Microelectronics Market Report Scope and Overview:

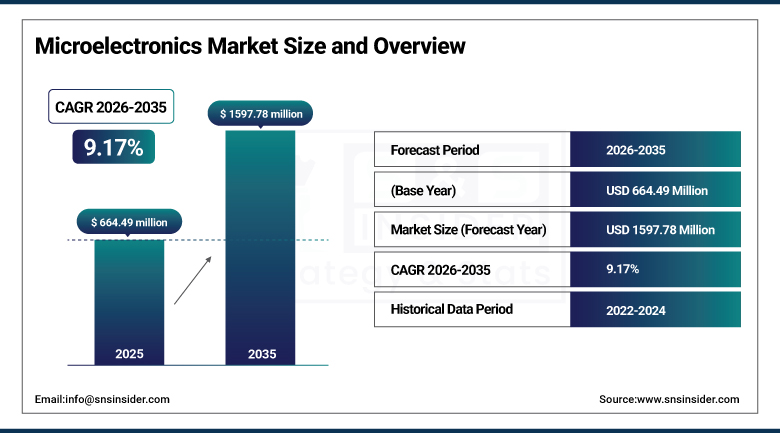

The Microelectronics Market size was valued at USD 664.49 Million in 2025 and is expected to reach USD 1597.78 Million by 2035, growing at a CAGR of 9.17% over the forecast period of 2026-2035.

The global market is expanding because of the modern technologies that widely adopt compact high-performance electronic components for rapid advancement. There is a rise in the demand for solutions that are smarter faster and more energy-efficient in order that microelectronic systems can develop more quickly globally. Continuous innovation in chip design is strengthening market potential. Improved connectivity capabilities with increased functionality at reduced sizes also contribute. Additionally, new opportunities are created by strong R&D investments coupled with breakthroughs in semiconductor manufacturing, and these opportunities enable common application of microelectronics in next-generation digital infrastructure and smart systems.

According to research, over 80% of new vehicles sold globally in 2024 featured at least Level 1 or Level 2 ADAS capabilities powered by microelectronic control units.

Microelectronics Market Size and Forecast:

-

Market Size in 2025 USD 664.49 Million

-

Market Size by 2035 USD 1,597.78 Million

-

CAGR CAGR of 9.17% from 2026 to 2035

-

Base Year 2025

-

Forecast Period 2026–2035

-

Historical Data 2022–2024

To Get More Information On Microelectronics Market - Request Free Sample Report

Microelectronics Market Highlights:

-

Product and technology innovation showcased at CES 2026 highlights advanced touch controllers, AI-enabled hardware, and smart transportation solutions, reflecting deeper integration of microelectronics with autonomous mobility and intelligent infrastructure

-

Regional value chain strengthening efforts in Québec focus on developing secure microelectronic and photonic ecosystems to support aerospace, electric vehicles, energy, defense, and life sciences industries

-

Government and policy support across North America is accelerating microelectronics research, education, and workforce development to strengthen domestic semiconductor capabilities

-

Capital market activity is rising as Highness Microelectronics files its DRHP for a BSE SME IPO, indicating growing investor interest in emerging microelectronics manufacturers

-

Ecosystem collaboration among industry players, academic institutions, and government bodies is driving innovation in advanced packaging, photonics, and semiconductor manufacturing infrastructure

-

Overall market outlook remains positive, supported by continuous innovation, strategic investments, and expanding applications across transportation, industrial, and digital technology sectors

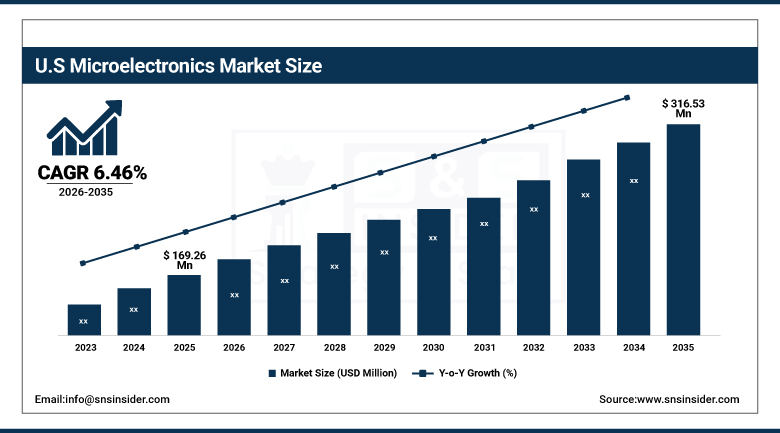

The U.S. Microelectronics Market size was USD 169.26 million in 2025 and is expected to reach USD 316.53 million by 2035, growing at a CAGR of 6.46% over the forecast period of 2026–2035.The US microelectronics market growth is mainly driven by government funding that rises because of advanced semiconductor research, electric vehicles are increasingly adopted, also leading technology firms are strongly present. Additionally, the healthcare electronics segment expands along with military-grade components being in demand, greatly accelerating the market within the country.

According to research, over 65% of wearable health devices sold globally are developed or manufactured in the U.S., including fitness trackers, glucose monitors, and portable ECGs.

Microelectronics Market Drivers:

-

Surging demand for miniaturized, power-efficient electronics accelerates microelectronics adoption across key industries globally

Microelectronics are increasingly integrated into compact devices such as smartphones, wearable gadgets, and medical instruments due to the rising demand for miniaturization and enhanced energy efficiency. These compact components support advanced functionalities while conserving space and power, making them essential in consumer electronics, automotive infotainment, and healthcare monitoring systems. The push for smart, interconnected devices in the age of IoT and Industry 4.0 amplifies this trend, encouraging manufacturers to invest in next-generation microelectronics with low-power consumption and high-performance output.

According to research, Modern smartphones include over 50 microelectronic chips per unit, many optimized for low power consumption and form factor efficiency.

Microelectronics Market Restraints:

-

Complexity in integration with legacy systems restricts large-scale deployment across traditional industries

Many industries, particularly in manufacturing and utilities, operate with legacy infrastructure that lacks compatibility with modern microelectronics. Integrating intelligent chips into these systems requires substantial upgrades, software overhauls, and retraining of personnel. This complexity creates resistance to adoption and can delay transition timelines. Additionally, the risk of system disruption during retrofitting adds to concerns, reducing enthusiasm among traditional sectors to fully embrace smart microelectronic technologies despite their long-term benefits.

Microelectronics Market Opportunities:

-

Emergence of 5G, IoT, and AI-based systems unlocks new demand for intelligent and real-time microelectronic components

The widespread rollout of 5G networks and proliferation of smart devices drive strong demand for microelectronic components with ultra-low latency, real-time processing, and energy-efficient operations. Edge computing, connected homes, smart factories, and AI-driven robotics all require integrated sensors, processors, and RF components. This trend creates massive opportunities for microelectronics manufacturers to design application-specific integrated circuits (ASICs) and system-on-chips (SoCs) tailored to these advanced technologies, further diversifying revenue streams.

According to research, over 70% of new IoT and AI devices launched in 2025 will rely on custom SoCs to meet space, power, and processing efficiency needs in edge applications.

Microelectronics Market Segment Analysis:

By Software & Algorithm

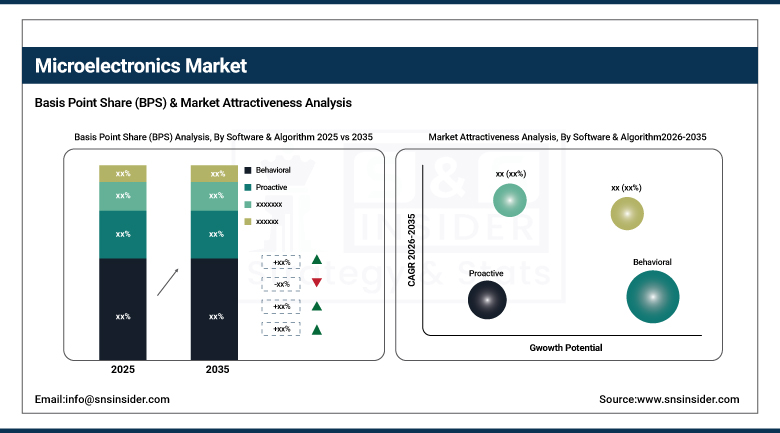

The Behavioral segment dominated the Microelectronics Market in 2025 with the highest revenue share of about 63.86% due to its proven effectiveness in reactive system management and real-time decision-making. Widely adopted across industrial automation, security, and consumer electronics, behavioral algorithms enable systems to respond to existing conditions efficiently. Microelectronics companies like Analog Devices Inc. have capitalized on this demand by integrating advanced behavioral logic into their signal processing solutions, enhancing performance. High adoption in smart infrastructure and energy systems solidifies its leadership.

The Proactive segment is expected to grow at the fastest CAGR of about 8.95% from 2026 to 2035, driven by rising demand for predictive and preventive technologies across industries. Increasing reliance on AI and machine learning to anticipate system needs is fueling rapid growth. Qualcomm Technologies is actively developing proactive microelectronic solutions using embedded intelligence for dynamic optimization. Industries such as healthcare, automotive, and aerospace are integrating proactive algorithms to ensure intelligent foresight, leading to its accelerated adoption and expansion.

By Product

The HVAC Control segment dominated the Microelectronics Market in 2025 with a revenue share of about 34.87%, supported by increasing demand for energy-efficient and smart building solutions. Widespread integration in residential and commercial spaces has propelled this segment’s growth. Honeywell International Inc. has been at the forefront, offering microelectronic HVAC systems with advanced sensors and automation. Enhanced indoor climate control and regulations promoting sustainability continue to drive dominance in this category across developed and developing markets alike.

The Lighting Control segment is projected to grow at the fastest CAGR of about 9.46% from 2026 to 2035 due to growing smart city initiatives and rising demand for energy-efficient lighting solutions. The integration of IoT-enabled systems is accelerating adoption. Signify N.V. (formerly Philips Lighting) is a leading innovator in smart lighting microelectronics, focusing on adaptive lighting and connected infrastructure. Technological advances in automation and wireless controls make intelligent lighting systems more accessible, fueling rapid growth in this segment.

By Type

The Transistors segment dominated the Microelectronics Market share of about 31.66% in 2025, owing to its critical role in almost all electronic devices. These components are indispensable in processors, amplifiers, and logic circuits. Texas Instruments Inc. maintains a strong market presence through its extensive portfolio of high-performance transistors for computing and automotive electronics. Their scalability, efficiency, and reliability ensure continued demand across legacy and emerging technologies, reinforcing the segment’s leadership.

The Capacitors segment is projected to grow at the fastest CAGR of about 9.40% from 2026 to 2035, driven by growing needs in energy storage, signal filtering, and power management. With the proliferation of EVs and renewable systems, demand is surging. Murata Manufacturing Co., Ltd. is innovating with miniaturized, high-capacitance ceramic capacitors for next-gen devices. Advances in materials and applications across industrial and consumer sectors are accelerating this segment’s growth trajectory in the years ahead.

By End Use Industry

The Automotive segment dominated the Microelectronics Market in 2025 with the highest revenue share of about 34.30%, due to widespread adoption in ADAS, infotainment, and powertrain control systems. The surge in EV and autonomous vehicle production intensifies component demand. NXP Semiconductors is a key provider of automotive-grade microcontrollers and radar solutions that are vital to modern vehicles. OEMs' investment in electronic system integration keeps the automotive sector at the forefront of microelectronics consumption.

The Medical segment is expected to grow at the fastest CAGR of about 9.30% from 2026 to 2035, driven by advancements in healthcare electronics and the rise of wearable technologies. Demand for compact, efficient, and reliable components is expanding rapidly. Medtronic plc is leading innovation in implantable and diagnostic microelectronics, improving patient monitoring and therapy delivery. Telehealth growth and the aging population are also supporting increased adoption of medical-grade microelectronic systems globally.

Microelectronics Market Regional Analysis:

North America Microelectronics Market Trends:

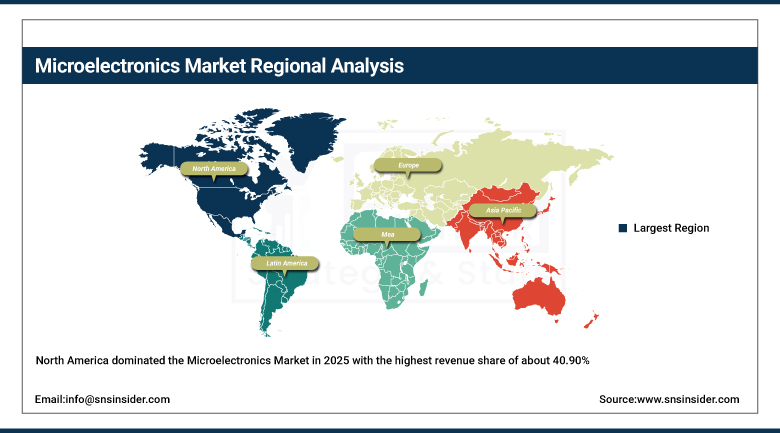

North America dominated the Microelectronics Market in 2025 with the highest revenue share of about 40.90%, driven by the presence of key market players, robust R&D investments, and advanced technological infrastructure. The U.S. leads in semiconductor manufacturing, defense electronics, and high-end computing applications. Strong demand from automotive, aerospace, and healthcare sectors further boosts market growth. Supportive government initiatives, such as the CHIPS Act, continue to foster innovation and ensure the region's leading position in microelectronics development and adoption.

The U.S. dominates the North American microelectronics market due to strong R&D infrastructure, the presence of leading semiconductor companies, and substantial government funding. Its advanced manufacturing capabilities and high demand from sectors like defense, healthcare, and automotive drive consistent market leadership.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia-Pacific Microelectronics Market Trends:

Asia Pacific is expected to grow at the fastest CAGR of about 9.13% from 2026 to 2035 due to increasing industrialization, rising consumer electronics demand, and expanding semiconductor manufacturing capabilities in countries like China, Taiwan, and South Korea. Government support for digital infrastructure, smart manufacturing, and electric mobility is driving investments in microelectronics. The region’s cost-competitive manufacturing and supply chain strength are attracting global players, while domestic innovations in 5G, AI, and IoT accelerate regional market expansion.

China’s dominance in the Asia Pacific microelectronics market stems from its vertically integrated supply chain, cost-efficient production, and vast domestic demand. With aggressive investments in fabrication facilities and strategic partnerships, China is rapidly advancing its capabilities in chip design and innovation.

Europe Microelectronics Market Trends:

Europe plays a vital role in the global microelectronics market, driven by robust innovation in automotive electronics, industrial automation, and healthcare technologies. Countries like Germany and France lead in R&D and chip design, while the European Chips Act aims to strengthen regional semiconductor independence. Growing demand for green energy solutions and IoT integration is also accelerating market growth across the continent.

Germany leads due to its strong semiconductor manufacturing base, advanced automotive electronics industry, and significant investments in Industry 4.0 technologies. The presence of key players like Infineon Technologies and robust R&D infrastructure further strengthen its market position across Europe.

Latin America and Middle East & Africa Microelectronics Market Trends:

In the Middle East & Africa, Saudi Arabia leads due to its strong investments in smart city projects like NEOM, digital infrastructure, and industrial automation. Meanwhile, in Latin America, Brazil dominates the market, driven by its expanding electronics manufacturing sector, government-backed innovation programs, and rising demand in automotive and consumer electronics segments.

Microelectronics Market Competitive Landscape:

Intel Corporation, established in 1968 in Santa Clara, California, is a global leader in microelectronics, specializing in processors, chipsets, memory, and semiconductor solutions. Renowned for innovation in CPUs, AI, and data center technologies, Intel serves computing, automotive, and IoT markets worldwide, driving performance, efficiency, and digital transformation.

-

In March 2025, Intel’s new CEO announced a strategic overhaul to revitalize AI-focused manufacturing, positioning Intel Foundry to build chips for external customers like Nvidia and Broadcom, signaling a renewed push into high-performance AI processors.

Qualcomm Technologies Inc., founded in 1985 in San Diego, California, is a leading semiconductor and telecommunications company. Specializing in mobile processors, 5G chipsets, IoT solutions, and wireless technologies, Qualcomm drives innovation in smartphones, automotive, and networking markets globally, enabling advanced connectivity, AI integration, and next-generation communication standards.

-

In May 2025, Qualcomm unveiled a strategic shift toward AI and AR, launching Snapdragon X‑series CPUs for Copilot+ PCs and announcing partnerships in wearables and edge AI, marking expanded chip diversification.

Microelectronics Market Key Players:

-

Intel Corporation

-

Samsung Electronics

-

Taiwan Semiconductor Manufacturing Company (TSMC)

-

Qualcomm Technologies Inc.

-

Texas Instruments

-

Broadcom Inc.

-

STMicroelectronics

-

NXP Semiconductors

-

Analog Devices Inc. (ADI)

-

Infineon Technologies AG

-

Micron Technology Inc.

-

SK Hynix Inc.

-

NVIDIA Corporation

-

Advanced Micro Devices (AMD)

-

Maxim Integrated (now part of ADI)

-

Renesas Electronics Corporation

-

ON Semiconductor (ON Semi)

-

Cadence Design Systems

-

Marvell Technology, Inc.

-

Microchip Technology Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 664.49 Million |

| Market Size by 2035 | USD 1597.78 Million |

| CAGR | CAGR of 9.17% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Software & Algorithm (Behavioral, Proactive) • By Product (Lighting Control, Security & Access Control, Entertainment Control, HVAC Control, Other Control) • By Type (Transistors, Capacitors, Inductors, Resistor, Insulators) • By End Use Industry (Aerospace & Defense, Medical, Construction, Automotive, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Intel Corporation, Samsung Electronics, Taiwan Semiconductor Manufacturing Company (TSMC), Qualcomm Technologies Inc., Texas Instruments, Broadcom Inc., STMicroelectronics, NXP Semiconductors, Analog Devices Inc. (ADI), Infineon Technologies AG, Micron Technology Inc., SK Hynix Inc., NVIDIA Corporation, Advanced Micro Devices (AMD), Maxim Integrated (now part of ADI), Renesas Electronics Corporation, ON Semiconductor (ON Semi), Cadence Design Systems, Marvell Technology Inc., and Microchip Technology Inc. |

Frequently Asked Questions

Ans: North America dominated the Microelectronics Market in 2025.

Ans: Behavioral segment dominated the Microelectronics Market.

Ans: The major growth factor of the Microelectronics Market is the increasing demand for smart devices, automotive electronics, and IoT integration.

Ans: The Microelectronics Market size was valued at USD 664.49 Million in 2025 and is expected to reach USD 1597.78 Million by 2035

Ans: The Microelectronics Market is expected to grow at a CAGR of 8.04% from 2026-2035.

Get in Touch