Talent Acquisition Software Market Report Scope & Overview:

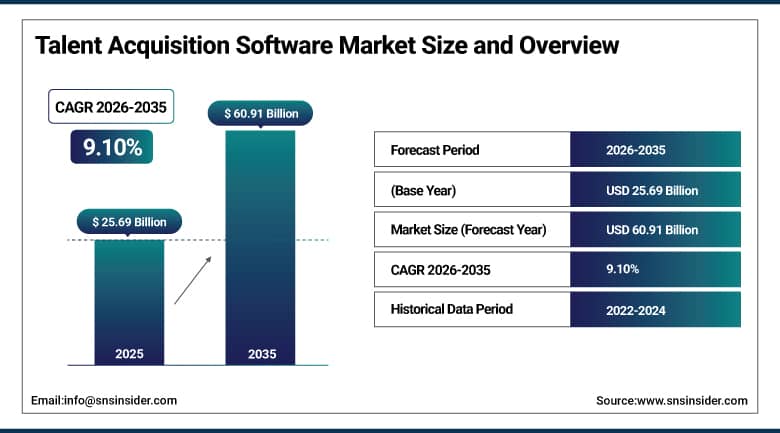

The Talent Acquisition Software Market was valued at USD 25.69 Billion in 2025 and is expected to reach USD 60.91 Billion by 2035, growing at a CAGR of 9.10% from 2026–2035.

The global talent acquisition software market is at a structural inflection point. AI-powered automation, cloud-native deployment, and data-driven candidate matching are replacing manual recruitment workflows at an accelerating pace. Organisations that once managed hiring through spreadsheets and email now deploy integrated platforms that track applicants, engage candidates, automate screening, and measure hiring quality within unified digital environments. Competition for skilled talent has intensified across virtually every industry and geography. Companies cannot afford slow, inefficient recruitment when candidates accept competing offers within days. Remote work adoption has simultaneously created globally distributed hiring demands that older geographically anchored systems were not built to serve effectively.

LinkedIn Talent Solutions’ 2025 Future of Recruiting report confirmed that 62% of talent acquisition professionals now consider AI tools essential to their recruitment workflows, up from 27% in 2022, indicating that AI in talent acquisition has crossed from early adopter novelty into mainstream operational necessity within a three-year period. Modern platforms embed AI across sourcing, screening, scheduling, and prediction. Bias detection tools help organisations meet diversity hiring commitments. Predictive analytics identify which candidates are most likely to succeed and stay, while conversational AI handles initial candidate engagement without human involvement.

Talent Acquisition Software Market Size and Forecast

-

Market Size in 2026E: USD 28.03 Billion

-

Market Size by 2035: USD 60.91 Billion

-

CAGR: 9.10% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Talent Acquisition Software Market - Request Free Sample Report

Talent Acquisition Software Market Trends

-

Growing adoption of AI-powered candidate screening and matching tools is significantly improving recruiter productivity by automating the most time-intensive stages of the hiring funnel and reducing average time-to-hire across enterprise recruitment operations globally.

-

Rising integration of large language model APIs into recruitment platforms is enabling automated job description generation, candidate communication drafting, and interview question creation within unified workflow environments without recruiter involvement at each step.

-

Increasing demand for skills-based hiring tools is driving adoption of structured assessment platforms that evaluate candidate competency rather than relying solely on degree credentials, as major employers explicitly de-emphasise educational requirements in favour of demonstrated capability.

-

Expanding use of workforce analytics dashboards is enabling HR leaders to measure time-to-hire, source quality, offer acceptance rate, and diversity metrics in real time, transforming recruitment from an anecdotal function into a data-driven commercial operation.

-

Growing regulatory pressure from AI hiring transparency laws across U.S. states and the EU AI Act’s high-risk classification of employment decision AI is compelling vendors to build explainability and bias auditing features into their screening systems as standard procurement prerequisites.

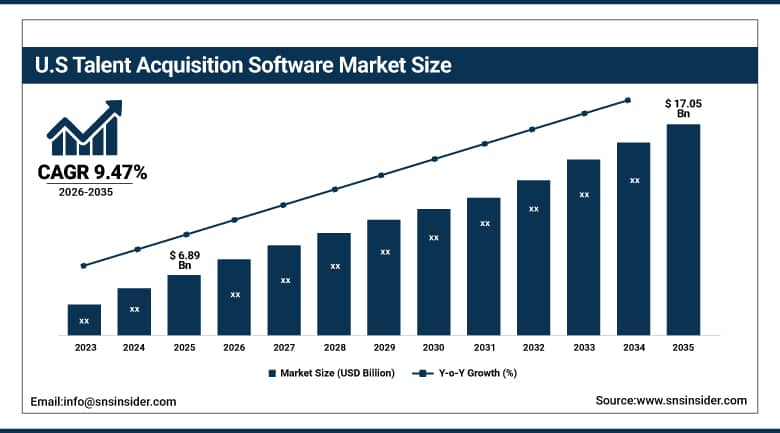

U.S. Talent Acquisition Software Market Outlook

The U.S. Talent Acquisition Software Market was valued at approximately USD 6.89 Billion in 2025 and is expected to reach approximately USD 17.05 Billion by 2035, growing at a CAGR of approximately 9.47%.

The United States is the world’s largest talent acquisition software market. It combines the highest enterprise technology adoption rate globally with a labour market that has maintained structural skill scarcity across engineering, healthcare, and professional services for the better part of a decade. American organisations invest more per hire than those in any other market and place proportionally greater commercial importance on reducing time-to-hire and improving hire quality through technology. Cloud-based SaaS is the dominant deployment model. Workday Recruiting, SAP SuccessFactors, Oracle Taleo, and iCIMS serve the Fortune 500 enterprise tier with comprehensive suites, while Greenhouse, Lever, JazzHR, and Jobvite serve the mid-market with faster-deploying and more flexible platforms. LinkedIn Talent Solutions occupies a unique position as both a sourcing network and a platform layer whose data depth provides AI matching advantages that standalone ATS competitors cannot replicate without equivalent candidate behavioural data access.

Workday’s January 2025 launch of its AI Recruiting Agent, which autonomously sources candidates, drafts outreach messages, and schedules interviews without manual recruiter involvement at each step, marked the first widely deployed example of agentic AI in enterprise talent acquisition at commercial scale. The subsequent Workday-Randstad partnership combined this autonomous capability with Randstad’s global talent network, enabling enterprise customers to access AI-powered candidate sourcing and measurably improved hiring velocity through a single commercial relationship that integrates workflow automation with one of the world’s largest professional staffing datasets across multiple international hiring markets.

Talent Acquisition Software Market Segment Analysis

-

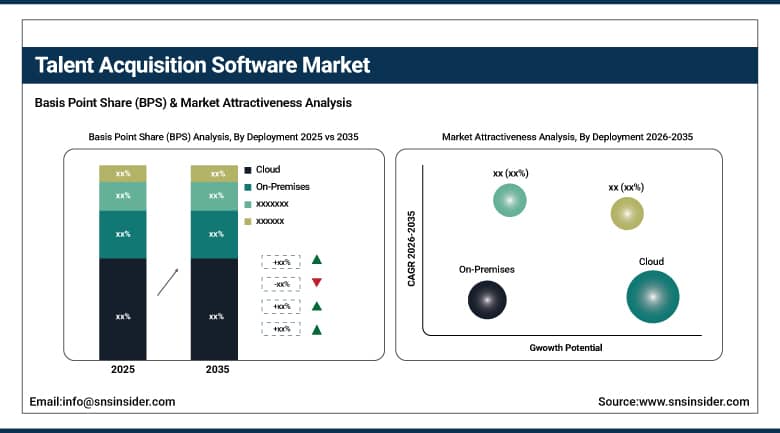

By Deployment, Cloud dominated with approximately 71% share in 2025 through its ease of deployment, automatic feature updates, and lower infrastructure cost that make it the default choice for organisations of all sizes undergoing digital hiring transformation; Cloud is also the fastest-growing deployment segment as continuing SaaS adoption displaces remaining on-premises installations and new market entrants adopt cloud-native architectures entirely from inception.

-

By Organization Size, Large Enterprises dominated with approximately 60% share in 2025 due to their large-scale recruitment volumes, diverse talent requirements, and financial capacity to invest in comprehensive integrated talent acquisition suites with advanced analytics; SMEs are the fastest-growing organisation size segment, driven by the increasing availability of affordable modular SaaS solutions that deliver enterprise-grade recruitment capability at accessible mid-market price points.

-

By Industry Vertical, IT & Telecom dominated with approximately 31% share in 2025 through the technology sector’s high hiring volume, technical candidate screening complexity, and above-average investment in HR technology platforms; Healthcare is the fastest-growing vertical, driven by structural nursing and clinical staffing shortages, compliance-heavy credentialing requirements, and the urgency of filling patient-care roles that makes efficient recruitment a direct clinical and financial business imperative.

-

By Functionality, Applicant Tracking System (ATS) dominated with approximately 35% share in 2025 as the core workflow infrastructure for digitising recruitment and managing candidate pipelines across enterprise teams; Candidate Relationship Management (CRM) is the fastest-growing functionality segment, driven by the organisational shift from reactive post-application candidate management to proactive talent community building and pipeline development ahead of active hiring cycles.

-

By Pricing Model, Subscription-Based pricing dominated with approximately 55% share in 2025 through its predictable cost structure and alignment with enterprise SaaS procurement preferences; Per-User pricing is the fastest-growing model, driven by SME adoption where usage-proportional cost scaling is more commercially accessible than flat subscription fees during periods of variable or seasonal hiring activity.

By Deployment, cloud dominates and grows fastest

Cloud deployment retained the dominant position with approximately 71% of the talent acquisition software market in 2025, a dominance that is both structural and self-reinforcing. Once the majority of enterprise HR systems moved to cloud-based platforms, the integration ecosystem built around those platforms also became cloud-native, creating network effects that further disadvantaged on-premises alternatives whose integration requirements grew progressively more complex relative to cloud-to-cloud API connectivity. Cloud platforms scale elastically with hiring volumes without requiring infrastructure sized for peak periods. Software updates deliver automatically without IT deployment projects. For globally distributed organisations, cloud delivery eliminates the geographic infrastructure constraints that on-premises systems create in non-headquarters locations, making cloud the natural architecture for enterprises whose recruitment operations span multiple countries and time zones.

Cloud is simultaneously the fastest-growing deployment segment as on-premises installations are decommissioned and replaced with cloud alternatives across the installed base. The remaining on-premises installations are concentrated in large financial services, government, and defence organisations whose data sovereignty and security requirements historically justified closed infrastructure. These organisations are progressively adopting private cloud and hybrid deployment architectures that deliver cloud economics while maintaining the data control requirements their regulatory environments impose. Each enterprise transition from on-premises to cloud-based talent acquisition adds recurring SaaS revenue to the market and removes a fixed-period licence, creating a revenue mix shift that elevates total market growth rate above what new customer acquisition alone would generate over the forecast period.

By Organization Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant organisation size position with approximately 60% of the talent acquisition software market in 2025, reflecting both the commercial scale of their recruitment operations and their financial capacity to invest in comprehensive talent acquisition platforms that integrate across HR, payroll, and workforce management systems. A Fortune 500 company hiring several thousand people annually generates platform usage volumes, integration requirements, and analytics complexity that justify the enterprise pricing of Workday, SAP SuccessFactors, and Oracle Taleo. Large enterprise customers also drive product development investment at the market’s leading vendors, as the advanced capabilities they demand, including predictive quality-of-hire models, diversity and inclusion analytics, and global compliance management, cascade down to mid-market products over time as technology matures and standardises across the competitive landscape.

SMEs are the fastest-growing organisation size segment as SaaS economics have made enterprise-grade recruitment capability accessible at price points that were impossible with licensed on-premises software. Platforms including Greenhouse, Lever, JazzHR, and Zoho Recruit offer applicant tracking, candidate communication automation, and hiring analytics at monthly subscription rates that small businesses can justify from hiring cost savings within a single successful hire. As SMEs compete for talent with larger organisations in structurally tight labour markets across technology, healthcare, and professional services, the productivity advantage of modern recruitment software becomes a competitive necessity rather than an optional upgrade. The addressable SME market is substantially larger by organisation count than the enterprise market, making its faster growth rate commercially significant for the market’s long-term total revenue trajectory.

By Industry Vertical, IT & telecom dominates, healthcare grows fastest

IT and telecom retained the dominant industry vertical position with approximately 31% of the talent acquisition software market in 2025, reflecting the sector’s above-average hiring volume, the technical complexity of screening engineering candidates, and the sector’s cultural orientation toward technology adoption in its own operations. Software engineers, data scientists, product managers, and cloud infrastructure specialists require structured technical assessment, multiple interview stages, and rapid offer velocity that manual recruitment processes cannot efficiently manage at the scale that technology companies require. When engineers routinely receive multiple competitive offers within a week of entering the market, the speed advantage of AI-automated sourcing, screening, and scheduling becomes a direct hiring conversion factor that translates technology investment into measurable commercial outcome improvement.

Healthcare is the fastest-growing industry vertical in the talent acquisition software market, driven by a structural nursing and clinical staffing shortage that has persisted since the COVID-19 pandemic amplified pre-existing workforce pipeline gaps. Hospitals and health systems compete aggressively for limited pools of qualified nurses, physicians, radiographers, and allied health professionals whose credential verification, licensing compliance, and clinical competency assessment requirements add recruitment complexity that generic ATS platforms were not originally designed to manage. Healthcare-specific talent acquisition platforms and purpose-built modules within iCIMS and Workday are growing faster than the overall market as this vertical’s recruitment complexity, combined with the direct patient care and financial impact of unfilled clinical roles, creates strong institutional motivation to invest in specialised recruitment technology that reduces both vacancy duration and compliance risk simultaneously.

By Functionality, ATS dominates, CRM grows fastest

Applicant Tracking Systems retained the dominant functionality position with approximately 35% of the talent acquisition software market in 2025. ATS is the foundational layer of every digital recruitment workflow. It captures applications, organises candidate information, tracks hiring stage progression, manages recruiter task assignments, and generates the compliance documentation that employment law requires. No other recruitment software category replaces ATS; every other functionality segment extends it. The modern ATS has significantly expanded beyond its origins as a database and workflow tool. Leading platforms from iCIMS, Greenhouse, and Jobvite now embed AI screening, automated candidate communication, interview scheduling, and hiring manager collaboration tools within the core ATS workflow, meaning the boundary between a standalone ATS and a full integrated talent acquisition suite has blurred substantially across the competitive product landscape.

Candidate Relationship Management is the fastest-growing functionality segment in the talent acquisition software market, driven by the commercial shift from reactive to proactive recruitment strategy that growing hiring velocity requirements and tighter labour markets are making commercially necessary. In a reactive model, organisations post jobs and screen applicants who respond. In a proactive model, organisations continuously build and nurture talent communities of pre-qualified candidates who can be activated quickly when roles open, reducing both time-to-hire and per-hire sourcing cost substantially. CRM tools automate periodic engagement communications, track candidate interest signals, and alert recruiters when previously engaged candidates re-enter the active job market. As the cost of extended vacancies in revenue-critical roles grows, the commercial value of a warm talent pipeline that CRM enables is becoming a differentiating operational capability across mid-market and enterprise organisations that previously relied entirely on reactive job posting strategies.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

India |

28.6% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Talent Acquisition Software Market Insights

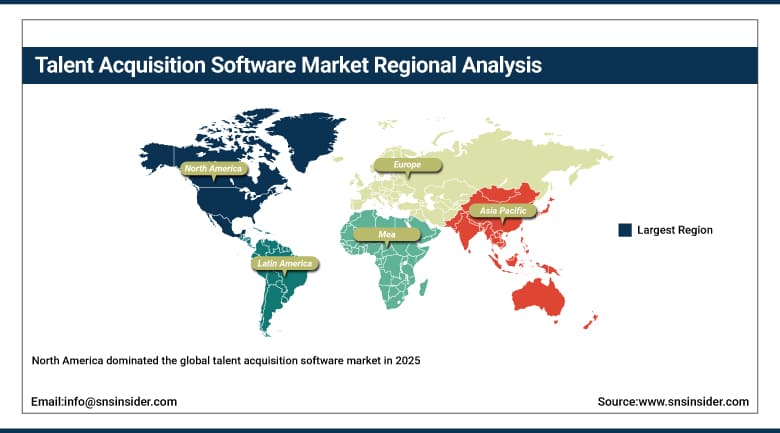

North America dominated the global talent acquisition software market in 2025, with the United States accounting for approximately 83.4% of North American revenues and representing the world’s largest national market by a significant commercial margin. The combination of a structurally tight labour market, above-average enterprise technology investment, and a mature SaaS vendor ecosystem whose commercial centre is in North America makes the region the global reference market for talent acquisition technology development, pricing, and competitive innovation. Enterprise procurement through long-term contracts with Workday, SAP, and Oracle defines the top tier, while agile mid-market adoption of modern platforms including Greenhouse, Lever, and Ashby defines the second, and both tiers are simultaneously growing as AI capability expansion creates new purchase motivation across existing and new customer segments.

Canada contributes approximately 16.6% of North American revenues through strong enterprise adoption, a competitive labour market whose technology, financial services, and natural resources sectors generate consistent recruitment software demand, and a growing domestic technology studio and AI company sector whose international talent competition makes modern recruitment infrastructure commercially essential. The Canadian market mirrors U.S. trends in cloud adoption rate, AI feature adoption pace, and the balance between enterprise suite and mid-market specialist platform procurement, making it a commercially consistent extension of the North American market’s demand patterns rather than a structurally distinct regional market requiring meaningfully different commercial or product strategy from vendors serving both countries simultaneously.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Talent Acquisition Software Market Insights

Europe is a commercially significant talent acquisition software market where GDPR compliance requirements have fundamentally shaped how candidate data is collected, stored, and processed, creating both procurement prerequisites and commercial differentiation opportunities that distinguish European market dynamics from North American equivalents. All major talent acquisition software vendors operating in Europe must demonstrate GDPR-compliant data handling, right-to-erasure enforcement, and data residency options as basic procurement requirements before enterprise consideration. Germany accounts for approximately 22.3% of European revenues as the region’s largest national market, anchored by its engineering and manufacturing sector’s high-volume technical recruitment demand and works council requirements that impose specific employee data handling governance on recruitment software deployments across the country’s major industrial enterprises.

The United Kingdom, France, and the Nordic countries are also significant European markets with established enterprise technology adoption and above-average investment in employer brand and candidate experience capabilities that drive adoption of recruitment marketing and CRM functionalities beyond basic ATS deployment. The EU AI Act’s classification of AI systems used in employment decisions as high-risk is reshaping vendor product development priorities across the region, requiring conformity assessments, human oversight documentation, and transparency disclosures that are progressively becoming competitive differentiators as European enterprise procurement teams add regulatory AI compliance audit capability to their standard vendor evaluation criteria for recruitment technology procurement.

Asia Pacific Talent Acquisition Software Market Insights

Asia Pacific is the fastest-growing regional talent acquisition software market, driven by India’s technology services sector’s extraordinary hiring volumes, Australia and Singapore’s sophisticated enterprise markets with above-average SaaS adoption, and China’s independently developing domestic HR technology ecosystem whose platforms including BOSS Zhipin and Lagou serve local enterprises with locally optimised solutions. India accounts for approximately 28.6% of Asia Pacific revenues as the region’s most commercially significant growth market, where the IT services sector’s requirement to hire tens of thousands of engineers annually across multiple cities creates platform usage scale that justifies enterprise contract values and drives adoption of AI-powered volume screening that manual processes cannot sustain at the pace that growth-stage technology service delivery demands.

Emerging Southeast Asian markets including Indonesia, Vietnam, and the Philippines are at earlier adoption stages but growing quickly as internet penetration, digital workforce formation, and the entry of multinational corporations building regional operations create structured demand for modern recruitment tools. The Asia Pacific market’s diversity of regulatory environments, languages, and labour market structures requires platform localisation investment that global vendors are progressively making as the region’s combined total addressable market scale justifies the development cost. Regional specialists who build for specific national requirements in Japan, South Korea, and Australia maintain strong home market positions through depth of local compliance and user experience adaptation that large global platforms targeting broad geographic coverage cannot match at equivalent quality.

MEA & Latin America Talent Acquisition Software Market Insights

The Middle East and Africa and Latin America are growing talent acquisition software markets where rising enterprise digitalisation, expanding multinational corporate operations, and the adoption of cloud-based HR platforms are creating structured demand for modern recruitment technology. Saudi Arabia leads MEA revenues at approximately 38.4% of the regional total, driven by Vision 2030’s economic diversification agenda that requires large-scale recruitment of domestic talent into new private sector roles and international specialist recruitment to develop sectors where local talent pipelines are currently insufficient to support the pace of economic transformation that the programme targets across energy, technology, tourism, and manufacturing verticals.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large private sector, significant presence of multinational corporations across financial services, manufacturing, and consumer goods, and a competitive professional labour market whose dynamics in technology and engineering mirror the structural talent competition driving recruitment software investment in more mature global markets. Portuguese-language localisation requirements, Brazilian labour law compliance features including CLT employment documentation, and local payment infrastructure integration are the key product localisation requirements that international vendors must address to compete effectively with domestic alternatives whose home market knowledge and commercial relationships provide initial advantages in enterprise procurement processes across Brazil and the wider Latin American region.

Market Dynamics

Growth Drivers: Structural talent competition making efficient recruitment a business priority, AI-powered automation improving recruiter productivity and hire quality

The primary structural growth driver for the talent acquisition software market is the persistent competition for skilled talent across technology, healthcare, finance, and engineering disciplines that makes efficient, high-quality recruitment a board-level business priority. When organisations cannot hire fast enough to execute growth strategies, recruitment software investment becomes a revenue enablement decision whose return is measurable in terms of revenue per open position and competitive advantage in executing expansion initiatives that depend on headcount. This structural motivation is geography-independent and cycle-resistant, sustaining software investment even during macroeconomic caution when other technology categories face budget scrutiny. Cloud SaaS deployment has simultaneously lowered the adoption barrier to the point where organisations with ten employees can access the same recruitment technology category as Fortune 500 enterprises, expanding the total addressable market substantially beyond the large enterprise segment that defined the market’s commercial base in its first decade.

AI automation is expanding what talent acquisition software can deliver and improving the measurable quality of hiring outcomes simultaneously. Platforms that autonomously source candidates from multiple channels, screen applications against defined criteria, schedule interviews without recruiter involvement, and predict candidate quality scores are delivering productivity improvements that traditional ATS tools were not capable of. These capabilities create commercial value that sustains above-market price realisation and customer retention, as organisations that have integrated AI-powered recruitment into their workflows demonstrate hiring performance improvements that make switching platforms commercially costly relative to the price of retaining and upgrading existing relationships. The agentic AI expansion represented by Workday’s AI Recruiting Agent launch in January 2025 demonstrates that the market’s capability evolution is accelerating rather than plateauing, sustaining the purchase motivation that drives both new customer acquisition and existing customer upsell.

Restraints: Data privacy compliance complexity across multiple jurisdictions increasing vendor development costs, AI bias and discrimination risk creating regulatory exposure

Data privacy compliance is a meaningful commercial restraint on global expansion for talent acquisition software vendors. GDPR in Europe, CCPA in California, PIPL in China, and a growing number of state-level and national data protection laws each impose specific requirements on candidate data collection, processing, storage, and deletion. Vendors operating globally must build compliance architecture for each jurisdiction, creating development cost and legal overhead that smaller vendors cannot sustain while simultaneously maintaining the AI feature development pace that competitive positioning requires. This creates a compliance-driven consolidation pressure that benefits established vendors with the compliance infrastructure investment capacity that their scale enables, potentially limiting the pace at which new entrants can challenge incumbents in regulated enterprise segments.

AI bias risk is creating both regulatory and reputational exposure for vendors and their enterprise customers. The EU AI Act’s high-risk classification of AI in employment decisions requires conformity assessments and human oversight documentation that add compliance cost to AI feature deployment in European markets. Several U.S. jurisdictions have passed or proposed AI hiring bias audit requirements. Vendors who cannot demonstrate that their AI screening systems do not create disparate impact across protected demographic groups face procurement disqualification from risk-averse enterprise buyers who cannot afford the employer liability that discriminatory automated screening creates in employment law jurisdictions with mature class action litigation infrastructure.

Opportunities: Skills-based hiring transformation creating demand for assessment integration, internal talent mobility software extending platform value beyond external hiring

Skills-based hiring represents the most commercially significant functional expansion opportunity in the talent acquisition software market. Major employers including IBM, Accenture, and the U.S. federal government have explicitly de-emphasised degree requirements in favour of demonstrated skill assessment, requiring talent acquisition platforms to integrate with skills assessment tools, build verified competency profiles, and match candidates to roles based on capability evidence rather than credential proxies. Vendors that build credible skills-assessment integration access a growing customer demand that existing degree-filter ATS functionality cannot satisfy, creating an upsell and cross-sell opportunity within established customer bases whose skills hiring ambitions exceed their current platform capabilities. The addressable market for skills-based hiring tooling extends across virtually every enterprise vertical, making this an opportunity whose commercial scale matches that of the core ATS replacement cycle.

Internal talent mobility is expanding the definition of talent acquisition beyond external candidate recruitment, as organisations with strong internal mobility programmes reduce external hiring costs and improve retention by identifying current employees who could fill open roles before posting externally. Talent marketplace software connecting internal candidates to opportunities is growing as a complement to external-facing ATS and CRM platforms. Vendors including Workday, Phenom People, and Eightfold AI are investing in internal mobility capabilities that extend their talent acquisition suite value proposition beyond the single hire event into ongoing workforce development and career management, deepening platform stickiness and increasing the commercial lifetime value of each enterprise customer relationship beyond what external recruitment software alone can sustain.

Recent Developments:

-

2025: Workday launched its AI Recruiting Agent in January 2025, enabling autonomous candidate sourcing, outreach drafting, and interview scheduling without manual recruiter involvement at each workflow step, marking the first widely deployed example of agentic AI in enterprise talent acquisition at commercial scale across the North American enterprise market.

-

2025: Workday and Randstad partnered to combine Workday’s AI Recruiting Agent with Randstad’s global talent network, enabling enterprise customers to access autonomous candidate sourcing and measurably improved hiring velocity through a unified commercial relationship that integrates AI workflow automation with one of the world’s largest professional staffing datasets.

-

2025: SAP SuccessFactors released enhanced AI candidate matching capabilities within its Recruiting module, integrating large language model-powered job description analysis with candidate profile scoring that automatically ranks applicants against role requirements across the full active candidate database, reducing average time-to-shortlist for enterprise customers across European and North American markets.

-

2025: iCIMS expanded its AI assistant capabilities across its talent acquisition platform, adding automated candidate engagement sequences, predictive offer acceptance scoring, and real-time recruiter productivity coaching that surfaces process bottlenecks and recommends workflow interventions to improve individual and team hiring performance metrics for its global enterprise and mid-market customer base.

-

2025: Greenhouse launched a structured hiring product update incorporating skills-based assessment integration, standardised interview scorecards with AI-powered calibration guidance, and diversity analytics measuring demographic representation at every hiring funnel stage, enabling customers to identify and address bias before final hiring decisions and demonstrate equitable process compliance to institutional stakeholders.

Talent Acquisition Software Market Key Players

-

Workday Inc.

-

SAP SE (SuccessFactors)

-

Oracle Corporation (Taleo)

-

iCIMS Inc.

-

Greenhouse Software Inc.

-

Lever Inc. (Employ Inc.)

-

LinkedIn Corporation (LinkedIn Talent Solutions)

-

Jobvite Inc. (Employ Inc.)

-

SmartRecruiters Inc.

-

Bullhorn Inc.

-

JazzHR (Employ Inc.)

-

Zoho Corporation (Zoho Recruit)

-

Cornerstone OnDemand Inc.

-

Phenom People Inc.

-

Eightfold AI Inc.

-

Beamery Ltd.

-

Ashby Inc.

-

Paradox AI Inc.

-

HireVue Inc.

-

Karat Inc.

Talent Acquisition Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.69 Billion |

| Market Size by 2035 | USD 60.91 Billion |

| CAGR | CAGR of 9.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Deployment (Cloud, On-Premises) • By Organization Size (Large Enterprises, Small & Medium Enterprises) • By Industry Vertical (IT & Telecom, Healthcare, BFSI, Retail, Manufacturing, Others) • By Functionality (Applicant Tracking System, Candidate Relationship Management, Recruitment Marketing, Onboarding Software, Others) • By Pricing Model (Subscription-Based, Per-User, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Workday Inc., SAP SE (SuccessFactors), Oracle Corporation (Taleo), iCIMS Inc., Greenhouse Software Inc., Lever Inc. (Employ Inc.), LinkedIn Corporation (LinkedIn Talent Solutions), Jobvite Inc. (Employ Inc.), SmartRecruiters Inc., Bullhorn Inc., JazzHR (Employ Inc.), Zoho Corporation (Zoho Recruit), Cornerstone OnDemand Inc., Phenom People Inc., Eightfold AI Inc., Beamery Ltd., Ashby Inc., Paradox AI Inc., HireVue Inc., Karat Inc. |

Frequently Asked Questions

The Talent Acquisition Software Market is expected to grow at a CAGR of 9.10% from 2026 to 2035.

The Talent Acquisition Software Market was valued at USD 25.69 Billion in 2025.

Structural talent competition making efficient recruitment a board-level business priority, combined with AI-powered automation improving recruiter productivity and hire quality.

Applicant Tracking System (ATS) dominated with approximately 35% of revenues in 2025.

North America dominated the Talent Acquisition Software Market in 2025, with the United States accounting for approximately 83.4% of North American revenues.

Get in Touch