Table-Top Games Market Report Scope & Overview:

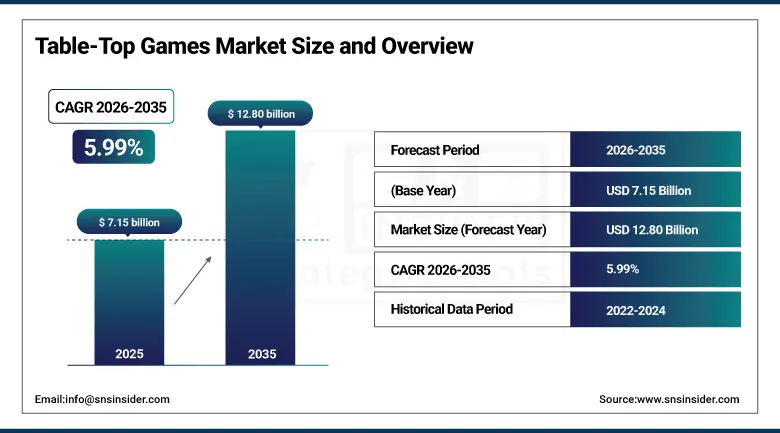

The Table-Top Games Market was valued at USD 7.15 billion in 2025 and is expected to reach USD 12.80 billion by 2035, growing at a CAGR of 5.99% from 2026–2035.

The market's sustained growth reflects the category's fundamental value proposition as a shared physical social activity providing meaningful interpersonal connection, cooperative decision-making challenge, and tactile engagement with physical objects that digital entertainment cannot replicate, addressing documented social isolation and screen fatigue that extensive digital media consumption generates. The crowdfunding explosion through Kickstarter and Gamefound has democratised game design and publishing by removing traditional publisher gatekeeping, creating millions of pre-committed purchasers whose advance financial support enables production quality levels and design ambitions that conventional retail economics could not sustain. Kickstarter table-top game campaign funding exceeded USD 1.9 billion in 2024, demonstrating the extraordinary consumer willingness to pre-fund innovative game design that characterises the most commercially motivated segment of the hobby community.

The convergence of pandemic-era family game time reconnection with the broader social gaming renaissance has created a multi-generational table-top game consumer base whose depth and commercial engagement is unprecedented in the category's modern history, with the structural nature of this demand shift confirmed by sustained above-pre-pandemic purchasing and playing frequency through 2025.

Market Size and Forecast

-

Market Size in 2026E: USD 7.58 Billion

-

Market Size by 2035: USD 12.80 Billion

-

CAGR: 5.99% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Table-Top Games Market - Request Free Sample Report

Table-Top Games Market Trends

-

Rapid growth of crowdfunding as the dominant channel for premium game development, where Kickstarter and Gamefound campaigns provide development financing while creating engaged pre-launch communities that sustain commercial momentum, validate demand before production commitment, and enable product configurations that traditional publishing economics would not support.

-

Growing integration of digital companion applications with physical game experiences, where smartphone apps provide ambient narrative audio, automated complex rule adjudication, enemy AI for solo modes, and integrated campaign tracking that enhance physical game experiences without replacing the tactile and social dimensions motivating table-top preference.

-

Increasing market penetration of educational table-top games designed for classroom, homeschool, and family learning contexts developing mathematics, literacy, critical thinking, and social-emotional competencies through game mechanics, supported by growing teacher awareness and curriculum-aligned game design investment.

-

Expanding licensed intellectual property game production from major entertainment franchises including Marvel, Star Wars, Disney, and streaming content, where recognition value lowers the barrier to purchase for casual buyers who might not engage with unfamiliar titles despite equivalent design quality.

-

Rising demand for premium production components including metal coins, acrylic tokens, sculpted miniatures, and custom moulded pieces that have become standard expectation in the crowdfunded premium segment, driving quality differentiation between mass-market releases and artisan-quality games whose physical component excellence is a primary purchase motivation.

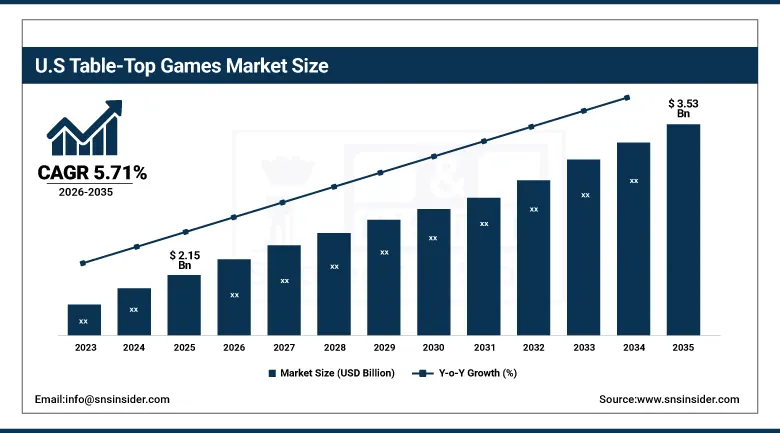

U.S. Table-Top Games Market Outlook

The U.S. table-top games market was valued at approximately USD 2.15 billion in 2025 and is expected to reach approximately USD 3.53 billion by 2035, growing at a CAGR of 5.71%, driven by strong engagement across board games, card games, and role-playing categories, the sustained cultural prominence of Dungeons and Dragons amplified by Critical Role's streaming content, and robust online and specialty retail distribution across the country's extensive hobby game store network.

The United States is the world's largest and most commercially developed table-top games market, where the highest per-capita game spending, the world's most active game design and publishing industry, the largest collection of game conventions including Gen Con, PAX Unplugged, and Origins attracting over 200,000 dedicated hobby consumers annually, and the most extensive specialty game store retail network create commercial infrastructure sustaining market leadership. The cultural resurgence of Dungeons and Dragons through Critical Role's actual-play streaming on YouTube and Twitch, which has accumulated tens of millions of views introducing the role-playing genre to mainstream audiences, has contributed to sustained RPG segment expansion drawing new consumers into the broader hobby game market through the accessible entry point of the game's Fifth Edition.

Table-Top Games Market Segment Analysis

-

By Game Type, Board Games dominated with approximately 47.10% in 2025 through broad demographic appeal, mass retail distribution, and sustained popularity of gateway titles attracting casual gamers alongside the enthusiast community; Tabletop Wargames is the fastest-growing at a CAGR of 5.10% driven by Games Workshop's Warhammer franchise expansion and growing miniature game interest among younger demographics through accessible starter formats.

-

By Player Count, Small Group games dominated with approximately 49.10% as the three to four player configuration suiting friend groups and family game nights represents the modal purchase context; Large Group games are the fastest-growing as party and social deduction formats expand for larger gathering occasions where inclusive whole-group games dominate entertainment selection.

-

By Distribution Channel, Online retail holds a growing share through crowdfunding fulfilment and e-commerce convenience, while specialty game stores maintain importance as the discovery, community, and demo experience environment driving purchase intention among enthusiast consumers evaluating complex game designs.

-

By Age Group, Adults dominated as the primary purchasing and playing demographic for the hobby game market's premium segments; Young Adults represent the fastest-growing segment as the demographic that discovered gateway games through university game societies and digital content is entering peak spending years with established hobby habits.

By Game Type, Board Games dominate, Tabletop Wargames is expected to grow fastest

The Board Games maintained its dominance with about 47.10% in 2025, which was due to a vast range of games in that segment. The range starts from very easy gateway games like Catan and Ticket to Ride, which offer very easy entry into the hobby for consumers who are not yet engaged with such activities; continues with the midweight strategy games like Wingspan, Viticulture, and Pandemic Legacy, which attract hobbyists; and concludes with heavy strategy games like Gloomhaven and Spirit Island, which provide hundreds of hours of fun for hobby communities, whose money expenditure per game makes them the top spending consumer segment. The board game segment is favored because it fits well into impulse and gifting situations, owing to its physicality, appeal, and familiarity.

Tabletop Wargames is the fastest-growing type at a CAGR of 5.10% through 2035, anchored by Games Workshop's extraordinary commercial success with Warhammer 40,000 and Warhammer: Age of Sigmar that have created the world's most commercially successful miniature wargame ecosystem encompassing plastic miniature kits, hobby paints, game rulebooks, licensed fiction, video game adaptations, and extensive merchandise. Games Workshop's ability to attract younger wargamers through streamlined starter products like Combat Patrol and Warcry skirmish formats providing satisfying complete game experiences at lower entry cost and complexity than full army-scale play has expanded the accessible recruitment population beyond the dedicated hobbyist who can commit to the multi-year painting and collection project that full-scale Warhammer development represents.

By Player Count, Small Group dominates, Large Group is expected to grow fastest

Small Group games retained the dominant position with approximately 49.10% in 2025, as the three to four player configuration that the majority of commercial board and card game designs target represents the modal social gaming context for the hobby's primary consumer demographic of friend groups gathering for game nights, couples with regular gaming groups, and family sessions typically involving three to five participants across age ranges. This player count aligns with design requirements maximising strategic depth, reasonable session duration, and individual agency that the hobby community values most highly, creating a self-reinforcing design convention sustaining small group dominance in both market share and new title development investment.

Large Group games are the fastest-growing player count category as expanding table-top deployment in social entertainment contexts including corporate team building, bar and restaurant game nights, party entertainment, and large family gatherings creates demand for designs supporting six or more simultaneous players without the exclusion dynamics of sequential-play games. Social deduction games including The Resistance, Deception: Murder in Hong Kong, Blood on the Clocktower, and party formats including Just One, Wavelength, and Codenames represent commercially successful large group designs whose wide accessibility and short playing time make them reliable gift and mainstream retail purchases.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.7% |

|

Europe |

Germany |

22.4% |

|

Asia Pacific |

Japan |

41.3% |

|

Middle East & Africa |

UAE |

27.6% |

|

Latin America |

Brazil |

43.8% |

North America Table-Top Games Market Insights

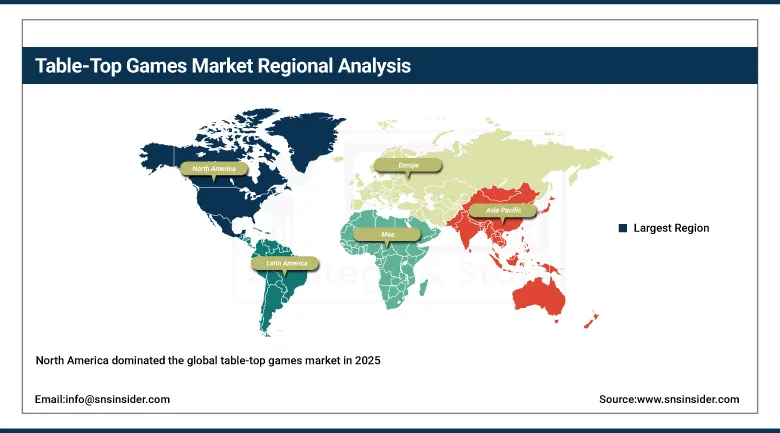

North America dominated the global table-top games market in 2025, with the United States accounting for approximately 83.7% of North American revenues as the world's largest table-top games market by both revenue and publishing industry activity. The region's leadership reflects extraordinary concentration of game design talent, publishing infrastructure, and hobby retail in the United States, where table-top gaming has achieved mainstream cultural visibility through the cultural prominence of Dungeons and Dragons, celebrity game advocacy, and television programmes featuring game nights. The Gen Con, PAX Unplugged, and Origins conventions collectively attract over 200,000 dedicated hobbyist attendees annually, sustaining a convention circuit serving simultaneously as the industry's primary product launch platform, fan community gathering, and new player recruitment pipeline.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Table-Top Games Market Insights

Europe is the birthplace of the modern hobby board game movement, where Reiner Knizia, Klaus Teuber, Wolfgang Kramer, and subsequent European designers established the Eurogame design tradition prioritising elegant mechanics, limited player elimination, and theme-integrated strategy that has defined global hobby board game design standards. Germany accounts for approximately 22.4% of European revenues through the Spiel des Jahres award programme identifying commercially and culturally influential game designs since 1979 and the Essen SPIEL fair as the world's largest table-top game trade fair and consumer event. The United Kingdom, France, Nordic countries, and Benelux represent additional significant markets with well-developed hobby game retail, café gaming culture, and convention scenes sustaining strong consumer communities.

Asia Pacific Table-Top Games Market Insights

Asia Pacific is the fastest-growing regional table-top games market, driven by South Korea's extraordinary board game café culture creating a densely networked infrastructure of commercial game playing venues, Japan's traditional card game strength including the globally dominant Pokémon Trading Card Game, and rapidly developing hobby board game awareness in China where Western Eurogame imports and domestic publisher development are simultaneously building a substantial consumer market. Japan accounts for approximately 41.3% of Asia Pacific revenues through the globally dominant Pokémon TCG, strong domestic publisher and retail infrastructure in major cities, and the traditional appreciation for game playing as a culturally valued leisure activity across Japanese demographics.

MEA & Latin America Table-Top Games Market Insights

The Middle East and Africa and Latin America represent developing table-top games markets where cultural traditions of social gathering, growing middle-class disposable income supporting hobby spending, and global accessibility of game content through online retail are building consumer awareness beyond chess, backgammon, and traditional card formats. UAE leads MEA revenues at approximately 27.6% through cosmopolitan expatriate populations with established hobby interests, premium retail infrastructure, and growing board game festival programming. Brazil leads Latin American revenues at approximately 43.8% through large urban populations, active gaming community culture in major cities, and growing dedicated table-top game retail and café infrastructure in major metropolitan markets.

Market Dynamics

Growth Drivers: Digital entertainment screen fatigue driving investment in offline social gaming combined with crowdfunding democratising innovative design and building committed pre-launch communities sustaining commercial momentum

The primary structural growth drivers are documented consumer fatigue with passive and isolated digital entertainment driving meaningful consumer segments toward the active, social, and cognitively engaging offline entertainment that table-top gaming provides uniquely, combined with the crowdfunding platform revolution democratising game design and publishing while creating millions of pre-committed purchasers whose advance financial support enables production quality and design ambitions that conventional retail economics could not sustain. The COVID-19 pandemic's acceleration of board game adoption as families sought shared entertainment has proven structural rather than temporary, as players who discovered or re-engaged with table-top gaming during isolation have maintained higher purchasing and playing frequency in the post-pandemic period.

Restraints: Market saturation and discoverability challenge with thousands of annual releases competing for limited retail shelf space and consumer attention, rising production cost from premium component expectations, and specialist hobby game barrier to entry for casual consumers

One notable limitation arises from the increasing problem of discoverability that confronts the thousands of new board games that are produced each year across the world, where the availability that has been provided through cheap production and crowdfunding mechanisms has resulted in an overcrowded market that places even high-caliber games under intense competition in terms of consumer attention, retail shelf space, and coverage on purchasing-oriented review websites. In 2024 alone, BoardGameGeek was forced to add over 3,500 new unique games, thus establishing "winner take most" conditions where success becomes concentrated among a few despite overall design caliber.

Opportunities: Hybrid digital-physical innovation creating new engagement models, international localisation for emerging markets, and educational institutional table-top game market development

The development of hybrid table-top games using physical components as the primary play interface while integrating digital augmentation through companion applications providing real-time rules adjudication, automated villain AI, and persistent campaign tracking represents the most commercially significant product innovation opportunity, simultaneously addressing complexity barriers preventing new player independent learning while enhancing narrative immersion achievable within physical game formats. International localisation of established titles for non-English-language markets in Asia, Latin America, and the Middle East represents substantial market expansion opportunity for publishers whose games have proven commercially successful in English-language markets but whose non-English market penetration is limited by absent localised editions.

Recent Developments:

-

2025: Hasbro reported continued strength in its Wizards of the Coast division, whose Magic: The Gathering and Dungeons and Dragons product lines collectively generated over USD 1.3 billion in annual revenue, with D&D's player base continuing to grow following the mainstreaming effect of Critical Role's streaming content and the 2023 film release.

-

2025: Games Workshop reported record annual revenues driven by continued global Warhammer 40,000 franchise expansion, new product launches across Age of Sigmar and specialist games ranges, and new company-owned retail store openings in Asia Pacific markets achieving above-average growth relative to established Western markets.

-

2025: Stonemaier Games' Wingspan reached over 4 million copies sold globally, demonstrating the extraordinary commercial longevity of gateway hobby games whose accessible design and wide demographic appeal sustain sales volumes that few hobby titles have historically achieved.

-

2025: Kickstarter reported table-top games as the platform's highest-grossing category by funded project value for the eleventh consecutive year, with several campaigns exceeding USD 10 million in backer funding confirming that crowdfunding continues generating the market's most commercially ambitious and consumer-anticipated releases.

-

2025: Asmodee Group continued international expansion through distribution network strengthening in Asian markets, entering licensing agreements for localised editions of its European Eurogame portfolio titles with South Korean, Chinese, and Japanese publishers serving rapidly developing Asian hobby game communities.

Table-Top Games Market Key Players

-

Hasbro Inc. (Wizards of the Coast)

-

Mattel Inc.

-

Games Workshop Group PLC

-

Asmodee Group

-

Ravensburger AG

-

CMON Limited

-

Stonemaier Games

-

Fantasy Flight Games (Asmodee)

-

Days of Wonder (Asmodee)

-

Alderac Entertainment Group

-

Z-Man Games (Asmodee)

-

Kosmos Verlag

-

Thames & Kosmos

-

Repos Production

-

Iello Games

-

Bezier Games

-

Roxley Games

-

Plaid Hat Games

-

Czech Games Edition

-

Stronghold Games

Table-Top Games Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.15 Billion |

| Market Size by 2035 | USD 12.80 Billion |

| CAGR | CAGR of 5.99% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Game Type (Board Games, Card Games, Role-Playing Games, Tabletop Wargames, Others) • By Player Count (Solo, Two-Player, Small Group, Large Group) • By Distribution Channel (Online Retail, Specialty Game Stores, Mass Merchandise Retail, Others) • By Age Group (Children, Young Adults, Adults) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Hasbro Inc. (Wizards of the Coast), Mattel Inc., Games Workshop Group PLC, Asmodee Group, Ravensburger AG, CMON Limited, Stonemaier Games, Fantasy Flight Games (Asmodee), Daktronics Inc., Broadsign International LLC , Z-Man Games (Asmodee), Kosmos Verlag, Thames & Kosmos, Repos Production, Iello Games, Bezier Games, Roxley Games, Plaid Hat Games, Czech Games Edition, Stronghold Games |

Frequently Asked Questions

The Table-Top Games Market is expected to grow at a CAGR of 5.99% from 2026 to 2035.

The Table-Top Games Market was valued at USD 7.15 billion in 2025.

Digital entertainment screen fatigue driving consumer investment in offline social gaming combined with crowdfunding democratising innovative game design and building committed pre-launch consumer communities that sustain commercial momentum at launch.

Board Games dominated with approximately 47.10% of revenues in 2025.

North America dominated the Table-Top Games Market in 2025.

Get in Touch