High Purity Pig Iron Market Report Key Insights:

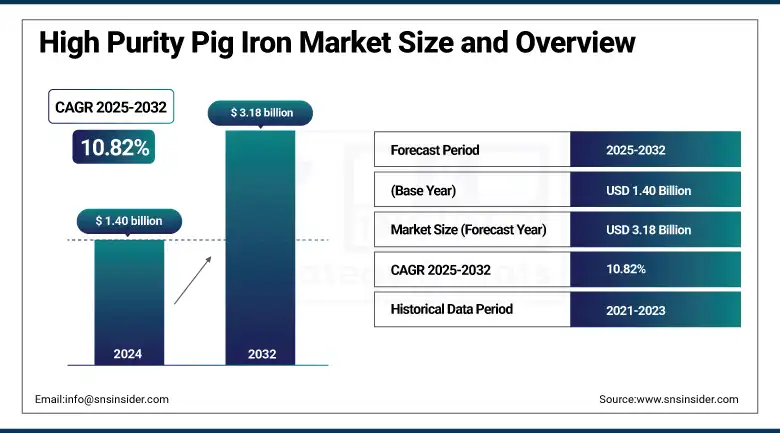

The High Purity Pig Iron market size was valued at USD 1.40 billion in 2024 and is expected to reach USD 3.18 billion by 2032, growing at a CAGR of 10.82%% over the forecast period of 2025-2032.

The high purity pig iron market is progressing due to the influence of the electric arc furnace and growing demand for special-grade pig iron for foundry in automotive casting. The rising emphasis on green steel industry projects continues to have a positive impact on the Asia Pacific pig iron market, keeping ordinary pig iron relevant for traditional industries. High purity pig iron market research report indicates that high purity pig iron manufacturers are focusing on precision carbon-control processes, as precision carbon-control processes significantly increase the quality and consistency of high purity pig iron.

To Get more information On High Purity Pig Iron Market - Request Free Sample Report

The high purity pig iron market was valued at 4.2 million tons in 2023, and the market of high purity pig iron of these premium grades has captured nearly 18.7% high purity pig iron market share as per the Ministry of Steel, Government of India. These numbers reflect the developing high purity pig iron market dynamics of decarbonization feedstock and premium-grade alloy growth, highlighting the industry’s focus on quality and environmentally sustainable production approaches.

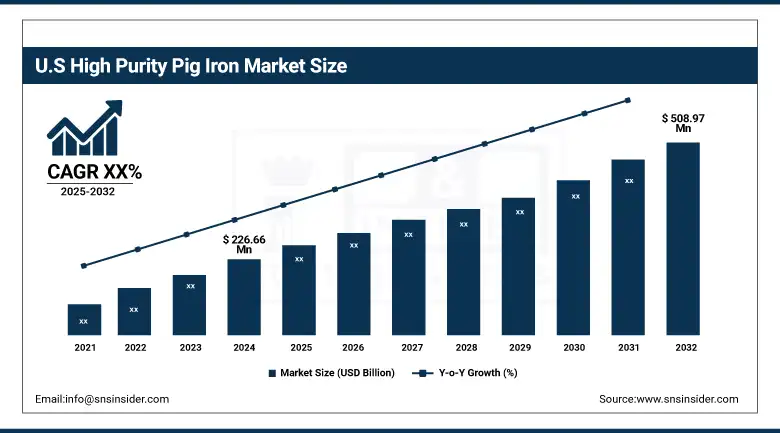

The U.S. dominates the North American high purity pig iron market with a market value of USD 226.66 million, holding a market share of around 73% in 2024, and is projected to reach a value of USD 508.97 million by 2032, through extensive automotive casting and foundry applications, accounting for the largest share within the region. The American Iron and Steel Institute highlights that US pig iron imports remained stable in 2023 to support the manufacturing of special-grade pig iron used in engine blocks and transmission parts. Leading high purity pig iron companies partner with automotive OEMs to ensure supply chain reliability, while government policies encourage modernization of steel plants through clean energy programs, reinforcing the country’s dominant position in the market.

High Purity Pig Iron Market Dynamics:

Drivers:

-

Growing Adoption of Special Grade Pig Iron in Precision Automotive Casting Applications

High purity pig iron market trends point towards an increasing requirement for special-grade pig iron for automotive casting. Steel producers invest in refining technology so the impurity level is kept low and higher purity levels are reached for the automotive tolerance requirements. A 7 per cent increase in the production of precision cast components in 2023 was reported by the US Geological Survey. This trend is favorable for the growing market of high purity pig iron as casting applications become more demanding of metallurgical quality while driving reliability to manage with reduced energy expense in subsequent production processes.

-

Rising Momentum of The Green Steel Industry Drives Demand in the Asia-Pacific Pig Iron Market

The green steel industry is transforming the Asia-Pacific pig iron market with its appetite for low-carbon feedstock. High purity pig iron analysis shows that cleaner materials are favorable in hydrogen steelmaking. During the 2023 Joule pilot projects, low-emission feedstock use was 10% higher during 2023, with India’s Ministry of Steel reporting a 10% rise. This move is consistent with sustainability plans and the importance of high purity pig iron in future capacity in recognition of companies’ proactive response to evolving environmental requirements.

Restraints:

-

Environmental Regulations Add Operational Costs To Asia-Pacific Pig Iron Market Production

The Asia-Pacific pig iron market is affected by new environmental regulations, especially by purer pig iron producers. Stricter standards were introduced in 2023 by the Chinese Ministry of Ecology and Environment, which is expected to raise production costs by some 4%. Aligned with the broader global goal of sustainability, these actions also work against the ability to sustain competitive pricing. While supporting the long-term green steel industry objectives, these regulations bring short-term restrictions to market growth of high-purity pig iron, impacting ordinary type pig iron and special grade pig iron equally.

High Purity Pig Iron Market Segmentation Analysis:

By Product Type

Standard high purity pig iron held a dominant high purity pig iron market share of 50.3% due to steady demand in automotive-grade casting. This segment benefits from balanced impurity control and cost efficiency, matching specifications for critical foundry applications. According to the US geological survey, pig iron imports in 2023 supported large-scale automotive casting, reflecting reliance on standard grades. Preference by leading foundries and heavy machinery makers sustains dominance through stable volume contracts and consistent metallurgical quality, strengthening its position in core applications.

Low-carbon high purity pig iron is the fastest-growing from 2025–2032 with the highest CAGR of 11.01%, driven by demand for specialty alloy production. The Ministry of Steel, India, reported multiple pilot projects adopting low-carbon pig iron for electric arc furnaces in 2023. This aligns with the green steel industry’s decarbonization push, making low-carbon grades a preferred choice to reduce carbon footprint and improve alloy performance, supporting sustainable manufacturing practices across the Asia-Pacific pig iron market.

By Form

Ingot held a dominant high purity pig iron market share of 58.4% due to strong demand in large casting operations. Its consistency and easy remelting make it the top choice for heavy industrial castings and shipbuilding. The Japan Iron and Steel Federation reported stable production of pig iron ingots in 2023 for large foundry applications, highlighting sustained market preference. Large block ingots continue as the standard feedstock for manufacturing engine blocks, industrial machinery, and structural parts due to uniform cooling and cost efficiency.

Granular is the fastest growing from 2025–2032 with the highest CAGR of 11.02%, driven by rising use in alloying and precision metallurgy. Nippon Steel technical updates noted a 7% increase in demand for granular pig iron in 2023, reflecting its role in producing customized alloys. Granular feedstock supports better melting control and composition accuracy, meeting the needs of industries like automotive casting and specialty foundries aiming for precise metallurgical performance and flexible batch processing.

By Production Technology

Blast furnace process held a dominant high purity pig iron market share of 61.3% due to large-scale integrated production. This traditional method offers consistent high-volume output critical for foundries. OECD steel committee data confirmed that over 60% of global pig iron is still produced by blast furnaces as of 2023, ensuring supply stability. Integrated mills rely on this technology to serve both ordinary type pig iron and special grade pig iron markets, reinforcing its role despite rising environmental pressures.

The electric arc furnace process is the fastest-growing from 2025–2032 with the highest CAGR of 11.03%, driven by the shift toward green steel production. The Ministry of Steel, India, documented a 9% increase in electric arc furnace capacity in 2023. Electric arc furnaces enable recycling and the use of low-carbon feedstock, supporting sustainability goals. This flexible technology aligns with modern foundry applications and alloy producers’ needs, driving adoption across the Asia-Pacific pig iron market and beyond.

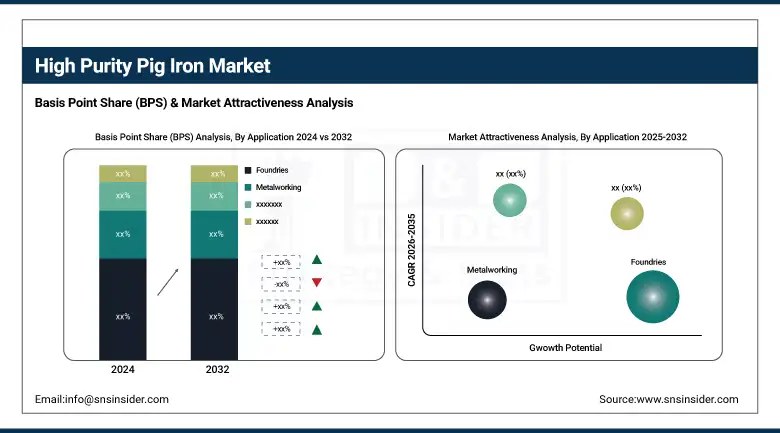

By Application

Foundries held a dominant high purity pig iron market share of 47.6% due to sustained demand for large casting applications. Foundries remain key consumers for automotive casting, heavy machinery, and structural components. The US Geological Survey reported stable pig iron consumption of around 2.8 million metric tons by US foundries in 2023, underscoring this segment’s resilience. Special grade pig iron supports higher mechanical properties, making it essential for modern foundry applications requiring consistent quality and precise impurity control.

Alloy production is the fastest growing from 2025–2032 with the highest CAGR of 11.51%, driven by rising demand for clean feedstock in specialty alloys. The Japan Iron and Steel Federation noted alloy makers increased low-phosphorus pig iron usage by 6% in 2023. This demand supports production of high-strength stainless and precision alloys, vital in automotive and aerospace industries, where metallurgical quality and defect reduction directly impact product performance and regulatory compliance.

By End-User Industry

The automotive industry held a dominant high purity pig iron market share of 42.8% due to strong demand for engine and transmission casting. Pig-controlled composition meets automotive casting standards. Nippon Steel reported consistent demand in 2023 for low-sulfur pig iron from automakers focused on fuel efficiency and emissions. This keeps the automotive industry as the leading consumer, supporting production of reliable, lightweight components and driving high-purity pig iron market trends in precision casting.

Aerospace and defense are the fastest-growing sectors from 2025–2032, with the highest CAGR of 11.57%, driven by the need for ultra-low impurity feedstock. The Ministry of Economy, Trade, and Industry, Japan, reported a 9% increase in aerospace alloy production in 2023. Aerospace casting requires defect-free pig iron to manufacture high-strength components. This specialization supports the rising demand for advanced alloys, aligning with the safety-critical standards and global defense programs.

By Distribution Channel

Direct sales held a dominant high-purity pig iron market share of 56.8% due to mill-to-foundry contracts ensuring consistent supply. Direct agreements help large foundries meet demand predictably, supporting both special-grade pig iron and ordinary-type pig iron use. OECD steel committee data confirmed that over half of the global pig iron trade relies on direct sales as of 2023, highlighting its efficiency in quality assurance and long-term pricing stability.

Online sales are the fastest growing from 2025–2032 with the highest CAGR of 10.76%, driven by digital supply chain transformation. Nippon Steel launched an online portal in 2023, increasing accessibility for small and mid-sized foundries. Digital platforms streamline orders and enable quicker delivery cycles, supporting flexibility. This trend reflects broader modernization in supply chains, aligning with Industry 4.0 strategies and rising demand for on-demand procurement in the Asia-Pacific pig iron market.

High Purity Pig Iron Market Regional Analysis

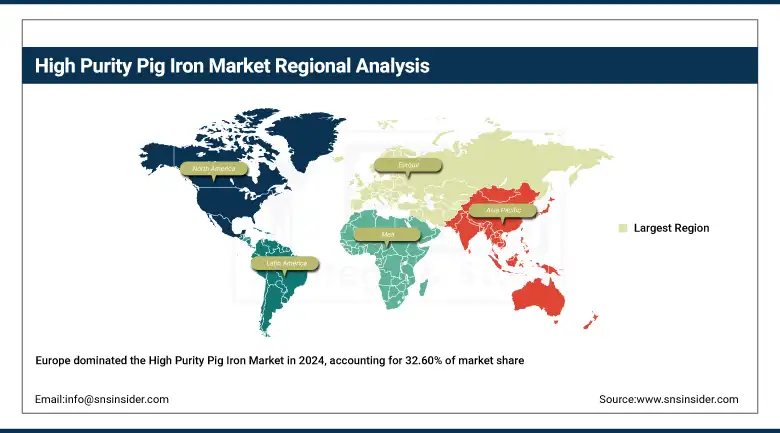

The Europe region is the dominating region with a high purity pig iron market share of 32.60% supported by advanced metallurgical standards and demand for high-end automotive casting. Germany leads due to robust foundry applications and specialty alloy production, as noted by Eurofer 2023 data, while France and Italy maintain steady special grade pig iron demand. European foundries emphasize low-carbon feedstock aligned with the green steel industry, reinforcing high-purity pig iron market trends driven by regulations and technological leadership across key economies.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia-Pacific region is the fastest-growing with the highest CAGR of 11.13% in the high purity pig iron market, driven by infrastructure expansion and specialty alloy demand. The Asia Pacific pig iron market benefits from rising urbanization and automotive casting needs, as the Ministry of Steel, India, reported higher output of ordinary type pig iron. China remains dominant with capacity upgrades, while India increases production for local and export markets. This growth supports broader high purity pig iron market growth and aligns with regional industry modernization strategies.

The North America region is the third dominating region in the high purity pig iron market with a significant market share of 22.3%, driven by steady industrial demand and increasing focus on sustainable steel production. Canada is expanding its green steel initiatives to reduce carbon emissions, with projects supported by Natural Resources Canada promoting electric arc furnace technology to use low-carbon feedstock like special grade pig iron. Additionally, Mexico’s growing manufacturing sector fuels demand for ordinary type pig iron in foundry applications, supported by the Mexican Ministry of Economy’s industrial growth reports. These dynamics bolster overall regional high purity pig iron market growth and evolving market trends.

High Purity Pig Iron Market Key Players:

The major high purity pig iron market competitors include High Purity Iron Inc., Ironveld Plc, Neo Metaliks Ltd., Asmet (UK) Ltd., Eramet Group, QIT-Fer et Titane (Rio Tinto Iron & Titanium), Richards Bay Minerals (RBM), Tronox Holdings plc, TiZir Limited, Tinfos AS, Saraf Group, Metinvest International SA, Hebei Long Feng Shan Casting Industry Co., Ltd., Miller and Company LLC, Mineral-Loy, Jindal Stainless Limited, Nippon Steel Corporation, Kobe Steel, Ltd., Dillinger Hütte, and Mideast Integrated Steel Ltd.

Recent Developments in the High Purity Pig Iron Market:

-

In June 2025, Richards Bay Minerals issued a press release forecasting significant high-purity pig iron growth through 2032, announcing new supply agreements with European foundries

-

In March 2025, Ironveld plc reported interim results for the six months to December 2024, highlighting the accelerated ramp-up of its high-purity iron project with offtake agreements in place

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.40 billion |

| Market Size by 2032 | USD 3.18 billion |

| CAGR | CAGR of 10.82% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Standard High Purity Pig Iron, Low Carbon High Purity Pig Iron, Ultra-High Purity Pig Iron) •By Form (Ingot, Granular, Powder) •By Production Technology (Electric Arc Furnace Process, Blast Furnace Process, Induction Furnace Process) •By Application (Foundries, Metalworking, Alloy Production, Recycling and Reclamation, Others) •By End-User Industry (Steel Manufacturing, Casting and Forging, Automotive Industry, Aerospace and Defense, Construction, Others) •By Distribution Channel (Direct Sales, Distributors and Wholesalers, Online Sales) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | High Purity Iron Inc., Ironveld Plc, Neo Metaliks Ltd., Asmet (UK) Ltd., Eramet Group, QIT-Fer et Titane (Rio Tinto Iron & Titanium), Richards Bay Minerals (RBM), Tronox Holdings plc, TiZir Limited, Tinfos AS, Saraf Group, Metinvest International SA, Hebei Long Feng Shan Casting Industry Co., Ltd., Miller and Company LLC, Mineral-Loy, Jindal Stainless Limited, Nippon Steel Corporation, Kobe Steel, Ltd., Dillinger Hütte, and Mideast Integrated Steel Ltd. |

Frequently Asked Questions

Electric arc furnace process adoption and precision carbon-control technologies help meet green steel goals and rising demand for low-carbon feedstock and premium alloys.

Special grade pig iron ensures tighter impurity control needed for high-strength alloys and precision foundry applications critical in automotive and aerospace sectors.

Automotive casting uses low-sulfur pig iron to produce lighter, emission-efficient engine parts, as reported by Nippon Steel and supported by US foundry imports.

The Asia-Pacific pig iron market is the fastest-growing region, supported by infrastructure expansion and higher low-carbon pig iron production noted by India’s Ministry of Steel.

Rising demand for special grade pig iron in precision automotive casting and green steel industry initiatives is driving high purity pig iron market growth.

Get in Touch