & Gamble and Henkel utilize Sodium Sulfate for its stability, cost-effectiveness, and compatibility with phosphate-free formulations. Regulatory frameworks like the U.S. Environmental Protection Agency’s Safer Choice program promote eco-friendly cleaning products, reinforcing demand. Additionally, Sodium Sulfate’s ability to maintain granule consistency makes it indispensable in high-efficiency detergent formats, especially in North America and Europe, where sustainable consumer products are prioritized.

Glass is the fastest-growing segment with a CAGR of 5.58%, driven by booming construction and automotive sectors. Sodium Sulfate acts as a fluxing agent in glass production, reducing furnace temperatures and enhancing product clarity. According to the U.S. Energy Information Administration (EIA), energy-efficient manufacturing practices are expanding, where Sodium Sulfate plays a critical role. Demand for architectural and solar glass in countries like the U.S., Germany, and India is also pushing growth. Companies like Saint-Gobain and Guardian Glass increasingly adopt Sodium Sulfate to meet rising standards in glass performance and sustainability.

By End-User

In 2024, the household segment led with a 42.6% market share, largely attributed to Sodium Sulfate’s prevalent use in laundry and dishwashing detergents. Top brands like Unilever’s Persil and Procter & Gamble’s Tide rely on Sodium Sulfate to maintain detergent volume and reduce formulation costs. Consumer demand for eco-friendly, phosphate-free products aligns with regulatory guidance from the U.S. EPA and EU REACH programs. Its non-toxic and biodegradable profile also aligns with household safety preferences, further strengthening its foothold in the consumer goods sector.

Industrial usage of Sodium Sulfate is expanding at the fastest rate with a CAGR of 5.06%, fueled by growth in sectors like textiles, glass, and paper. It serves as a processing aid, drying agent, or additive in several manufacturing workflows. Notably, increasing demand for sustainable packaging materials and specialty glass products supports this trend. The European Chemicals Agency (ECHA) has recognized Sodium Sulfate as a low-risk industrial chemical, encouraging its broader application. Industrial players are also benefiting from low raw material costs and growing demand in emerging markets.

Regional Analysis

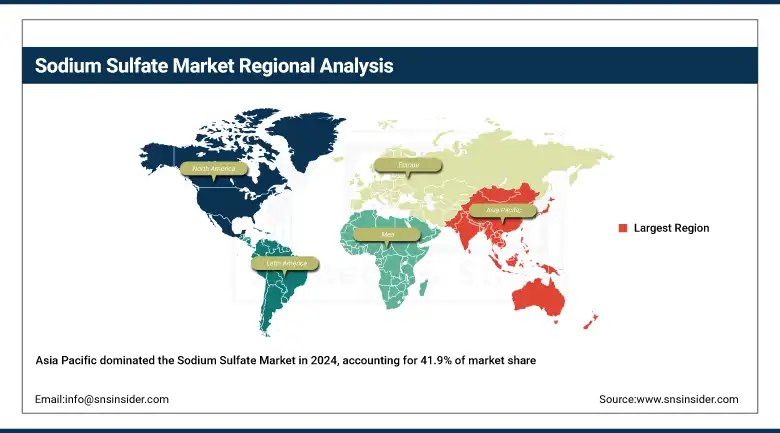

The Asia Pacific region leads the Sodium Sulfate Market Analysis in 2024, commanding a 41.9% share. China dominates the region due to its vast reserves of Natural Sodium Sulfate and aggressive expansion in Synthetic Sodium Sulfate output, used primarily in detergents and paper. The Ministry of Natural Resources of China reported over 3.5 million metric tons in output last year. India follows, with government programs like “Make in India” boosting the detergent and textile sectors. Rising middle-class demand and urbanization across Southeast Asia have also fueled the regional Sodium Sulfate Market Growth significantly.

Get Customized Report as per Your Business Requirement - Enquiry Now

The North American Sodium Sulfate Industry is experiencing rapid growth in 2024, with the U.S. leading the surge due to the rising demand for Anhydrous Sodium Sulfate in phosphate-free detergents and high-grade glass manufacturing. Supported by the U.S. Geological Survey, production reached over 350,000 metric tons in 2023. Eco-conscious trends and innovations in powder detergent formulations are accelerating the Sodium Sulfate Market Growth. Canada is also playing a key role, where Saskatchewan Mining and Minerals expanded exports of Natural Sodium Sulfate, supported by demand in pulp, paper, and laundry sectors across North America.

Europe holds the second-largest Sodium Sulfate Market Share in 2024, led by countries like Germany, France, and Italy, with Germany at the forefront. The region’s stringent environmental regulations, such as REACH, are driving the shift to phosphate-free detergents, where Synthetic Sodium Sulfate is essential. Eurostat reported a steady increase in the consumption of eco-compliant detergents across Germany and France. Demand for Sodium Sulfate in textile dyeing and glass production also remains strong, particularly in industrial hubs like Frankfurt and Lyon, contributing to robust Sodium Sulfate Market Trends in Western Europe.

Key Players

The major competitors in the sodium sulfate market include Nippon Chemical Industrial Co., Ltd., Elementis PLC, Shikoku Kasei Holdings Corporation, Cooper Natural Resources, Searles Valley Minerals, Godavari Biorefineries Ltd., MINERA DE SANTA MARTA, S.A., Saskatchewan Mining and Minerals Inc., Alkim Alkali Kimya A.Ş., and Sulquisa S.A.

Recent Developments

-

May 2025: Shandong company launched an MVR plant to improve sodium sulfate recovery efficiency and reduce emissions in industrial chemical processes.

-

July 2024: Lupin received FDA tentative approval for generic Sutab® tablets used in colonoscopy prep, with $148M U.S. market value.

-

June 2024: Aepnus Technology raised $8M to develop a system converting sodium sulfate battery waste into reusable chemicals for circular sustainability.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.29 billion |

| Market Size by 2032 | USD 3.31 billion |

| CAGR | CAGR of 4.70% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Nature (Natural, Synthetic) •By Application (Paper & Pulp, Detergents, Glass, Food & Beverage, Others) •By End-User (Household, Industrial, Commercial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Nippon Chemical Industrial Co., Ltd., Elementis PLC, Shikoku Kasei Holdings Corporation, Cooper Natural Resources, Searles Valley Minerals, Godavari Biorefineries Ltd., MINERA DE SANTA MARTA, S.A., Saskatchewan Mining and Minerals Inc., Alkim Alkali Kimya A.Ş., Sulquisa S.A. |

Frequently Asked Questions

The Sodium Sulfate Market is expected to reach USD 3.31 billion by 2032, growing at a 4.70% CAGR.

The Sodium Sulfate Market is led by the detergent industry, accounting for 38.5% due to its filler role in powders.

Glass production in the Sodium Sulfate Market is expanding due to sodium sulfate’s role in lowering furnace temperatures and improving clarity.

Industrial applications in the Sodium Sulfate Market are growing fastest, fueled by demand in textiles, glass, and sustainable packaging.

Key players in the Sodium Sulfate Market include Searles Valley Minerals, Saskatchewan Mining and Minerals, and Elementis PLC.

Get in Touch