Stratospheric UAV Payload Technology Market Report Scope & Overview:

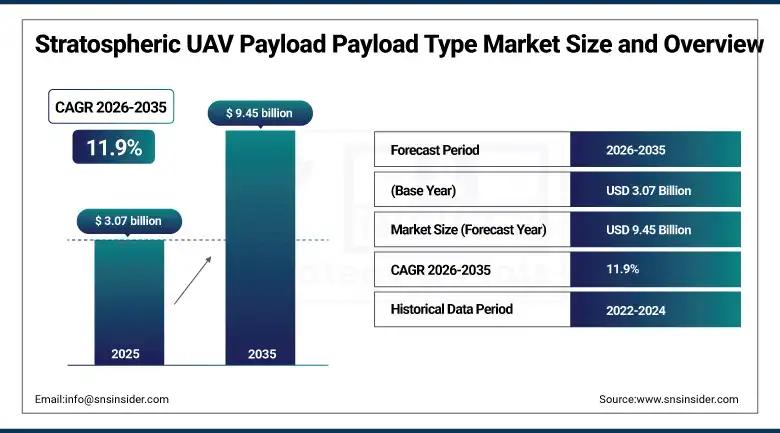

The Stratospheric UAV Payload Technology Market was valued at USD 3.07 Billion in 2025 and is expected to reach USD 9.45 Billion by 2035, growing at a CAGR of 11.9% from 2026–2035.

The global stratospheric UAV payload technology market is advancing on the convergence of persistent surveillance requirements, communications relay demand, and scientific monitoring needs that high-altitude long-endurance platforms uniquely serve at a cost and operational flexibility advantage over traditional satellites. Stratospheric UAVs operating at altitudes between 15 and 50 kilometres deliver satellite-like capabilities including broadband communications relay, wide-area persistent surveillance, and real-time environmental monitoring at a fraction of satellite deployment cost and with the operational flexibility to reposition, service, or recover the aircraft as mission requirements evolve. Defence agencies worldwide are investing in stratospheric UAV programmes to extend ISR coverage over adversary territory and provide resilient communications relay in contested environments where low-earth-orbit satellites face growing anti-satellite weapon threats. Solar-powered stratospheric platforms are simultaneously demonstrating multi-month continuous operation capability that makes them commercially viable substitutes for certain geostationary satellite functions at dramatically lower capital cost.

Airbus completed an extended endurance flight test of its Zephyr S solar-powered stratospheric UAV in 2024, achieving over 64 days of continuous flight at stratospheric altitude on solar power alone. The test validated the platform’s operational viability for persistent intelligence, surveillance, and communications relay missions and directly demonstrated the multi-month endurance capability that makes solar stratospheric UAVs commercially competitive with the persistent coverage that low-earth-orbit satellite constellations provide at substantially higher capital cost.

Market Size and Forecast

-

Market Size in 2026E: USD 3.40 Billion

-

Market Size by 2035: USD 9.45 Billion

-

CAGR: 11.9% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Stratospheric UAV Payload Technology Market - Request Free Sample Report

Stratospheric UAV Payload Technology Market Trends

-

Rising investment in solar-powered stratospheric UAVs is enabling long-endurance surveillance and communication operations.

-

Growing payload miniaturization is improving multi-mission intelligence and monitoring capabilities.

-

Increasing defence spending on resilient communication relay systems is accelerating military UAV deployment.

-

Expanding commercial applications in agriculture, disaster management, and climate monitoring are supporting market growth.

-

Rising adoption of AI-enabled autonomous payload management is enhancing mission efficiency and real-time decision-making.

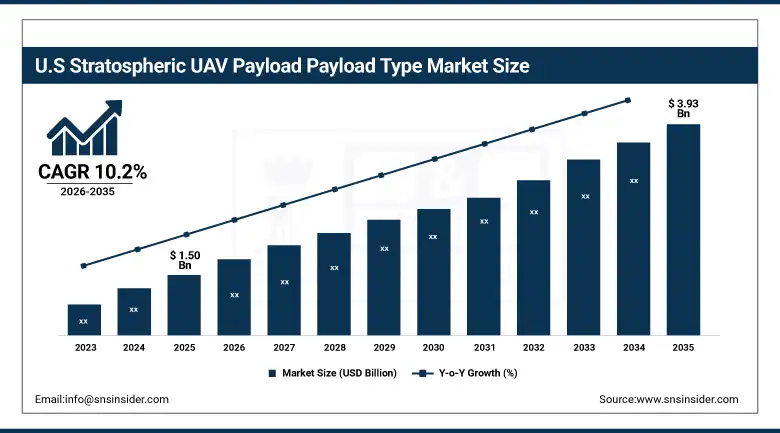

The U.S. Stratospheric UAV Payload Technology Market Outlook

The U.S. Stratospheric UAV Payload Technology Market was valued at approximately USD 1.50 Billion in 2025 and is expected to reach approximately USD 3.93 Billion by 2035, growing at a CAGR of approximately 10.2%.

The United States is the world’s dominant stratospheric UAV payload technology market, anchored by the Department of Defense’s persistent ISR and communications relay programme investment, the intelligence community’s classified high-altitude collection requirements, and the concentration of the market’s leading platform and payload technology providers. Northrop Grumman’s RQ-4 Global Hawk programme, General Atomics’ Predator and extended range platforms, and Lockheed Martin’s classified high-altitude programme investments collectively define the U.S. market’s technological frontier. The U.S. Space Force’s investment in stratospheric platforms as a complement to satellite capabilities reflects the growing strategic importance of high-altitude persistent platforms in the contested space environment that adversary anti-satellite capabilities are creating. FAA regulatory framework evolution for stratospheric UAV operations is progressively creating the commercial flight approval pathway that civilian stratospheric applications require.

Northrop Grumman delivered an enhanced Block 40 RQ-4 Global Hawk to the U.S. Air Force in 2024 with upgraded multi-spectral sensor integration and improved data link capacity that substantially increases the platform’s intelligence collection volume per sortie. The delivery demonstrated the U.S. government’s continued investment in proven high-altitude ISR capability alongside the emerging solar stratospheric programmes whose longer endurance promises future persistence advantages.

Stratospheric UAV Payload Technology Market Segment Analysis

-

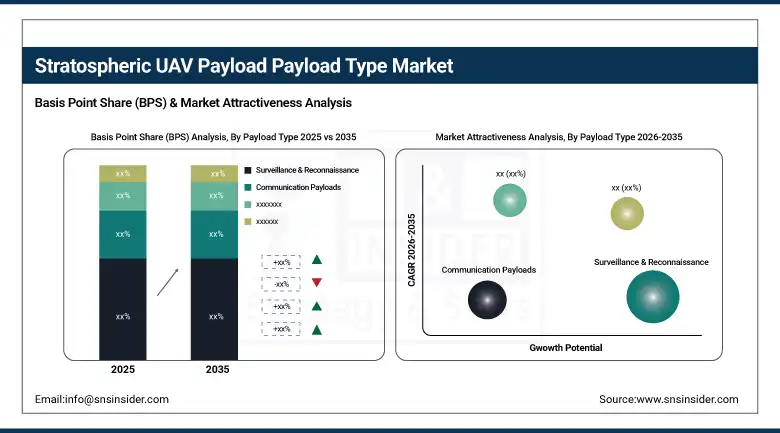

By Payload Type, surveillance & reconnaissance payloads dominated the stratospheric UAV payload technology market with approximately 44% share in 2025. Communication payloads are the fastest-growing segment with a CAGR of around 15.20% during 2026–2035.

-

By Technology, electro-optical technology held the largest market share of nearly 39% in 2025. Radar technology is projected to be the fastest-growing segment with a CAGR of approximately 14.80%.

-

By Application, defence & military dominated the market with an estimated share of about 52% in 2025. Commercial communications is the fastest-growing application segment with a CAGR of nearly 16.10% through the forecast period.

-

By Platform, fixed-wing HALE UAVs accounted for the dominant market share of around 58% in 2025. Solar-powered UAVs are the fastest-growing platform segment with a CAGR of approximately 17.30% during 2026–2035.

By Payload Type, surveillance dominates, communications grows fastest

Surveillance and reconnaissance retained the dominant payload type position in the stratospheric UAV payload technology market in 2025. The commercial and operational primacy of ISR payloads reflects the foundational role that persistent wide-area intelligence collection plays in both military operational planning and the commercial applications, including border monitoring, maritime domain awareness, and infrastructure inspection, that stratospheric UAVs serve across the spectrum of government and civilian customers. Defence agencies that invest in stratospheric UAV programmes almost universally define ISR as the primary mission whose payload capability determines platform value, creating a procurement logic that concentrates the majority of payload technology investment in the surveillance and reconnaissance category. Electro-optical and multi-spectral sensors, wide-area motion imagery systems, and ground moving target indicator radar collectively constitute the ISR payload suite whose performance improvement drives successive generations of stratospheric UAV payload development investment.

Communication payloads are the fastest-growing payload type in the stratospheric UAV payload technology market because the strategic value of resilient, high-altitude communications relay in contested electromagnetic environments is receiving rapidly growing defence investment alongside the commercial opportunity of providing broadband connectivity to underserved populations through stratospheric communications platforms. The U.S. military’s JADC2 communications resilience requirement creates structural demand for communications relay payloads that can survive in contested environments where satellite links face anti-satellite weapon threats. Simultaneously, commercial initiatives including Airbus Zephyr’s broadband relay demonstration and SoftBank’s HAPSMobile programme are validating the commercial business case for stratospheric communications as a cost-effective alternative to satellite broadband for specific coverage scenarios.

By Application, defence dominates, commercial communications grows fastest

Defence and military retained the dominant application position in the stratospheric UAV payload technology market in 2025. The sector’s commercial primacy reflects the strategic imperative that drives defence procurement: persistent, wide-area ISR and communications relay capability over adversary territory or in contested environments where manned aircraft cannot operate continuously. Stratospheric UAVs’ combination of endurance measured in days, weeks, or months; operational altitudes above the reach of most short-range air defence systems; and payload capacity sufficient for multiple intelligence collection and communications functions simultaneously creates a capability profile that no alternative platform provides at equivalent cost and operational risk. The U.S., UK, France, and Australia defence programmes collectively sustain the majority of the market’s current commercial activity, with growing investment from the Middle East, India, and Asia Pacific defence agencies adding new national programme demand.

Commercial communications is the fastest-growing application in the stratospheric UAV payload technology market because the convergence of technology maturity, regulatory progress, and commercial demand for connectivity in remote and underserved regions is creating viable business cases for stratospheric communications relay at a scale that was not commercially credible five years ago. Airbus Zephyr’s extended endurance demonstration, HAPSMobile’s Sunglider programme, and Facebook’s Aquila conceptual validation have collectively established the technology’s feasibility for broadband relay applications. The commercial opportunity is substantial: providing 4G and 5G broadband equivalent connectivity to the 3 billion people without reliable internet access in remote regions requires the kind of persistent area coverage that stratospheric UAVs can provide at lower cost than satellite alternatives for many geographic coverage scenarios.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

United Kingdom |

28.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Stratospheric UAV Payload Technology Market Insights

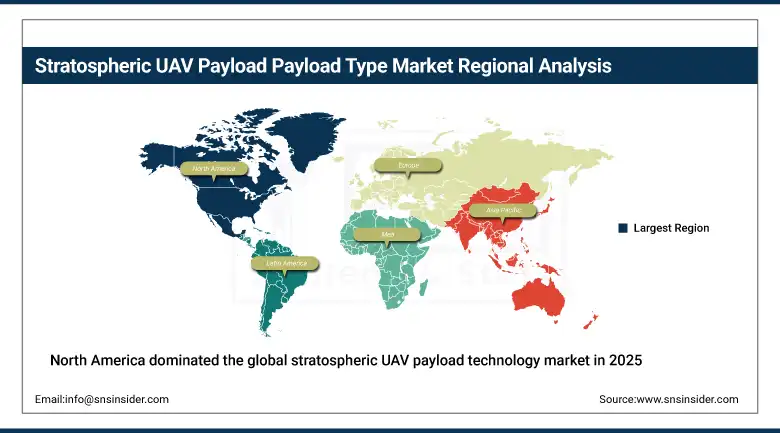

North America dominated the global stratospheric UAV payload technology market in 2025 with approximately 49.07% of global revenues, with the United States accounting for approximately 87.4% of North American revenues. The region’s market leadership reflects its extraordinary concentration of the world’s leading stratospheric UAV and payload technology companies, the U.S. military’s sustained multi-billion-dollar ISR and communications programme investment, and the intelligence community’s classified stratospheric collection requirements whose combined procurement defines the most commercially significant national market for stratospheric UAV payload technology globally.

Canada contributes approximately 12.6% of North American revenues through its military ISR programme participation in Five Eyes intelligence alliance operations, its aerospace industry’s stratospheric UAV component manufacturing capability, and growing commercial interest in stratospheric platforms for Arctic surveillance, natural resource monitoring, and remote connectivity applications where Canada’s vast geographic extent creates compelling operational use cases for persistent high-altitude coverage.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Stratospheric UAV Payload Technology Market Insights

Europe is the world’s second-largest stratospheric UAV payload technology market, characterised by the Airbus Zephyr S solar stratospheric programme’s position as the global benchmark for solar-powered stratospheric UAV endurance and the active national military investment in MALE and HALE UAV capability by the UK, France, Germany, and Italy. The United Kingdom accounts for approximately 28.4% of European revenues through its military ISR programme investment, QinetiQ’s stratospheric payload technology specialisation, and the UK Ministry of Defence’s Airbus Zephyr S evaluation programme that validated the platform’s operational performance for persistent ISR and communications relay missions over extended flight periods.

France and Germany are significant secondary European markets where national defence programme investment in high-altitude surveillance and the EU’s MALE RPAS programme are creating structured stratospheric UAV payload procurement. The European Defence Fund’s UAV technology investment is progressively improving the European defence industrial base’s stratospheric payload capability, reducing dependence on U.S. technology for NATO alliance stratospheric ISR programmes.

Asia Pacific Stratospheric UAV Payload Technology Market Insights

Asia Pacific is the fastest-growing regional stratospheric UAV payload technology market, driven by China’s comprehensive high-altitude UAV development programme, India’s strategic ISR investment under its defence modernisation programme, Japan’s growing high-altitude surveillance capability investment, and South Korea and Australia’s ISR programme expansion. China accounts for approximately 44.8% of Asia Pacific revenues through its indigenous stratospheric UAV development including the solar-powered Caihong solar-powered stratospheric platforms and classified military high-altitude systems whose capabilities are challenging the U.S. and European stratospheric UAV technology leadership in the Asian theatre.

India represents the most commercially significant emerging market within Asia Pacific, where the Indian Air Force’s HALE UAV procurement programme and the DRDO’s indigenous stratospheric UAV development are creating domestic demand and supply development simultaneously. Japan’s SoftBank subsidiary HAPSMobile’s Sunglider stratospheric communications programme represents the most commercially advanced civilian stratospheric application in Asia Pacific, targeting rural broadband connectivity across Southeast Asia through solar stratospheric relay.

MEA & Latin America Stratospheric UAV Payload Technology Market Insights

Middle East and Africa and Latin America are growing stratospheric UAV payload technology markets where border surveillance, maritime domain awareness, and military ISR requirements are creating defence procurement demand for high-altitude persistent platforms. UAE leads MEA revenues at approximately 38.4% of the regional total through its advanced defence technology procurement investment, the Emirates’ strategic interest in persistent surveillance capability for regional security monitoring, and Abu Dhabi’s active defence aerospace development programme whose investment in UAV technology reflects the country’s ambition to develop indigenous high-altitude aviation capability.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its vast geographical expanse whose border surveillance, Amazon monitoring, and maritime domain awareness requirements create compelling operational use cases for persistent stratospheric coverage that no other platform type serves as efficiently. Brazil’s Air Force high-altitude ISR programme and EMBRAER’s strategic interest in UAV development create domestic supply development alongside the military demand that sustains the Brazilian stratospheric UAV payload market.

Market Dynamics

Growth Drivers: Defence ISR and communications relay investment driving sustained programme procurement

Defence sector investment in persistent ISR and communications relay capability is the market’s most commercially certain growth driver. Stratospheric UAVs’ unique combination of endurance, altitude, and payload capacity creates an ISR and communications capability that no alternative platform provides at equivalent lifecycle cost. The growing anti-satellite weapon threat environment simultaneously strengthens the strategic case for stratospheric UAV platforms as resilient alternatives to vulnerable satellite assets for certain persistent coverage requirements whose operational continuity cannot depend on potentially targetable satellite infrastructure.

Solar propulsion technology maturation is transforming stratospheric UAV operational economics by eliminating the fuel resupply limitation that constrains conventional aircraft endurance. Airbus Zephyr S’s 64-day continuous flight achievement validates the multi-month persistence capability that solar stratospheric platforms can provide, creating operational scenarios including persistent sovereignty enforcement over exclusive economic zones, continuous climate monitoring over remote regions, and sustained communications relay in areas without terrestrial infrastructure that were previously only feasible with expensive satellite alternatives.

Restraints: High development and programme cost limiting adoption to well-funded defence programmes

The high development cost of stratospheric UAV programmes limits market participation to well-funded national defence programmes and commercially motivated private sector investments whose expected revenue scale justifies the capital intensity of stratospheric platform development. The developmental risk of operating at stratospheric altitudes, where temperatures, pressures, and radiation environments impose severe constraints on component selection and system design, creates engineering complexity that substantially elevates programme cost relative to conventional UAV development whose design environment is far less demanding.

Regulatory certification for stratospheric airspace operations presents a meaningful barrier to commercial programme development. Stratospheric altitude operations require international airspace coordination, telecommunications spectrum licensing for payload frequencies, and safety certification frameworks whose development by regulators is still maturing in most jurisdictions. The regulatory uncertainty this creates extends commercial programme timelines and increases the compliance investment required before commercial stratospheric operations can begin at the scale that viable business models require.

Opportunities: Persistent broadband relay for underserved populations, climate science and environmental monitoring mission development, and defence resilient communications programme expansion

Persistent broadband communications relay represents the most commercially significant near-term application expansion for stratospheric UAV payload technology beyond its established defence ISR market. The 3 billion people without reliable internet access, concentrated in sub-Saharan Africa, South and Southeast Asia, and Latin America’s remote regions, represent an addressable market for stratospheric broadband relay whose coverage economics compare favourably to satellite broadband and ground infrastructure extension in specific geographic scenarios. Each successful commercial deployment demonstration creates the reference evidence that attracts the programme investment and regulatory support needed to scale commercial stratospheric communications operations.

Climate science and environmental monitoring represent a high-value niche application where stratospheric UAVs’ unique altitude range enables measurements that neither aircraft nor satellites can efficiently provide. Atmospheric composition sampling at stratospheric altitudes, ozone layer characterisation, stratospheric aerosol measurement, and upper atmosphere weather research collectively represent scientific payload applications whose institutional funding from government research agencies creates a growing civilian stratospheric payload procurement channel independent of commercial and military demand.

Recent Developments:

-

2024: Airbus completed an extended endurance validation flight of its Zephyr S solar-powered stratospheric UAV in 2024, achieving over 64 days of continuous flight at stratospheric altitude on solar power alone, validating the multi-month persistence capability that makes solar stratospheric platforms commercially competitive with satellite alternatives for specific persistent coverage missions.

-

2024: Northrop Grumman delivered an enhanced Block 40 RQ-4 Global Hawk to the U.S. Air Force in 2024 with upgraded multi-spectral sensor integration and expanded data link capacity, demonstrating continued U.S. military investment in proven high-altitude ISR capability alongside emerging solar stratospheric platform development programmes.

-

2024: HAPSMobile’s Sunglider stratospheric UAV programme advanced its commercial broadband relay capability demonstration in 2024, conducting connectivity trials targeting rural internet access provision over Southeast Asian markets whose large populations without reliable broadband access represent the most commercially significant civilian stratospheric communications relay addressable market in Asia Pacific.

Stratospheric UAV Payload Technology Market Key Players are:

-

Northrop Grumman Corporation

-

Lockheed Martin Corporation

-

BAE Systems plc

-

RTX Corporation

-

Thales Group

-

L3Harris Technologies Inc.

-

Leonardo S.p.A.

-

Airbus SE

-

Boeing Company

-

Israel Aerospace Industries Ltd.

-

Elbit Systems Ltd.

-

General Atomics Aeronautical Systems Inc.

-

Aurora Flight Sciences (Boeing)

-

AeroVironment Inc.

-

BAE Systems Australia

-

Sierra Nevada Corporation

-

Zephyr (Airbus Defence and Space)

-

Skydweller Aero Inc.

-

Shield AI Inc.

-

Raytheon Intelligence & Space (RTX Corporation)

Stratospheric UAV Payload Technology Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.07 Billion |

| Market Size by 2035 | USD 9.45 Billion |

| CAGR | CAGR of 11.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Payload Type (Surveillance & Reconnaissance, Communication Payloads, Scientific & Environmental, Navigation & Positioning, Others) • By Technology (Electro-Optical, Infrared, Radar, LIDAR, SIGINT, Others) • By Application (Defence & Military, Commercial Communications, Environmental Monitoring, Disaster Management, Precision Agriculture, Others) • By Platform (Fixed-Wing HALE UAV, Solar-Powered UAV, Hybrid Propulsion UAV) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Northrop Grumman Corporation, Lockheed Martin Corporation, BAE Systems plc, RTX Corporation, Thales Group, L3Harris Technologies Inc., Leonardo S.p.A., Airbus SE, Boeing Company, Israel Aerospace Industries Ltd., Elbit Systems Ltd., General Atomics Aeronautical Systems Inc., Aurora Flight Sciences (Boeing), AeroVironment Inc., BAE Systems Australia, Sierra Nevada Corporation, Zephyr (Airbus Defence and Space), Skydweller Aero Inc., Shield AI Inc., and Raytheon Intelligence & Space (RTX Corporation) |

Frequently Asked Questions

North America dominated the Stratospheric UAV Payload Technology Market in 2025, holding approximately 49.07% of global revenues, with the United States accounting for approximately 87.4% of North American revenues.

Surveillance & Reconnaissance dominated the Stratospheric UAV Payload Technology Market in 2025.

Rising defence investment in persistent ISR and communication systems, advancing solar propulsion technology, and growing commercial broadband connectivity demand are driving growth in the stratospheric UAV payload technology market.

The Stratospheric UAV Payload Technology Market was valued at USD 3.07 Billion in 2025.

The Stratospheric UAV Payload Technology Market is expected to grow at a CAGR of 11.9% from 2026 to 2035.

Get in Touch