Solid State Cooling Market Size & Trends:

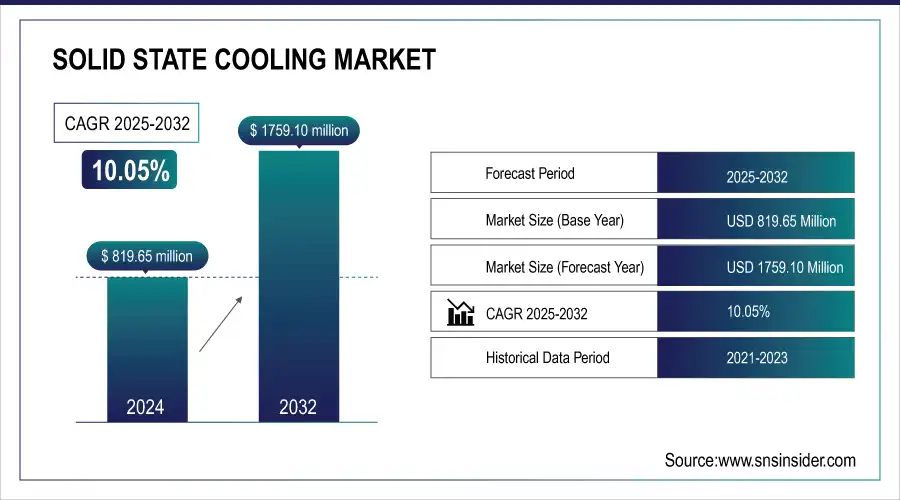

The Solid State Cooling Market size was valued at USD 819.65 million in 2024 and is expected to reach USD 1759.10 million by 2032, growing at a CAGR of 10.05% over the forecast period of 2025-2032. The major factors driving the Solid State Cooling Market are the increasing demand for energy-efficient, and eco-friendly cooling technologies in industries covering up medical devices, consumer electronics, and electric vehicles. Solid state systems are smaller, can offer more precise temperature control, and lead to fewer greenhouse gas emissions than traditional compressor-based cooling methods.

To Get more information On Solid State Cooling Market - Request Free Sample Report

The Solid State Cooling Market growth is driven by the rising adoption of small-footprint, dependable, and energy-saving cooling solutions across various industries, such as healthcare, electronics, and automotive. Solid state cooling is capable of operating with noiselessness, requires virtually no maintenance, will not use harmful refrigerants, and thus fits neatly onto the global sustainability agenda, unlike traditional systems. Continued innovation in thermoelectric, electrocaloric, and magnetocaloric technologies is improving performance and efficiency, which will only propel further uptake. At the same time, the demand for small form factor consumer devices and the emergence of electric vehicle growth are driving further market growth.

-

Researchers at the Hong Kong University of Science and Technology have developed the world's first kilowatt-scale elastocaloric cooling device, capable of stabilizing indoor temperatures at 21°C–22°C within 15 minutes, even when outdoor temperatures reach 30°C–31°C.

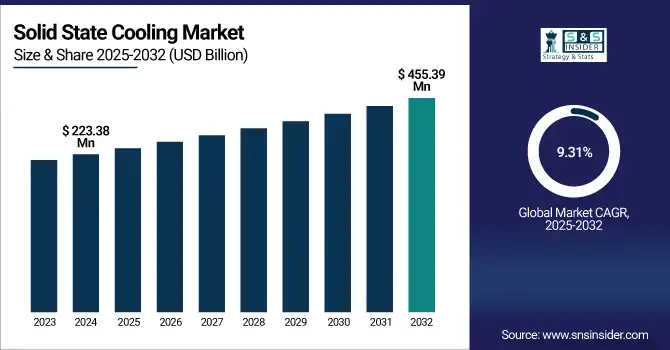

The U.S. Solid State Cooling market size is estimated to be valued at USD 223.38 million in 2024 and is projected to grow at a CAGR of 9.31%, reaching USD 455.39 million by 2032. The rapid development of the U.S. State Cooling business is being fueled by the departure from conventional refrigerant-based devices because of stringent environmental regulations. The market will continue to grow further due to developments in semiconductor production, increasing deployment of precision cooling in defense and medical applications, along with the increasing adoption of smart and noiseless thermal management solutions.

Solid State Cooling Market Dynamics

Key Drivers:

-

Rising Demand for Eco-Friendly Cooling Drives Growth in Solid State Thermal Management Solutions

The major growth contributing to the global Solid State Cooling market is the increasing requirement for eco-friendly as well as energy-efficient cooling solutions in various fields such as healthcare, automotive, and electronics, among others. The advantages of solid state systems, in which the cooling is achieved using technologies such as thermoelectric, electrocaloric, and magnetocaloric cooling, are compact size, low maintenance, noise-free operation, and the elimination of harmful refrigerants, making them useful in sustainability-related applications. As electronic devices undergo increasing miniaturization and electric vehicles proliferate, the demand for cutting-edge thermal management solutions is growing.

-

Laird Thermal Systems introduced the OptoTEC MSX Series in June 2023, featuring compact thermoelectric coolers that offer a 10% increase in cooling capacity within a micro footprint, catering to high-performance image-sensing applications.

Restraints:

-

Material Limits and Efficiency Challenges Restrain Solid State Cooling in Large-Scale Applications

The low cooling efficiency of some solid-state systems, especially compared to traditional refrigerant-based systems that perform better, hampers their use in large-scale cooling applications. Performance and scalability may suffer due to a lack of customary materials and components, leading to another complication. Also, the limited stability of some solid-state cooling devices for long-term operation due to the degradation of materials over time and thermal stability is are challenge.

Opportunities:

-

Future Growth Driven by Green Tech Push and Expanding Use in Electronics, Healthcare, and HPC

The future potential of solid state cooling is in consumer electronics, wearables, and high-performance computing systems. In addition, the government regulation around phasing out hydrofluorocarbon (HFC) refrigerants, coupled with incentive structures that promote green technologies, also aid market growth. Solid state cooling market trends indicate rising adoption across sectors, driven by sustainability and innovation. Growing industrialization and improvement in healthcare infrastructure in emerging economies have likewise driven the adoption of UV light disinfection systems in these regions. Furthermore, continuous R&D in material science is likely to improve performance and cost-effectiveness, leading to new application areas around the world.

-

Recent studies have demonstrated significant advancements in electrocaloric cooling devices. For instance, a device using lead scandium tantalate (PST) multilayer capacitors achieved a temperature span of 13 K, showcasing the potential of electrocaloric materials for efficient cooling solutions

Challenges:

-

Limited Awareness and Infrastructure Hinder Solid-State Cooling Adoption in Emerging Global Markets

Market growth may also be hampered by low awareness and penetration level of solid-state technologies in other sectors, especially in developing regions. However, the slow pace of commercialization due to a lack of infrastructure and market readiness in some regions remains a challenge. Finally, while these technologies, in general, have a low environmental impact, the sustainability of the materials employed for some solid-state systems is still being evaluated, which may prevent wider use.

Solid State Cooling Market Segmentation Outlook:

By Product Type

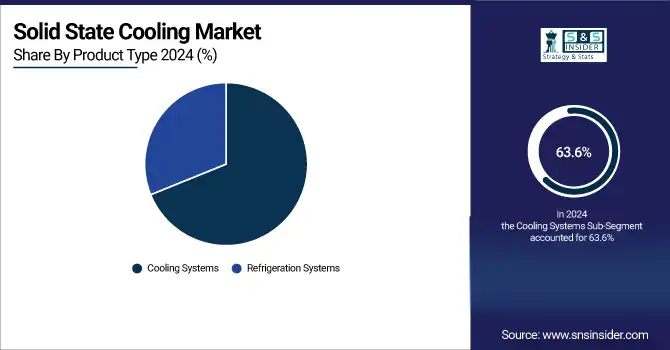

The cooling systems accounted for 63.6% of the solid state cooling market share in 2024. Factors contributing to this dominance include a growing need for advanced thermal management technologies in consumer electronics, high-performance computing, and automotive applications. These solid-state systems and in particular, thermoelectric coolers are advantageous for reasons such as compact size, maintenance-free and noiseless operation, making these well-suited for use in the above industries.

From 2025 and 2032, refrigeration systems will likely be the segment to experience the highest CAGR. This shift is fueled by the increasing demand for green and energy-efficient cooling solutions among markets such as healthcare, food processing, and industrial applications. The solid-state cooling market is experiencing an increased adoption of refrigeration systems, which can competently complement the existing refrigerant systems while keeping in mind the worldwide sustainability targets.

By Type

The single-stage systems in the solid state cooling market share was 47.1% in 2024. Such systems are very popular due to their simple and efficient design, low cost, and good performance in applications ranging from consumer electronics to small refrigeration. Single-stage systems are more efficient at cooling when extreme precision is not necessary, which is why they are often used in commercial or residential applications.

From 2025-2032, multi-stage systems are anticipated to witness the fastest CAGR. It is fueled by the growing need for improved and more efficient cooling capable of managing higher heat loads, particularly in high-performance computing, automotive, and industrial applications. Ideal for applications needing high-accuracy temperature control, multi-stage systems combine multiple stages of cooling.

By Technology

Thermoelectric cooling represented the largest share of the solid state cooling market at 70.4% in 2024. The Peltier effect is used to transfer heat between the two sides of the device, and is thus applied in consumer electronics, automotive systems, portable cooling devices, and much more. The growing popularity of this cycle is mainly due to its small footprint, high reliability, low maintenance requirement, and ability to work without vapor-compression harmful refrigerants, which makes it suitable for size and environmentally constrained applications.

The segment of electrocaloric cooling is projected to witness the highest CAGR from 2025 to 2032. This increase can be attributed to the growth in electrocaloric materials that change temperature with the application of an electric field. KVT offers highly efficient, energy-saving systems with potential applications in more challenging fields like large-scale refrigeration and precision thermal management for high-performance electronics.

By End Use

Healthcare held a 47.3% share of the solid state cooling market in 2024. Strict temperature control is required for portable refrigerators, vaccine storage, and diagnostic equipment in healthcare applications, thus driving the demand for solid-state cooling in the market. For example, solid-state cooling technologies within units such as thermoelectric coolers are reliable and efficient, providing a compact option for energy-efficient temperature control of delicate materials while avoiding the use of environmentally critical refrigerants.

Consumer electronics will grow at the highest CAGR between 2025 and 2032. As devices like smartphones, laptops, and wearables are becoming more miniaturized, the need for ultra-efficient cooling increases as well. But solid-state cooling is becoming a popular technology in this space, as these systems can be made smaller, quieter, and more energy-efficient than conventional solutions, and with ever-smaller and more powerful devices, the future of heat management provides challenges.

Solid State Cooling Market Regional Analysis:

North America accounted for 34.7% of the global solid state cooling market in 2024. The region dominates the thermal management market due to the strong presence of various advanced industries including healthcare, aerospace & defense, and consumer electronics, where there is a growing requirement for energy-efficient, compact and reliable thermal management solutions. The United States is characterized by the presence of key market players along with active R&D, which drives innovation and adoption of solid-state cooling technologies for numerous applications.

Get Customized Report as per Your Business Requirement - Enquiry Now

The solid state cooling market is dominated by the United States in the North America region, owing to the well-established healthcare, electronics, and aerospace sectors, the growing R&D infrastructure, the early adoption of green technologies, and high capital investment in developing innovative thermal management solutions.

During the forecast period, from 2025 to 2032, the Asia Pacific region is anticipated to be the fastest-growing region. China, Japan, South Korea, and India are the major countries leading this growth owing to rapid industrialization, growing electronics manufacturing hubs, and increasing investments in electric vehicles and smart healthcare infrastructure. The regional market adoption is also likely to be accelerated by governmental initiatives to encourage green technologies and the transition towards sustainable cooling solutions.

The Asia Pacific market is dominated by China owing to its huge electronics manufacturing industry, fast industrialization, government initiatives promoting green technologies, investments in electric vehicles, and high-end healthcare infrastructure supporting the need for efficient thermal management solutions.

The market in Europe is characterized by strict environmental regulations, a strong emphasis on sustainability, and significant advancements in material science. The research of thermoelectric & electrocaloric technology is supported by the region and is implemented, fast fast-growing traction in automotive, healthcare, and electronics markets, specifically in Germany, France, and the U.K.

Germany is the largest contributor to the solid state cooling market in Europe, following the automotive and electronics industries, with highly developed R&D capabilities and proactive adoption of sustainable, energy-efficient cooling technologies.

Latin America and the Middle East & Africa (MEA) are new emerging markets in the global solid-state cooling market gradually adopting solid-state cooling technologies due to increasing demand for sustainable and energy-efficient technologies. In Latin America, growth is driven by rising healthcare and consumer electronics investments. Particularly in MEA, urbanization and better medical infrastructure are creating interest. Despite a currently limited market due to technology awareness and infrastructure, continued development initiatives and a supportive climate for solid-state cooling will help propel global demand over the next few years.

Key Players:

Some of the major Solid State Cooling companies are Thermoelectric Cooling America, Cooler Master, II-VI Incorporated, Alphabet Energy, RTP Company, Laird Thermal Systems, Kryotherm, MicroCool, Calyos, and Ouroboros Technologies and others.

Recent Developments:

-

In October 2024, Cooler Master introduced next-generation cooling solutions for Intel Core Ultra 200S CPUs, compatible with the new LGA1851 socket and RL-ILM standard. The lineup includes MasterLiquid Ion, Atmos, and Core Series, along with various air and liquid cooling options.

-

In June 2024, Laird Thermal Systems launched the SuperCool X Series, featuring next-gen thermoelectric coolers that improve performance by up to 10%. The eco-friendly units offer up to 400W cooling capacity, ideal for tight-space applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 819.65 Million |

| Market Size by 2032 | USD 1759.10 Million |

| CAGR | CAGR of 10.05% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Refrigeration Systems and Cooling Systems) • By Type (Single Stage, Multi-Stage, and Thermocycler) • By Technology (Electrocaloric Cooling, Magnetocaloric Cooling, and Thermoelectric Cooling) • By End Use (Consumer Electronics, Healthcare, Automotive, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Thermoelectric Cooling America, Cooler Master, II-VI Incorporated, Alphabet Energy, RTP Company, Laird Thermal Systems, Kryotherm, MicroCool, Calyos, and Ouroboros Technologies. |