Digital Signal Processor Market Report Scope & Overview:

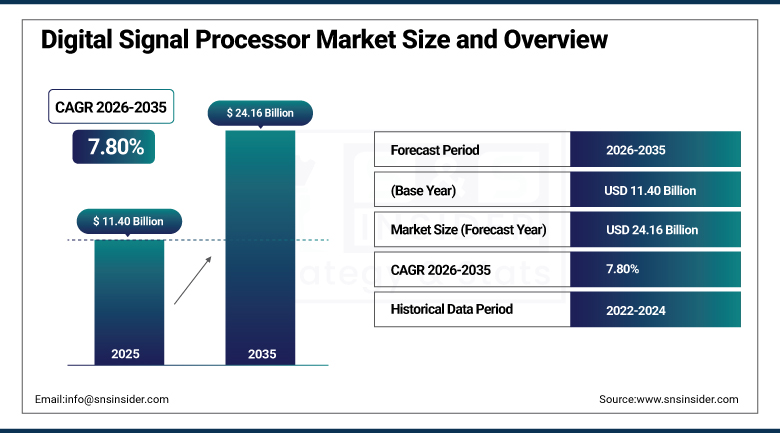

The Digital Signal Processor Market size was valued at USD 11.40 Billion in 2025 and is expected to reach USD 24.16 Billion by 2035, growing at a CAGR of 7.80% from 2026 to 2035.

The Digital Signal Processor Market continues to evolve as chip designers push signal processing capability deeper into integrated system-on-chip architectures that fuse traditional DSP cores with CPUs and neural processing engines for edge artificial intelligence workloads. Rising demand for advanced consumer electronics including smartphones, tablets, and wearables continues requiring higher-speed signal processing capability, while automotive systems spanning advanced driver-assistance systems, infotainment, and autonomous driving technology keep pulling DSP content further into vehicle electronics architecture. Growing integration of artificial intelligence and machine learning directly into DSP silicon continues transforming what these processors can accomplish, enabling on-device voice recognition, natural language processing, and increasingly personalized user experiences without depending on cloud connectivity.

NXP Semiconductors announced a partnership in November 2025 with a leading automotive manufacturer to develop advanced DSP solutions purpose-built for electric vehicles, positioning the company at the forefront of a rapidly growing segment where efficient signal processing is becoming essential to both vehicle performance and safety.

Market Size and Forecast

-

Market Size in 2026E: USD 12.29 Billion

-

Market Size by 2035: USD 24.16 Billion

-

CAGR: 7.80% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

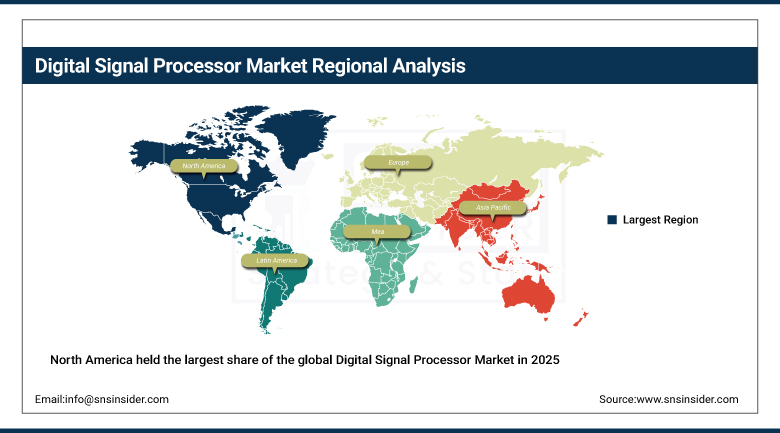

Largest Region: North America

To Get more information On Digital Signal Processor Market - Request Free Sample Report

Digital Signal Processor Market Trends

-

Chip architectures are shifting from stand-alone DSP chips toward highly integrated system-on-chip solutions.

-

Rising automotive adoption of advanced driver-assistance systems continues pulling DSP content deeper into vehicle electronics.

-

Speech processing and recognition applications are seeing accelerated adoption driven by advances in AI and machine learning.

-

Embedded DSP IP core licensing is gaining traction among fabless chip designers seeking pre-validated signal processing macros.

-

General-purpose processors with expanding multi-core and SIMD capability are increasingly encroaching on traditional DSP application territory.

U.S. Digital Signal Processor Market Size Outlook

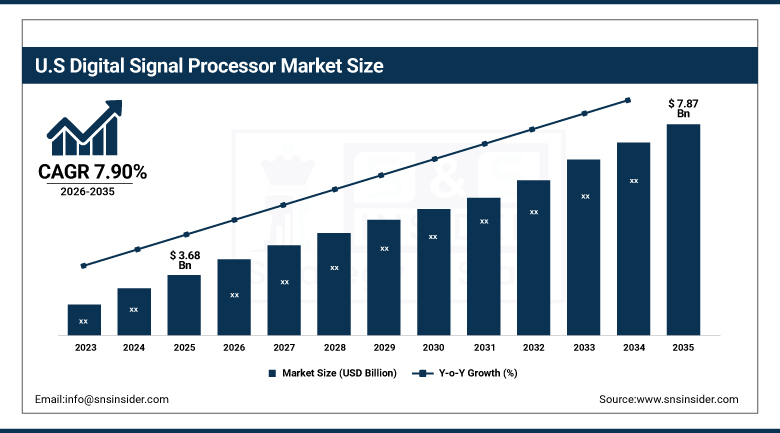

The U.S. Digital Signal Processor Market was valued at USD 3.68 Billion in 2025 and is expected to reach USD 7.87 Billion by 2035, growing at a CAGR of 7.90% from 2026 to 2035.

The United States had continued to maintain its leadership in North American Digital Signal Processor Market through sustained corporate investments in incorporating AI and machine learning into products as well as concentration of top chip designers based within the country. Increased focus on energy efficiency in design along with increasing uptake of advanced signal processors by industries and automobiles made the country one of the most commercially important national markets for the technology all through the year.

In October 2025, Infineon Technologies launched its range of energy-efficient digital signal processors targeting the industrial automation segment in line with increasing importance of sustainable manufacturing which helped improve its position in the industrial automation market in the country.

Digital Signal Processor Market Segment Analysis

-

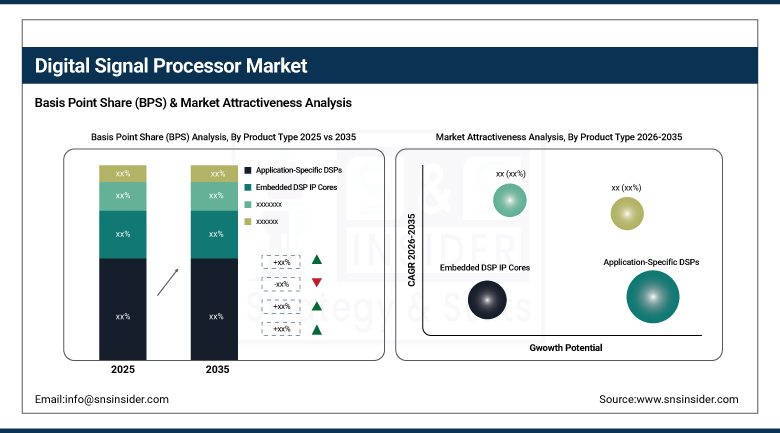

By Product Type, the Application-Specific DSPs segment held approximately 47.60% share in 2025, while the Embedded DSP IP Cores segment is the fastest growing, with a CAGR of approximately 4.02%.

-

By Architecture, the Single Instruction Multiple Data segment held approximately 51.85% share in 2025, while the Very Long Instruction Word segment is the fastest growing, with a CAGR of approximately 4.21%.

-

By Numeric Format, the Fixed-Point segment held approximately 54.90% share in 2025, while the Floating-Point segment is the fastest growing, with a CAGR of approximately 4.62%.

-

By End-User Industry, the Communications segment held approximately 39.65% share in 2025, while the Automotive segment is the fastest growing, with a CAGR of approximately 5.29%.

By Product Type, Application-Specific DSPs led the market, Embedded DSP IP Cores grew fastest

The Application-Specific DSPs segment dominated the product type category in 2025, holding approximately 47.60% of total revenue, as chip designers increasingly favor purpose-built signal processing silicon optimized for specific workloads over general-purpose alternatives. That optimization advantage continues delivering meaningfully better power efficiency and performance for well-defined applications, keeping this product category firmly at the top of the broader product type segmentation across consumer electronics, automotive, and communications equipment.

The Embedded DSP IP Cores segment is projected to grow at the fastest CAGR of approximately 4.02% during the forecast period, reflecting rising fabless semiconductor demand to license pre-validated signal processing macros rather than developing proprietary designs from scratch. As more chip designers outsource fabrication entirely to third-party foundries, demand for hardened, licensable DSP cores continues climbing, pushing this product category's growth rate ahead of the broader product type segmentation.

By Architecture, Single Instruction Multiple Data led the market, Very Long Instruction Word grew fastest

The Single Instruction Multiple Data segment held the largest architecture share in 2025, at approximately 51.85%, favored for its ability to execute the same operation across multiple data points simultaneously, a capability particularly well suited to the repetitive mathematical operations that audio, video, and telecommunications signal processing require. That parallel processing efficiency keeps SIMD designs the dominant architecture choice across the overwhelming majority of commercial DSP implementations.

The Very Long Instruction Word segment is projected to grow at the fastest CAGR of approximately 4.21% during the forecast period, gaining ground in applications requiring explicit parallel instruction scheduling determined at compile time rather than runtime, an approach that can deliver superior performance predictability for safety-critical automotive and industrial applications. Rising demand for deterministic, real-time signal processing performance continues pushing VLIW architecture adoption ahead of the broader architecture segmentation.

By Numeric Format, Fixed-Point led the market, Floating-Point grew fastest

The Fixed-Point segment held the largest numeric format share in 2025, at approximately 54.90%, favored for its lower power consumption and simpler hardware implementation relative to floating-point alternatives, characteristics that matter considerably in battery-powered consumer electronics and embedded automotive applications. That power efficiency advantage keeps fixed-point processors the default numeric format choice across the majority of cost- and power-sensitive DSP applications.

The Floating-Point segment is projected to grow at the fastest CAGR of approximately 4.62% during the forecast period, driven by rising demand for the wider dynamic range and computational precision that increasingly sophisticated AI-enabled signal processing algorithms require. As edge AI workloads grow more complex, floating-point precision is becoming progressively more valuable for maintaining algorithm accuracy, pushing this numeric format's growth rate ahead of the broader numeric format segmentation.

By End-User Industry, Communications led the market, Automotive grew fastest

The Communications segment held the largest end-user industry share in 2025, at approximately 39.65%, anchored by sustained global demand for wireless infrastructure, mobile devices, and telecommunications equipment that all depend fundamentally on efficient signal processing capability. That broad-based, sustained demand keeps communications firmly at the center of overall DSP consumption across nearly every major semiconductor market worldwide.

The Automotive segment is projected to grow at the fastest CAGR of approximately 5.29% during the forecast period, driven by rising DSP adoption across advanced driver-assistance systems, infotainment platforms, and autonomous driving technology that all require increasingly sophisticated real-time signal processing. Continued electric vehicle production growth and expanding vehicle electronics content per car continue pushing automotive end-user demand ahead of the broader end-user industry segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Asia Pacific |

China |

38.60% |

|

North America |

United States |

86.20% |

|

Europe |

Germany |

27.80% |

|

Middle East & Africa |

UAE |

26.30% |

|

Latin America |

Brazil |

37.60% |

North America Digital Signal Processor Market Insights

North America held the largest share of the global Digital Signal Processor Market in 2025, supported by the region's concentration of leading chip designers, sustained enterprise AI integration investment, and strong automotive and communications equipment manufacturing base. Continued domestic semiconductor research investment kept the region at the center of DSP architecture innovation throughout the year.

The United States accounted for roughly 86.20% of regional revenue, reflecting its dense concentration of leading semiconductor companies and downstream automotive, communications, and consumer electronics customers. Canada contributed a smaller but steadily growing share of regional revenue, supported by its own expanding semiconductor design ecosystem, keeping North America firmly ahead of every other region in this market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Digital Signal Processor Market Insights

Asia Pacific was the fastest-growing region in the global Digital Signal Processor Market, driven by the region's massive consumer electronics manufacturing base and rapidly expanding telecommunications sector across China, Japan, and South Korea. Growing 5G network deployment and rising domestic semiconductor manufacturing investment continued driving regional demand at a pace considerably faster than more mature Western markets.

China accounted for roughly 38.60% of regional revenue, supported by its role as a global consumer electronics manufacturing hub and expanding domestic semiconductor design capability. Japan and South Korea contributed significant additional regional demand through their own advanced electronics and telecommunications industries, reinforcing Asia Pacific's position as the clear growth leader in DSP adoption through the forecast period.

Europe Digital Signal Processor Market Insights

Europe occupied a significant market share in the Global Digital Signal Processor Market in 2025 due to the presence of robust automotive electronics industry and rising adoption of industrial automation in Europe. Around 27.80% share in regional revenue was witnessed in Germany owing to its presence of automotive industry which is using DSP technology in their automobile electronics.

The trends observed in France, United Kingdom, and Italy were also same as they were seeing rising adoption of DSP technology due to rise in electric vehicles and industrial automation. The continuous development of automobile electronics will continue to drive the demand in the region.

MEA & Latin America Digital Signal Processor Market Insights

The Middle East and Africa region recorded steady growth in DSP adoption in 2025, driven by expanding telecommunications infrastructure investment and growing industrial automation across the Gulf states in particular, supported by 5G network expansion. The UAE accounted for roughly 26.30% of regional revenue, supported by national digitization strategies and rising enterprise demand for advanced telecommunications equipment.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.60% of regional revenue, where growing telecommunications and automotive electronics manufacturing continued to support category growth. Mexico and Argentina followed a similar trajectory as regional electronics manufacturing capacity expanded further through the remainder of the forecast period.

Market Dynamics

Growth Drivers: AI integration and automotive electronics expansion

The integration of artificial intelligence and machine learning into DSP silicon continues to be the central force behind market growth, transforming these processors' capabilities across virtually every application category. As consumer devices become more intelligent and connected, DSPs increasingly play a pivotal role in enabling seamless voice recognition, natural language processing, and personalized user experiences directly at the device level rather than depending on cloud processing.

The rapid adoption of DSPs in automotive systems, including advanced driver-assistance systems, infotainment platforms, and autonomous driving technology, continues reinforcing this growth trajectory further. Rising demand for advanced consumer electronics requiring high-speed signal processing capability, combined with expanding 5G infrastructure and massive multiple-input multiple-output implementations, keeps structural demand growth firmly intact across nearly every major DSP application category worldwide.

Restraints: Design complexity and competition from general-purpose processors

Developing and programming DSPs requires specialized expertise in signal processing and real-time systems that continues increasing development time and cost relative to more generalized processing solutions. Balancing performance, power consumption, and cost simultaneously continues complicating the design process for chip developers working within increasingly tight competitive margins.

General-purpose processors, with continued advancements in multi-core and SIMD capability, continue encroaching on traditional DSP application territory, while graphics processing units and field-programmable gate arrays also offer viable co-processing alternatives for certain signal processing workloads. That competitive pressure from adjacent processor categories continues requiring DSP manufacturers to demonstrate clear performance or efficiency advantages to maintain design wins across contested application categories.

Opportunities: Edge AI acceleration and licensable IP core expansion

Growing demand for tightly coupled signal processing and AI inference silicon presents substantial opportunity for chip designers positioned to deliver integrated system-on-chip solutions that fuse DSP, CPU, and neural engine capability within a single package. As edge computing applications continue proliferating across industrial and automotive settings, manufacturers capable of delivering this convergent silicon architecture stand to capture a growing share of demand.

Rising fabless semiconductor demand for licensable, pre-validated DSP IP cores presents a further significant growth avenue, as companies increasingly outsource manufacturing while still requiring proven signal processing designs for their chips. Technology suppliers capable of delivering both direct DSP products and licensable IP cores stand to capture meaningful new revenue streams as speech processing, automotive, and industrial edge computing applications continue expanding through 2035.

Recent Developments:

-

2025: Texas Instruments continued expanding its programmable DSP hardware and embedded signal processing core portfolio, reinforcing its long-standing position as a leading supplier across industrial, automotive, and communications signal processing applications.

-

2025: Analog Devices continued advancing its mixed-signal and digital signal processing product roadmap, targeting increasingly sophisticated automotive radar and industrial sensor fusion applications requiring high-precision real-time processing.

-

2024: Qualcomm Technologies continued integrating advanced DSP capability within its mobile platform system-on-chip designs, supporting on-device AI processing for next-generation smartphone camera and audio applications.

Digital Signal Processor Companies are:

-

Analog Devices, Inc.

-

Qualcomm Technologies, Inc.

-

Intel Corporation

-

Broadcom Inc.

-

STMicroelectronics N.V.

-

NXP Semiconductors N.V.

-

Renesas Electronics Corporation

-

MediaTek Inc.

-

Cirrus Logic, Inc.

-

Cadence Design Systems, Inc.

-

CEVA, Inc.

-

Synopsys, Inc.

-

Microchip Technology Incorporated

-

ON Semiconductor Corporation

-

Marvell Technology, Inc.

-

Advanced Micro Devices, Inc.

-

Skyworks Solutions, Inc.

-

Knowles Corporation

Digital Signal Processor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.40 Billion |

| Market Size by 2035 | USD 24.16 Billion |

| CAGR | CAGR of 7.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product Type (Application-Specific DSPs, Embedded DSP IP Cores, General-Purpose DSPs) • by Architecture (Single Instruction Multiple Data, Very Long Instruction Word) • by Numeric Format (Fixed-Point, Floating-Point) • by End-User Industry (Communications, Automotive, Consumer Electronics, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Texas Instruments Incorporated, Analog Devices, Inc., Qualcomm Technologies, Inc., Intel Corporation, Broadcom Inc., STMicroelectronics N.V., Infineon Technologies AG, NXP Semiconductors N.V., Renesas Electronics Corporation, MediaTek Inc., Cirrus Logic, Inc., Cadence Design Systems, Inc., CEVA, Inc., Synopsys, Inc., Microchip Technology Incorporated, ON Semiconductor Corporation, Marvell Technology, Inc., Advanced Micro Devices, Inc., Skyworks Solutions, Inc., Knowles Corporation |

Frequently Asked Questions

The Digital Signal Processors Market was valued at USD 11.40 Billion in 2025.

The Digital Signal Processors Market is expected to grow at a CAGR of 7.80% from 2026 to 2035.

The Application-Specific DSPs segment held approximately 47.60% share in 2025.

North America held the largest share of the Digital Signal Processors Market in 2025, while Asia Pacific was the fastest-growing region.

Get in Touch