Tactical Optics Market Report Scope & Overview:

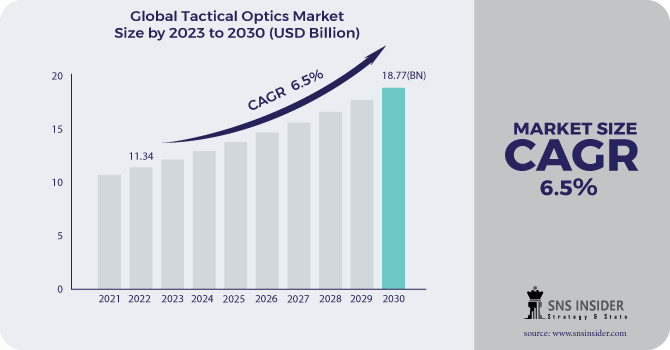

The Tactical Optics Market Size was valued at USD 11.34 billion in 2022 and is expected to reach USD 18.77 Billion by 2030 with a growing CAGR of 6.5% over the forecast period 2023-2030.

The Global Tactical Optics Market is estimated to increase significantly during the forecast period as a result of factors such as rising demand for EO/IR cameras and expanding weapon modernization programmer around the world. Furthermore, rising procurement of tactical optics for dismounted soldiers and vehicle platforms is likely to boost market expansion. Furthermore, the rising usage of tactical optics by the United States military services is likely to fuel market expansion.

To get more information on Tactical Optics Market - Request Free Sample Report

MARKET DYNAMICS

KEY DRIVERS

-

Weapon Enhancement programs across the world

-

Increase in tactical optics acquisition for vehicle platforms and dismounted soldiers: The government is investing in tactical optics to provide increased ISR and target acquisition capabilities to the defence forces.

RESTRAINTS

-

High technological skill is required to produce tactical optics.

-

Government rules are strict.

THE IMPACT OF COVID-19

The report discusses the impact of the Corona virus COVID-19: Since the breakout of the COVID-19 virus in December 2019, the disease has spread to practically every country on the planet, prompting the World Health Organization to declare it a public health emergency. The global effects of the corona virus illness 2019 (COVID-19) are already being noticed, and they will have a considerable impact on the Tactical Optics industry in 2020. Flight cancellations; travel bans and quarantines; restaurants closed; all indoor/outdoor events restricted; over forty countries declared states of emergency; massive slowing of the supply chain; stock market volatility; falling business confidence, growing panic among the population, and uncertainty about the future.

The Intelligence, Surveillance, and Reconnaissance (ISR) segment is expected to grow at a rapid pace during the forecast period due to increased demand for expanded ISR capabilities by armed forces throughout the world as a result of rising terrorism. The target acquisition and identification segment dominated the market in 2022 and is predicted to exhibit the greatest CAGR throughout the forecast period due to rising installations of target identification and acquisition solutions across many platforms. The increasing use of drones and unmanned systems for search and rescue missions is likely to fuel segment expansion.

Increased deployment of EO/IR cameras for border and coastal surveillance to track illegal activities is likely to fuel market growth. The increased implementation of thermal imaging technology for enhanced visibility at night and in low visibility conditions is likely to fuel the segment's growth. The segment's growth is being driven by the increased adoption of innovative optical technologies such as rangefinders, binoculars, target acquisition & surveillance systems, and night vision goggles. Due to the rising use of thermal cameras for border monitoring, the cameras & display segment dominated the market in 2022 and is predicted to post the highest CAGR during the forecast period. The rising need for head-mounted displays for soldiers on the battlefield is projected to propel the market forward. The segment's growth is likely to be driven by rising demand for improved target identification capabilities and the requirement to provide soldiers with improved visibility in low-light situations.

Factors such as increased military acquisition of armoured vehicles and expanded installation of high-tech cameras for border monitoring are boosting the segment's expansion. Increased naval modernization efforts by countries such as China, India, and the United States to bolster their marine capabilities are expected to boost the segment's expansion.

Due to the growing use of tactical UAV and unmanned systems by the military forces, as well as the rising adoption of attack helicopters by several emerging countries such as India, this category is expected to grow at the fastest CAGR during the forecast period. The armed forces' increasing requirement for greater situational awareness is projected to drive the segment's growth.

The increased procurement of new weapons is likely to drive the segment's growth. Increased army modernization efforts around the world are projected to drive segment growth. Due to the increased use of unmanned systems by nations such as the United States and China for various applications such as border surveillance and search and rescue, this category is projected to grow at the fastest rate CAGR during the forecast period.

KEY MARKET SEGMENTATION

By End-Use

-

Manned Platform

-

Weapon Mounted

-

Soldier

-

Unmanned Platform

By Range

-

Short Range

-

Medium Range

-

Long Range

By Application

-

Intelligence, Surveillance, & Reconnaissance

-

Target Acquisition & Identification

-

Search & Rescue

-

Border & Coastal patrol

By Platform

-

Ground

-

Naval

-

Airborne

By Product

-

Weapon Scopes & Sights

-

Handheld Sighting Devices

-

Cameras & Displays

-

Night Vision Scopes

.png)

Need any customization research on Tactical Optics Market - Enquiry Now

REGIONAL ANALYSIS

Asia Pacific is expected to lead the tactical optics market for the next decade beginning in 2022. Because of the demand for dismounted soldiers, armoured vehicles, drones, aircraft, and helicopters, the industry in this region has enormous potential. Furthermore, increased military weapon purchase is propelling the Asia Pacific Tactical Optics market.

Because of the existence of firms such as Raytheon Technologies Corporation, Lockheed Martin Corporation, and Northrop Grumman Corporation, North America led the worldwide tactical optics market in 2022.

The increasing use of smart weaponry by armed forces in nations such as the United Kingdom is likely to boost market expansion in the area. the UK Army tested a new smart rifle-scope that uses computer image technology to improve target acquisition skills. Increasing territorial conflicts in the region, as well as rising defence expenditures in nations such as China and India, are driving Asia-Pacific market expansion.

The presence of firms such as Israel Aerospace Industries and Elbit Systems Ltd, as well as increased terrorist activity in the region, are projected to boost market expansion in the region.

Extreme conflict scenarios in nations such as Mexico are projected to drive tactical optics demand in this region.

REGIONAL COVERAGE:

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

KEY PLAYERS

The Major Platyers are Kongsberg Gruppen, Vortex Optics, Saab AB, Raytheon Company, Sig Sauer, Elbit Systems, Leupold & Stevens Inc., BAE Systems, Leonardo, Bushnell Corporation and Other Players

Kongsberg Gruppen-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2022 | US$ 11.34 Billion |

| Market Size by 2030 | US$ 18.77 Billion |

| CAGR | CAGR of 6.5% From 2023 to 2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Platform (Ground, Naval and Airborne) • By Application (Intelligence, Surveillance, & Reconnaissance, Target Acquisition & Identification, Search & Rescue and Border) • By Range (Short Range, Medium Range and Long Range) • By Product (Weapon Scopes & Sights, Handheld Sighting Devices, Cameras & Displays) • By End-Use (Manned Platform, Weapon Mounted, Soldier and Unmanned Platform) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Kongsberg Gruppen,Vortex Optics,Saab AB,Raytheon Company,Sig Sauer,Elbit Systems,Leupold?Stevens,BAE Systems,Leonardo,Bushnell Corporation, |

| DRIVERS | • Weapon Enhancement programs across the world • Increase in tactical optics acquisition for vehicle platforms and dismounted soldiers: The government is investing in tactical optics to provide increased ISR and target acquisition capabilities to the defence forces. |

| RESTRAINTS | • High technological skill is required to produce tactical optics. • Government rules are strict. |

Frequently Asked Questions

During the forecast period, the APAC market is expected to increase significantly.

Because of their modest magnification range, these devices assist shooters/pilots/soldiers in seeing beyond the scope of their usual eyesight.

Kongsberg Gruppen AS, Raytheon Company, Elbit Systems Ltd., Saab AB, Thales Group Are the major contributing player to this market

With a significant number of companies making tactical optic equipment, North America maintains its lead in terms of supply.

Manufacturers/Service provider, Consultant, Association, Research institute, private and universities libraries, Suppliers and Distributors of the product.

Get in Touch