Thin Film Material Market Report Scope & Overview

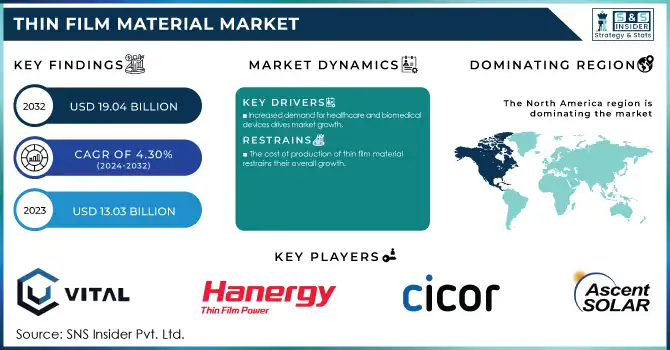

The Thin Film Material Market was USD 13.03 billion in 2023 and is expected to reach USD 19.04 billion by 2032, growing at a CAGR of 4.30% over the forecast period of 2024-2032.

Get E-PDF Sample Report on Thin Film Material Market - Request Sample Report

The thin film material market growth is increasing due to rising demand for electronics and semiconductors. The demand for electronic devices with smaller sizes, higher efficiency, and lower power dissipation is increasing, and so also is the demand for advanced materials that can facilitate these innovations. Such thin films are key to miniaturization and even identify the path toward miniaturized but higher-performing semiconductors, sensors, and displays. As an example, integrated circuits that drive modern electronic devices from smartphones, and computers to wearables, are manufactured based on thin film materials. Moreover, TFTs are also used in the creation of flat-panel displays and touchscreens. Additionally, in semiconductor fabrication, thin films are utilized in multiple deposition processes to form the precise and complex layers essential for contemporary microchips. In addition, as consumer need continues to grow for smaller, faster, and more energy-efficient electronic devices, thin films will become increasingly adopted, hence they will be an integral content for further technological development in the electronics and semiconductor industry.

India's display panel market is estimated to reach USD 19 billion by 2025, reflecting the government's commitment to enhancing domestic manufacturing capabilities.

Growing demand for renewable energy markets, which is the foremost driver for the development of the thin film material market, primarily in solar energy. With the world heading towards the transition of energy, the known source of energy is increasing in demand with renewable energy technologies, specifically solar energy. These thin film materials are essential in the research of thin film solar cells, which are increasingly preferred due to their lightweight, flexible, and less expensive nature than silicon-based solar panels. Because thin film solar panels can be embedded into various surfaces, they offer high versatility as they can be integrated into buildings, vehicles, and even wearables. The international movement towards lower carbon emissions and improved energy efficiency is providing thin film solar technology with large-scale investments due to its relatively low cost per watt and easier installation.

The government has set an ambitious target to achieve 500 GW of non-fossil fuel-based electricity generation capacity by 2030, underscoring the nation's dedication to sustainable energy.

Thin Film Material Market Dynamics

Drivers

-

Increased demand for healthcare and biomedical devices drives market growth.

Rising requirements for healthcare and biomedical devices such as diagnostic equipment, implants, and medical sensors are one of the major factors driving the growth of the global thin film material market. As worldwide healthcare demands increase, particularly with aging societies and burgeoning chronic illness, advanced medical technologies are increasingly needed. Functional layers formed by thin films are among the most important features of a broad range of biomedical devices. Healthcare devices use thin films to manufacture flexible, lightweight, and compact sensors used to detect health conditions in real-time. As an example, there are many applications of thin film materials in biosensor-based glucose monitoring, wearable medical devices, and diagnostic imaging tools that incorporate them to improve their performance, reduce size, or improve durability. Furthermore, in the case of implants what is needed is a coating which helps for the biocompatibility and enhances the life of the devices such as pacemakers and prosthetics, where the thin films are helped as a coating.

Restraint

-

The cost of production of thin film material restrains their overall growth.

The high cost of production of thin film materials presents a major hindrance to their growth. However, the production process of thin films can be complicated and costly, but they do provide flexibility, lightweight properties, and high-performance capabilities. Thin film materials are typically fabricated using advanced deposition techniques like chemical vapor deposition (CVD), sputtering, or atomic layer deposition (ALD), which rely on specialized equipment, energy-intensive processes, and expensive raw materials. On top of this, the specificity demanded by thin films will increase the challenge, resulting in the need for tight control of temperature, pressure, and material composition. The above reasons lead to increased capital and operational expenditure that makes the thin film technologies higher in cost as compared to associated conventional materials.

Thin Film Material Market Segmentation

By Type

a-Si held the largest revenue share 42% in 2023. This is due to its high production-output costs, ease of fabrication, and backed with strong efficiency in some applications. Being the most commercial thin film solar cell, a-Si provides several advantages from manufacturing to the consumer level. The advantage of a-Si essentially lies in the fact that it is a cheaper thin-film material to produce, compared to say, cadmium telluride (CdTe) or copper indium gallium selenide (CIGS), making it an economically suitable choice for large-scale production, especially in the solar field. A-Si absorbs sunlight efficiently, even at low-light conditions, and can be fabricated on a flexible substrate and therefore maintains market domination. As an additional consideration, a-Si technology is developed and most manufacturers already have an efficient process for a-Si-based products, thus limiting entry barriers for new players.

By Application

Photovoltaic (PV) solar cells held the largest market share around 32% in 2023. they are widely used in renewable energy applications and the growing global emphasis on green energy production. With countries and industries working towards climate goals and reducing carbon footprints, a wide range of clean, renewable energy sources including, in particular, solar power have become more in demand. Thin film materials a technology associated with PV solar cells have many advantages over silicon-based panels, including reduced manufacturing cost, flexibility, and the ability to be integrated into a variety of surfaces for example, buildings, vehicles, and portable devices. Improvements in cost-efficient materials, including amorphous silicon (a-Si), cadmium telluride (CdTe), and copper indium gallium selenide (CIGS) have accelerated the establishment of thin-film photovoltaic (TFPV) technology, which rivals or even exceeds the performance of traditional crystalline silicon cells under some conditions.

Thin Film Material Market Regional Analysis

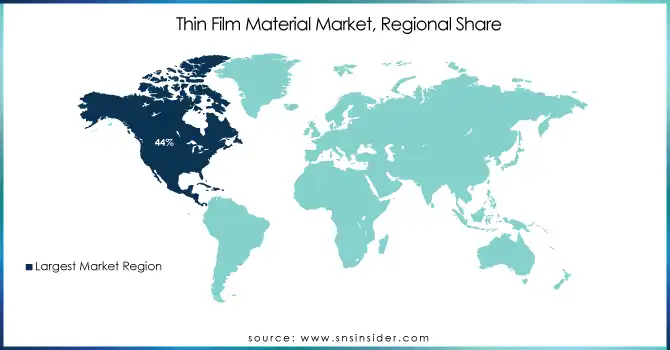

North America held the highest share of thin film material market of around 44% in 2023. It is owing to various reasons such as government stability towards renewable energy, advancement in technologies, and industrial infrastructure. For more than a decade, the U.S. and Canada have led in renewable energy adoption and in solar PV in particular, where thin film materials have a significant role. The increasing demand for thin film solar cells is also backed by government initiatives, such as tax incentives, subsidies, and renewable energy mandates, which promote rapid growth of solar energy installations. As a result of significant investments in the research and development of novel materials for solar technologies, the U.S. especially has been able to commercialize high-efficiency thin film materials such as a-Si, CdTe, and CIGS. North America is also supported by a strong manufacturing base and a high level of technological know-how, which enables the companies to manufacture thin-film materials on a large scale with premium quality and performance.

Get Customized Report as per Your Business Requirement - Request For Customized Report

Key Players

-

Ascent Solar Technologies, Inc. (USA)

-

Cicor Management AG (Switzerland)

-

Hanergy Thin Film Power Group (China)

-

Vital Materials Co. Ltd (China)

-

Indium Corporation (USA)

-

Umicore (Belgium)

-

Kyoto Thin Film Materials Institute (Japan)

-

Geomatec Co. Ltd (Japan)

-

Ferroperm Optics (Denmark)

-

JX Nippon Mining & Metals (Japan)

-

First Solar, Inc. (USA)

-

Solar Frontier K.K. (Japan)

-

SunPower Corporation (USA)

-

Sharp Corporation (Japan)

-

Canadian Solar Inc. (Canada)

-

REC Group (Norway)

-

Trina Solar Limited (China)

-

LONGi Green Energy Technology Co., Ltd. (China)

-

Q CELLS (South Korea)

-

Taiyo Yuden Co., Ltd. (Japan)

Recent Development:

-

June 2024, Geomatec Co. Ltd. (Japan) introduced an innovative thin film deposition technique that significantly reduces production costs while enhancing the overall performance of thin film materials.

-

March 2024, Indium Corporation (USA) Introduced a new line of indium-based solder materials optimized for thin film applications in the electronics industry.

-

May 2024, Umicore Expanded its research and development center to focus on sustainable materials for thin-film technologies.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 13.03 Billion |

| Market Size by 2032 | USD19.04 Billion |

| CAGR | CAGR of 4.30% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (a-Si, CdTe, and CIGS) • By End User (Electrical, MEMS, Photovoltaic Solar cells, Semiconductors, Optical coating, Other), |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Ascent Solar Technologies, Inc., Cicor Management AG, Hanergy Thin Film Power Group, Vital Materials Co. Ltd, Indium Corporation, Umicore, Kyoto Thin Film Materials Institute, Geomatec Co. Ltd, Ferroperm Optics, JX Nippon Mining & Metals, First Solar, Inc., Solar Frontier K.K., SunPower Corporation, Sharp Corporation, Canadian Solar Inc., REC Group, Trina Solar Limited, LONGi Green Energy Technology Co., Ltd., Q CELLS, Taiyo Yuden Co., Ltd. |

| Key Drivers | • Increased demand for healthcare and biomedical devices drives market growth. |

| Restraints | • The cost of production of thin film material restrains their overall growth. |

Frequently Asked Questions

Increased demand for healthcare and biomedical devices drives market growth.

The North America led the Thin Film Material Market in the region with the highest revenue share in 2023.

The automotive & transportation application will grow rapidly in the Thin Film Material Market from 2024-2032.

The expected CAGR of the global Thin Film Material Market during the forecast period is 4.30%.

The Thin Film Material Market was valued at USD 4.9 Billion in 2023.

Get in Touch