Steel Rebar Market Report Scope & Overview

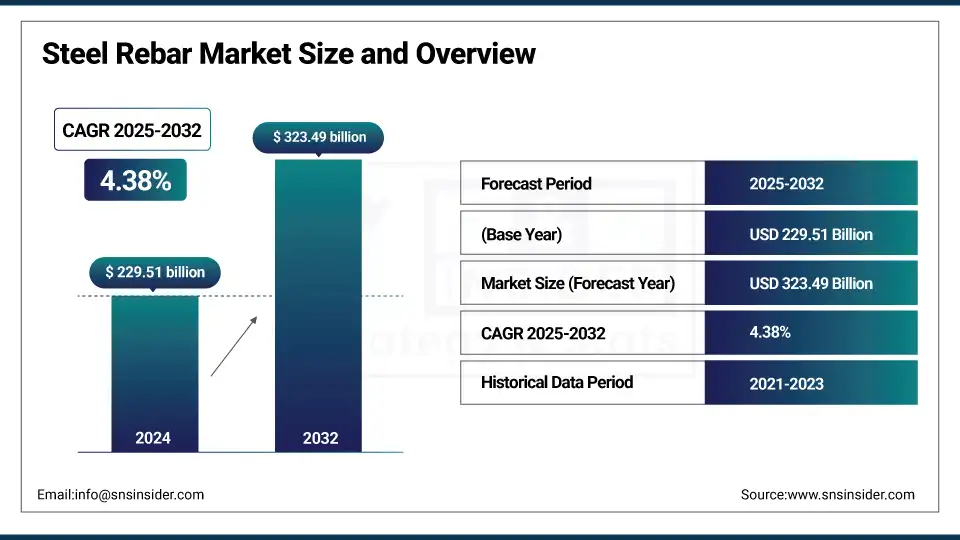

The Steel Rebar Market size was valued at USD 229.51 billion in 2024 and is expected to reach USD 323.49 billion by 2032, growing at a CAGR of 4.38% over the forecast period of 2025-2032.

Steel Rebar Market analysis indicates growing demand from renewable energy infrastructure are the major factors the major factor driving the market. The global shift towards clean and renewable energy sources has seen a lot of money poured into wind farms, solar parks, sustainable construction materials, hydro and energy storage projects, and so it needs reinforced concrete for the foundations, support structures, and transmission infrastructure. This strength and durability, steel rebar are critical for ensuring the structural integrity of these installations, such as offshore wind and large-scale solar projects. The government and private players are expected to accelerate their renewable energy targets to accommodate climate goals, which would create opportunities for steel rebar for such infrastructure, further driving the steel rebar market growth.

To Get more information On Steel Rebar Market - Request Free Sample Report

in March 2024, the U.S. Department of Energy pledged USD 6billion in March 2024 to decarbonize heavy industries (including iron & steel) via hydrogen-based steelmaking and electric-arc furnace (EAF) showcases.

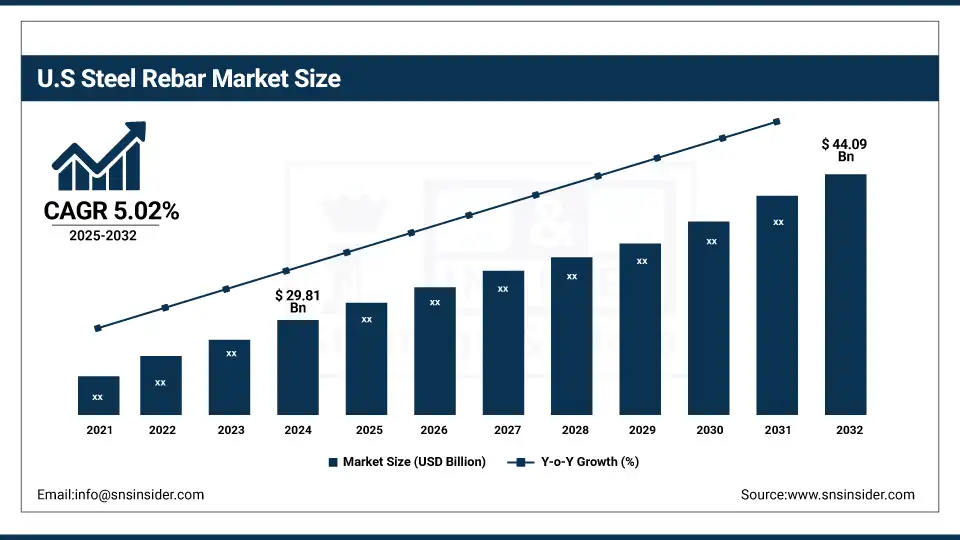

The U.S. Steel Rebar market size was USD 29.81 billion in 2024 and is expected to reach USD 44.09 billion by 2032 and grow at a CAGR of 5.02% over the forecast period of 2025-2032. It is owing to technology innovation, stringent requirements for safety from industries such as military, healthcare, oil & gas, and athletics. Combined with the localized R&D and high-end manufacturing to meet American needs for functionality such as UV protective, flame resistant and breathable textiles, American consumers and industries demand functional textiles.

Market Dynamics

Drivers

-

Growth in Residential and Commercial Construction Drive the Market Growth

The growth in construction activity, especially across fast-developing economies, is one of the key factors gaining traction for the steel rebar market. Steel rebar is a fundamental part of every building, providing the tensile strength that reinforced concrete needs for foundations, slabs, beams, and columns. The rural-to-urban shift and sprawling metropolitan areas have resulted in continuous urban demand for high-rise flats, smart townships, office buildings, building materials, retail malls, parking facilities and transit nodes. In addition, government‐sponsored affordable housing programs like India’s Pradhan Mantri Awas Yojana and the U.S. Low‐Income Housing Tax Credit (LIHTC) program are pushing residential construction even more, particularly in growth markets and low‐ to middle‐income neighborhoods.

Restrain

-

Volatility in Raw Material Prices May Hamper the Market Growth

Iron ore, scrap steel, and coking coal are the three main raw materials for steel rebar production, and because of that, metal prices are particularly volatile. Multiple global factors, such as supply disruptions, geopolitical actions (sanctions or conflict situations), export/import duties, shifts in demand patterns by major consumers like China, India, etc., have led to these changes. Iron ore prices, in addition, iron ore is also affected by energy prices, especially electricity and natural gas prices, particularly for electric arc furnace (EAF) units. Such cost uncertainties impact the entire pricing of rebars, tighten profit margins, and make long-term procurement planning a challenge for the manufacturers as well as the end users.

Opportunities

-

Rising Demand in Home Furnishings and Upholstery Creates Opportunities in the Market

The steel rebar industry is experiencing a paradigm shift due to developments in production technologies and materials science. The new generation of rebar, such as thermo-mechanically treated (TMT) bars, gives a much higher strength, ductility, and even weldability, making these suitable for areas where earthquake-resistant designs are required, or instead, areas where other environmental conditions are influencing structures, such as coastal areas. The use of corrosion-resistant coatings greatly prolongs the service life of concrete structures and reduces maintenance and lifecycle costs. Digital solutions provide a greater degree of accuracy as well as minimizing wastage on construction jobs through the likes of BIM (Building Information Modeling) and automated bending/cutting systems. Not only do these innovations improve rebar performance, but they also help meet green building standards and sustainability goals, which drive the steel rebar market trends.

In 2023, Commercial Metals Company (CMC) announced a USD 450 million investment to build a state-of-the-art micro-mill in Berkeley County, West Virginia.

Segmentation Analysis:

By Application

Construction held the largest Steel Rebar market share, around 42%, in 2024. It’s due to high demand from both residential as well as commercial infrastructure. Steel rebar is a key concrete reinforcement material that gives tension and durability to concrete structures commonly found in buildings, bridges, highways, tunnels and other civil engineering works. The global construction activity has strongly benefited from rapid urbanization, population growth, and increasing government expenditure on smart cities and affordable housing schemes. Moreover, by vertical constructions in city areas and expansions in transportation networks, the usage of reinforced concrete, and also the demand for steel rebar have increased.

Infrastructure held a significant Steel Rebar market share. It is attributed to large-scale public and industrial infrastructure investment projects all over the world. Steel rebar is an important part of many types of roads, bridges, tunnels, dams, airports, railways, and power plants where structural strength and long life are needed. In developed and emerging economies alike, governments are focusing on infrastructure development as a driver for economic growth and job creation. Projects like the U.S. Infrastructure Investment and Jobs Act, India Gati Shakti plan, and Belt and Road Initiative in China have ramped up infrastructure spending with a solid concrete demand.

Regional Analysis:

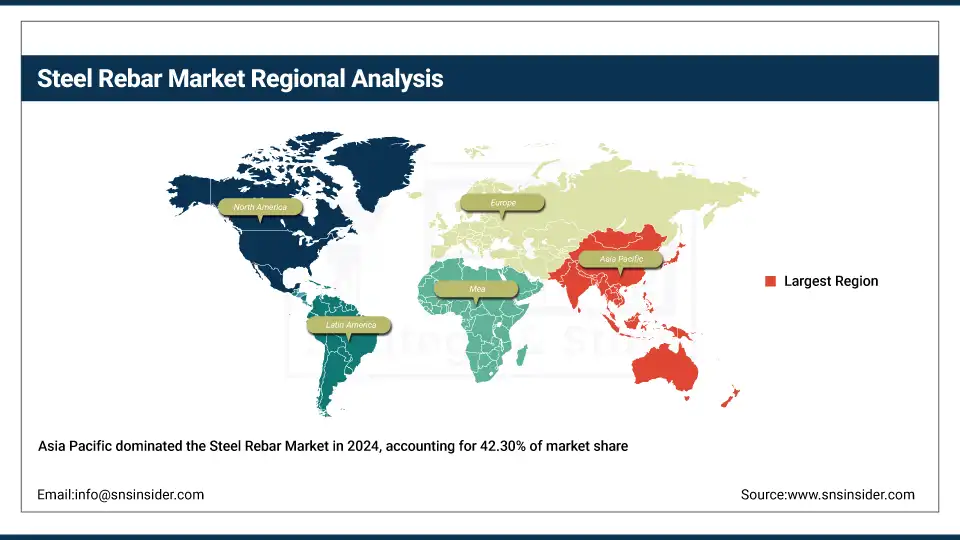

Asia-Pacific held the largest market share, around 42.30%, in 2024. It is due to the presence of textile manufacturing giants like China, India, Japan, and South Korea. Production costs and labor are cheaper in the region, and with government backing, they have an advantage over domestic manufacturing. The rising health awareness, improved income levels, and higher usage of technical textiles in health and fitness, automotive, healthcare, and activewear are some factors driving the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

In 2023, India broadened the existing Production Linked Incentive (PLI) scheme for technical textiles, rolling out USD 1.3 bn investment in innovation and production of high-performance fabrics such as those used in defense, aerospace, and medical applications.

North America Steel Rebars market held a significant market share and is the fastest-growing segment in the forecast period. It is due to being powered by the robustness of the industrial base of North America and the high consumer market spend on sportswear, followed by the huge demand for advanced textile technologies in the defense, healthcare, automotive, and sportswear markets. It has a strong ecosystem of manufacturers, research institutes, and regulators that encourages innovation and ensures quality in the region. High-performance fabrics like fire-resistant, antimicrobial, and moisture-wicking textiles are really popular in both application for military and commercial applications.

The U.S. Department of Defense and MIT launched the Advanced Functional Fabrics of America (AFFOA) with a USD 75 million grant to create smart textiles, including the fabrics that can sense and transmit data and provide temperature regulation, which makes it possible to reach high-performance applications in various fields.

Europe held a significant market share in the forecast period. It is owing to the strength in sustainability, quality certifications, and advanced applications in automotive, protective clothing, and industrial filtration. The nations, including German, Italian & French, invest massively in R&D over green coat, anti-microbial business finish, and high-strength fabric over trade. In sourcing for safe and product adherence to REACH, OEKO-TEX, and other strict safety and environmental regulations, followed by European customers.

A new directive from the European Union calls for all public procurement of textiles to meet eco-design and durability requirements by 2030, forcing producers to specify recyclable, bio-based, and energy-efficient performance fabrics, establishing a new market for certified suppliers

Key Players:

The major steel rebar companies are ArcelorMittal, Tata Steel, Gerdau, Nippon Steel, Nucor Corporation, JSW Steel, POSCO, Hyundai Steel, Celsa Group, and Steel Authority of India Limited (SAIL).

Recent Development

-

In February 2024, Nucor's board approved spending $860 million in February 2024 to construct what will be the company's largest rebar micro‑mill to date in the Pacific Northwest Pacific Northwest, which will have an annual rebar capacity of 650,000 tons, serving the expected increase in domestic infrastructure demand driven by the U.S. Infrastructure Law.

-

In March 2025, Nippon Steel will penetrate corrosion resistance float gown epoxy coated rebar for coastal infrastructure with a 100-year service life using nanotechnology.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 229.51 Billion |

| Market Size by 2032 | USD 323.49 Billion |

| CAGR | CAGR of 4.38% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Application (Construction, Infrastructure, and Industrial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | ArcelorMittal, Tata Steel, Gerdau, Nippon Steel, Nucor Corporation, JSW Steel, POSCO, Hyundai Steel, Celsa Group, Steel Authority of India Limited (SAIL) |

Frequently Asked Questions

Ans: Infrastructure development directly boosts steel rebar demand, as projects like bridges, roads, railways, and power plants require large volumes of reinforced concrete. Rebar provides the necessary strength and durability for these structures, making it a critical material in civil construction.

Ans: Emerging opportunities in the steel rebar market include the rising demand for green and low-carbon rebar driven by government mandates, and the growth of prefabricated and high-strength rebar for smart and sustainable infrastructure. Advancements in EAF-based production and corrosion-resistant materials also open new value-added segments.

Ans: Major trends shaping the steel rebar industry include a shift toward green and low-carbon steel production, increased use of corrosion-resistant and high-strength rebar, and rising adoption of automation and digital technologies in manufacturing. Growing demand from infrastructure and renewable energy projects also continues to drive innovation and capacity expansion.

Ans: Growth in residential and commercial construction drive the market growth.

Ans: The steel rebar market was valued at USD 229.51 billion in 2024.

Get in Touch