Aerospace Bearings Market Report Scope & Overview:

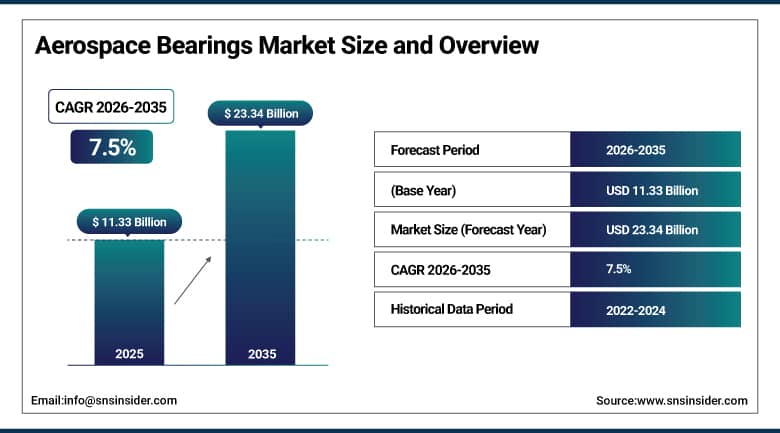

The Aerospace Bearings Market was valued at USD 11.33 Billion in 2025 and is expected to reach USD 23.34 Billion by 2035, growing at a CAGR of 7.5% from 2026–2035.

The Aerospace Bearings Market is witnessing strong growth due to the increase in the number of passengers flying worldwide and an increase in aircraft production. The rising commercial aircraft fleet size and demand for energy-efficient and lightweight aircraft has been promoting the adoption of aerospace bearings. In addition, growing defense budgets and modernization of military aircraft have aided market growth. There has been innovation in the form of enhanced performance, corrosion resistance, and longevity of aerospace bearings which are contributing towards making their operations more efficient.

According to the International Air Transport Association, global air passenger traffic has recovered to record levels post-pandemic and is expected to continue growing annually, with long-term demand projected to double over the coming decades. According to the Airbus Global Market Forecast, the world will require over 40,000 new passenger and freighter aircraft by 2042, driven by rising air travel demand. Furthermore, the Boeing Commercial Market Outlook estimates that the global fleet size will nearly double over the next 20 years, significantly increasing demand for critical aircraft components, including high-performance aerospace bearings.

Aerospace Bearings Market Size and Forecast:

-

Market Size in 2026E: USD 12.17 Billion

-

Market Size by 2035: USD 23.34 Billion

-

CAGR: 7.5% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Aerospace Bearings Market - Request Free Sample Report

Aerospace Bearings Market Trends:

-

Rising aircraft production and growing commercial aviation fleet expansion driving strong demand for high-performance aerospace bearings

-

Increasing adoption of lightweight, high-strength materials such as ceramic and hybrid bearings to improve fuel efficiency and reduce maintenance needs

-

Growing focus on aircraft reliability and safety standards boosting the use of advanced precision bearings in critical aerospace systems

-

Expanding investments in defense modernization and military aircraft upgrades supporting demand for durable, high-load-capacity bearing systems

-

Continuous technological advancements in bearing design, lubrication systems, and temperature resistance enhancing performance in extreme aerospace operating conditions

U.S. Aerospace Bearings Market Outlook:

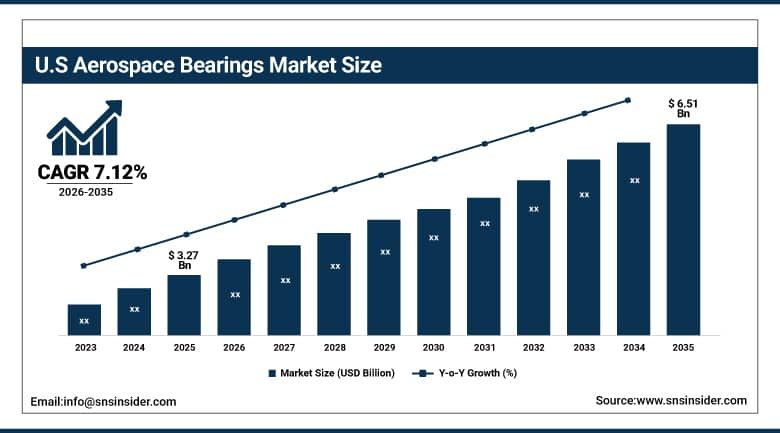

The U.S. Aerospace Bearings Market was valued at USD 3.27 Billion in 2025 and is expected to reach USD 6.51 Billion by 2035, growing at a CAGR of 7.12% from 2026–2035.

The United States leads North American aerospace bearings revenues through its position as home to the world’s largest commercial and military aircraft manufacturing base, the concentration of major aerospace OEMs and Tier 1 suppliers, and sustained defence procurement investment. RBC Bearings, The Timken Company, and NSK sustain U.S. market leadership through their comprehensive bearing portfolios serving commercial aviation, military aviation, and the rapidly growing unmanned aerial vehicle segment, whose expanding defence and commercial procurement budgets continue to broaden the addressable customer base for domestic bearing manufacturers.

According to the Federal Aviation Administration, U.S. commercial aviation supports over 2.9 million jobs and generates trillions in economic activity, reflecting the scale of aircraft operations and associated component demand.

Aerospace Bearings Market Segment Analysis:

-

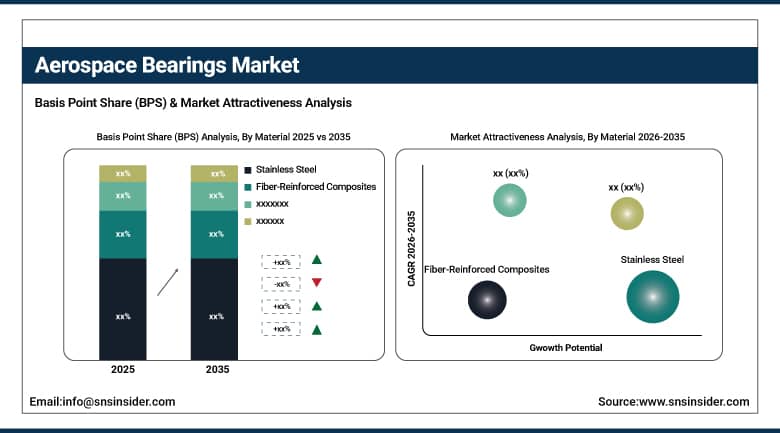

By Material, Stainless Steel segment dominated the Aerospace Bearings Market in 2025 with 36% share; Fiber-Reinforced Composites segment is the fastest growing segment.

-

By Bearing Type, Roller Bearing segment dominated the market in 2025 with 42% share; Ball Bearing segment is the fastest growing segment.

-

By Aircraft Type, Fixed Wings segment dominated the market in 2025 with 64% share; Unmanned Aerial Vehicle segment is the fastest growing segment.

-

By Application, Commercial Aviation segment dominated the market in 2025 with 48% share; Unmanned Aerial Vehicle segment is the fastest growing segment.

-

By Platform, Commercial segment dominated the market in 2025 with 71% share; Military segment is the fastest growing segment.

By Material, stainless steel segment dominates the aerospace bearings market, while fiber-reinforced composites segment is the fastest-growing segment.

Stainless steel dominated the Aerospace Bearings Market in 2025 due to its excellent strength and durability along with good corrosion-resistance properties that enable this metal to operate in high-temperature and high-pressure environments. They are extensively used in engines, landing gears, and various other components of the plane which require maximum strength and performance capabilities. Stainless steel has an exceptional track record, cost-effectiveness when compared with other alloys, and availability making them a favored choice for aerospace bearings production.

Fiber-reinforced composites are the fastest growing segment due to their light weight along with high strength and fatigue resistance characteristics. These materials reduce the overall weight of the aircraft resulting in enhanced performance and fuel consumption. Growing need for efficient planes, electric aircraft, and other aerospace advancements is boosting their adoption rates. Their superior performance in harsh conditions will be driving their popularity in future aerospace projects.

By Bearing Type, roller bearings segment dominates the aerospace bearings market, while ball bearings segment is the fastest-growing segment.

Roller bearings dominated the market in 2025 because of the strength they have regarding carrying heavy loads, durability, and suitability for aerospace applications. These bearings are common in the engine, gears, and landing gears where there are heavy loads in both radial and axial directions. The capability of these bearings to be able to work well in situations where there is much stress and heat makes them important in aerospace. Other factors such as stable operation and longevity further make roller bearings occupy a large share of the market.

Ball bearings are the fastest growing segment due to the low coefficient of friction and efficiency of ball bearings that made them appropriate for high-speed aerospace applications. These bearings were gaining popularity in the field of aviation in lightweight aircraft and unmanned aerial vehicles, where speed was a necessity. Rising demand for advanced avionics and UAVs as well as next generation aerospace applications was propelling the usage of ball bearings.

By Aircraft Type, fixed-wing aircraft segment dominates the aerospace bearings market, while unmanned aerial vehicles segment is the fastest-growing segment

Fixed-wing aircraft dominated the Aerospace Bearings Market in 2025 because of their wide applicability in commercial aviation, defense activities, and cargo handling. A significant number of high-end bearing parts are used in engines, landing gears, and flight controls in fixed-wing aircraft. They have efficient flights, high-load carrying capabilities, and longer flights than any other type of aircrafts. Their consistent manufacturing and fleet expansions help them maintain their lead in the aerospace domain.

Unmanned Aerial Vehicles are the fastest growing segment owing to the rising adoption of unmanned aerial vehicles in the areas of defense, surveillance, logistics, and civil aviation. High precision bearings used in UAVs are important for efficiency and effective operation of the machines. Growing adoption of drones and advanced aerial mobility solutions leads to an increase in the number of these unmanned vehicles.

By Application, commercial aviation segment dominates the aerospace bearings market, while unmanned aerial vehicles segment is the fastest-growing segment

Commercial aviation dominated the Aerospace Bearings Market in 2025 owing to the large number of aircraft and increase in passengers using the airways. In fact, the use of bearings is quite extensive in aircrafts and includes their use in the engines, landing gears and various controls. Growing air traffic and replacement and manufacturing of new aircraft by major manufacturers are expected to drive demand. Growing emphasis on fuel efficiency and performance will be another reason for its high share.

Unmanned Aerial Vehicles are the fastest growing application segment due to rapid expansion of defense and surveillance systems as well as commercial drones. UAVs require aerospace bearings that provide precision, light weight, and enhanced life cycle. Rising utilization of unmanned aerial vehicles for logistical purposes, mapping, agricultural activities, and security are some of the factors boosting their demand. Technological developments and increasing investment in autonomous aerial vehicle technology are also contributing towards this trend.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

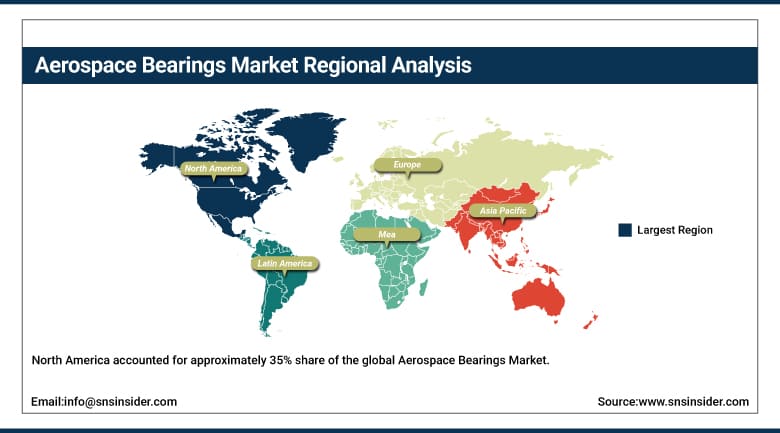

North America Aerospace Bearings Market Insights

North America accounted for approximately 35% share of the global Aerospace Bearings Market. The region hosts many bearing manufacturers and suppliers contributing to market growth, supported by its position as home to the world’s largest commercial and military aircraft manufacturing base. The United States accounts for approximately 82.5% of North American revenues through RBC Bearings, The Timken Company, and NSK’s comprehensive aerospace bearing manufacturing and distribution infrastructure serving Boeing, Lockheed Martin, and other major aerospace OEMs.

The United States Department of Defense reports an annual defense budget exceeding $800 billion, driving continuous modernization of military aircraft fleets and sustaining long-term demand for high-performance aerospace components, including advanced bearings.

Canada contributes supplementary North American revenues through its aerospace manufacturing sector’s component supply relationships and growing unmanned aerial vehicle development programmes. Mexico’s expanding aerospace manufacturing cluster, serving as a cost-competitive production base for North American aerospace supply chains, creates additional secondary regional demand for aerospace bearing components.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Aerospace Bearings Market Insights

Europe is a significant aerospace bearings market where SKF and Schaeffler’s established European manufacturing presence, Airbus’s commercial aircraft production requirements, and growing defence procurement investment collectively sustain regional demand. Germany accounts for approximately 22.4% of European revenues through Schaeffler AG’s domestic manufacturing leadership and the country’s broader aerospace component supply chain.

France’s Airbus assembly operations creating substantial bearing procurement, the United Kingdom’s aerospace manufacturing sector’s component supply relationships, and Italy’s growing aerospace industrial base collectively sustain European market development. SKF’s headquarters presence in Sweden anchors the region’s technical leadership in precision aerospace bearing manufacturing.

According to Eurostat, aerospace and defense manufacturing contributes significantly to EU industrial output and high-value exports, supporting the demand for advanced engineering components used in aircraft production and maintenance.

According to Airbus production data from Airbus, the company delivers over 700 commercial aircraft annually during strong production cycles, requiring large volumes of precision-engineered components such as aerospace bearings to support assembly and operational performance.

Asia Pacific Aerospace Bearings Market Insights

Asia Pacific is expected to register the highest growth rate of 8.56% during the forecast period, driven by rising demand for air travel and increasing aircraft deliveries across the region. Expansion of commercial airline fleets and growing investments in aviation infrastructure are significantly boosting demand for aerospace bearings. Additionally, the increasing number of maintenance, repair, and overhaul (MRO) service providers is strengthening aftermarket opportunities. Rapid industrialization, rising defense modernization programs, and growing adoption of advanced lightweight and high-performance bearing solutions further support market growth, making Asia Pacific a key high-growth region in the aerospace bearings industry.

Japan’s JTEKT Corporation manufacturing leadership, South Korea’s growing aerospace component supply chain, and India’s expanding commercial aviation fleet and maintenance provider network collectively sustain Asia Pacific’s fastest-growing regional trajectory.

MEA & Latin America Aerospace Bearings Market Insights

Increased MRO facilities and air traffic management in countries such as the UAE and Saudi Arabia would greatly boost the Middle East and Africa region’s growth pace, with the UAE leading MEA revenues at approximately 22.8% through its position as a major aviation hub with extensive maintenance, repair, and overhaul infrastructure investment. Israel’s advanced aerospace technology sector contributes secondary regional demand.

Brazil leads Latin American revenues at approximately 43.8% through Embraer’s commercial and military aircraft manufacturing programmes creating substantial domestic bearing procurement. Argentina and other Latin American markets contribute growing secondary demand through their developing aerospace maintenance infrastructure.

Market Dynamics:

Growth Drivers: Commercial aircraft demand growth and aerospace lightweighting initiatives driving sustained bearing market expansion

As the use of bearing goods in various end-use industries, rolling mills, and aircraft rises, so does the worldwide aerospace bearing market, with Airbus projecting demand for approximately 40,000 new aircraft over the coming decade creating substantial procurement opportunities for aerospace manufacturers to establish relationships with new companies and provide services to existing customers. Each new commercial aircraft programme creates bearing procurement across engines, landing gear, flight control systems, and auxiliary systems whose aggregate per-aircraft bearing content sustains structural market demand growth.

Restraints: High raw material costs and lengthy accreditation delays constraining aerospace bearing market growth

Obstacles such as high raw material costs, increases in operational costs followed by seasonal serviceability, and delays in acquiring accreditations impede global market growth. High cost and steel price fluctuating create margin pressure on bearing manufacturers whose long product development and certification cycles cannot quickly adjust pricing to reflect raw material cost volatility, creating commercial planning challenges for both manufacturers and their aerospace OEM customers whose own production scheduling depends on predictable component delivery and pricing.

The COVID-19 pandemic affected every business, with travel restrictions badly harming aviation and transportation businesses, severely impacting the aerospace bearing industry by halting supply chains and numerous distribution channels. While the sector has substantially recovered, the episode demonstrated the aerospace bearing market’s structural vulnerability to demand shocks affecting commercial aviation, whose passenger travel volume directly determines new aircraft order rates and corresponding bearing procurement.

Opportunities: Urban air mobility expansion and additive manufacturing technologies creating new aerospace bearing market categories

The expansion of the urban air mobility platform, the emergence of sensor-carrying units, and the growing growth of additive manufacturing technologies and building materials for the production of bearings create greater market growth opportunities during forecasting. Zero-emission aircraft development and lightweight, fuel-efficient bearing design represent significant opportunity categories whose successful commercialisation could create substantial new bearing procurement as next-generation aircraft platforms enter production.

Each new urban air mobility eVTOL aircraft programme that advances toward certification creates bearing procurement for novel electric propulsion and flight control system architectures whose technical requirements differ from conventional fixed-wing and rotorcraft bearing specifications. Additive manufacturing’s potential to enable novel bearing geometries and material combinations not achievable through conventional manufacturing processes creates a technology frontier whose successful aerospace qualification could unlock new bearing performance categories.

Recent Developments:

-

2024: The Royal Navy and broader aerospace supply chain saw NSK continue development of low-maintenance gearbox bearings increasing engine reliability in heavy duty engines, reflecting sustained technical investment in maintenance interval extension.

-

2023: Triumph Group continued its role as an important provider of water systems, locks, and components for Boeing systems, reinforcing established OEM supplier relationships that sustain fixed-wing aircraft bearing procurement growth.

-

2024: RBC Bearings and other major suppliers continued expanding aerospace bearing production capacity to address growing commercial aircraft order backlogs at Boeing and Airbus, supporting fixed-wing segment’s anticipated market leadership.

Aerospace Bearings Market Key Players are:

-

SKF Group

-

The Timken Company

-

Schaeffler AG

-

NTN Corporation

-

NSK Ltd.

-

JTEKT Corporation

-

RBC Bearings Incorporated

-

Aurora Bearing Company

-

MinebeaMitsumi Inc.

-

Boca Bearing Company

-

Kaman Corporation

-

SKF Aerospace

-

NSK Aerospace

-

NTN Aerospace Corporation

-

Trelleborg Group

-

Aurora Bearing Company

-

Harbin Bearing Manufacturing Co., Ltd.

-

Luoyang LYC Bearing Co., Ltd.

-

Fersa Bearings

-

National Engineering Industries Ltd.

Aerospace Bearings Market Report Scope:

| Report Attributes | Details |

|---|---|

|

Market Size in 2025 |

USD 11.3 Billion |

|

Market Size by 2035 |

USD 23.34 Billion |

|

CAGR |

CAGR of 7.5% From 2026 to 2035 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2035 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Material (Stainless Steel, Fiber-Reinforced Composites, Engineered Plastics, Aluminum Alloys, Others) |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

|

Company Profiles |

SKF Group, The Timken Company, Schaeffler AG, NTN Corporation, NSK Ltd., JTEKT Corporation, RBC Bearings Incorporated, Aurora Bearing Company, MinebeaMitsumi Inc., Boca Bearing Company, Kaman Corporation, SKF Aerospace, NSK Aerospace, NTN Aerospace Corporation, Trelleborg Group, Harbin Bearing Manufacturing Co., Ltd., Luoyang LYC Bearing Co., Ltd., Fersa Bearings, National Engineering Industries Ltd. |

Frequently Asked Questions

The Aerospace Bearings Market is expected to grow at a CAGR of 7.5% from 2026 to 2035.

The Aerospace Bearings Market was valued at USD 11.33 Billion in 2025.

Commercial aircraft growth, weight reduction focus, space industry expansion, and urban air mobility drive Aerospace Bearings Market growth.

Stainless Steel held the largest market share through wide availability at lower cost compared to other carrier materials.

North America hosts many leading bearing manufacturers and suppliers contributing to regional market growth.

Get in Touch