Stainless Steel Round Bar Market Report Scope & Overview:

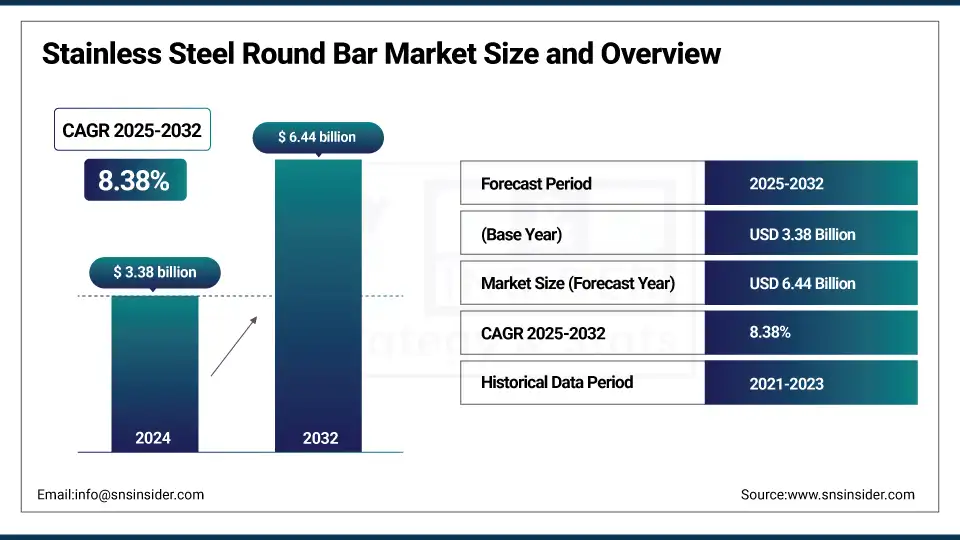

The Stainless-Steel Round Bar Market size was valued at USD 3.38 billion in 2024 and is expected to reach USD 6.44 billion by 2032, growing at a CAGR of 8.38% over the forecast period of 2025-2032.

The Stainless-Steel Round Bar Market is undergoing a noticeable paradigm shift due to its rising demand among several industries, including construction, automotive, oil & gas, and heavy engineering, among others. It is important to mention that these bars are known for their corrosion resistance, tensile strength, and durability, which makes them an indispensable part of load-bearing and precision machining applications. The increasing transition to high-performance materials capable of wide use in harsh operational environments is one of the major factors fueling the Stainless-Steel Round Bar Growth. In addition, innovations in production technologies, including precision forging and automated rolling mills, are improving product quality and customization to better meet the developing Stainless-Steel Round Bar Industry needs.

To Get more information On Stainless Steel Round Bar Market - Request Free Sample Report

Key Stainless-Steel Round Bar Trends are turning towards duplex and precipitation-hardening stainless-steel grades to accommodate high-stress applications and sustainability by converting to a scrap-based electric arc furnace (EAF) production process. The market is also witnessing heightened levels of digital supply chain and inventory tracking integration across the industry, creating the opportunity for unprecedented turnaround speeds and material waste lessening. Global stainless steel round bar demand surged in 2023, with the manufacturing and tooling sectors driving the majority of its consumption. Besides that, stricter emission norms and quality benchmarks are forcing manufacturers to develop low-carbon alloys and eco-friendly processing techniques that would redefine the horizon of the stainless-steel round bar market in the years to come.

In June 2025, India’s stainless-steel industry, led by Jindal Stainless, is seeking anti-dumping duties on low-priced imports to safeguard domestic producers. With imports comprising nearly 30% of consumption, industry bodies plan to file a formal petition, citing underutilized local capacity. They argue the move is essential to protect investments and ensure sectoral growth.

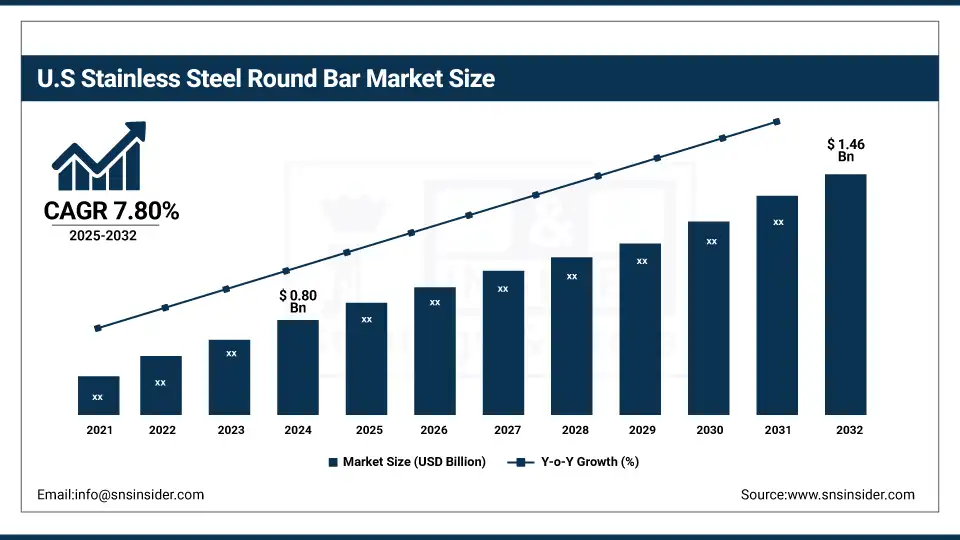

The U.S. dominates the North American stainless-steel round bar market, expected to grow from USD 0.80 billion in 2024 to USD 1.46 billion by 2032, at a CAGR of 7.80%. High demand in construction, automotive, and energy power growth. Continuous upgrading of infrastructure and a strong base of manufacturing also pay dividends to help grow the market. The U.S. is still one of the most important markets for developing stainless steel in the region.

Stainless Steel Round Bar Market Dynamics:

Drivers:

-

Rising Infrastructure and Urbanization Fuel Demand For 304 Stainless Steel Round Bars in the Global Construction Sector

The demand in construction or infrastructure is one of the key drivers for the growth of the stainless-steel round bar market, as it is very strong, durable, and can withstand harsh environments. The need for strong structural materials has increased as urbanization continues, with smart city developments spreading globally. Being highly resistant to corrosion, 304 Stainless Steel Round Bar has now found their applications in structural frameworks, support columns, and in architectural elements exposed to the weather.

Despite a gradual increase in output globally, the global construction industry is growing, with high infrastructure investments in countries, such as India, China, and the U.S. The rising number of residential and commercial developments, along with several ongoing infrastructure projects including bridges, railways, and power plants, is driving the construction market higher. Additionally, corrosion-resistant steel bars are favored in coastal and humid regions, where conventional steel faces faster degradation, making stainless-steel round bars an essential material in modern infrastructure.

Restraints:

-

Trade Barriers and Anti-Dumping Duties Disrupt Global Stainless-Steel Round Bar Supply Chains and Inflate Operational Costs

Trade restraints and import–export charges, primarily anti-dumping (AD) rules, are two principal hurdles for the stainless-steel round bar market as they reduce the cross-border flows drastically and fuel the costs. India in March 2024 slapped an extension of anti-dumping duty for the third time on stainless-steel bars from China and Indonesia to protect local mills. At the same time, the U.S. imposed antidumping (AD) duties on Indian stainless-steel bars with margins remaining in up range of 21% as of January 2024. Tariff increases have, in practice, placed a cumulative duty burden of almost 60% on Chinese stainless-steel products in the U.S.–China relationship. Such elevated tariffs fortify local producers but strangle importers, elevating prices and creating shortages of supply in dependent markets.

Additionally, the frequent swings in trade policy create uncertainty that prevents the signing of long-term contracts and the investment of capital. The result is that companies are compelled to either diversify their supply chains or spur local production hubs to tackle these trade barriers, which ultimately leads to heightened operational complexities and cost burdens across the supply chain.

Stainless Steel Round Bar Market Segmentation Outlook

By Type

The hot-rolled segment dominated the market, accounting for 68% of the Stainless-Steel Round Bar market share. The high demand for them is mainly attributed to applications in construction and infrastructure, and heavy-duty machinery, where close tolerances and surface finish are not as important. Hot rolling is often the preferred option for large-scale use due to its low cost, simple processing at elevated temperatures, and high strength. Moreover, high volume demand from the automotive and shipbuilding industries reinforces the product market position, particularly in emerging and developed economies with an established manufacturing landscape.

Cold-rolled stainless steel round bars are projected to grow at the fastest rate over the forecast period due to their superior mechanical properties, dimensional accuracy, and high-quality surface finish. They are finding more and more use in precision engineering, medical devices, and electronics, where surface integrity and close tolerances are of paramount importance. There is an increase in the need for sophisticated machining and miniaturized parts in industries including aerospace and automotive, leading to the implementation of cold-rolled counterparts. They also have improved strength and appearance, which makes them a popular choice for architectural and decorative applications.

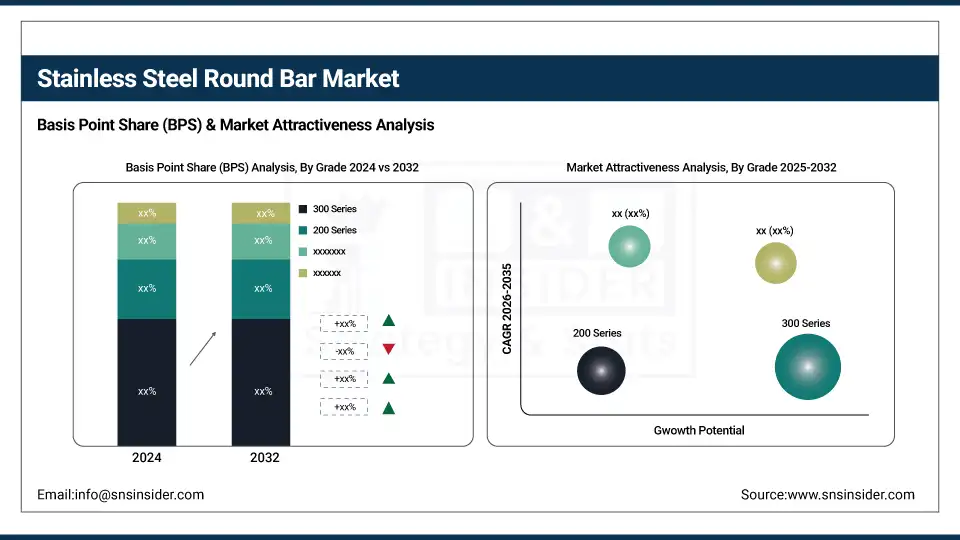

By Grade

The 300 series stainless steel round bars held the largest share, contributing 28% to the market in 2024. These grades, including 304 and 316, are known for their excellent corrosion resistance, weldability, and formability. They dominate due to extensive applications across various sectors including food processing, petrochemicals, and marine applications. This versatility and compliance with hygiene and survival standards make the 300 series a standard material for critical and high-performance applications, ensuring its place as the number-one grade in the stainless-steel round bar market.

The 400 series is experiencing the fastest growth owing to its high strength, wear resistance, and affordability compared to austenitic grades. These martensitic and ferritic stainless steels are being more widely used for automotive components, appliances, and industrial tools that require moderate corrosion resistance. This change in trend requires cost-effective content while still maintaining the structural property in developing economies is propelling its consumption. Apart from the above-mentioned factors, advancements in heat treatment and alloying techniques are improving the properties and applications of 400 series grades, which also contributes to their rapid market growth.

By End-Use Industry

Aerospace emerged as the leading end-use industry, accounting for 32% of the market in 2024 due to their excellent high strength-to-weight ratio, fatigue resistance, and high and low temperature strength, stainless steel round bars are an important aspect of aerospace manufacturing. This includes structural components, fasteners, engine parts, and landing gear systems. Rising commercial aircraft demand, modernization of defense aircraft, and satellite systems are expected to boost the stainless-steel consumption in this segment. In addition to this, aerospace fuel standards are very strict, and that would directly require high-quality stainless-steel bars.

The heavy engineering and machinery sector is witnessing the fastest growth in the stainless-steel round bar market. The segment’s growth is driven by increasing investments in infrastructure, power generation, mining equipment, and industrial automation. Round bars are favored for their mechanical strength, durability, and corrosion resistance, making stainless steel round bars exactly what is needed for machines in demanding conditions at high loads and under excruciating conditions. Emerging markets are investing in capital goods and expanding the productive base, which in itself is and will be driving demand in the coming years. Furthermore, this segment is also propelled by the worldwide spotlight on construction machinery and renewable energy equipment.

Stainless Steel Round Bar Market Regional Analysis:

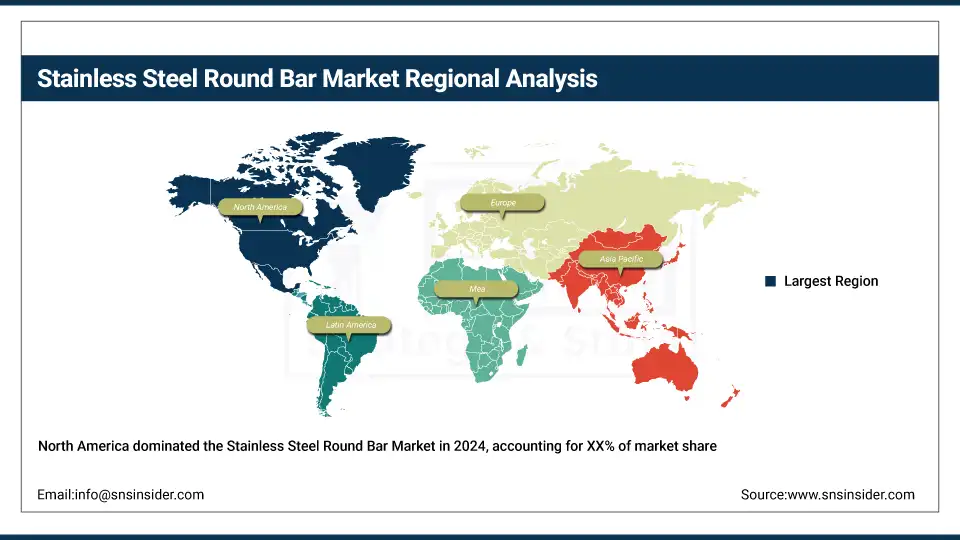

North America continues to be a key region in the stainless-steel round bar market, driven by its robust demand across heavy industries, aerospace, and automotive sectors. Increased consumption in the regions is further increased by large manufacturers, metallurgical technologies, mature metallurgical processes, and high infrastructure spending of the U.S. and Canada. In the region, demand for premium stainless-steel products is also supported by high-quality standards and sustainable sourcing. Market conditions are also affected by trade restrictions including anti-dumping duties that defend local producers from international competition. North America continues to be an important region for the stainless-steel round bar industry, with constant demand by end-users and modernization drives by the industry.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is witnessing the fastest CAGR growth in the stainless-steel round bar market, primarily fueled by rapid industrialization, urban development, and massive infrastructure investments in countries including China, India, and Southeast Asia. Supported by a robust manufacturing ecosystem and industrial development policies, China has long held regional production and consumption dominance. India, meanwhile, has also begun to position itself as a driver of global growth and flat-panel business with long-term policy support including prolonged anti-dumping duties and its Make in India programs. The construction, energy, and automotive sectors, which require massive quantities of stainless-steel components, are also well on track. The region is also enjoying a remarkably high compound annual growth rate (CAGR), driven by rising foreign investments, cheaper production, and an expanding output base for exports.

Europe holds a significant share in the stainless-steel round bar market, characterized by a mature yet stable demand across engineering, construction, and precision manufacturing sectors. In contrast, Germany, Italy, and France, have an established stainless steel processing industry, advanced technology, and comply with stringent environmental laws. This transition not only supports the sustainable infrastructure and clean energy but also reinforces the market opportunities. Above all, its growth rate is relatively modest, but steady innovation, manufacturing quality, and increasingly integrated intra-European trade still sustain a strong market share. Europe, as a modern, albeit traditional node of the global value chain with import competition and strong regulatory hurdles, still stays in the game as a global key player in stainless steel.

Stainless Steel Round Bar Companies are:

Universal Stainless, H. Stainless, Zhejiang Tsingshan Steel Pipe Co., Ltd, NIPPON STEEL CORPORATION, Tata Steel, Jindal Steel and Power Limited, Outokumpu, Acciaierie Valbruna, Electralloy, and ArcelorMittal.

Recent Developments:

-

In March 2025, Jindal Stainless announced a ₹40,000 crore investment plan to set up a greenfield stainless-steel plant in Maharashtra. The project aims for a 4 MTPA capacity and will be developed in phases over 10 years. It is expected to generate over 15,000 jobs and support sectors like hydrogen, defence, and nuclear energy. The Maharashtra government has approved the proposal with land and policy support.

-

In March 2025, ArcelorMittal Nippon Steel India secured land in Andhra Pradesh to set up a 7.3 MTPA greenfield integrated steel plant. This is part of its expansion strategy alongside the Hazira plant upgrade in Gujarat. The company also flagged concerns over India’s import restrictions on low-ash metallurgical coke, which could impact production.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.38 Billion |

| Market Size by 2032 | USD 6.44 Billion |

| CAGR | CAGR of 8.38% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Cold Rolled, Hot Rolled, Others) • By Grade (200 Series, 300 Series, 400 Series, 600 Series, Others) • By End-Use Industry (Heavy Engineering and Machinery, Automotive, Construction, Aerospace, Oil & Gas, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Universal Stainless, H. Stainless, Zhejiang Tsingshan Steel Pipe Co., Ltd, NIPPON STEEL CORPORATION, TataSteel, Jindal Steel and Power Limited, Outokumpu, Acciaierie Valbruna, Electralloy, ArcelorMittal |

Frequently Asked Questions

In 2024, the market share of North America is 1.08.

The “hot-rolled” segment dominated the Stainless-Steel Round Bar Market.

Rising Infrastructure and Urbanization Fuel Demand For 304 Stainless Steel Round Bars in the Global Construction Sector

The Stainless-Steel Round Bar Market was USD 3.38 billion in 2024 and is expected to reach USD 6.44 billion by 2032.

The Stainless-Steel Round Bar Market is expected to grow at a CAGR of 8.38% from 2025-2032.

Get in Touch