Spout Packaging Market Report Scope & Overview:

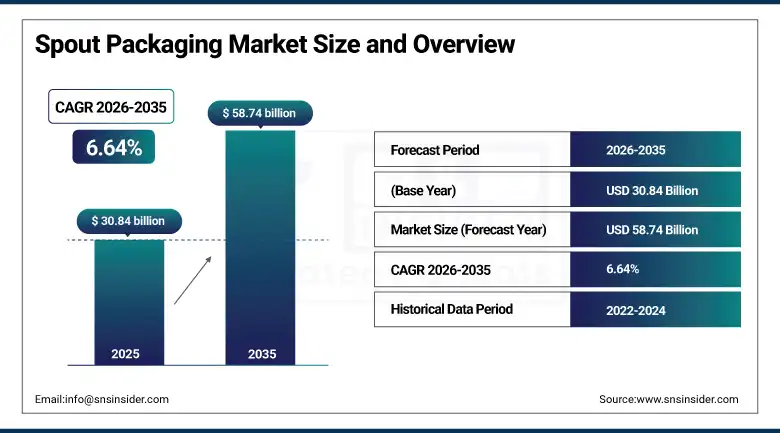

The Spout Packaging Market was valued at USD 30.84 Billion in 2025 and is expected to reach USD 58.74 Billion by 2035, growing at a CAGR of 6.64% from 2026 to 2035.

Spout packaging has emerged as one of the most commercially successful flexible packaging formats in the global consumer goods industry, combining the lightweight and material-efficient advantages of flexible pouch construction with the dispensing convenience, resealability, and shelf stability that consumer markets increasingly demand across food, beverage, personal care, pharmaceutical, and household product categories. The commercial proposition of spout packaging is grounded in measurable logistical and environmental advantages. Spout pouches are typically 80 to 90% lighter than equivalent rigid glass or plastic containers, reducing transportation fuel costs and associated carbon emissions per unit of product delivered. Their lay-flat form factor enables significantly higher packing density in storage and distribution facilities, reducing warehousing costs and optimizing container utilization in export supply chains. The shelf presentation flexibility that gusseted stand-up spout pouches provide enables eye-catching retail display across a wide range of product categories without the shelf depth requirements of rigid packaging formats.

Amcor plc, the world's largest flexible packaging manufacturer, reported that its Flexibles segment generated USD 2.55 Billion in net sales in the first quarter of fiscal 2025, with spout pouch and flexible liquid packaging formats identified as among the highest-growth sub-categories within the portfolio. Amcor's investment in recyclable and mono-material flexible packaging structures capable of incorporating spout fitments is enabling its consumer goods customers to pursue both packaging sustainability commitments and the consumer convenience advantages that spout formats deliver, positioning the company at the commercial intersection of the market's two most powerful growth drivers.

Market Size and Forecast

-

Market Size in 2026E: USD 32.89 Billion

-

Market Size by 2035: USD 58.74 Billion

-

CAGR: 6.64% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Spout Packaging Market - Request Free Sample Report

Spout Packaging Market Trends

-

Growing consumer preference for lightweight and convenient flexible packaging is driving spout pouch adoption globally.

-

Rising development of recyclable and compostable spout packaging is supporting sustainability goals and regulatory compliance.

-

Expanding e-commerce activities are increasing demand for durable and space-efficient spout packaging solutions.

-

Baby food and infant nutrition applications are accelerating innovation in retort-capable spout pouch formats.

-

Increasing adoption of digital printing technologies is enabling customized and short-run flexible packaging production.

The U.S. Spout Packaging Market Outlook

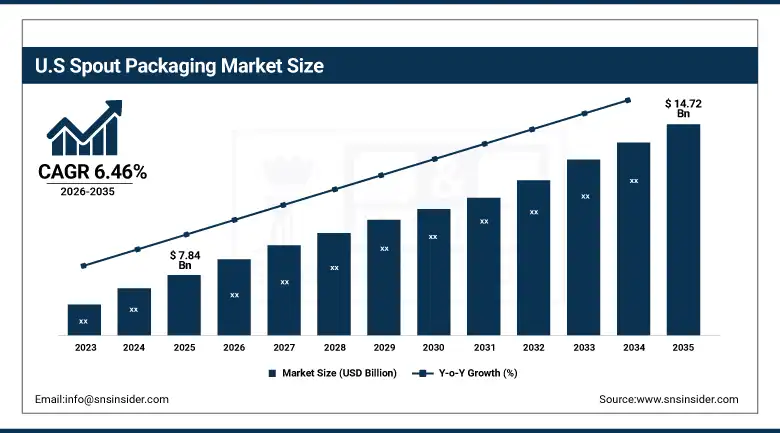

The U.S. Spout Packaging Market was valued at approximately USD 7.84 Billion in 2025 and is expected to reach approximately USD 14.72 Billion by 2035, growing at a CAGR of approximately 6.46%.

The United States is the world's largest individual national market for spout packaging, driven by the country's advanced flexible packaging industry infrastructure, high consumer receptivity to packaging convenience innovations, and the commercial scale of its food, beverage, and personal care sectors whose combined retail revenues sustain among the world's highest per-capita flexible packaging consumption rates. Established spout pouch applications in juice and beverage, baby food, pet food, and laundry detergent categories are sustaining baseline market volume, while growth is being driven by the expansion of spout packaging into premium food categories including soups, sauces, meal kits, and plant-based food products whose packaging transition from rigid cans and jars to flexible spouted formats is gaining commercial momentum. The growth of direct-to-consumer and subscription food delivery businesses, which benefit disproportionately from the logistical advantages of lightweight flexible packaging in parcel fulfilment operations, is creating additional structural demand for spout packaging across emerging retail channel formats.

Glenroy Inc., a U.S.-based flexible packaging converter specializing in sustainable packaging innovations, launched its Recycled spout pouch line in 2025, providing food and beverage manufacturers with certified recyclable spout pouch structures that meet How2Recycle label programme standards. The commercial availability of a certified recyclable spout pouch format addresses a key barrier to brand owner adoption of spout packaging in sustainability-committed product lines, potentially accelerating category conversion from rigid formats whose recyclability credentials are more established in consumer recycling infrastructure.

Spout Packaging Market Segment Analysis

-

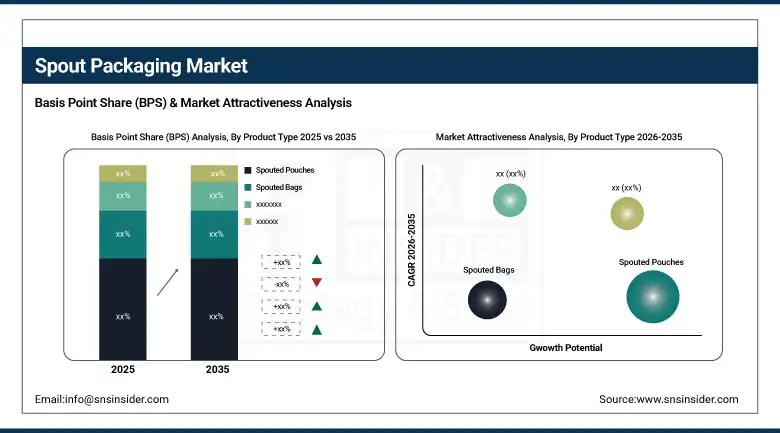

By Product Type, spouted pouches segment dominated the spout packaging market with 52.47% share in 2025, while the spouted bags segment is the fastest growing product type during 2026 to 2035.

-

By Material, plastic segment dominated the spout packaging market with 58.74% share in 2025, while the biodegradable & compostable segment is the fastest growing material during 2026 to 2035.

-

By Capacity, below 200 ml segment dominated the spout packaging market with 42.38% share in 2025, while the 501 ml to 1,000 ml segment is the fastest growing capacity range during 2026 to 2035.

-

By Application, food & beverages segment dominated the spout packaging market with 46.84% share in 2025, while the pharmaceuticals & healthcare segment is the fastest growing application during 2026 to 2035.

By Product Type, spouted pouches dominate, spouted bags grow fastest

Spouted pouches retained the dominant product type position with 52.47% of spout packaging market revenue in 2025. The stand-up spouted pouch format delivers the most complete consumer value proposition within the spout packaging category, combining self-standing shelf presentation with resealable dispensing convenience that sustains product quality across multiple use occasions. Its structural versatility across retort sterilization, frozen food, and ambient shelf-life applications makes it commercially applicable across a wider range of food and beverage product formats than any competing flexible packaging structure. Spouted bags are the fastest-growing product type, driven by the growing adoption of bulk liquid, sauce, and concentrate formats in food service, institutional catering, and industrial process applications where large-volume spouted bag-in-box configurations deliver significant handling efficiency and product waste reduction advantages over conventional rigid pail and drum alternatives.

By Material, plastic dominates, biodegradable & compostable grows fastest

Plastic laminate materials accounted for 58.74% of spout packaging market revenue in 2025, reflecting the material's combination of barrier performance, heat-seal reliability, and cost competitiveness that makes it the default structural specification for the majority of commercial spout pouch applications. Multi-layer plastic laminate structures provide the oxygen and moisture barrier properties essential for ambient shelf-life performance across food and beverage applications whose product stability requirements cannot be met by single-layer films. Biodegradable and compostable materials are the fastest-growing segment as the EU Packaging and Packaging Waste Regulation's mandatory compostable packaging provisions and retailer sustainability mandates create first-time commercial demand for certified biodegradable spout pouch structures across food and personal care categories where composting infrastructure is developing in alignment with regulatory timelines.

By Application, food & beverages dominate, pharmaceuticals & healthcare grow fastest

Food and beverages accounted for 46.84% of spout packaging application revenue in 2025. The breadth of food and beverage product formats that spout pouches can accommodate, spanning infant formula, fruit purees, juice drinks, soups, sauces, alcoholic beverages, sports nutrition supplements, and cooking oils, makes the food and beverage sector the structurally largest and most diversified end-use application within the market. Pharmaceuticals and healthcare represent the fastest-growing application segment as the adoption of spout packaging for liquid oral medications, nutritional supplements, wound care solutions, and single-use diagnostic reagent packaging accelerates under the combined influence of patient compliance convenience requirements, dose accuracy advantages, and tamper-evident closure security that spout fitment designs can incorporate into pharmaceutical-grade packaging specifications.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.62% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.74% |

|

Middle East & Africa |

UAE |

24.38% |

|

Latin America |

Brazil |

46.84% |

North America Spout Packaging Market Insights

North America dominated the global spout packaging market in 2025, holding approximately 34.84% of global revenues, with the United States accounting for approximately 84.62% of regional revenue. The region's market leadership reflects its early and deep commercial adoption of flexible packaging formats across consumer goods categories, the commercial scale of its food and beverage manufacturing sector, and the presence of the world's most technologically advanced flexible packaging converter base including Amcor, Berry Global, Sealed Air, and Glenroy whose innovation programmes continuously expand the range of product applications where spout packaging can replace rigid alternatives. Canada contributes supplementary regional demand through its food processing industry and growing adoption of spout packaging across both retail and foodservice channels.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Spout Packaging Market Insights

Europe accounted for approximately 26.47% of global spout packaging revenues in 2025. The European market is shaped by a unique combination of sophisticated consumer convenience expectations and the world's most stringent flexible packaging sustainability regulatory framework. The EU Packaging and Packaging Waste Regulation's mandatory recyclability and compostability targets for flexible packaging are driving significant product development investment by converters and brand owners to advance recyclable spout pouch structures from innovation concept to commercially validated format within compressed timelines. Germany accounts for approximately 28.47% of European revenues through its large food processing and personal care manufacturing sector. The United Kingdom, France, the Netherlands, and the Nordic nations contribute substantial regional demand through their respective consumer packaged goods industries whose shelf renovation programmes are progressively incorporating spout packaging across multiple product categories.

Asia Pacific Spout Packaging Market Insights

Asia Pacific is the fastest-growing regional spout packaging market at a CAGR of approximately 8.24% through 2035. China accounts for approximately 38.74% of Asia Pacific revenues as the world's largest flexible packaging manufacturing base and a rapidly growing consumer market for convenient food and beverage formats whose urbanizing population and rising disposable incomes are driving first-time and growing adoption of premium packaged food products across spout pouch formats. India's food processing sector expansion, its large and growing baby food market, and its increasingly sophisticated retail distribution infrastructure are positioning it as the region's fastest-growing country-level spout packaging market. Southeast Asia, Japan, and South Korea each contribute meaningful regional demand through their respective food processing and consumer goods manufacturing sectors.

MEA & Latin America Spout Packaging Market Insights

Middle East and Latin America are growing spout packaging markets where expanding packaged food consumption, growing modern retail infrastructure, and increasing consumer exposure to international packaged goods formats are driving spout packaging adoption across beverage, baby food, personal care, and household product categories. The UAE leads MEA revenues at approximately 24.38% of the regional total through its advanced modern retail sector, high imported goods consumption, and growing domestic food processing industry, whose premium product ambitions align with the shelf differentiation advantages that spout packaging provides. Brazil leads Latin American revenues at approximately 46.84% of the regional total through its large food and beverage manufacturing sector, growing organized retail footprint across Tier 2 and Tier 3 cities, and domestic flexible packaging converter base whose capacity investments are expanding to serve growing regional demand.

Market Dynamics

Growth Drivers: Accelerating consumer preference for packaging convenience

Consumer lifestyle changes including smaller household sizes, on-the-go consumption occasions, and growing preference for portioned single-serve formats are creating expanding demand for spout packaging whose resealability, portion control, and dispensing convenience match these evolving consumption patterns more precisely than rigid jar, bottle, or can alternatives. The e-commerce distribution channel's structural growth is amplifying spout packaging's logistical advantages because lightweight, shatterproof, and space-efficient spout pouches significantly reduce parcel fulfilment costs and breakage rates compared to rigid packaging alternatives whose weight and fragility impose meaningful cost and damage penalties in direct-to-consumer parcel delivery operations. Retailer sustainability commitments to reduce packaging weight and material per unit of product are creating institutional procurement incentives for spout packaging adoption across consumer goods categories where equivalent rigid packaging options involve substantially greater material mass.

Restraints: Recyclability limitations of multi-layer laminate spout pouch structures and consumer uncertainty about spout packaging disposal create barriers to full sustainability.

Conventional spout pouch structures utilize multi-layer laminate combinations of polyester, aluminium foil, and polyethylene whose material blending is commercially essential for barrier performance but creates recyclability challenges in mechanical recycling systems designed for single-material plastic streams. Most existing spout pouches cannot be recycled through kerbside household recycling programmes in major markets including the United States, United Kingdom, and Germany, creating an sustainability positioning gap between the material efficiency advantages of flexible packaging and the end-of-life recyclability credentials that environmentally conscious consumers and brand sustainability commitments increasingly require. The development and commercial validation of mono-material recyclable spout pouch structures is advancing but has not yet achieved the barrier performance parity with multi-layer laminates required for all ambient shelf-life food and beverage applications.

Opportunities: Pharmaceutical liquid packaging conversion and premium food category penetration represent high-value application growth frontiers.

The pharmaceutical liquid packaging market represents a structurally underserved opportunity for spout packaging whose dose accuracy, tamper-evidence, and patient compliance advantages over conventional liquid oral medication packaging are increasingly recognized by pharmaceutical manufacturers seeking to improve medication adherence outcomes through packaging design innovation. Unit-dose and multi-dose spout packaging formats for liquid oral medications, pediatric dosing supplements, and hospital clinical nutrition products each represent application categories where spout packaging's functional advantages over rigid glass or plastic bottle alternatives have been clinically and commercially validated in early adopter programmes. Premium food categories including craft spirits, premium olive oil, specialty sauces, and direct-trade coffee concentrate represent high-brand-value spout packaging opportunities where format novelty, premiumization messaging, and portion convenience create willingness-to-pay premiums that improve packaging economics relative to commodity food applications.

Recent Developments:

-

2025: Glenroy Inc. launched its RecycReady certified recyclable spout pouch line, providing food and beverage brand owners with How2Recycle label-eligible flexible packaging structures that maintain the barrier performance and sealing reliability of conventional multi-layer spout pouches while meeting retailer sustainability requirements for commercially recyclable packaging formats.

-

2024: DQ Pack introduced a retort-capable stand-up spout pouch engineered for sterilization temperatures up to 125 degrees Celsius, enabling ready-to-eat meal, soup, and baby food manufacturers to utilize the consumer convenience advantages of spout packaging across shelf-stable ambient products that previously required rigid can or glass jar packaging to achieve comparable thermal processing requirements.

-

2024: Huhtamaki Oyj expanded its sustainable spout packaging portfolio with new paper-based spout pouch structures incorporating certified renewable fiber content, targeting European food and beverage manufacturers whose sustainability commitments require demonstrable progress toward packaging recyclability and bio-based content targets mandated under EU packaging regulatory timelines.

Spout Packaging Market Key Players are:

-

Amcor plc

-

Berry Global Inc.

-

Sealed Air Corporation

-

Huhtamaki Oyj

-

Mondi Group

-

Sonoco Products Company

-

Uflex Limited

-

Constantia Flexibles

-

Glenroy Inc.

-

Swiss Pac Pvt. Ltd.

-

Tetra Pak International SA

-

Smurfit Kappa Group

-

Fres-co System USA Inc.

-

ProAmpac Holdings

-

Paxxus Inc.

-

DQ Pack

-

Clondalkin Group

-

Impak Corporation

-

Winpak Ltd.

-

Printpack Holdings Inc

Spout Packaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 30.84 Billion |

| Market Size by 2035 | USD 58.74 Billion |

| CAGR | CAGR of 6.64% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Spouted Pouches, Spouted Bags, Spouted Containers, Spouted Cartons) •By Material (Plastic, Aluminium Foil Laminate, Paper-Based, Biodegradable & Compostable) •By Capacity (Below 200 ml, 201 ml to 500 ml, 501 ml to 1,000 ml, Above 1,000 ml) •By Application (Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals & Healthcare, Household Care, Agricultural Chemicals) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amcor plc, Berry Global Group Inc., Mondi plc, Sonoco Products Company, Sealed Air Corporation, ProAmpac LLC, Constantia Flexibles Group GmbH, Huhtamaki Oyj, Coveris Holdings S.A., Glenroy Inc., SIG Group AG, Smurfit Westrock plc, UFlex Limited, Winpak Ltd., Clondalkin Group Holdings B.V., Scholle IPN Corporation, AptarGroup Inc., Korozo Ambalaj Sanayi ve Ticaret A.Ş., Bischof + Klein SE & Co. KG, and Swisspac Pvt. Ltd. |

Frequently Asked Questions

North America dominated the Spout Packaging Market in 2025, holding approximately 34.84% of global revenues, with the United States accounting for approximately 84.62% of North American revenues.

The food & beverages segment dominated the Spout Packaging Market with 46.84% share in 2025.

The primary growth factors include rising consumer preference for convenient and resealable packaging, growing demand for lightweight flexible packaging.

The Spout Packaging Market was valued at USD 30.84 Billion in 2025.

The Spout Packaging Market is expected to grow at a CAGR of 6.64% from 2026 to 2035.

Get in Touch