Self-injection Devices Market Overview

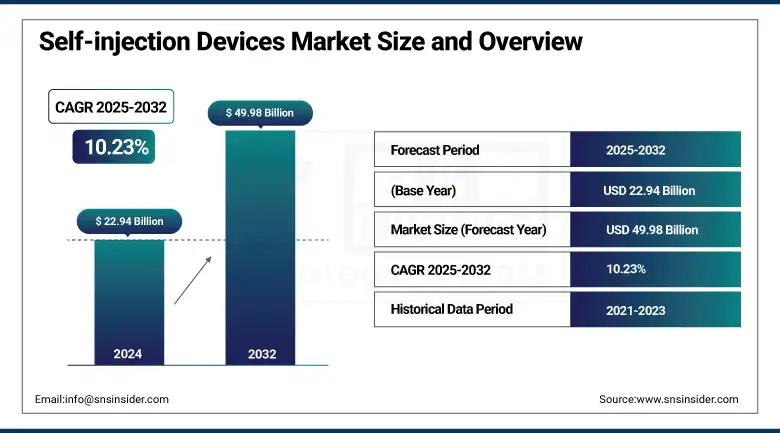

The Self-injection Devices Market size was valued at USD 22.94 billion in 2024 and is expected to reach USD 49.98 billion by 2032, growing at a CAGR of 10.23% over the forecast period of 2025-2032.

Owing to the growing burden of chronic diseases, technological developments in such devices, and favourable reimbursement and regulatory support from authorities such as the U.S FDA and the European Medicines Agency (EMA), the self-injection device market is registering significant growth.

For instance, in 2021, 537 million people were suffering from diabetes (the International Diabetes Federation), and in 2022, a total of 20 million new cancer cases were counted (World Health Organization).

To Get more information On Self-injection Devices Market - Request Free Sample Report

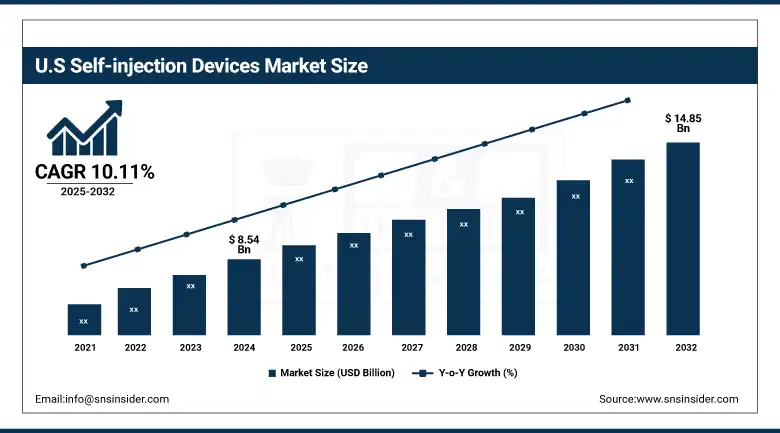

The lack of self-injectable devices for chronic disease management, due to a lack of accessibility and safety, is reflected in these stats, from diabetes self-management to rheumatoid arthritis treatment. The U.S. self-injection devices market size was valued USD 8.54 billion in 2024 and it’s expected to reach USD 14.85 billion by 2032 with a CAGR of 10.11% during the forecast period, benefiting from high healthcare expenditure, widespread adoption of next-generation self-injection technologies, and a large number of indications that require biologics drug delivery and home-based injectable therapy. A recent example of regulatory support for self-injectable expansion in the U.S. is the April 2025 approval of argenx's VYVGART Hytrulo prefilled syringe for self-injection in generalized myasthenia gravis and CIDP by the FDA.

Recently, self-injectable devices, including autoinjectors, pen injectors, and wearable injectors, have rapidly changed the field of administration of chronic diseases by enabling patients to self-administer medications at home without outside intervention safely. Regulatory agencies accelerated approval pathways for devices such as the smart injection devices and the subcutaneous self-injection device to facilitate innovative delivery of the drug and to increase accessibility to home-administered injectable therapy. These innovations help increase patient compliance, cut down healthcare spending while providing autonomy towards personalized medicine also representing self injection devices market trends.

Self-injection Devices Market Dynamics

Drivers

-

The Growing Prevalence of Diabetes and Chronic Diseases Generates Globally Demand for Self-Injection Devices

The increasing global incidence of several chronic diseases, including diabetes, is considerably accelerating the acceptance of self-injection devices since many of these conditions demand regular, long-term medication supply.

For instance, The Diabetes Atlas published by the International Diabetes Federation (IDF), projects that 140 million cases of diabetes worldwide would increase from 643 million in 2030 to 783 million by 2045. Affected are 537 million adults; most of them live in low- and middle-income countries.

Since patient-centric, convenient medication delivery solutions help individuals oversee their treatment plans from home, therefore reduce the load on healthcare institutions and promote adherence. This growth in the prevalence of chronic diseases makes these solutions more relevant. Self-injection devices, including autoinjectors and pen injectors, have become indispensable tools for patients because they provide autonomy, flexibility, and a greater quality of life. Regulatory authorities and healthcare facilities, as well as individuals, are realizing its benefits, so they are gradually encouraging the shift toward home-based treatment.

Restraints

-

Limited Access to Advanced Self-Injection Devices in Developing Countries Restricts Market Growth and Patient Outcomes

Despite the technological advancements and growing demand for self-injection devices, limited availability of these sophisticated drug delivery methods in low- and middle-income nations still remains a major obstacle to market development. Self-injection devices are somewhat more popular in high-income countries, while many underdeveloped countries have significant challenges from cost, lack of infrastructure, and limited delivery routes.

Studies reveal that a significant portion of the global diabetes population stays untreated or incorrectly managed, particularly in underdeveloped nations such as India and China, where knowledge is limited and healthcare resources are taxed. The significant upfront cost of premium devices, including wearable autoinjectors, makes many patients and healthcare workers in these fields.

Moreover, factors affecting the safe and effective use of self-injection devices are inadequate patient education and limited training of healthcare professionals. Under legislative and logistical restrictions, differences in approval processes and a lack of established healthcare infrastructure accentuate these issues and result in differences in access and patient outcomes. Dealing with these challenges ensures equitable access to self-injection technology and helps to completely realize their capacity in improving the management of chronic diseases.

Self-injection Devices Market Segmentation Analysis

By Product

Comprising over 29% of the self-injection devices market share, the industry leader in 2024 is the needle-free injectors. Their reduced needlestick injury and needle anxiety risk largely help to explain their increased needle safety and usability. Regulatory approvals (FDA, EMA) for needle-free devices have surged as government bodies give safety in self-injection systems top priority. These devices find use in hormone treatments, insulin self-injection devices, and biologics medication delivery systems. Such as Astra Therapeutics' August 2024 agreement with Ypsomed to deploy the YpsoMate autoinjector technology for allergy medication, recent improvements illustrate the trend toward improving home-based injectable therapy and patient adherence.

Driven by the expanding load of chronic diseases and the integration of smart injectable devices with digital connectivity, dose tracking, and real-time feedback, the category of autoinjectors is anticipated to develop the quickest. Approvals for new autoinjectors, including Molly autoinjectors from SHL Medical for MoonLake Immunotherapeutics in May 2023, highlight the market's focus on biologics and personalized treatment.

By Usability

Disposable self-injectable devices held 61% of the self-injectable device market share in 2024. These devices are recommended by the FDA and CDC as favored for their convenience as well as for their infection control qualities, therefore promoting patient adherence and diabetes self-management. Government campaigns and public health guidelines still advocate disposable devices for the control of chronic diseases, especially about insulin self-injection devices and subcutaneous self-injection devices. For instance, Phillips-Medisize added more disposable pen injectors in February 2023 in response to the growing need for basic, single-use devices for biologics drug administration.

The reusable sector is expected to also see the fastest self-injection devices market growth, driven by sustainability, affordability, and technical innovation. Smart reusable pen injectors and wearable injectors that track dose and provide digital feedback are increasingly used for diabetes self-management and rheumatoid arthritis treatment, as regulatory approvals stress their safety and usefulness for home-based injectable treatment.

By Application

The cancer accounted for 27% self-injection devices market share in 2024. Rising cancer incidence is driving demand for self-injectable devices for chemotherapy, hormone treatment, and supportive care, according to WHO data. By enabling cancer patients to manage treatments at home, hence reducing hospital visits, self-injection devices enhance the quality of life. Regulatory approvals increasing access to creative self-injection devices in oncology include the FDA's October 2023 clearance of the enFuse injector for Empaveli.

Driven by the growing prevalence of chronic pain issues and acceptance of self-injectable devices for home-based therapy, the pain management market is set for rapid rise. Supported by government initiatives and regulatory agencies, smart injectable devices with dose tracking and feedback properties are improving patient adherence and enabling tailored medicine in pain management.

Self-injection Devices Market Regional Outlook

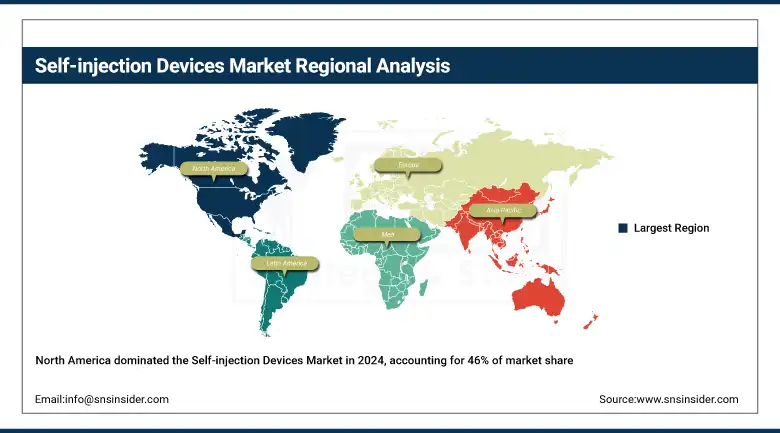

With a 46% of the global self-injection devices market share in 2024, North America is the dominating region. Underlying this leadership are several interconnected factors. The area has a high and rising prevalence of chronic diseases, including diabetes, cancer, and hormone abnormalities, which create continuous demand for self-injection devices, allowing patients to treat their conditions at home.

Get Customized Report as per Your Business Requirement - Enquiry Now

Approx. 90% of the USD 4.1 trillion spent on healthcare in the United States is on chronic and mental health problems, according to the U.S. Centers for Disease Control and Prevention (CDC); diabetes alone will cause USD 413 billion in direct and indirect costs by 2022. Especially, the American market benefits from a strong culture of patient autonomy and self-medication, advanced healthcare infrastructure, and large healthcare expenditure. Strategic relationships and regular product releases have accelerated the acceptance of wearable injectable, pen injectable, and auto-injectable technologies. Leading players in the industry, such as Ypsomed AG, BD, and SHL Medical AG, support the domination of North America.

Europe is the second-largest region it is predicted to grow noticeably within the forecast period. This momentum driven by growing healthcare infrastructure, increasing incidence of chronic diseases, and a strong focus on technological innovation. Rising disease prevalence paired with reasonably low-cost advancements in device fabrication is pushing development in countries including the UK and France. Also, marking the area by joint efforts between important corporations is significant companies include the exclusive deal between Stevanato Group and Owen Mumford in May 2022 to enhance the Aidaptus auto-injector, so improving patient experience and adherence.

Asia Pacific is predicted to have the fastest CAGR through 2032 under the leadership of growing economies such as China and India. The region’s growth is driven by a substantial patient population affected with asthma, diabetes, cardiovascular illnesses, and allergies, as well as increasing healthcare costs and more access to innovative medicine delivery systems. The shift toward home-based treatment and the growing acceptability of self-injection devices in response to growing chronic illness loads are the main forces behind this transition. As knowledge of self-injection benefits spreads and healthcare infrastructure gets stronger, Asia Pacific is set to become a major market force.

Key Players in the Self-injection Devices Market

The key self-injection devices companies are Pfizer, Inc., NuGen Medical Devices, Gerresheimer AG, Owen Mumford Ltd., Antares Pharma, Inc., Haselmeier AG, SHL Medical AG, YPSOMED, Amgen Inc., BD, and others

Recent Developments in the Global Self-injection Devices Market

-

With U.S. FDA approval for the Cyltezo Pen autoinjector in May 2023, Boehringer Ingelheim is proving regulatory support for creative autoinjector platforms and therefore extending therapy choices for chronic inflammatory illnesses.

-

The FDA authorized the enFuse injector from Enable Injections for Empaveli in October 2023, therefore allowing at-home treatment for paroxysmal nocturnal hemoglobinuria (PNH). This clearance emphasizes the government's will to increase access to sophisticated self-injection treatments in oncology.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 22.94 Billion |

| Market Size by 2032 | USD 49.98 Billion |

| CAGR | CAGR of 10.23% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Needle-free injectors, Pen injectors, Autoinjectors, and Wearable injectors) • By Usability (Reusable, and Disposable) • By Application (Cancer, Pain management, Hormonal disorders, Autoimmune disorders, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Pfizer, Inc., NuGen Medical Devices, Gerresheimer AG, Owen Mumford Ltd., Antares Pharma, Inc., Haselmeier AG, SHL Medical AG, YPSOMED, Amgen Inc., BD, and others |

Frequently Asked Questions

Ans: The Disposable segment dominated the Self-injection Devices Market.

Ans: Limited Access to Advanced Self-Injection Devices in Developing Countries Restricts Market Growth and Patient Outcomes

Ans. The CAGR of the Self-injection Devices Market is 10.23% during the forecast period of 2025-2032.

Ans: The North America region dominated the Self-injection Devices Market in 2024.

Ans. The projected market size for the Self-injection Devices Market is USD 49.98 billion by 2032.

Get in Touch