Space Economy Market Report Scope & Overview:

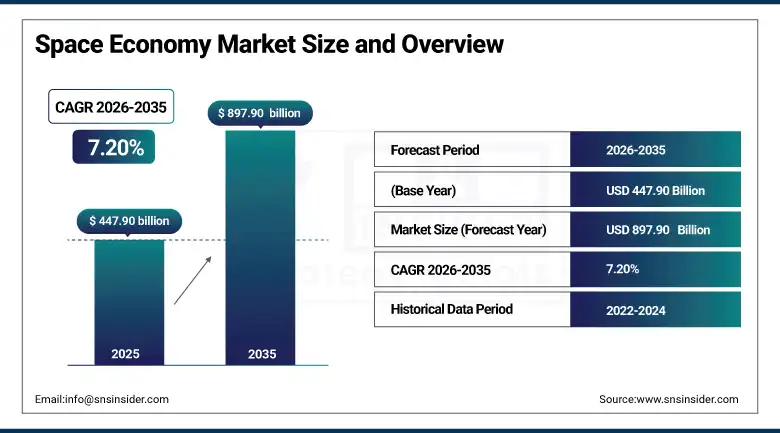

The Space Economy market was valued at USD 447.90 billion in 2025 and is expected to reach USD 897.90 billion by 2035, growing at a CAGR of 7.20% from 2026–2035.

The space economy encompasses the full spectrum of economic activity enabled by or dependent upon access to outer space, spanning the manufacturing and launch of satellites providing communications, navigation, earth observation, and scientific research services; the space launch vehicle industry transporting government and commercial payloads from terrestrial launch facilities to low Earth orbit and beyond the ground infrastructure of control stations, antenna networks, and data processing centers that operate space systems and distribute their services; the applications and services layer where satellite-enabled capabilities including broadband internet, GPS navigation, weather forecasting, agricultural monitoring, disaster response coordination, and financial transaction timing are translated into commercial products consumed by billions of daily users; and the emerging frontiers of crewed space tourism, in-space manufacturing, and resource extraction that represent the nascent industries whose commercial development over the next decade will define whether humanity establishes a permanent and self-sustaining economic presence beyond Earth's atmosphere.

NASA's 2025 economic impact assessment estimating that the U.S. space economy generates over USD 200 billion in direct economic activity while enabling over USD 2 trillion in downstream economic value through GPS-enabled commerce, weather-dependent industry, and satellite communication-dependent business activities provides the most comprehensive quantification of space systems' foundational role in the modern global economy.

Space Economy Market Size and Forecast

-

Market Size in 2026E: USD 480.15 Billion

-

Market Size by 2035: USD 897.90 Billion

-

CAGR: 7.20% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Space Economy Market - Request Free Sample Report

Space Economy Market Trends

-

Explosive growth of low Earth orbit satellite mega constellations including SpaceX Starlink, Amazon Kuiper, OneWeb, and emerging Chinese constellations that are collectively deploying tens of thousands of small satellites to provide global broadband internet coverage, creating the largest satellite manufacturing and launch volume in history and fundamentally reshaping the economics and competitive dynamics of both the satellite manufacturing and launch services sectors.

-

Accelerating commercialization of reusable launch vehicle technology pioneered by SpaceX's Falcon 9 and Falcon Heavy boosters, now being pursued by Blue Origin, United Launch Alliance, Ariane 6, and emerging Asian launch vehicle developers, that is progressively reducing per-kilogram launch costs from the tens of thousands of dollars per kilogram of early satellite launches toward hundreds of dollars per kilogram at full reusability maturity.

-

Growing private sector investment in crewed commercial space stations to succeed the International Space Station, where Axiom Space, Blue Origin, and Northrop Grumman are developing commercial orbital infrastructure designed to serve not only government research users but also commercial manufacturing in microgravity, space tourism accommodation, and media production in the novel environment of orbital space.

-

Rising application of artificial intelligence and machine learning in satellite constellation management, autonomous spacecraft navigation, earth observation data analysis, and space situational awareness that is transforming the information processing capabilities of space systems and creating new space-derived data services whose commercial value exceeds the satellite infrastructure that generates the data.

-

Expanding international government space programme investment across China, India, UAE, Japan, South Korea, and European nation programmes that is broadening space capability beyond the traditional U.S.-Russia duopoly, creating new national launch vehicle programmes, satellite manufacturing capabilities, and space exploration ambitions that are simultaneously expanding the global space economy's scale and increasing competitive intensity across its commercial segments.

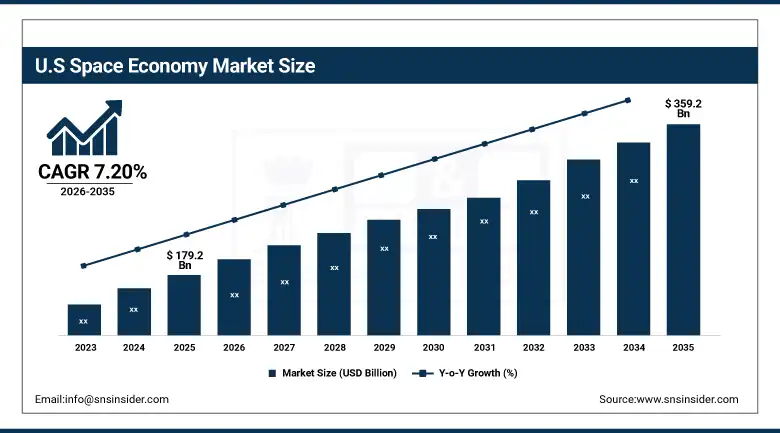

The U.S. Space Economy Market Outlook

The U.S. Space Economy Market was valued at approximately USD 179.2 billion in 2025 and is expected to reach approximately USD 359.2 billion by 2035, growing at a CAGR of 7.20%.

The United States commands the global space economy through the combination of the world's most commercially active launch sector where SpaceX alone has achieved over 90% of global commercial launch market share through its reusable Falcon 9 system's cost and cadence advantages over all current competitors, NASA's over USD 25 billion annual budget that sustains the Artemis lunar exploration programme, Mars exploration missions, the James Webb Space Telescope operations, and commercial crew transportation that collectively advance human space exploration while generating technology transfer benefits to the commercial sector, and the Department of Defense's enormous space system procurement sustaining intelligence satellite, missile warning, communications, and space situational awareness capabilities that represent the most classified and strategically sensitive component of the national space programme.

The U.S. Space Force's establishment as a separate military branch and its growing procurement of commercial space services through Other Transaction Authority agreements that bypass traditional defense acquisition bureaucracy is creating a new and expanding government commercial space customer whose programmatic flexibility and responsiveness is enabling U.S. commercial space companies to develop dual-use capabilities serving both commercial markets and national security requirements simultaneously.

Space Economy Market Segment Analysis

-

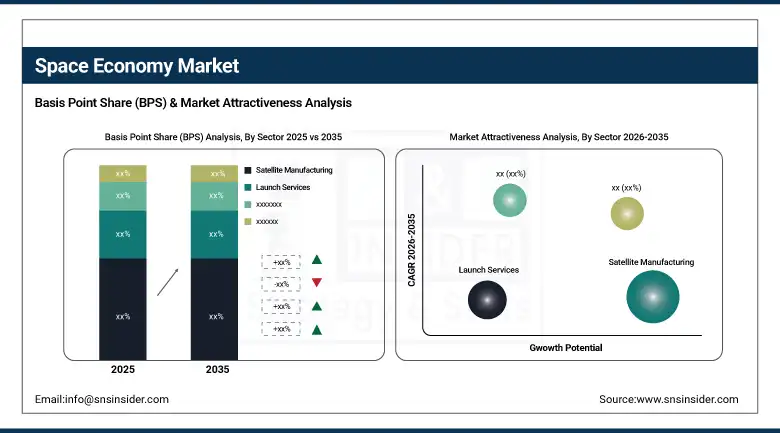

By Sector, Satellite Manufacturing dominated with approximately 32.45% in 2025; Space Tourism is the fastest-growing at a CAGR of 9.80%.

-

By Application, Telecommunications dominated with approximately 28.67% in 2025; Earth Observation is the fastest-growing application as AI-powered analysis of satellite imagery creates new commercial intelligence services across agriculture, insurance, environmental monitoring, and defense.

-

By End User, Government & Defense dominated as the anchor customer for the space economy's highest-value capabilities including intelligence satellites, early warning systems, secure communications, and space situational awareness; Commercial Companies are the fastest-growing end user category as the commercial space economy develops services and revenue models independent of government contracting.

By Sector, Satellite Manufacturing dominates, space tourism is expected to grow fastest

Satellite Manufacturing retained the dominant sector position with approximately 32.45% of space economy market revenues in 2025, reflecting the anchoring commercial importance of spacecraft production as the physical foundation upon which all space services depend, where the sustained demand from government defense and intelligence programmes for exquisite high-capability satellites, the explosive commercial demand from LEO broadband constellation operators deploying thousands of small satellites on accelerated schedules, and the civil government science and Earth observation missions from agencies including NASA, ESA, JAXA, and ISRO collectively sustain a large and diversifying satellite manufacturing market.

Space Tourism is the fastest-growing sector at a CAGR of 9.80% through 2035, representing the nascent but rapidly commercializing market for human spaceflight experiences that Blue Origin's New Shepard suborbital programme, SpaceX's Dragon spacecraft orbital tourism missions, and Axiom Space's commercial ISS visits are collectively developing into a commercially viable premium experiential travel category whose growth trajectory will be determined by the rate at which reusable launch vehicle economics can bring ticket prices from their current multi-million-dollar levels toward the hundreds of thousands of dollar range that dramatically expands the addressable high-net-worth consumer market.

By Application, Telecommunications dominates, earth observation is expected to grow fastest

Telecommunications retained the dominant application position with approximately 28.67% of space economy market revenues in 2025, encompassing the satellite-based communications services that provide connectivity across the full spectrum from traditional geostationary broadcast and fixed broadband services through the revolutionary LEO broadband constellation services that Starlink has demonstrated can deliver consumer-grade internet access with genuinely competitive speeds and latency to previously unserved rural and remote locations globally.

Earth Observation is the fastest-growing application as the combination of dramatically improved satellite imagery resolution, multi-spectral and SAR sensing capabilities, high revisit frequency from large constellations enabling near-daily complete Earth coverage, and AI-powered analytical platforms that automatically extract commercially valuable intelligence from raw imagery data are creating a rapidly expanding market for satellite-derived geospatial intelligence services across every sector that depends on accurate, timely, and comprehensive information about physical conditions on the Earth's surface.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

88.2% |

|

Europe |

France |

32.4% |

|

Asia Pacific |

China |

48.6% |

|

Middle East & Africa |

UAE |

34.7% |

|

Latin America |

Brazil |

41.3% |

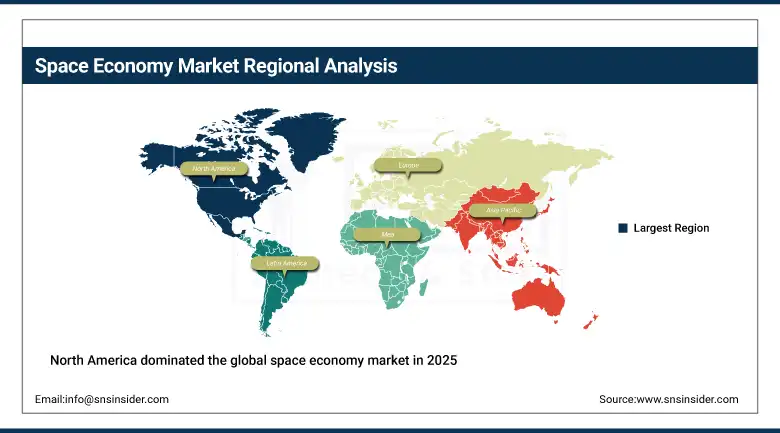

North America Space Economy Market Insights

North America dominated the global space economy market in 2025, with the United States accounting for approximately 88.2% of North American revenues as the world's largest national space economy by a substantial margin. The region's dominance reflects the extraordinary concentration of the world's most capable and commercially active space companies including SpaceX, Boeing, Lockheed Martin, Northrop Grumman, Raytheon Technologies, General Dynamics, and hundreds of emerging commercial space companies whose combined annual space-related revenue exceeds that of all other nations combined. The unique commercial dynamism of the U.S. space sector, where private venture capital investment has created SpaceX as a company valued at over USD 350 billion that has single-handedly transformed global launch market economics, demonstrates the extraordinary commercial scale that the American private space industry has achieved beyond the government-funded institutional base that characterizes space sectors in all other major space nations.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Space Economy Market Insights

Europe is a substantial and technically sophisticated space economy anchored by ESA's civil space programme, the French national CNES space agency, Arianespace's commercial launch operations, Airbus Defense & Space and Thales Alenia Space's satellite manufacturing capabilities, and a growing commercial new space sector across the United Kingdom, Germany, Italy, Spain, and Luxembourg that is developing small satellite manufacturing, commercial launch services, and space applications in the spirit of ESA's Business Incubation Centers and national space agency startup support programmes. France accounts for approximately 32.4% of European space economy revenues through its central role in ESA governance, the presence of Airbus Defense & Space headquarters in Toulouse, and the Guiana Space Centre providing Europe's primary orbital launch facility. The Ariane 6 vehicle's qualification following development delays represents a critical capability restoration for European institutional launch access independence that is strategically important for ESA member states seeking to maintain autonomous access to space.

Asia Pacific Space Economy Market Insights

Asia Pacific is the fastest-growing regional space economy, driven by China's extraordinary and sustained investment in national space capabilities spanning crewed lunar exploration through the Chang'e programme, the Tiangong space station operations hosting both government and commercial research, commercial satellite constellation development by Spacesail, Galaxyspace, and emerging LEO broadband operators, and a rapidly expanding commercial launch sector led by LandSpace and iSpace whose reusable rocket development is following SpaceX's commercial template. China accounts for approximately 48.6% of Asia Pacific space economy revenues as the region's most comprehensive national space programme. India's ISRO commercial subsidiary NewSpace India Limited and the Chandrayaan lunar exploration programme combined with the liberalization of Indian space sector regulations allowing private company participation are creating a rapidly developing national space commercial ecosystem that is positioning India as the developing world's most significant emerging space economy.

MEA & Latin America Space Economy Market Insights

The Middle East and Africa and Latin America are developing space economies where ambitious national space programme investment in Gulf Cooperation Council countries, growing satellite services consumption, and in the case of the UAE an internationally recognized space exploration achievement through the Hope Mars Mission is creating institutional foundations for broader space economy development. UAE leads MEA space economy revenues at approximately 34.7% of regional revenues through its Mohammed bin Rashid Space Centre's ambitious exploration and Earth observation satellite programme, the UAE Space Agency's commercial space sector development initiatives, and the country's positioning as a regional hub for space technology companies seeking Middle Eastern market access. Brazil leads Latin American space economy revenues at approximately 41.3% through the AEB national space agency's satellite development programme, Brazil's Alcantara launch center whose equatorial location provides commercial launch efficiency advantages, and the Brazilian commercial space sector's growing involvement in earth observation data services.

Market Dynamics

Growth Drivers: Advancements in reusable launch vehicles, rapid expansion of LEO satellite constellations, and growing commercial space applications are driving market growth.

The primary structural growth drivers for the space economy market are the technological revolution in launch vehicle economics enabled by SpaceX's demonstrated reusability that has reduced launch costs by 90% or more from pre-Falcon 9 reference prices and created the economic conditions for satellite constellation architectures deploying thousands of spacecraft that would have been commercially infeasible at previous launch prices, combined with the resulting explosion of commercial satellite applications whose expanding capabilities across broadband connectivity, Earth intelligence, and precision navigation are penetrating new industry vertical markets in agriculture, energy, finance, maritime, logistics, and defense whose operational decisions are being transformed by access to continuous, comprehensive, and high-resolution satellite-derived data that redefines what is possible in operational intelligence gathering and decision support.

Restraints: Orbital congestion, high space infrastructure costs, and launch schedule uncertainties are limiting market growth and satellite deployment activities.

A significant restraint on the space economy market is the growing orbital congestion problem created by the proliferation of active satellites and accumulating debris objects in low Earth orbit, where the combination of tens of thousands of existing satellites and debris fragments with the tens of thousands of new satellites planned by LEO constellation programmes creates a long-term collision risk environment that threatens the operational sustainability of the orbital environment on which the entire space economy depends. The ESA and NASA debris tracking networks have documented a significant increase in conjunction events requiring avoidance manoeuvres by active satellites, and the Kessler Syndrome theoretical cascade scenario where collisions generate debris that cause further collisions in a runaway chain represents the existential operational risk that space situational awareness investment and active debris removal technology development are being mobilized to address.

Opportunities: In-space manufacturing, lunar infrastructure development, and space-based solar power technologies are creating new long-term growth opportunities.

The commercialization of in-space manufacturing as a distinct economic activity, where the unique physical environment of microgravity enables the production of biological materials, optical fibre, advanced alloys, and pharmaceutical crystals with properties unachievable through terrestrial manufacturing, represents a potentially transformative commercial frontier whose development by companies including Axiom Space, Varda Space Industries, and Space Forge is creating the first genuinely novel manufacturing applications for space beyond the satellite services and launch services that have constituted the space economy's commercial foundation for decades. The Artemis programmer’s commitment to return humans to the Moon and establish a sustainable lunar presence is creating a long-term infrastructure development demand, encompassing lunar surface transportation, habitat systems, power generation, in-situ resource utilisation for propellant production, and communication relay networks, that will generate substantial procurement activity for commercial space companies over the 2026 to 2035 forecast period.

Recent Developments:

-

January 2025: SpaceX launched Starship SN25 on its first fully integrated orbital test flight demonstrating advanced reusability and heavy-lift potential for planetary missions, while simultaneously deploying 60 Starlink satellites as part of the global broadband coverage expansion that represents the most commercially significant ongoing satellite constellation deployment programme in the market's history.

-

July 2025: Blue Origin flew its tenth crewed New Shepard suborbital flight, upgrading passenger experience capabilities and demonstrating the operational maturity required for commercial space tourism scalability, while advancing preparations for New Glenn orbital launch operations targeting the commercial satellite launch market with a heavy-lift reusable rocket designed to compete with SpaceX Falcon 9.

-

October 2025: NASA's Artemis III lunar lander passed its first key qualification test, advancing the programme toward its goal of returning humans to the Moon's surface and establishing the commercial and government procurement frameworks that will define the emerging lunar economy over the following decade.

Space Economy Market Key Players

-

SpaceX

-

Boeing Defense, Space & Security

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Raytheon Technologies (RTX)

-

Airbus Defence & Space

-

Thales Alenia Space

-

Maxar Technologies

-

Planet Labs PBC

-

Amazon (Kuiper Systems)

-

Blue Origin

-

Virgin Galactic Holdings

-

SES S.A.

-

Intelsat S.A.

-

Eutelsat Communications

-

OneWeb (Eutelsat)

-

Axiom Space Inc.

-

Rocket Lab USA Inc.

-

United Launch Alliance (ULA)

-

Arianespace

Space Economy Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 447.90 Billion |

| Market Size by 2035 | USD 897.90 Billion |

| CAGR | CAGR of 7.20% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Sector (Satellite Manufacturing, Launch Services, Ground Equipment, Space Applications & Services, Space Tourism, Space Mining, Others) • By Application (Telecommunications, Earth Observation, Navigation & Positioning, Scientific Research, Defense & Security, Others) • By End User (Government & Defense, Commercial Companies, Civil/Dual-Use) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SpaceX, Boeing Defense, Space & Security, Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies (RTX), Airbus Defence & Space, Thales Alenia Space, Maxar Technologies, Planet Labs PBC, Amazon (Kuiper Systems), Blue Origin, Virgin Galactic Holdings, SES S.A., Intelsat S.A., Eutelsat Communications, OneWeb (Eutelsat), Axiom Space Inc., Rocket Lab USA Inc., United Launch Alliance (ULA), and Arianespace. |

Frequently Asked Questions

North America dominated the Space Economy Market in 2025, with the United States as the undisputed global leader.

Satellite Manufacturing dominated with approximately 32.45% of revenues in 2025.

Reusable launch vehicle technology revolutionizing access-to-space economics combined with LEO satellite constellation expansion creating unprecedented satellite manufacturing and launch demand, and commercial space applications penetrating new industry verticals through AI-powered satellite data analytics.

The Space Economy Market was valued at USD 447.90 billion in 2025.

The Space Economy Market is expected to grow at a CAGR of 7.20% from 2026 to 2035.

Get in Touch