Synthetic Rubber Market Report Scope & Overview:

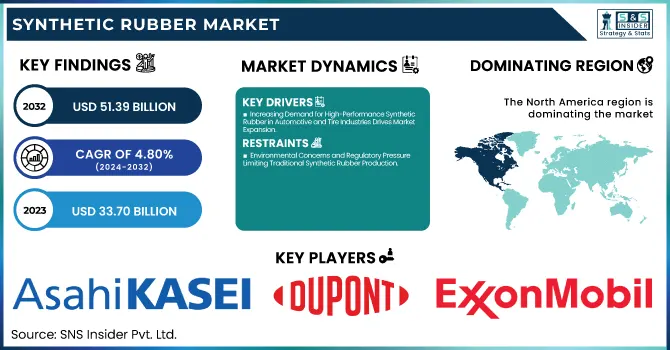

The Synthetic Rubber Market Size was valued at USD 33.70 Billion in 2023 and is expected to reach USD 51.39 Billion by 2032, growing at a CAGR of 4.80% over the forecast period of 2024-2032.

To Get more information on Synthetic Rubber Market - Request Free Sample Report

The synthetic rubber market is undergoing significant changes, driven by various key factors. Pricing trends are influenced by fluctuations in raw material costs, global supply-demand dynamics, and geopolitical uncertainties. Sustainability is becoming a central focus, with the industry adopting greener practices, such as bio-based feedstocks and improved recycling initiatives. As demand for synthetic rubber grows across sectors like automotive and footwear, understanding the evolving end-user needs is essential. Simultaneously, the carbon footprint and environmental impact of production processes are under increasing scrutiny. Our report delves into these critical aspects, providing insights into how pricing, sustainability efforts, end-user demand, and environmental considerations are shaping the synthetic rubber market's current and future landscape.

The US Synthetic Rubber Market Size was valued at USD 9.59 Billion in 2023 and is expected to reach USD 13.56 Billion by 2032, growing at a CAGR of 3.93% over the forecast period of 2024-2032.

The United States synthetic rubber market is experiencing growth driven by several key factors. Major tire manufacturers, such as Bridgestone Americas Tire Operations and Goodyear Tire & Rubber Company, have implemented price increases to offset rising raw material costs, including synthetic rubber, carbon black, and butadiene. These adjustments reflect the dynamic nature of raw material prices and their impact on production costs. Additionally, the U.S. automotive industry's recovery has bolstered demand for synthetic rubber, particularly in tire manufacturing. However, challenges like production overcapacity and price volatility persist, requiring strategic adjustments from industry players. Overall, the U.S. synthetic rubber market continues to evolve, influenced by economic conditions, supply chain dynamics, and strategic decisions by leading manufacturers.

Synthetic Rubber Market Dynamics

Drivers

-

Increasing Demand for High-Performance Synthetic Rubber in Automotive and Tire Industries Drives Market Expansion

The growing need for durable, high-performance synthetic rubber is primarily driven by the automotive industry, where it plays a crucial role in tire manufacturing. As vehicle production increases, particularly in markets like North America and Asia Pacific, demand for synthetic rubber has surged. Tire manufacturers are increasingly adopting synthetic rubber to meet the rising demand for high-quality tires with improved safety, fuel efficiency, and durability. Synthetic rubber types such as styrene-butadiene rubber, polybutadiene rubber, and ethylene-propylene-diene rubber are preferred for their superior performance characteristics, such as enhanced abrasion resistance and improved wet traction. Additionally, automotive manufacturers are moving towards electric vehicles, which require advanced tire materials that can perform under varied environmental conditions. As a result, this shift towards high-performance rubber is driving growth in synthetic rubber demand, ensuring that the market continues to thrive in the coming years.

Restraints

-

Environmental Concerns and Regulatory Pressure Limiting Traditional Synthetic Rubber Production

Despite the significant demand for synthetic rubber, the industry faces increasing environmental concerns regarding the impact of its production processes. The use of petrochemical-based raw materials and the high energy consumption involved in traditional rubber manufacturing processes contribute to carbon emissions, leading to environmental degradation. Regulatory bodies are imposing stricter environmental standards, forcing companies to adopt greener alternatives or face penalties and reputational damage. Many synthetic rubber manufacturers are under pressure to implement sustainable practices, such as using renewable feedstocks, reducing waste, and minimizing energy consumption. While some companies have made strides toward more eco-friendly production methods, the shift requires significant investment in new technologies and infrastructure. These regulatory challenges present a major restraint for the market, as companies must balance the need for sustainability with the high costs of transitioning to greener practices, slowing overall industry growth.

Opportunities

-

Growing Automotive Industry in Emerging Markets Creates Lucrative Opportunities for Synthetic Rubber Manufacturers

The expanding automotive sector in emerging markets, particularly in Asia Pacific and Latin America, presents significant growth opportunities for the synthetic rubber market. As disposable incomes rise and the middle class expands in these regions, the demand for vehicles, particularly affordable cars, is increasing. Synthetic rubber is a key component in tire production, and the growing automotive market will lead to higher demand for durable and cost-effective tires. Furthermore, with the global shift towards electric vehicles, the need for high-performance rubber products that meet specific safety and performance standards is driving innovation. Manufacturers who are able to cater to the needs of emerging markets by offering affordable, high-quality synthetic rubber products will be well-positioned to capitalize on this growth. Moreover, the rising focus on sustainability in these regions is also pushing the automotive industry to adopt eco-friendly tire solutions, creating new opportunities for manufacturers that specialize in environmentally conscious rubber products.

Challenge

-

Dependency on Petrochemical Industry Makes Synthetic Rubber Vulnerable to External Economic Shocks

The synthetic rubber industry is heavily dependent on the petrochemical sector, which exposes it to the risk of external economic shocks, such as fluctuations in crude oil prices. These price variations have a direct impact on the cost of raw materials for synthetic rubber production, including butadiene and styrene. Economic downturns, geopolitical instability, and changes in oil supply can disrupt the production and pricing of these essential materials, affecting the stability and profitability of the synthetic rubber market. Manufacturers that rely on the petroleum industry for feedstocks are particularly vulnerable to such shocks, which can lead to cost volatility, reduced profit margins, and supply chain disruptions. As a result, the synthetic rubber market faces a challenge in mitigating the risks associated with its reliance on the petrochemical industry.

Synthetic Rubber Market Segmental Analysis

By Type

In 2023, Styrene Butadiene Rubber (SBR) dominated the Synthetic Rubber Market with a market share of 40.2%. SBR is widely favored in the automotive industry due to its excellent performance characteristics, including good abrasion resistance and heat stability, making it ideal for tire manufacturing. For instance, the American Chemical Society highlights that SBR's versatility allows for its use in various applications, including tires and footwear, further cementing its position in the market. Major tire manufacturers like Goodyear Tire and Rubber Company and Bridgestone have adopted SBR extensively in their tire formulations, leveraging its performance benefits to meet stringent safety and efficiency standards. This strong demand from leading tire manufacturers, coupled with its cost-effectiveness, has made SBR the predominant synthetic rubber type in 2023.

By Application

In 2023, the tire segment dominated the Synthetic Rubber Market with a market share of 60.8%. This substantial share is primarily driven by the increasing demand for tires in the automotive industry, particularly as vehicle production ramps up. The Tire Industry Association reports that the rising production of passenger and commercial vehicles significantly contributes to tire demand, which directly impacts the consumption of synthetic rubber. Leading tire manufacturers, such as Michelin and Continental, are focusing on producing high-performance tires that utilize advanced synthetic rubber formulations to enhance safety, fuel efficiency, and durability. Furthermore, as the automotive industry shifts towards electric vehicles, the need for specialized tires that can handle the unique performance requirements of these vehicles further fuels growth in the tire segment, solidifying its dominance in the synthetic rubber market.

Synthetic Rubber Market Regional Outlook

In 2023, North America dominated the Synthetic Rubber Market with a market share of 35.4%. The region’s dominance is largely attributed to the advanced automotive and tire manufacturing sectors, particularly in the United States, where companies like Goodyear Tire and Rubber Company, ExxonMobil, and DuPont are leading synthetic rubber producers. The demand for high-performance tires in North America is robust, driven by a growing number of vehicles on the road and the increasing demand for electric vehicles (EVs) that require specialized tire formulations. According to the U.S. Tire Manufacturers Association, the tire market continues to expand, creating a strong demand for synthetic rubber. Moreover, the presence of major chemical companies and robust infrastructure in North America allows for efficient production and distribution. The United States, in particular, holds the largest share due to its established manufacturing base and strong automotive industry. Canada and Mexico, while smaller markets, are also growing due to rising industrial activities and growing automotive production, contributing to the region's dominance in synthetic rubber consumption.

Moreover, The Asia Pacific region emerged as the fastest-growing region in the Synthetic Rubber Market in the forecast period with a significant CAGR. The region’s rapid industrialization, expanding automotive industry, and growing demand for high-performance tires drive this growth. Leading countries like China, Japan, and India are major contributors to this expansion. China, as the largest manufacturer and consumer of synthetic rubber, is supported by strong domestic demand for tires and automotive components, with companies like Sinopec and Lanxess being key players in the region. According to the China Rubber Industry Association, the demand for synthetic rubber is set to rise as the country shifts towards electric and hybrid vehicles, which require specialized rubber materials. Japan’s automotive giants, such as Toyota and Honda, continue to innovate with tire and component technologies, contributing to the increase in synthetic rubber demand. India, with its rapidly growing automotive sector and improving infrastructure, is another key growth driver. This collective growth in Asia Pacific makes the region a critical market for synthetic rubber in the coming years.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Apcotex Industries Limited (Nitrile Rubber, Styrene Butadiene Rubber)

-

Asahi Kasei Corporation (Butadiene Rubber, Styrene-Butadiene Rubber)

-

China National Petroleum Corporation (CNPC) (Buna-S Rubber, Ethylene Propylene Diene Monomer Rubber)

-

China Petroleum & Chemical Corporation (Sinopec Corporation) (Buna-N Rubber, Styrene Butadiene Rubber)

-

Denka Company Ltd. (Nitrile Rubber, Styrene Butadiene Rubber)

-

DuPont (Hytrel, Crude Butadiene)

-

Dynasol Elastomers S.A. (SBR, SBC)

-

ExxonMobil (Butyl Rubber, EPDM)

-

Goodyear Tire and Rubber Company (SBR, Natural Rubber)

-

Indian Synthetic Rubber Private Limited (Butadiene Rubber, Styrene Butadiene Rubber)

-

JSR Corporation (SBR, Polybutadiene Rubber)

-

Kumho Petrochemical Company Ltd (Buna-N Rubber, EPDM)

-

LANXESS AG (Buna-S Rubber, Butyl Rubber)

-

Mitsui Chemical Inc. (EPDM, Hydrogenated Nitrile Rubber)

-

Nizhnekamskneftekhim (Butyl Rubber, Styrene-Butadiene Rubber)

-

Reliance Industries Limited (Ethylene Propylene Diene Monomer Rubber, Nitrile Rubber)

-

Sinopec (Buna-N Rubber, Styrene Butadiene Rubber)

-

Sumitomo Chemical Co., Ltd. (Butadiene Rubber, Polybutadiene Rubber)

-

TSRC Corporation (Styrene Butadiene Rubber, Butyl Rubber)

-

Versalis S.p.A. (SBR, EPDM)

Recent Developments

-

May 2024: Deesawala Rubber Industries launched its fourth manufacturing unit in Hyderabad with an investment of Rs 40 crore. The unit, set to triple production capacity, will also diversify into sectors like adhesives and rubber profiles for automobiles. The company plans to increase its workforce and expand exports to Europe and the Middle East.

-

December 2024: Eneos Corp. acquired full ownership of Eneos MOL Synthetic Rubber Ltd., a joint venture with MOL Group. This acquisition strengthens Eneos's position in the European market, focusing on solution polymerized styrene-butadiene rubber for high-performance tires.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 33.70 Billion |

| Market Size by 2032 | USD 51.39 Billion |

| CAGR | CAGR of 4.80% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Styrene butadiene rubber (SBR), Polybutadiene Rubber (BR), Styrene block copolymer (SBC), Ethylene-propylene-diene rubber (EPDM), Butyl rubber (IIR), Others) •By Application (Tire, Automotive (Non-tire), Footwear, Industrial Goods, Consumer Goods, Textiles, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Sinopec, DuPont, The Dow Chemical Company, ExxonMobil, Kumho Petrochemical Company Ltd, Zeon Corporation, Nizhnekamskneftekhim, The Goodyear Tire and Rubber Company, JSR Corporation, LANXESS AG and other key players |

Frequently Asked Questions

The United States holds the largest share of the Synthetic Rubber Market in North America.

Styrene Butadiene Rubber dominated the Synthetic Rubber Market with a share of 40.2% in 2023.

The demand for synthetic rubber in the automotive sector is driven by the need for high-performance tires and durable components.

Pricing trends in the Synthetic Rubber Market are influenced by raw material costs, supply-demand dynamics, and geopolitical uncertainties.

The Synthetic Rubber Market was valued at USD 33.70 billion in 2023.

Get in Touch