Motion Control Market Report Scope & Overview:

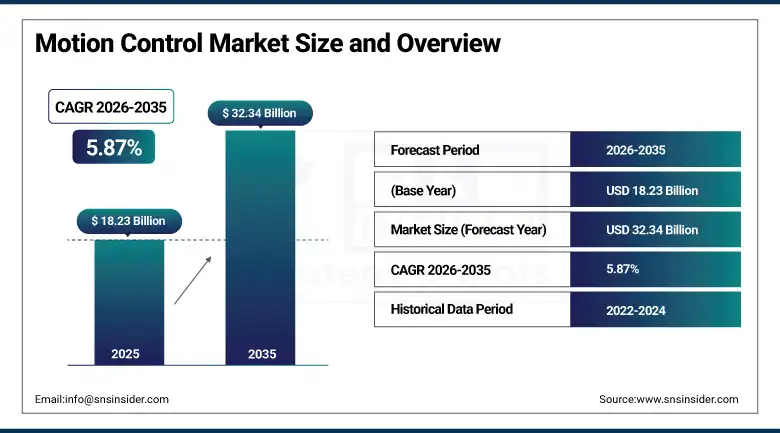

The Motion Control Market was valued at USD 18.23 Billion in 2025 and is expected to reach USD 32.34 Billion by 2035, growing at a CAGR of 5.87% from 2026–2035.

Motion control encompasses a set of systems and technologies employed to manage the movement, velocity, torque, and positioning of machines and equipment in various industries and applications. Such systems have an essential part in automation as they provide highly accurate, repeatable, and efficient movements that are important in manufacturing, semiconductor, medical, robotics, and packaging processes. An example of a motion control system includes such components as servo motors, drives, controllers, feedback mechanisms, and software capable of executing motions with precision. The trend toward adoption of Industry 4.0 technologies is driving the use of motion control systems to boost productivity and manufacturing quality.

In January 2024, Goodyear Tire & Rubber Company and ZF achieved seamless integration of tire intelligence technologies with vehicle motion control software, combining Goodyear's IntelliTire sensor platform with ZF's integrated vehicle dynamics motion control system to create a tyre-to-chassis data loop that enables predictive dynamic adjustment of suspension damping, brake distribution, and steering response based on real-time tyre contact patch load and temperature data.

Market Size and Forecast

-

Market Size in 2026E: USD 19.30 Billion

-

Market Size by 2035: USD 32.34 Billion

-

CAGR: 5.87% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Motion Control Market - Request Free Sample Report

Motion Control Market Trends

-

AI-powered adaptive motion control is improving machine performance by continuously optimizing motion parameters based on operating conditions, equipment wear, and workload variations

-

Collaborative robots integrated with advanced motion control systems are enabling safe and precise human-machine interaction for assembly, handling, and inspection applications

-

Adoption of EtherCAT and Time-Sensitive Networking (TSN) technologies is enhancing multi-axis motion synchronization through ultra-fast and deterministic industrial communication networks

-

Replacement of hydraulic systems with servo-electric motion control solutions is increasing as manufacturers seek higher energy efficiency, improved precision, and lower maintenance costs

-

Rising semiconductor manufacturing complexity is driving demand for ultra-precise motion control systems capable of achieving nanometer-level positioning accuracy in advanced fabrication equipment

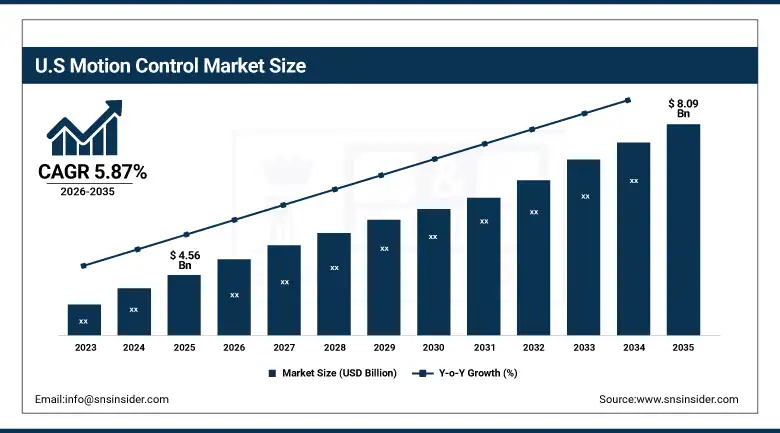

U.S. Motion Control Market Outlook

The U.S. Motion Control Market was valued at approximately USD 4.56 Billion in 2025 and is expected to reach approximately USD 8.09 Billion by 2035, growing at a CAGR of approximately 5.87%.

The U.S. motion control market is getting boosted by the presence of significant investment in domestic manufacturing, especially semiconductor manufacturing, wherein the latest manufacturing plants use sophisticated motion control products for wafer handling, testing, and automated handling of machinery in production processes. The government initiatives towards the modernization of defense are also helping to fuel demand for motion control systems for autonomous systems, robotics, and high-end machinery. The trend towards bringing back the manufacturing process of automobiles, electronics, and medical devices from offshore countries to onshore operations has led to investments in factory automation and intelligent manufacturing units.

In 2025, Siemens launched its SIMOTION D435-2 distributed servo drive platform incorporating edge AI capability for real-time motion profile adaptation based on process feedback, enabling CNC machine tool operators to achieve adaptive cutting parameter adjustment that improves surface finish and tool life without interrupting production cycles for manual parameter recalibration.

Motion Control Market Segment Analysis

-

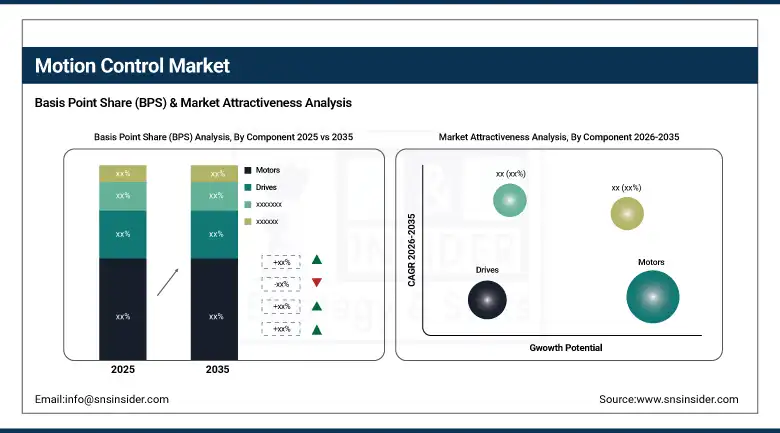

By Component, the Motors segment dominated the Motion Control Market with approximately 32% share in 2025, while the Drives segment is the fastest growing.

-

By System Type, the Closed-Loop segment dominated the Motion Control Market with approximately 52% share in 2025, while the Open-Loop segment is growing at a higher CAGR of approximately 8.65%.

-

By End User, the Manufacturing & Industrial Automation segment dominated the Motion Control Market with the largest share in 2025, while the Semiconductor & Electronics segment is the fastest growing end user.

By Component, motors dominate, drives grow fastest

Motors retained the dominant component position with approximately 32% of the motion control market in 2025. Their commercial primacy reflects the universal requirement for electromagnetic torque generation across every motion control application from miniature servo motors in medical robotic surgical tools through large frameless torque motors in semiconductor wafer handling robots to high-speed spindle motors in CNC machine tools whose combined deployment across millions of motion axes in global manufacturing creates an enormous aggregate motor market that sustains the segment's revenue leadership.

Drives are growing fastest as servo drives' evolution from power electronics converting electrical input to motor current toward intelligent edge computing platforms providing real-time process monitoring, predictive maintenance analytics, and adaptive motion control creates expanding functionality whose per-drive value increases drive average selling prices while delivering operational value that sustains premium pricing.

By End User, manufacturing & industrial automation dominates, semiconductor & electronics grows fastest

Manufacturing and industrial automation retained the dominant end user position, reflecting the breadth of motion control application across machining, forming, welding, assembly, material handling, and inspection processes whose collective automation investment across global manufacturing creates the most commercially significant single end-user category in the motion control market. The continued expansion of factory automation investment under Industry 4.0 programmes, reshoring incentives in North America and Europe, and the automation imperative that rising manufacturing labour costs create in Asia Pacific collectively sustain manufacturing and industrial automation as the foundational demand base whose stability provides commercial predictability that higher-growth but more volatile end user segments cannot match.

Semiconductor and electronics is the fastest-growing end user as each successive semiconductor node advancement requires lithography, deposition, etch, and inspection equipment whose motion control precision requirements exceed the prior node's specification by meaningful margins, creating a technology-driven performance upgrade cycle that sustains above-market motion control investment at leading-edge semiconductor manufacturers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

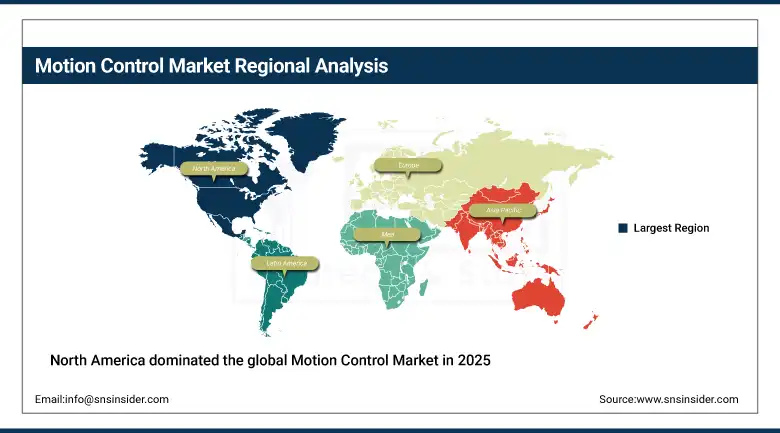

North America Motion Control Market Insights

North America dominated the global Motion Control Market in 2025, accounting for the largest regional revenue share. The United States accounts for approximately 82.5% of North American revenues through its world-leading semiconductor fabrication equipment, aerospace manufacturing, medical device, and defence automation sectors whose motion control requirements define the global performance frontier and sustain premium segment pricing. Rockwell Automation, Parker Hannifin, and the U.S. operations of global motion control leaders create a concentrated commercial ecosystem whose innovation output and customer relationships sustain North American market leadership.

Canada contributes supplementary demand through its aerospace manufacturing, oil and gas process automation, and growing robotics integration across its manufacturing sectors whose motion control requirements span conventional servo automation through specialised motion applications in harsh environmental conditions. The Canadian government's advanced manufacturing investment programmes are progressively creating new motion control procurement in automotive electrification, cleantech manufacturing, and agri-food processing automation contexts.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Motion Control Market Insights

Europe held a significant share of the global Motion Control Market in 2025. Germany, Italy, Switzerland, Sweden, and the United Kingdom are the leading national markets whose machine tool, packaging machinery, semiconductor equipment, and precision manufacturing sectors create consistent and technically demanding motion control demand. Germany accounts for approximately 28.5% of European revenues through the commercial concentration of Siemens, Bosch Rexroth, and SEW-Eurodrive whose motion control product portfolios define European industrial automation standards, and the world-leading German machine tool industry whose precision machining equipment represents the most technically demanding application category in the commercial motion control market.

Italy's packaging machinery sector, Switzerland's watch manufacturing and pharmaceutical automation industries, and Sweden's robotics and automated warehouse equipment sectors each contribute premium motion control demand whose technical specifications and per-system value substantially exceed standard industrial automation applications. European manufacturing reshoring investment in response to supply chain resilience priorities is creating new automated facility construction whose motion control content is growing with each new generation of flexible manufacturing system.

Asia Pacific Motion Control Market Insights

Asia Pacific is the fastest-growing regional motion control market, driven by the world's largest electronics and semiconductor manufacturing base, rapid industrial automation adoption as manufacturing labour costs rise across the region, and the extraordinary scale of Chinese industrial investment whose automated factory construction creates the world's largest single national motion control demand. China accounts for approximately 38.5% of Asia Pacific revenues through its enormous manufacturing sector's automation investment, the domestic semiconductor equipment programme whose motion control requirements are creating new domestic supplier development, and the growing robotics adoption across automotive and electronics manufacturing.

Japan, South Korea, and Taiwan contribute high-value regional demand through their world-leading semiconductor equipment, flat panel display manufacturing, and precision industrial automation sectors whose motion control requirements encompass the most performance-demanding applications in the global market. India is the most commercially dynamic emerging motion control market within Asia Pacific where manufacturing sector automation investment, pharmaceutical production automation, and the growing electronics manufacturing sector's precision equipment requirements are creating above-regional-average growth momentum.

MEA & Latin America Motion Control Market Insights

The UAE leads MEA revenues at approximately 22.8% of the regional total through its advanced manufacturing investment, oil and gas process automation, and the growing semiconductor and electronics manufacturing initiatives under its industrial diversification strategy. Saudi Arabia's manufacturing sector development under Vision 2030 and its chemical processing automation create growing motion control demand from both industrial automation and process control applications.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its automotive manufacturing, food and beverage processing, and agricultural equipment production sectors whose automation investment creates consistent motion control demand. Mexico contributes significant secondary market demand through its large automotive and electronics manufacturing export sectors whose near-shoring investment from North American manufacturers is creating new automated facility construction with sophisticated motion control requirements.

Market Dynamics

Growth Drivers: Industrial automation acceleration driven by manufacturing labour cost increases and Industry 4.0 digital factory investment creating sustained motion control demand growth

The motion control market is experiencing strong growth as manufacturers worldwide increasingly adopt automation to improve productivity, reduce labor dependency, and enhance product quality. Rising labor costs, growing demand for operational efficiency, and expanding Industry 4.0 initiatives are encouraging industries to deploy advanced motion control systems that enable precise, reliable, and data-driven manufacturing processes. Emerging economies are also accelerating automation investments, creating new opportunities for motion control solution providers.

At the same time, continuous advancements in semiconductor manufacturing, electronics production, robotics, and high-precision industrial equipment are driving demand for increasingly sophisticated motion control technologies. The need for higher accuracy, faster response times, and improved synchronization in automated systems is supporting ongoing investments in servo motors, drives, controllers, and intelligent motion platforms across a wide range of industries.

Restraints: High system complexity and the shortage of qualified motion control engineers constraining automated system deployment velocity in emerging markets

The installation of motion control technology requires extensive knowledge in specialized fields like servo motor sizing, motion control programming, sensor calibration, and system validation, thereby complicating the process for most manufacturers. There is currently a lack of experts who can integrate motion control technology into automated processes, resulting in increased difficulties due to the rapid implementation of automation in various industries. The long training time necessary to create qualified engineers is an additional factor that makes the acquisition of qualified professionals difficult. Besides, the cost of owning motion control technology is not just the price of buying hardware but also the expense of employing engineers and integrating systems.

Opportunities: Collaborative robot integration and electrification of hydraulic motion systems represent high-value conversion markets for precision motion control

The increasing deployment of collaborative robots offers what is one of the biggest growth prospects in the motion control market segment. The increased application of collaborative robots in manufacturing and assembly operations has led to an increase in the demand for servo motors, drives, encoders, and motion controllers. Increased performance and improved capabilities of payload handling, accuracy, and safety of collaborative robots have led to an increase in demand due to higher volumes and better value offered by motion control components.

On the other hand, there is a shift from hydraulic motion control technologies to servo-electric motion controls in various industries. Hydraulic systems are being replaced by servo electric motion control systems to increase energy efficiency, improve accuracy, decrease maintenance, and reduce operating costs.

Recent Developments:

-

2025: Siemens launched its SIMOTION D435-2 distributed servo drive platform incorporating edge AI capability for real-time motion profile adaptation based on process feedback, enabling CNC machine tool operators to achieve adaptive cutting parameter adjustment and improved surface finish without interrupting production cycles.

-

2024: Goodyear and ZF achieved integration of IntelliTire tyre intelligence with ZF's vehicle dynamics motion control system, creating a tyre-to-chassis data loop enabling predictive dynamic adjustment of suspension, braking, and steering response based on real-time tyre contact data.

-

2023: Rockwell Automation launched its iTRAK 5730 independent cart system intelligent track technology incorporating wireless power and communication for cart-based flexible manufacturing motion control, enabling pharmaceutical, food, and consumer goods manufacturers to achieve flexible production line reconfiguration without physical track modification.

Motion Control Market Key Players

-

Siemens AG

-

Rockwell Automation Inc.

-

ABB Ltd.

-

Yaskawa Electric Corporation

-

Parker Hannifin Corporation

-

Mitsubishi Electric Corporation

-

Bosch Rexroth AG

-

Fanuc Corporation

-

Beckhoff Automation GmbH

-

Kollmorgen Corporation (Altra Industrial Motion)

-

Moog Inc.

-

Rexnord Corporation

-

Nidec Corporation

-

Schneider Electric SE

-

Honeywell International Inc.

-

Emerson Electric Co.

-

Delta Electronics Inc.

-

Lenze SE

-

SEW-Eurodrive GmbH & Co. KG

-

Pilz GmbH & Co. KG

Motion Control Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.23 Billion |

| Market Size by 2035 | USD 32.34 Billion |

| CAGR | CAGR of 5.87% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Motors, Drives, Motion Controllers, Actuators, Sensors, Software, Others) • by System Type (Open-Loop, Closed-Loop) • by Motion Type (Linear, Rotary, Oscillatory) • by End User (Manufacturing & Industrial Automation, Semiconductor & Electronics, Automotive, Healthcare & Medical, Packaging & Food Processing, Aerospace & Defense, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Siemens AG, Rockwell Automation Inc., ABB Ltd., Yaskawa Electric Corporation, Parker Hannifin Corporation, Mitsubishi Electric Corporation, Bosch Rexroth AG, Fanuc Corporation, Beckhoff Automation GmbH, Kollmorgen Corporation (Altra Industrial Motion), Moog Inc., Rexnord Corporation, Nidec Corporation, Schneider Electric SE, Honeywell International Inc., Emerson Electric Co., Delta Electronics Inc., Lenze SE, SEW-Eurodrive GmbH & Co. KG, Pilz GmbH & Co. KG |

Frequently Asked Questions

The Motion Control Market is expected to grow at a CAGR of 5.87% from 2026 to 2035.

The Motion Control Market was valued at USD 18.23 Billion in 2025.

Electrification of hydraulic equipment and Industry 4.0-driven smart factory investments are further accelerating motion control adoption by improving efficiency, precision, and production automation capabilities

The Motors segment dominated the Motion Control Market with approximately 32% share in 2025, while the Drives segment is the fastest growing component as servo drive intelligence and connectivity expands their commercial value.

North America dominated the Motion Control Market in 2025, with the United States accounting for approximately 82.5% of North American revenues through its semiconductor fabrication equipment, aerospace, medical device, and defence automation sectors.

Get in Touch