Telecom Site Management Software Market Report Scope & Overview:

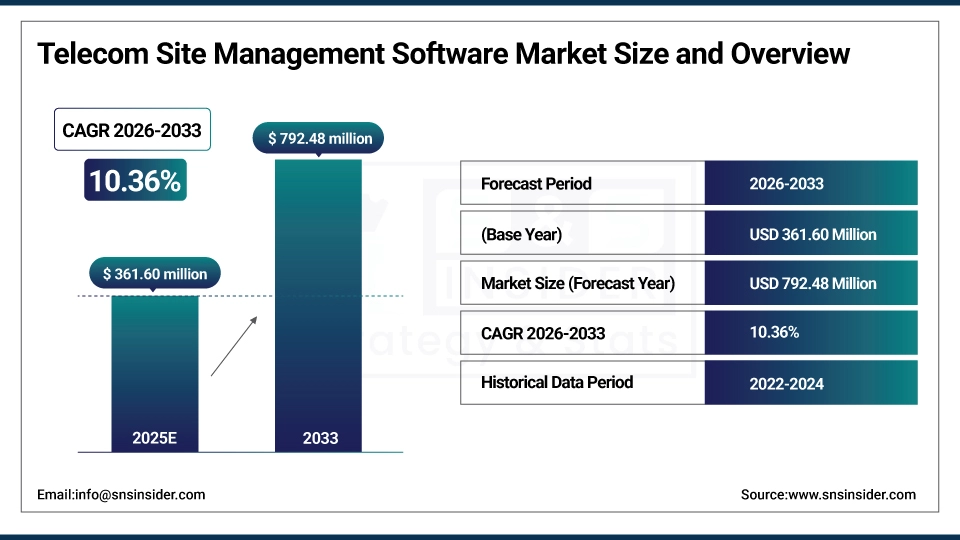

The Telecom Site Management Software Market is valued at USD 361.60 Million in 2025E and is expected to reach USD 792.48 Million by 2033, growing at a CAGR of 10.36% from 2026-2033.

The Telecom Site Management Software Market is growing due to the rapid expansion of 5G networks, increasing telecom tower deployments, and the need for more efficient site operations. Rising demand for remote monitoring, predictive maintenance, and automated workflow management is pushing operators to adopt advanced digital tools. Additionally, the shift toward energy-efficient infrastructure, real-time asset tracking, and improved compliance management is driving telecom companies to use centralized platforms that reduce operational costs and enhance network reliability.

In 2025, global adoption of telecom site management software rose by 34%, as 75% of operators leveraged AI and IoT-enabled platforms to achieve 35% energy savings, real-time asset visibility, and 28% faster resolution of site-level issues across 5G networks.

Telecom Site Management Software Market Size and Forecast

-

Market Size in 2025E: USD 361.60 Million

-

Market Size by 2033: USD 792.48 Million

-

CAGR: 10.36% from 2026 to 2033

-

Base Year: 2025E

-

Forecast Period: 2026–2033

-

Historical Data: 2022–2024

To Get more information on Telecom Site Management Software Market - Request Free Sample Report

Telecom Site Management Software Market Trends

-

Rising adoption of centralized software platforms to optimize telecom site operations and reduce maintenance costs

-

Increasing integration of IoT and AI for real-time monitoring and predictive maintenance of telecom infrastructure

-

Growing demand for cloud-based solutions enabling remote management and scalable telecom site operations

-

Expansion of 5G networks driving need for efficient site planning, deployment, and performance monitoring tools

-

Rising focus on energy management and sustainability in telecom sites to reduce operational expenditures

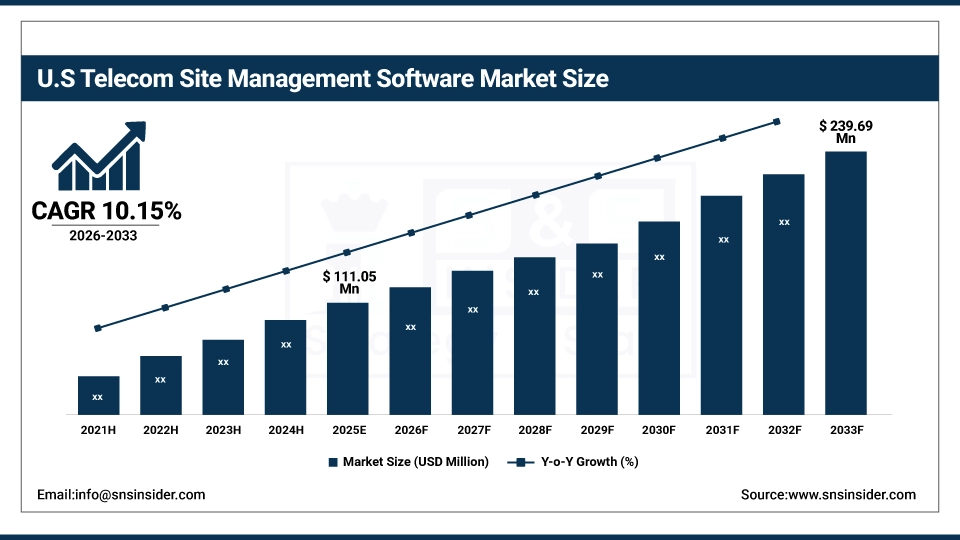

U.S. Telecom Site Management Software Market is valued at USD 111.05 Million in 2025E and is expected to reach USD 239.69 Million by 2033, growing at a CAGR of 10.15% from 2026-2033.

The U.S. Telecom Site Management Software Market is growing due to expanding 5G infrastructure, rising tower density, and the need for streamlined site operations. Increasing adoption of remote monitoring, energy optimization tools, and automated maintenance systems is driving demand as operators focus on reducing costs and improving network uptime.

Telecom Site Management Software Market Growth Drivers:

-

Rapid expansion of 4G and 5G networks is driving demand for telecom site management software to optimize infrastructure deployment, monitoring, and maintenance globally

The global rollout of 4G and 5G networks has significantly increased the complexity of telecom infrastructure, including base stations, small cells, and fiber connections. Telecom operators are adopting site management software to efficiently plan, monitor, and maintain network sites while ensuring minimal downtime. These solutions help in asset tracking, site audits, and performance monitoring, optimizing network coverage and quality. The accelerated deployment of next-generation networks, combined with rising data traffic and connectivity demands, continues to fuel software adoption, making site management tools essential for telecom operators seeking operational efficiency and cost-effective network expansion.

In 2025, the rapid rollout of 4G and 5G networks drove a 40% increase in demand for telecom site management software, with 68% of operators using it to streamline infrastructure deployment, reduce maintenance costs by 30%, and enhance site performance globally.

-

Growing need to reduce operational costs and enhance network efficiency encourages telecom operators to adopt advanced software solutions for site management and energy optimization

Telecom operators face mounting operational expenses, including energy consumption, maintenance, and labor costs associated with managing multiple network sites. Site management software enables automated monitoring of energy usage, predictive maintenance, and resource allocation, helping operators minimize expenses while maximizing network efficiency. Advanced analytics and reporting features allow real-time decision-making, improving uptime and service reliability. The increasing focus on sustainable and energy-efficient operations further drives adoption. As operators aim to reduce operational expenditure and enhance service quality, advanced site management solutions have become a critical tool for optimizing overall network performance and reducing costs.

In 2025, 72% of telecom operators deployed advanced site management software, cutting operational costs by 28% and improving energy efficiency by 35% through AI-driven monitoring and automation across 5G and legacy networks.

Telecom Site Management Software Market Restraints:

-

High implementation and integration costs of telecom site management software limit adoption, particularly among small operators and emerging market telecom providers

Deploying telecom site management software involves substantial initial investments, including software licenses, hardware, integration with existing systems, and staff training. Smaller operators and companies in emerging markets may find these costs prohibitive, limiting widespread adoption. Additionally, integration with legacy infrastructure and multi-vendor networks can be technically challenging and time-consuming. These financial and operational hurdles may delay ROI, discouraging investment in advanced solutions. As a result, high costs create a barrier for smaller telecom providers and slow market penetration, particularly in regions with constrained budgets or limited technical expertise for managing sophisticated software systems.

In 2025, 60% of small and emerging-market telecom providers deferred adoption of site management software due to implementation costs exceeding USD100,000 and complex integration with legacy multi-vendor infrastructure.

-

Data security concerns and complexity of software deployment across multi-vendor networks hinder widespread implementation and operational efficiency

Telecom site management software often handles sensitive operational and network data, raising cybersecurity concerns for operators. The risk of data breaches, unauthorized access, or system failures can affect network reliability and service quality. Additionally, integrating software across heterogeneous networks with equipment from multiple vendors increases deployment complexity, requiring specialized knowledge and coordination. These challenges can lead to implementation delays, operational inefficiencies, and higher maintenance costs. Security concerns and technical complexity remain significant restraints for telecom operators, slowing the adoption of advanced site management solutions despite their potential benefits in monitoring and optimizing network infrastructure.

In 2025, 65% of telecom operators cited data security risks and multi-vendor integration complexity as key barriers, delaying software deployment and reducing operational efficiency by up to 25% in heterogeneous network environments.

Telecom Site Management Software Market Opportunities:

-

Increasing adoption of IoT, AI, and cloud-based solutions in telecom operations provides opportunities for software providers to offer advanced monitoring and predictive maintenance features

Emerging technologies such as IoT, artificial intelligence, and cloud computing are transforming telecom network operations. IoT-enabled sensors allow real-time site monitoring, while AI algorithms predict maintenance needs and detect anomalies, reducing downtime. Cloud-based platforms enable centralized management of distributed network sites, providing scalability and remote accessibility. Telecom operators are increasingly seeking software solutions that leverage these technologies to enhance efficiency, reduce operational costs, and improve service reliability. These technological trends create substantial opportunities for software providers to develop innovative, feature-rich solutions catering to next-generation telecom networks and advanced site management requirements.

In 2025, 70% of telecom operators integrated IoT, AI, and cloud-based software, boosting predictive maintenance adoption by 45% and reducing network downtime by 30% through advanced remote monitoring and analytics.

-

Rising investments in network infrastructure, smart cities, and energy-efficient telecom sites create new market potential for innovative site management solutions

Governments and private operators are investing heavily in expanding telecom infrastructure, supporting 5G deployment, smart city initiatives, and energy-efficient network operations. These investments drive demand for software that can efficiently manage large-scale networks, optimize energy consumption, and monitor multiple sites simultaneously. Site management solutions play a critical role in asset tracking, preventive maintenance, and resource optimization, aligning with sustainability and operational efficiency goals. As network densification and modernization continue, telecom operators have significant opportunities to adopt innovative software solutions that enhance performance, reduce costs, and support scalable, technologically advanced infrastructure development.

In 2025, rising investments in smart cities and green telecom infrastructure drove a 38% increase in demand for intelligent site management solutions, enhancing energy efficiency, remote monitoring, and operational reliability across 5G and IoT deployments.

Telecom Site Management Software Market Segment Highlights

-

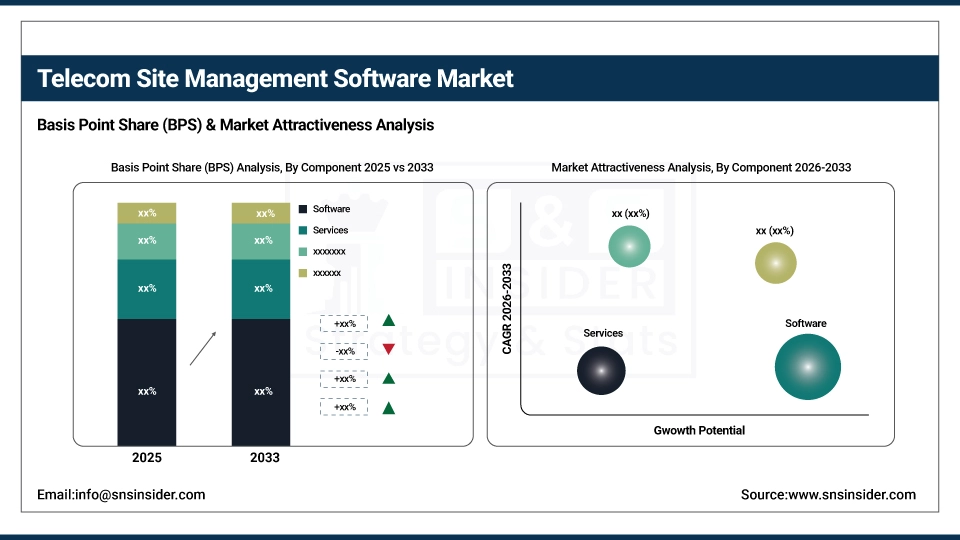

By Component: Software led with 42.5% share, while Consulting & Integration Services is the fastest-growing segment with CAGR of 14.1%.

-

By Network Type: 4G LTE led with 38.7% share, while 5G is the fastest-growing segment with CAGR of 16.3%.

-

By Application: Site Monitoring & Control led with 40.2% share, while Network Optimization is the fastest-growing segment with CAGR of 15.2%.

-

By End User: Telecom Operators led with 44.6% share, while Enterprises are the fastest-growing segment with CAGR of 13.9%.

Telecom Site Management Software Market Segment Analysis

By Component: Software led, while Consulting & Integration Services is the fastest-growing segment.

Software dominates the component segment as telecom operators depend on advanced platforms for asset tracking, fault management, workflow automation, and network resource planning. Its scalability, predictive analytics capabilities, and seamless integration with multi-vendor infrastructure make it the core operational layer for site management. With increasing network complexity, operators prioritize centralized, real-time monitoring software to reduce downtime, optimize energy usage, and streamline maintenance, solidifying its continued leadership in global deployments.

Consulting & Integration Services is the fastest-growing segment as operators increasingly require tailored solutions, customized workflows, and expert-led deployment support during network modernization and 5G rollouts. The rise of multi-technology environments—spanning legacy 4G, expanding fiber networks, and emerging 5G infrastructures—demands professional integration for seamless interoperability. These services also help optimize operational costs, ensure regulatory compliance, and enable efficient system upgrades, driving rapid global adoption, particularly across high-growth Asian and Middle Eastern markets.

By Network Type: 4G LTE led, while 5G is the fastest-growing segment.

4G LTE remains the dominant network type due to its widespread global deployment, mature infrastructure, and continued heavy usage across consumer and enterprise segments. Operators maintain large-scale 4G networks to support voice, broadband, and IoT applications, driving sustained investment in monitoring, maintenance, and optimization. With billions of existing connections and extensive rural and urban coverage, 4G LTE still forms the backbone of telecom operations, ensuring stable revenue contribution despite ongoing 5G adoption.

5G is experiencing the fastest growth as countries rapidly expand deployments to support ultra-low-latency applications, enhanced mobile broadband, and industrial automation. Its rising adoption drives demand for advanced site management tools capable of handling dense small-cell networks, high-frequency spectrum, and energy-intensive hardware. Operators increasingly prioritize 5G-specific optimization and remote monitoring capabilities to manage complex, high-capacity infrastructures. Accelerated government initiatives, private 5G networks, and enterprise digitalization further fuel its rapid global expansion, especially in Asia-Pacific.

By Application: Site Monitoring & Control led, while Network Optimization is the fastest-growing segment.

Site Monitoring & Control leads the application segment due to its essential role in ensuring network uptime, detecting equipment failures, and enabling real-time visibility across distributed tower sites. Operators rely on these solutions to automate maintenance, reduce operational costs, and prevent outages through predictive alerts. As networks grow more complex, centralized monitoring becomes critical for efficient resource allocation and risk management, reinforcing its dominance across both developed and emerging telecom markets.

Network Optimization is the fastest-growing segment, driven by the need to improve performance, manage rising traffic demand, and enhance energy efficiency. With 5G expansion, operators require advanced analytical tools to optimize spectrum usage, reduce latency, and balance network loads. The shift toward AI-driven optimization, dynamic resource allocation, and automated performance tuning accelerates adoption. Enterprises deploying private networks also fuel demand, making optimization solutions central to delivering superior connectivity and operational reliability.

By End User: Telecom Operators led, while Enterprises are the fastest-growing segment.

Telecom Operators dominate the end-user segment because they manage the largest share of network assets, including towers, fiber nodes, and distributed sites. Their need for comprehensive tools to streamline maintenance, reduce downtime, and ensure regulatory compliance drives heavy adoption of site management platforms. With increasing pressure to enhance service quality and control operational costs, operators prioritize integrated solutions that unify monitoring, asset management, and workflow automation, securing their continued leadership in the market.

Enterprises are the fastest-growing segment as organizations deploy private LTE/5G networks to support IoT, robotics, automation, and secure digital communication systems. These deployments require robust site management capabilities for monitoring assets, optimizing energy usage, and ensuring network reliability. Rising digital transformation initiatives across manufacturing, logistics, oil & gas, and smart campuses accelerate adoption. The shift toward decentralized enterprise networks and edge infrastructure further strengthens demand, driving rapid growth across global markets.

Telecom Site Management Software Market Regional Analysis

North America Telecom Site Management Software Market Insights:

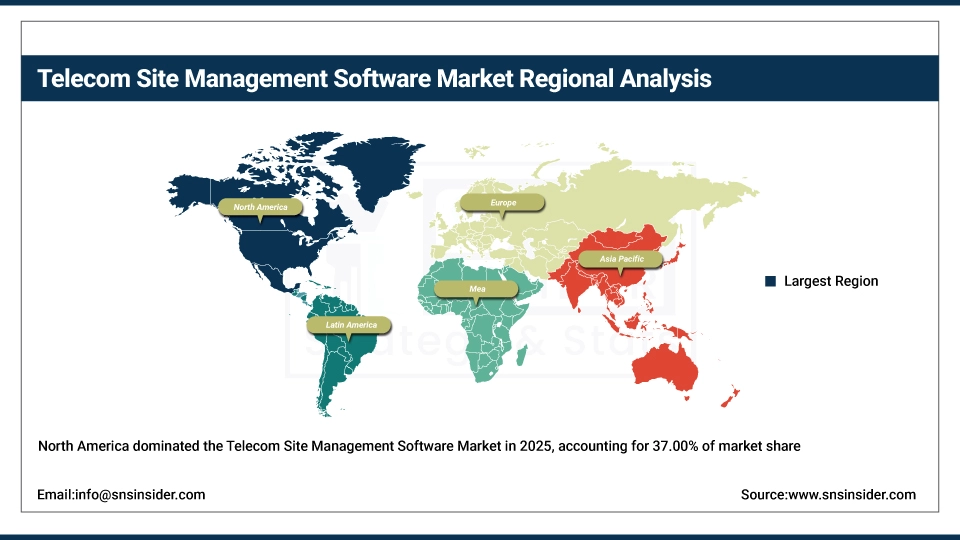

North America dominated the Telecom Site Management Software Market with a 37.00% share in 2025 due to the presence of advanced telecom infrastructure, high adoption of network optimization tools, and strong presence of leading software providers. Continuous investments in 5G deployment, IoT integration, and automated site management solutions further reinforced regional dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Telecom Site Management Software Market Insights

Asia Pacific is expected to grow at the fastest CAGR of about 12.32% from 2026–2033, driven by rapid expansion of mobile networks, increasing 4G/5G adoption, and growing investments in telecom infrastructure. Rising demand for efficient site management, network optimization, and cloud-based solutions, along with supportive government initiatives, accelerates software adoption across the region.

Europe Telecom Site Management Software Market Insights

Europe holds a strong position in the Telecom Site Management Software Market due to its mature telecom ecosystem, widespread 5G rollout, and rapid adoption of automation technologies across network operations. The region benefits from strict regulatory frameworks that encourage infrastructure modernization, energy-efficient site management, and enhanced monitoring capabilities. Strong investments from major telecom operators further support steady growth in software deployment.

Middle East & Africa and Latin America Telecom Site Management Software Market Insights

Middle East & Africa and Latin America together show steady growth, driven by expanding mobile subscriber bases, increasing telecom tower installations, and rising interest in digitizing network operations. Both regions are investing in improving connectivity, enhancing site reliability, and reducing operational costs. Growing 4G penetration, early 5G initiatives, and modernization of legacy infrastructure are pushing operators to adopt telecom site management solutions for improved visibility and performance.

Telecom Site Management Software Market Competitive Landscape:

Accruent

Accruent is a leading provider of asset, facilities, and site management software, offering solutions that help telecom operators manage tower assets, site infrastructure, maintenance, and compliance. Its platform enhances visibility, operational efficiency, and lifecycle management across distributed telecom sites. With powerful analytics, automation, and real-time monitoring, Accruent enables operators to optimize workflows, reduce downtime, and control costs. The company serves global telecom enterprises by integrating site data, improving collaboration, and ensuring consistent network performance.

-

2024, Accruent launched the AssetWorks Telecom Site Suite, a unified platform for managing passive and active telecom infrastructure across towers, rooftops, and small cells.

Tarantula

Tarantula is a specialized telecom site management software provider known for its tower-industry-focused platform used by towercos and mobile network operators worldwide. The software supports site lifecycle management, asset tracking, tenancy management, billing, compliance, and workflow automation. Tarantula helps organizations manage large tower portfolios with accuracy, ensuring transparency and operational efficiency. Its configurable modules, reporting tools, and integration capabilities enable better decision-making, revenue optimization, and seamless coordination between site owners, operators, and field teams.

-

2023, Tarantula introduced Helix, a next-generation network rollout and site management platform optimized for fiber broadband and 5G densification; AI-powered forecasting of build timelines based on permit approvals, weather, and resource availability

Sitetracker

Sitetracker is a globally recognized project and asset management platform widely used in the telecom sector for managing tower rollouts, 5G deployments, fiber projects, and site operations. Known for its cloud-based architecture, Sitetracker provides real-time visibility, workflow automation, document control, and predictive analytics to streamline complex telecom infrastructure programs. The platform improves productivity, reduces project delays, and enhances collaboration across stakeholders. Its scalability and intuitive interface make it a preferred solution for telecom operators, tower companies, and infrastructure service providers.

-

2025, Sitetracker launched Velocity, a purpose-built module for high-volume, rapid deployment of 5G small cells and DAS (Distributed Antenna Systems) in urban environments.

Telecom Site Management Software Market Key Players

Some of the Telecom Site Management Software Market Companies

-

Accruent

-

Tarantula

-

Sitetracker

-

IT‑Development

-

IFS

-

RSG Telecom

-

FieldEx

-

Praxedo

-

WorkOtter

-

Epicflow

-

Rakuten Symphony

-

Tehayu

-

Smartsheet

-

Etaprise

-

Asentria

-

Cisco Systems

-

IBM Corporation

-

Nokia Corporation

-

Hewlett Packard Enterprise

-

Mavenir Systems

|

Report Attributes |

Details |

|---|---|

|

Market Size in 2025E |

USD 361.60 Million |

|

Market Size by 2033 |

USD 798.48 Million |

|

CAGR |

CAGR of 10.36% From 2026 to 2033 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2033 |

|

Historical Data |

2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Component (Software, Services, Professional Services, Managed Services, Consulting & Integration Services) |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

|

Company Profiles |

Accruent, Tarantula, Sitetracker, IT‑Development, IFS, RSG Telecom, FieldEx, Praxedo, WorkOtter, Epicflow, Rakuten Symphony, Tehayu, Smartsheet, Etaprise, Asentria, plus additional relevant software/telecom players like Cisco Systems, IBM Corporation, Nokia Corporation, and Hewlett Packard Enterprise |

Frequently Asked Questions

North America dominated with a 37.00% share in 2025, driven by advanced telecom infrastructure, strong 5G investments, and high adoption of IoT- and AI-enabled site management solutions.

The Software segment dominated, accounting for 42.5% share, due to high adoption of centralized platforms for asset tracking, monitoring, workflow automation, and multi-vendor network integration.

Major growth is driven by rapid 4G/5G expansion, rising telecom tower density, increasing demand for remote monitoring, predictive maintenance, and energy optimization tools to reduce operational costs and enhance network reliability.

The market size of the Telecom Site Management Software Market in 2025 is USD 361.60 Million, supported by the global shift toward automation, real-time monitoring, and energy-efficient telecom sites.

The Telecom Site Management Software Market is expected to grow at a CAGR of 10.36% from 2026 to 2033, driven by increasing 5G deployments and rising demand for efficient remote site operations.

Get in Touch