Sperm Count Test Market Report Scope & Overview:

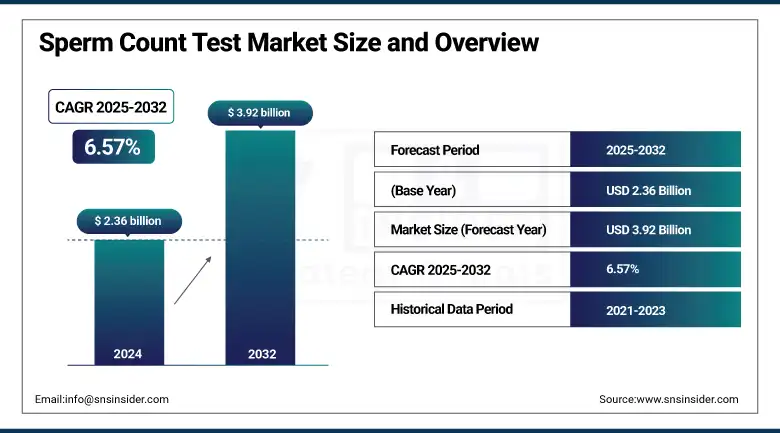

The sperm count test market size was valued at USD 2.36 billion in 2024 and is expected to reach USD 3.92 billion by 2032, growing at a CAGR of 6.57% over 2025-2032.

The sperm count test market is driven by the increasing incidence of male infertility, decline in global sperm count, surge in public awareness, and availability of at-home testing kits. According to recent studies in health, men’s sperm count has decreased by more than 50% over the past 4 decades, which raises the need for at-home diagnosis as well.

In March 2025, ExSeed Health will release its next-generation smartphone-based sperm analysis device with improved AI-powered motility analysis skill, marking the beginning of a new trend of innovation-driven sperm count test market.

There are also technological advances in tests, including smartphone-compatible semen analysis tests and AI sperm tracking, which are making testing more affordable and reliable, too. Additionally, fertility clinics are witnessing a consistent increase in the patient pool, and the global sperm count test market is evolving with greater innovations in laboratory and home-use test equipment. Government campaigns for reproductive health and the focus on early detection are contributing to this trend.

Investments in R&D in the reproductive diagnostics sector, and in particular among the makers of sperm count tests such as ExSeed Health and Medical Electronic Systems, have already markedly risen. Approvals of regulatory bodies such as the FDA and CE mark certificate for home-use semen analysis kits have increased the trust of consumers and the sperm count test market growth.

In June 2025, Medical Electronic Systems announced it had expanded the availability of its FDA-cleared YO Home Sperm Test product line throughout North America and Europe in response to consumer demand and favorable sperm count tests market analysis.

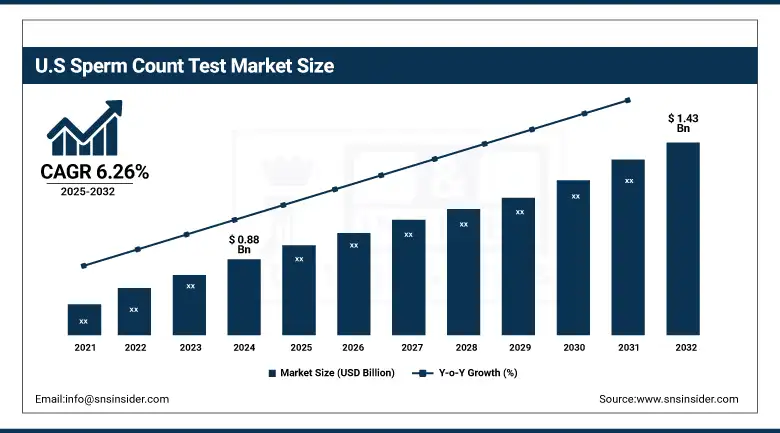

The U.S. sperm count test market size was valued at USD 0.88 billion in 2024 and is expected to reach USD 1.43 billion by 2032, growing at a CAGR of 6.26% over 2025-2032. Due to strong FDA approvals, robust insurance coverage, as well as increased investment in fertility-focused startups, the U.S. dominated the market in the region with the biggest market share. In the U.S., in 2023, the investment for male fertility-focused companies had crossed USD 150 million in the last year alone, indicating increased demand and innovation. Canada is the fastest-growing country, led by growing telehealth infrastructure, positive reimbursement, and increasing consumer uptake of home-based testing kits. Growing media awareness and public and private fertility cooperation are also increasing demand for sperm count tests in Canada. Major companies such as Medical Electronic Systems and Trak Fertility have enhanced their overall distribution network in North America over the years, thus fuelling the demand for sperm count tests in the market.

Market Dynamics:

Drivers:

-

Rising Infertility Rates, Home Diagnostics, and Technological Advancements Fuel Growth

Male infertility cases are growing significantly, driven by the surging number of male infertility cases, growing health awareness, and availability of home-based diagnostic devices are some of the factors lending impetus to the global sperm count test market. The WHO estimates that nearly one in six people globally experience infertility, and about 50% of these cases are due to male factors. This has driven the need for non-invasive and convenient fertility testing tools.

The trend toward at-home sperm testing is also driven by the rapid proliferation of AI (Artificial Intelligence)-based mobile kits and Bluetooth devices, which can help analyze sperm motility, as well as provide sperm concentration snapshots. Upstarts such as Fertility Focus and Trak Fertility have raised millions in venture capital in recent years, evidence of increasing investor interest in men’s reproductive health. Further, there is a health and wellness trend toward preventative care, and as such, younger people are looking to get tested for fertility before there are potential issues.

Certification (CE, ISO) requirements for medical diagnostic devices are also contributing to facilitating product entry in new markets and leading to further R&D investment in this area. A report from NIH for 2024 estimated that public and private R&D spending on male fertility diagnostics is increasing by 18% in the last three years, indicating a fertile environment for growth and innovation in the sperm count test market.

Restraints:

-

Lack of Awareness, Social Stigma, and Test Reliability Concerns Impede Growth

The sperm count test market is heavily restricted due to a lack of product awareness in underdeveloped regions, cultural barriers, and doubts related to the product's precision and the authenticity of performance benefits in home-based test kits. Embarrassment and fear of stigmatization are deterrents to infertility evaluation among men and contribute to the underuse of diagnostic services. There is low market penetration due to a lack of public education programmes on male reproductive health in the low and middle-income countries. Additionally, a 2023 study published in Human Reproduction Update reported that 35% of at-home sperm tests deliver inconsistent results because of improper technique, lack of professional interpretation, and environmental factors such as fluctuating temperatures. The expense of high-end home kits can similarly be a barrier, particularly if they are not covered by insurance.

Sperm testing is also limitedly incorporated in routine health checkups, inhibiting consistent demand. Market access is also hindered by regulatory obstacles, as clinical approvals are time-consuming and regulatory requirements are sometimes entry barriers for certain orders. For instance, AI-powered diagnostics have faced delays in FDA approval stemming from concerns over data security and accuracy, which have impeded the adoption of certain next-gen products in the U.S. These challenges remain a barrier to the widespread implementation of sperm analysis systems and limit the sperm count tests market.

Segmentation Analysis:

By Product Type

The kits segment dominated the market revenue in the sperm count test market in 2024 with a 47.6% sperm count test market share, as the demand for convenient, in-home convenience for fertility testing grows. They are popular owing to their low costs, privacy, and availability, particularly for young men and for couples choosing to become pregnant. And now many kits also include smartphone connectivity and AI analysis, which makes it more convenient to use and makes analysis more accurate, too. The fastest-growing segment is reagents and consumables, driven by the increasing volume of lab-performed semen analyses and the need for repeat testing in fertility centers. As these ingredients are required for every diagnostic round, cyclic demand is the ideal motor for fast increase. Significant parameters that are driving the demand for reagents are rising technological developments and growing application of automated systems in laboratories, all over the clinical sector.

By Technique

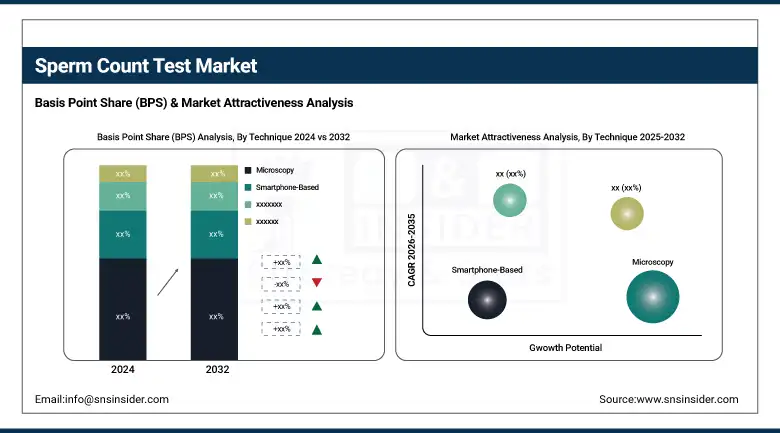

Microscopy held the largest market share with 38.9% in 2024, as it has been used in clinical fertility testing for several decades. It is still the reference method for the examination of sperm motility, sperm concentration, and morphology when used by trained professionals. Its precision and economy lead to its continued use, particularly in the hospital and laboratory environment. Smartphone-based is the fastest-growing of all the segments, based on growing consumer aspiration for digital health tools, remote testing, and real-time reporting. New products that include app integration, video-based sperm motility analysis, and cloud-based results tracking are helping drive adoption. What’s more, as telehealth and male wellness platforms gain momentum, smartphone-based testing is being driven forward, particularly by tech-savvy, younger men.

By Age Group

The sperm count test market is dominated by the 34 years and below age group, which accounted for a 44.3% sperm count test market share in 2024. This is due to increasing knowledge about the importance of male fertility and a rise in proactive family planning. Men in this range are also increasingly relying on at-home test kits and fertility-tracking apps, particularly as more couples put off parenthood. The 35–40 years group is experiencing the highest growth rate, since men in this age group are now starting to experience fertility-related problems and are proactive in getting checked. Healthcare provider education, advertising, and employer-based fertility programs are also driving this age group to regular checks of their sperm health.

By End User

In 2024, fertility centers held the leading share in the sperm count test market by registering a share of 41.2%, on the back of an increasing number of patients receiving male infertility treatment in surrogacy centers and reproductive health centers. These centers may provide a more extensive menu of semen analysis services, including advanced testing such as DNA fragmentation and motility monitoring, leading to better patient outcomes. The largest end-user segment is diagnostic laboratories, which are growing robustly due to the increasing number of physician referrals and the demand for precise and validated sperm analysis. Increased capacity and the automation of laboratory services are making it possible to process more tests more quickly. Moreover, coverage of fertility testing by insurance in various countries has helped increase the laboratory test volumes, contributing to the growth of the segment.

Regional Analysis:

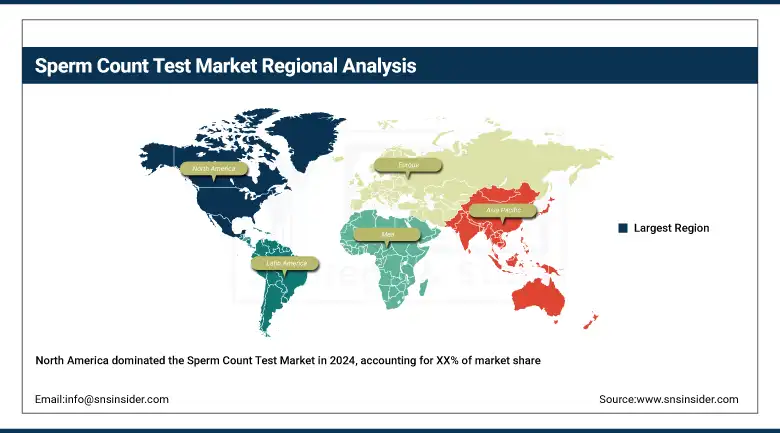

In 2024, North America was a major shareholder of the sperm count test market due to a rise in the prevalence of male infertility, increased awareness about reproductive health, and high usage of at-home diagnostic kits.

The sperm count test market in Europe has the second largest share after North America. The European market is further segmented into Germany, France, Italy, Spain, the UK, and the rest of Europe.

Germany is the largest market in Europe due to the presence of a large number of IVF centers and an increasing number of male reproductive health screenings. Between 2021 and 2024, there was a 20% increase in male fertility consultations at German clinics. The fastest rising is the UK, where demand for home testing has soared for a generation of parents whose average age is increasing, getting digital tools to help them access their fertility. Early in 2025, companies such as ExSeed Health extended into the UK with smartphone-based sperm testing kits, which empowered local growth. Moreover, straightforward market access due to EU-wide CE marking guidelines and supportive fertility reimbursement policies has facilitated the entry for players, driving further R&D and clinical innovation in France and Italy, further underpinning the overall growth of the sperm count test market in Europe.

Asia Pacific is the fastest-growing region globally for the sperm count test market because of increasing population, infertility rate, and access to healthcare. Rising public awareness and digital health uptake count as important influencers. CD Leading Circulating Diagnostics Comparator Producing Country and Diagnostics Landscape Country in Asia.

China leads the CD test volumes in Asia and is the leading regional market, owing to fertility programs supported by the government and growth in diagnostics infrastructure. The fastest-growing country is India, buoyed by the rapid growth of fertility clinics, easy availability of testing kits, and high demand for sperm count analysis in Tier-2 and Tier-3 cities. India has witnessed a 28% growth in cases of male infertility over the past year, recent reports have suggested, in addition to an increase in sales of confidential, at-home fertility test kits. Smartphone sperm test is also gaining traction in Japan and South Korea due to high digital literacy, which boosts sperm count test market trends & sperm count test market analysis as well.

Key Players:

Leading sperm count test companies operating in the market comprise Medical Electronic Systems, Fertility Focus Inc., Andrology Solutions, Vitrolife AB, DxNow, Hamilton Thorne, Artron Laboratories Inc., ExSeed Health, Olympus Corporation Inc., AB ANALITICA s.r.l., SCSA Diagnostics, Bonraybio Co. Ltd., CooperSurgical Inc., Aytu BioScience Inc., IVFtech ApS, Medical International Research (MIR), Bioneer Corporation, Biosigma S.p.A., Microptic S.L., and Genea Biomedx.

Recent Developments:

-

In February 2025, PS Fertility launched PS Detect, an innovative at-home diagnostic test that measures sperm fertilization competency via a novel phosphatidylserine (PS) marker. The test can be self-administered and sent to labs, enabling early detection of conditions like varicocele and guiding personalized treatments, marking a step forward in more comprehensive male fertility diagnostics.

-

In September 2024, Spermosens received ethical clearance to initiate clinical trials of its advanced JUNO‑Checked device at Malmö's Reproductive Medicine Center. This next-generation system, designed to assess sperm-egg binding efficiency, offers faster results and refined diagnostic capabilities, underscoring a significant R&D advancement in fertility testing.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.36 billion |

| Market Size by 2032 | USD 3.92 billion |

| CAGR | CAGR of 6.57% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Instrument, Reagents And Consumables, and Kits) • By Technique (Microscopy, Chromatographic Immunoassay and Colorimetric Reaction, Smartphone-Based, and Others) • By Age Group (34 And Below 34 Years, 35-40 Years, and 41 Years and Above) • By End User (Hospitals, Fertility Centers, Diagnostic Laboratories, and Others) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Medical Electronic Systems, Fertility Focus Inc., Andrology Solutions, Vitrolife AB, DxNow, Hamilton Thorne, Artron Laboratories Inc., ExSeed Health, Olympus Corporation Inc., AB ANALITICA s.r.l., SCSA Diagnostics, Bonraybio Co. Ltd., CooperSurgical Inc., Aytu BioScience Inc., IVFtech ApS, Medical International Research (MIR), Bioneer Corporation, Biosigma S.p.A., Microptic S.L., and Genea Biomedx. |

Frequently Asked Questions

Regulatory approvals like FDA and CE certification are critical to sperm count test market growth. Countries with streamlined approval pathways see faster product rollouts in the global sperm count test market.

Technology enhances accuracy in evaluating sperm morphology, motility, and sperm concentration through automated and AI-driven platforms. Innovations are transforming traditional male fertility testing.

The sperm count test market analysis shows a mix of established players and startups competing on tech, pricing, and accessibility. Innovation in diagnostic devices and partnerships with andrology labs drive competition.

Home diagnostics market solutions offer privacy, convenience, and real-time analysis, increasing their popularity among younger males. These at-home kits are reshaping the U.S. sperm count test market landscape.

Key sperm count test market trends include smartphone-based semen analysis, AI-integrated devices, and direct-to-consumer testing models. Integration with assisted reproductive technology is also gaining momentum.

Declining sperm concentration and poor sperm morphology have led to a spike in demand for male fertility testing solutions. This trend fuels growth in both clinical andrology labs and consumer-based testing segments.

Get in Touch