Subfloor Adhesives Market Report Scope & Overview:

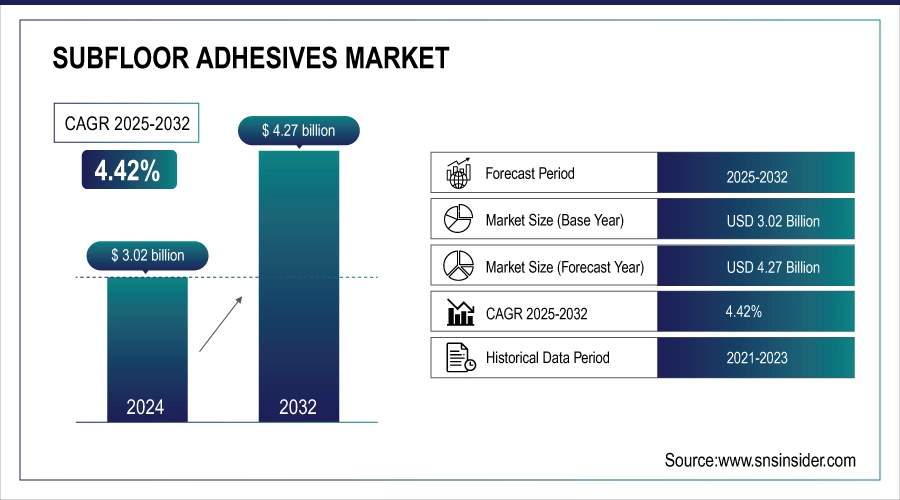

The Subfloor Adhesives Market Size was valued at USD 3.02 Billion in 2024 and is expected to reach USD 4.27 Billion by 2032, growing at a CAGR of 4.42% over the forecast period of 2025-2032.

Heavy government spending on public infrastructure and sharp spikes in residential building is driving demand for subfloor adhesives. Increasing obligations on the part of governments to build green and falling investments in the sustainable public housing and renovation projects are also boosting the demand for low-VOC, durable adhesive technologies.

Total US construction spending for Jun 2025 was an annualized USD 2.136 trillion vs a revised USD 2.144 trillion in May (~ 0.4%), but still substantial by scale.

Subfloor Adhesives Market Size and Forecast

-

Market Size in 2024: USD 3.02 Billion

-

Market Size by 2032: USD 4.27 Billion

-

CAGR: 4.42% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Subfloor Adhesives Market - Request Free Sample Report

Key Subfloor Adhesives Market Trends:

-

Shift toward Low-VOC & Eco-Friendly Adhesives due to environmental regulations and indoor air quality concerns.

-

Growing adoption of Hybrid Adhesives combining polyurethane, acrylic, and epoxy for strength and flexibility.

-

Increasing demand from Renovation & Remodeling Projects, boosting fast-curing and easy-to-apply adhesives.

-

Technological Advancements enhancing installation efficiency, moisture resistance, and durability.

-

Expansion of Distribution Channels, including e-commerce and retail DIY stores.

-

Surge in Infrastructure and Housing Investments driving demand for high-performance subfloor adhesives.

U.S. Subfloor Adhesives Market Insights:

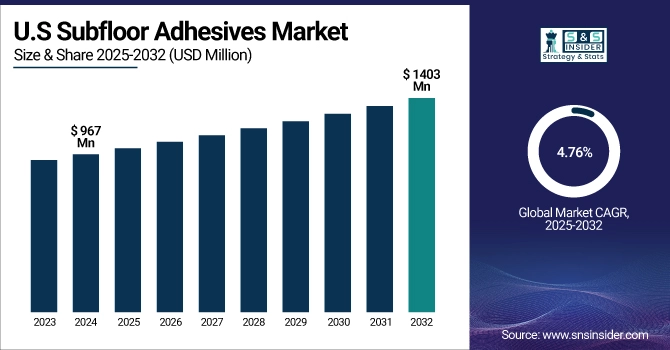

The U.S. Subfloor Adhesives Market size was valued at USD 967 Million in 2024 and is projected to reach USD 1403 Million by 2032, growing at a CAGR of 4.76% during 2025-2032.

In the U.S., the subfloor adhesives sector is the most significant due to mature construction industry, stringent standards for flooring quality, and the incorporation of engineered and composite flooring materials continue to drive market growth. ADHESIVES Professional installers and contractors demand adhesives that perform well and are easy to work with while consumers want an adhesive that delivers on its promises, every time.

The development in Franklin International is its leading low-emission, high-strength adhesives for subfloor applications for residential and commercial uses. The increase is an indication of a rise in the demand for sustainable and effective products in the U.S. construction market, leading to market expansion.

Subfloor Adhesives Market Growth Drivers

-

Surge in Infrastructure Development Drives the Market Growth

The subfloor adhesives market is growing with economic expansion. A rise in the number of construction projects globally, large amount of money is being invested by the government in the development of infrastructure, transportation network, residential structures, and commercial buildings, and this in turn has created the demand for building materials, such as adhesives.

For instance, India's 2024–25 budget earmarks ₹11.11 lakh crore (USD 132.85 billion) for developing infrastructure, which is 3.4% of the country's GDP. This enormous investment is projected to spark economic growth and job creation, further increasing the demand for building materials such as adhesives.

Subfloor Adhesives Market Restraints:

-

Stringent Regulatory Standards May Hamper the Market Growth

Strict environmental regulatory mandates, such as those about VOC emissions, are challenging the growth of the subfloor adhesives market. Government regulators, such as the U.S. Environmental Protection Agency (EPA) establish stringent VOC content requirements for adhesives as a means of addressing environmental and health concerns. For instance, in EPA's rules at 40 CFR Part 59, EPA lists certain categories of products among which adhesives fall, and requires that VOC emissions be controlled in order to maintain air quality. This legislation forces manufacturers to reformulate products, which can result in higher manufacturing costs and disruptions in the supply chain.

Subfloor Adhesives Market Opportunities:

-

Adoption of Green Building and Sustainable Construction Creates an Opportunity for the Market

Growing preference for eco-friendly structures is a key growth opportunity for subfloor adhesive manufacturers. Sustainable building is also driven by governments seeking to reduce their environmental impact with regulations, incentives, or certifications, such as LEED. For instance, GRIHA (Green Rating for Integrated Habitat Assessment) of India promotes green building practices, such as the use of low-VOC and environmentally friendly adhesives and provides tax benefits and fast-track approvals to such certified projects. Likewise, the U.S. Green Building Council (USGBC) is driving LEED-certified buildings that require low-emitting materials, driving the demand for green adhesives for flooring. They give manufacturers a chance to introduce sustainability-promoting adhesive solutions, capture environmentally conscious consumers, and enter markets with government-led sustainability initiatives readily in place.

Subfloor Adhesives Market Segment Highlights:

-

By Product Type: Polyurethane Adhesives led with 32% share in 2024; Hybrid Adhesives are the fastest growing (CAGR 4.8%).

-

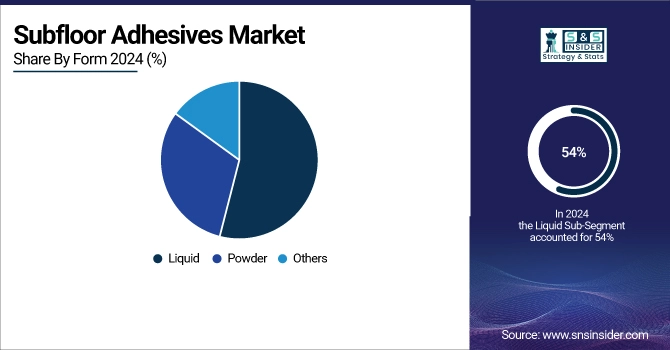

By Form: Liquid adhesives held 54% share in 2024; Foam-based & Spray-on (Others) are the fastest growing (CAGR 4.5%).

-

By Distribution Channel: Direct Sales accounted for a 40% share in 2024; E-commerce Platforms are the fastest growing (CAGR 4.7%).

-

By End-use: Residential Construction dominated with 45% share in 2024; Industrial Facilities are the fastest growing (CAGR 4.6%).

Subfloor Adhesives Market Segment Analysis:

-

By Product Type

Polyurethane adhesives held the highest market share of around 32% for subfloor adhesives in 2024, due to their superior bonding strength, flexibility, and adhesiveness on multiple substrates, such as wood, concrete and engineered flooring. Moisture and impact resistant, these adhesives are often used in residential and commercial construction. Furthermore, Hybrid adhesives will be the fastest-growing product segment (CAGR ~4.8%) on account of value-added properties of the product, such as polyurethane and silane technology compatibility, providing low VOC and nature-friendly products. Rising use in green building projects and sustainable building practices globally is also aiding in establishing itself in a growing segment.

-

By Form

Liquid adhesives accounted for the largest share at 54% in 2024 owing to easy application, quick bonding, and being favourable for large floor coverings. They are popular in professional installations and renovation projects as they are versatile. Powders is the fastest growing segment (CAGR 4.5%), owing to their added stability during storage and usage, shelf life, and good performance in high temperature or high humidity settings. Growing demand in industrial and developing markets also plays a major role in the growth of the market.

-

By Distribution Channel

Direct sales segment dominated the market in 2024, accounting for over 40% share with long-term contracts with construction companies, architects, and contractors for bulk purchase of products for current projects. This network provides the necessary flow and technical support required for large construction projects. On the other hand, E-commerce is the fastest-growing distribution channel (CAGR 4.7%), powered by the growth of digital procurement in small contractors, independent builders, and DIY end-users. Online platforms are convenient, cost-saving, and deliver faster, and more and more buyers are being lured away from traditional channels.

-

By End-use Industry

The residential buildings segment held the largest market share of 45% in 2024, due to ongoing urban housing projects, renovations, and new real estate development, all bolstering demand for stable subfloor adhesives. Homeowners and builders prefer adhesives that are durable and have strong adhesion, and are hence, leading segment. Industrial establishments are the most rapidly growing end-user (CAGR 4.6%), on the back of an increasing number of warehouses, manufacturing facilities, and specialized industrial flooring, where heavy-duty and long-lasting adhesives are required to bear maximum load and frequent usage. Investments in logistics infrastructure and smart factories globally also help this expansion.

Subfloor Adhesives Market Regional Analysis:

North America Subfloor Adhesives Market Insights:

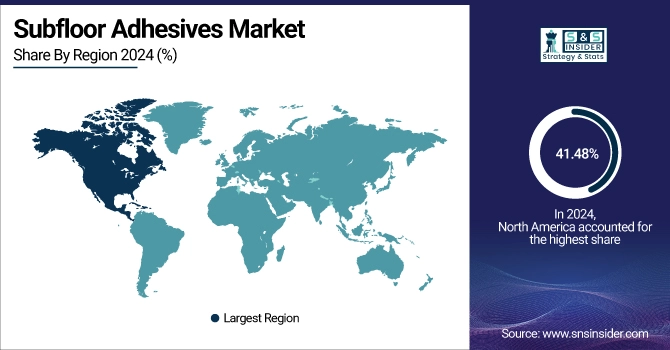

North America held the largest Subfloor Adhesives market share in 2024, around 41.48% 2024. It is attributed to the presence of a well-established construction industry, adoption of new flooring technology, and rising demand for durable, high-performance adhesives in both residential and commercial construction. In addition, strong construction spending, notably in the U.S. and Canada, will back the use of higher-value flooring products in the region. Henkel recently invested to increase adhesive capacity in the U.S., meet the growing demand for sustainable, low-VOC products, and support overall growth in North America. Building codes are evolving to mandate not just appearance, but quality and longevity in flooring installations, further strengthening this growth, particularly within North America as a leading market globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Subfloor Adhesives Market Insights:

Asia Pacific is becoming a swiftly growing market for the subfloor adhesives owing to urbanization, huge infrastructure projects, and increasing residential and commercial construction. It is also worth noting that India, China, and Japan are putting ever more infrastructure in place, including housing, industrial parks and commercial buildings that need reliable subflooring adhesives for longevity and safety. Presently, there is a growing trend, where India based adhesive manufacturers have been investing for the development of eco-friendly high performance adhesive products in line with the government’s vision for sustainable construction. This, teamed with growing awareness of environmentally friendly constructions, is driving the uptake of high-end adhesive solutions in the region.

Europe Subfloor Adhesives Market Insights:

In Europe, there is heavy demand for subfloor adhesives as a result of urban housing projects, commercial construction, and remodeling projects. Nations including France, Italy, and the U.K., focusing on infrastructural developments and eco-friendly construction, are promoting the use of low-VOC and high-performing adhesives. A new addition to the European sector is Sika AG, which increased its adhesive production in France in response to the increasing demand for green subfloor adhesive for use in construction and refurbishment projects. The stringent product and environmental regulations in the region also favor the use of high-quality adhesives.

Germany Subfloor Adhesives Market Insights:

Germany has a major share of the European subfloor adhesives market due to its advanced manufacturing industry and stringent construction standards, along with high-quality building materials. Across Germany, every single person is dependent on high-end adhesive and sealant solutions that facilitate durable constructions and appealing interiors. Recently, the local companies have introduced new polyurethane-based adhesives that, while achieving high adhesion strength, can be used to minimize the emissions of VOCs. Such developments are well in line with Germany’s environmental legislation and energy standards, thereby fuelling the persistent expansion of the subfloor adhesives market.

Latin America (LATAM) and Middle East & Africa (MEA) Subfloor Adhesives Market Insights

The market for subfloor adhesives is gradually expanding in Latin America and MEA owing to rapid urbanization, infrastructural investment, and a rise in residential, commercial, and industrial construction. In Latin America, countries including Brazil, Mexico, and Argentina are observing rising application of high-performance adhesives for long-lasting floors owing to the presence of government-endorsed infrastructure projects. The new Mapei S.p.A. production plant for adhesives in Brazil speaks to the high demand for flooring that can hold up under the weather. In the same vein, the upsurge in developing economies, such as the UAE, Saudi Arabia, and South Africa calls for adhesives capable of withstanding high temperature and harsh weather conditions in MEA.

Competitive Landscape for Subfloor Adhesives Market:

Henkel AG & Co. KGaA

Henkel is one of the leading global players in adhesive technologies, offering a wide range of subfloor adhesive solutions for residential, commercial, and industrial flooring applications. The company emphasizes low-VOC, high-strength, and quick-curing products designed to meet modern green building standards.

-

In March 2024, Henkel announced the expansion of its adhesives production facility in North Carolina, U.S., dedicated to manufacturing sustainable flooring adhesives. This move strengthens Henkel’s North American footprint, shortens supply chains, and supports the rising demand from the construction and renovation sectors.

Sika AG

Sika is a prominent supplier of flooring and construction chemicals, including subfloor adhesives that deliver excellent moisture resistance, bond strength, and durability. The company focuses heavily on R&D to provide hybrid adhesive technologies with improved sustainability profiles.

-

In July 2024, Sika inaugurated a new technology center in Singapore to enhance adhesive innovation for flooring applications in Asia Pacific. The facility will accelerate the development of moisture-curing adhesives and provide faster technical support to regional construction customers.

Mapei S.p.A.

Mapei is a major provider of flooring adhesives, offering versatile polyurethane, acrylic, and hybrid solutions for subflooring in residential, commercial, and sports applications. The company is known for its strong distribution networks across Europe and the Americas.

-

In May 2024, Mapei launched a new range of solvent-free, low-VOC subfloor adhesives in Italy, targeting the European market’s shift toward eco-friendly construction products. The launch strengthens Mapei’s sustainability portfolio while aligning with EU green building initiatives.

3M Company

3M manufactures high-performance adhesives for industrial and construction applications, including subfloor adhesives that deliver fast-setting, durable, and flexible bonding. Their focus is on advanced formulations that reduce installation time and enhance worker safety.

-

In October 2023, 3M introduced an innovative spray-applied subfloor adhesive system in the U.S., designed for large-scale commercial and residential projects. This product launch reduces installation time by up to 30% and improves workplace ergonomics compared to traditional liquid adhesives.

Arkema S.A.

Arkema provides specialty chemicals and adhesive technologies with a growing focus on sustainable and bio-based solutions. Its subfloor adhesives are widely used in commercial flooring and industrial construction due to their strong bonding and resistance to environmental stress.

-

In February 2024, Arkema invested in expanding its Bostik adhesives division in France, adding capacity for hybrid subfloor adhesives. This expansion supports the growing European demand for high-performance, environmentally friendly flooring adhesives while enhancing Arkema’s innovation pipeline.

Subfloor Adhesives Market Key Players:

-

Henkel AG & Co. KGaA

-

Sika AG

-

Arkema Group (Bostik)

-

3M Company

-

H.B. Fuller Company

-

Mapei S.p.A.

-

BASF SE

-

The Dow Chemical Company

-

DAP Products Inc.

-

Franklin International

-

Akzo Nobel N.V.

-

Forbo Group

-

Pidilite Industries Ltd.

-

Royal Adhesives & Sealants

-

Ardex GmbH

-

Tremco Incorporated

-

Fosroc International

-

Laticrete International, Inc.

-

Soudal Group

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.02 Billion |

| Market Size by 2032 | USD 4.27 Billion |

| CAGR | CAGR of 4.42% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type: Polyurethane Adhesives, Epoxy Adhesives, Acrylic Adhesives, Hybrid Adhesives, Others (Water-based, Solvent-based, Cementitious, Pressure-sensitive) • By Form: Liquid, Powder, Others (Foam-based, Spray-on, Specialty formulations) • By Distribution Channel: Direct Sales, Distributors & Wholesalers, Retail Stores, E-commerce Platforms, Others (Specialty Suppliers, Local Dealers) • By End-use: Residential Construction, Commercial Buildings, Industrial Facilities, Others (Sports Flooring, Marine, Healthcare) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Henkel AG & Co. KGaA, Sika AG, Arkema Group (Bostik), 3M Company, H.B. Fuller Company, Mapei S.p.A., BASF SE, The Dow Chemical Company, Illinois Tool Works Inc., DAP Products Inc., Franklin International, Akzo Nobel N.V., Forbo Group, Pidilite Industries Ltd., Royal Adhesives & Sealants, Ardex GmbH, Tremco Incorporated, Fosroc International, Laticrete International, Inc., Soudal Group |

Frequently Asked Questions

Ans: The Subfloor Adhesives Market comprises adhesives used to bond flooring materials to subfloors, ensuring durability, stability, and structural integrity in residential, commercial, and industrial construction.

Ans: Growth is driven by rapid urbanization, infrastructure development, rising construction activities, demand for durable and low-VOC adhesives, and adoption of sustainable building practices.

Ans: The market is growing steadily with a global CAGR of approximately 4.42%, supported by increasing residential and commercial construction and the shift toward advanced flooring solutions.

Ans: North America leads the market, followed by Europe and Asia Pacific, due to high construction activities, advanced technology adoption, and strong infrastructure investments.

Ans: Key players include Henkel AG & Co. KGaA, Sika AG, Arkema Group (Bostik), 3M Company, H.B. Fuller Company, Mapei S.p.A., BASF SE, The Dow Chemical Company, Illinois Tool Works Inc., and DAP Products Inc.

Get in Touch