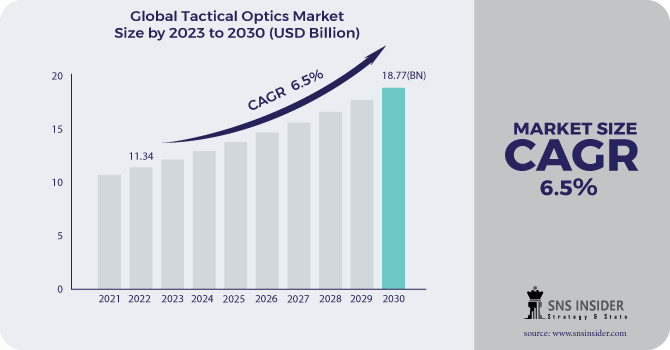

The Tactical Optics Market Size was valued at USD 11.34 billion in 2022 and is expected to reach USD 18.77 Billion by 2030 with a growing CAGR of 6.5% over the forecast period 2023-2030.

The Global Tactical Optics Market is estimated to increase significantly during the forecast period as a result of factors such as rising demand for EO/IR cameras and expanding weapon modernization programmer around the world. Furthermore, rising procurement of tactical optics for dismounted soldiers and vehicle platforms is likely to boost market expansion. Furthermore, the rising usage of tactical optics by the United States military services is likely to fuel market expansion.

To get more information on Tactical Optics Market - Request Free Sample Report

MARKET DYNAMICS

KEY DRIVERS

Weapon Enhancement programs across the world

Increase in tactical optics acquisition for vehicle platforms and dismounted soldiers: The government is investing in tactical optics to provide increased ISR and target acquisition capabilities to the defence forces.

RESTRAINTS

High technological skill is required to produce tactical optics.

Government rules are strict.

THE IMPACT OF COVID-19

The report discusses the impact of the Corona virus COVID-19: Since the breakout of the COVID-19 virus in December 2019, the disease has spread to practically every country on the planet, prompting the World Health Organization to declare it a public health emergency. The global effects of the corona virus illness 2019 (COVID-19) are already being noticed, and they will have a considerable impact on the Tactical Optics industry in 2020. Flight cancellations; travel bans and quarantines; restaurants closed; all indoor/outdoor events restricted; over forty countries declared states of emergency; massive slowing of the supply chain; stock market volatility; falling business confidence, growing panic among the population, and uncertainty about the future.

The Intelligence, Surveillance, and Reconnaissance (ISR) segment is expected to grow at a rapid pace during the forecast period due to increased demand for expanded ISR capabilities by armed forces throughout the world as a result of rising terrorism. The target acquisition and identification segment dominated the market in 2022 and is predicted to exhibit the greatest CAGR throughout the forecast period due to rising installations of target identification and acquisition solutions across many platforms. The increasing use of drones and unmanned systems for search and rescue missions is likely to fuel segment expansion.

Increased deployment of EO/IR cameras for border and coastal surveillance to track illegal activities is likely to fuel market growth. The increased implementation of thermal imaging technology for enhanced visibility at night and in low visibility conditions is likely to fuel the segment's growth. The segment's growth is being driven by the increased adoption of innovative optical technologies such as rangefinders, binoculars, target acquisition & surveillance systems, and night vision goggles. Due to the rising use of thermal cameras for border monitoring, the cameras & display segment dominated the market in 2022 and is predicted to post the highest CAGR during the forecast period. The rising need for head-mounted displays for soldiers on the battlefield is projected to propel the market forward. The segment's growth is likely to be driven by rising demand for improved target identification capabilities and the requirement to provide soldiers with improved visibility in low-light situations.

Factors such as increased military acquisition of armoured vehicles and expanded installation of high-tech cameras for border monitoring are boosting the segment's expansion. Increased naval modernization efforts by countries such as China, India, and the United States to bolster their marine capabilities are expected to boost the segment's expansion.

Due to the growing use of tactical UAV and unmanned systems by the military forces, as well as the rising adoption of attack helicopters by several emerging countries such as India, this category is expected to grow at the fastest CAGR during the forecast period. The armed forces' increasing requirement for greater situational awareness is projected to drive the segment's growth.

The increased procurement of new weapons is likely to drive the segment's growth. Increased army modernization efforts around the world are projected to drive segment growth. Due to the increased use of unmanned systems by nations such as the United States and China for various applications such as border surveillance and search and rescue, this category is projected to grow at the fastest rate CAGR during the forecast period.

By End-Use

Manned Platform

Weapon Mounted

Soldier

Unmanned Platform

By Range

Short Range

Medium Range

Long Range

By Application

Intelligence, Surveillance, & Reconnaissance

Target Acquisition & Identification

Search & Rescue

Border & Coastal patrol

By Platform

Ground

Naval

Airborne

By Product

Weapon Scopes & Sights

Handheld Sighting Devices

Cameras & Displays

Night Vision Scopes

.png)

Need any customization research on Tactical Optics Market - Enquiry Now

REGIONAL ANALYSIS

Asia Pacific is expected to lead the tactical optics market for the next decade beginning in 2022. Because of the demand for dismounted soldiers, armoured vehicles, drones, aircraft, and helicopters, the industry in this region has enormous potential. Furthermore, increased military weapon purchase is propelling the Asia Pacific Tactical Optics market.

Because of the existence of firms such as Raytheon Technologies Corporation, Lockheed Martin Corporation, and Northrop Grumman Corporation, North America led the worldwide tactical optics market in 2022.

The increasing use of smart weaponry by armed forces in nations such as the United Kingdom is likely to boost market expansion in the area. the UK Army tested a new smart rifle-scope that uses computer image technology to improve target acquisition skills. Increasing territorial conflicts in the region, as well as rising defence expenditures in nations such as China and India, are driving Asia-Pacific market expansion.

The presence of firms such as Israel Aerospace Industries and Elbit Systems Ltd, as well as increased terrorist activity in the region, are projected to boost market expansion in the region.

Extreme conflict scenarios in nations such as Mexico are projected to drive tactical optics demand in this region.

REGIONAL COVERAGE:

North America

USA

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

The Netherlands

Rest of Europe

Asia-Pacific

Japan

south Korea

China

India

Australia

Rest of Asia-Pacific

The Middle East & Africa

Israel

UAE

South Africa

Rest of Middle East & Africa

Latin America

Brazil

Argentina

Rest of Latin America

The Major Platyers are Kongsberg Gruppen,Vortex Optics, Saab AB, Raytheon Company, Sig Sauer, Elbit Systems, Leupold & Stevens Inc., BAE Systems, Leonardo, Bushnell Corporation and Other Players

Kongsberg Gruppen-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2022 | US$ 11.34 Billion |

| Market Size by 2030 | US$ 18.77 Billion |

| CAGR | CAGR of 6.5% From 2023 to 2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Ground, Naval and Airborne) • By Application (Intelligence, Surveillance, & Reconnaissance, Target Acquisition & Identification, Search & Rescue and Border) • By Range (Short Range, Medium Range and Long Range) • By Product (Weapon Scopes & Sights, Handheld Sighting Devices, Cameras & Displays) • By End-Use (Manned Platform, Weapon Mounted, Soldier and Unmanned Platform) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Kongsberg Gruppen,Vortex Optics,Saab AB,Raytheon Company,Sig Sauer,Elbit Systems,Leupold?Stevens,BAE Systems,Leonardo,Bushnell Corporation, |

| DRIVERS | • Weapon Enhancement programs across the world • Increase in tactical optics acquisition for vehicle platforms and dismounted soldiers: The government is investing in tactical optics to provide increased ISR and target acquisition capabilities to the defence forces. |

| RESTRAINTS | • High technological skill is required to produce tactical optics. • Government rules are strict. |

Manufacturers/Service provider, Consultant, Association, Research institute, private and universities libraries, Suppliers and Distributors of the product.

With a significant number of companies making tactical optic equipment, North America maintains its lead in terms of supply.

Kongsberg Gruppen AS, Raytheon Company, Elbit Systems Ltd., Saab AB, Thales Group Are the major contributing player to this market

Because of their modest magnification range, these devices assist shooters/pilots/soldiers in seeing beyond the scope of their usual eyesight.

During the forecast period, the APAC market is expected to increase significantly.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 COVID-19 Impact Analysis

4.2 Impact of Ukraine- Russia war

4.3 Impact of ongoing Recession

4.3.1 Introduction

4.3.2 Impact on major economies

4.3.2.1 US

4.3.2.2 Canada

4.3.2.3 Germany

4.3.2.4 France

4.3.2.5 United Kingdom

4.3.2.6 China

4.3.2.7 Japan

4.3.2.8 South Korea

4.3.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8.Tactical Optics Market Segmentation, By End-Use

8.1 Manned Platform

8.2 Weapon Mounted

8.3 Soldier

8.4 Unmanned Platform

9.Tactical Optics Market Segmentation, By Range

9.1 Short Range

9.2 Medium Range

9.3 Long Range

10.Tactical Optics Market Segmentation, By Application

10.1 Intelligence, Surveillance, & Reconnaissance

10.2 Target Acquisition & Identification

10.3 Search & Rescue

10.4 Border & Coastal patrol

11.Tactical Optics Market Segmentation, By Platform

11.1 Ground

11.2 Naval

11.3 Airborne

12.Tactical Optics Market Segmentation, By Product

12.1 Weapon Scopes & Sights

12.2 Handheld Sighting Devices

12.3 Cameras & Displays

12.4 Night Vision Scopes

13. Regional Analysis

13.1 Introduction

13.2 North America

13.2.1 USA

13.2.2 Canada

13.2.3 Mexico

13.3 Europe

13.3.1 Germany

13.3.2 UK

13.3.3 France

13.3.4 Italy

13.3.5 Spain

13.3.6 The Netherlands

13.3.7 Rest of Europe

13.4 Asia-Pacific

13.4.1 Japan

13.4.2 South Korea

13.4.3 China

13.4.4 India

13.4.5 Australia

13.4.6 Rest of Asia-Pacific

13.5 The Middle East & Africa

13.5.1 Israel

13.5.2 UAE

13.5.3 South Africa

13.5.4 Rest

13.6 Latin America

13.6.1 Brazil

13.6.2 Argentina

13.6.3 Rest of Latin America

14.Company Profiles

14.1 Elbit Systems Ltd

14.1.1 Financial

14.1.2 Products/ Services Offered

14.1.3 SWOT Analysis

14.1.4 The SNS view

14.2 KONGSBERG Gruppen AS

14.3 L3Harris Technologies, Inc.

14.4 Northrop Grumman Corporation

14.5 Raytheon Technologies Corporation

14.6 Thales Group

14.7 Saab AB

14.8 Lockheed Martin Corporation

14.9 Leonardo S.p.A.

14.10 BAE Systems

15. Competitive Landscape

15.1 Competitive Benchmarking

15.2 Market Share Analysis

15.3 Recent Developments

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Caliber Ammunition Market Size was valued at USD 24.20 billion in 2022 and is expected to reach USD 32.62 billion by 2030 and grow at a CAGR of 3.8% over the forecast period 2023-2030.

The Aerospace Bearings Market Size was valued at USD 7.24 billion in 2022 and is expected to reach USD 14.42 billion by 2030 with a growing CAGR of 9% over the forecast period 2023-2030.

The Aircraft Fuel Cells Market size was valued at USD 1.42 Billion in 2022 & is estimated to reach USD 3.27 Billion by 2030 and increase at a compound annual growth rate (CAGR) of 11% between 2023 and 2030.

The Drone Package Delivery System Market Size was valued at USD 0.29 billion in 2022 and is expected to reach USD 7.33 billion by 2030 with an emerging CAGR of 49.22% over the forecast period 2023-2030.

The Small Arms Market Size was valued at USD 9.18 billion in 2022 and is expected to reach USD 11.06 billion by 2030 with a growing CAGR of 2.1% over the forecast period 2023-2030.

The Nanosatellite and Microsatellite Market Size was valued at US$ 2.92 billion in 2022a and is expected to reach USD 14.36 billion by 2030 with a growing CAGR of 22% over the forecast period 2023-2030.

Hi! Click one of our member below to chat on Phone

© 2024 All Rights Reserved by SNS Insider Pvt Ltd