Tile Adhesives & Stone Adhesives Market Report Scope & Overview:

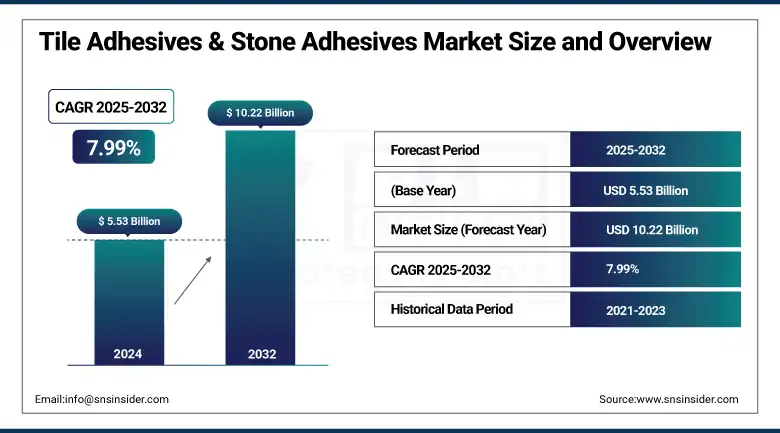

The tile adhesives & stone adhesives market size was valued at USD 5.53 billion in 2024 and is expected to reach USD 10.22 billion by 2032, growing at a CAGR of 7.99% over the forecast period of 2025-2032.

The tile adhesives & stone adhesives market is witnessing notable momentum on account of rapid urban infrastructure development, escalating home remodeling trends, and rising inclination toward big tiles. Eco-friendly adhesives are in high demand due to sustainable construction, and tile adhesives & stone adhesives such as Ardex and LATICRETE are at the forefront, with innovations designed to be ultra-low-VOC. Polymer-enhanced solutions, along with smart application systems, are revamping the tile adhesives & stone adhesives market trends. Additionally, increasing the modular housing and smart interiors trend in the market is projected to drive the tile and marble adhesives market.

To Get more information On Tile Adhesives & Stone Adhesives Market - Request Free Sample Report

The U.S. Geological Survey also reported that the consumption of tile increased in 2023, thereby solidifying tile adhesives & stone adhesives market growth. Saint-Gobain Weber extended capacity in India, suggesting changes in the tile adhesives & stone adhesives market share. Pidilite Industries pushed up its R&D spend to improve its product. These are some of the developments that are favouring ongoing tile adhesives & stone adhesives market analysis that will be shaping the market in the long run, which in turn is indicating a change for the better happening in the market.

Market Dynamics

Drivers

-

Accelerated Home Renovation Spending Stimulates Market Demand

The strong investments in home renovations are a considerable factor influencing the growth of the tile adhesives & stone adhesives market.

For instance, U.S. home improvement spending surpassed $567 billion in 2022, according to data compiled by Harvard's Joint Center for Housing Studies.

Homeowners are increasingly focused on modern interiors, along with wanting their finishes to last, which is driving demand for premium adhesives. Increasing inclination towards remote work enhances residential renovations and will increase the tile adhesives industry size. As a result, tile adhesives & stone adhesives manufacturers are coming with simple-to-use and high-performance products in the market. Therefore, this growing trend, observed particularly in North America and Europe, augments the market analysis due to the increasing demand for ready-to-use and quick-curing solutions.

-

Increasing Adoption of Large-Format and Heavy-Duty Tiles Elevates Adhesive Technology Needs

The growth of large-format tiles fosters innovation throughout the tile stone adhesive market. Such tiles need very high grab and peel-resistant adhesives. Formulations with polymers are required for tile sizes greater than 5×10 ft. Manufacturers of tile adhesives & stone adhesives are providing specialty products for these formats. The trends in the tile adhesives & stone adhesives market are also dependent on the way structures are designed and built, as architects prefer sleek aesthetics. The increasing penetration of luxury commercial and residential buildings illustrates an evolving landscape of the market share and presents new ventures for manufacturers of sophisticated tile-setting materials.

Restraints

-

Complex Installation Requirements Limit Market Penetration Among Smaller Contractors

As tile installations become more technically complex, this is an increasingly tough hurdle to overcome for smaller contractors. Various installation standards have been established by the Tile Council of North America, and non-adherence to these will result in adhesive failure. More complicated products for large-format tiles, underfloor heating, and resin materials need expertise in application. Most independent installers do not have the proper training or certifications. This hampers the usage, thereby affecting the market size. It means tile adhesives & stone adhesives companies will need to invest in educational tools and programs that work to broaden installer skill-set along with these other flow-on benefits such as more consistent application and access to new market potential for untapped contractor segments in urban and rural markets.

-

Volatile Raw Material Price Fluctuations Pressure Adhesive Manufacturers’ Profitability

The tile adhesives & stone adhesives market is impacted by the price instability of raw materials. Important inputs such as epoxy resins, polymers and cement scale with global supply chain interruptions and energy price changes.

According to BLS, by Nov 2024, the U.S. Producer Price Index had risen by 3% from a year earlier. This volatility affects the difference between selling price and cost, which urges tile adhesives & stone adhesives companies to raise prices or absorb costs.

Tile adhesives & stone adhesives market share are project sensitive, and in case if they deem that the cost is higher, they would opt for cheaper alternatives thereby, impacting market growth. Additionally, input costs lead to uncertainty, which in turn hinders long-term planning and consistency of product, thus limiting growth prospects for the market.

Segmentation Analysis

By Chemistry

Cementitious adhesives dominated the market and accounted for about 61% market share in 2024. Cementitious formulations remain the workhorse of the tile adhesives & stone adhesives market due to their cost-effectiveness, versatility across ceramic and porcelain substrates, and full compliance with ANSI A118.1 standards promoted by the Tile Council of North America. Their steady application through the range of temperatures and the easy use are part of the reason these have been the go-to amongst tile adhesives & stone adhesives industries, confirming it’s longevity on residential and commercial jobs, where the flat-laying hydration dominates.

Epoxy adhesives emerged as the fastest growing segment with a CAGR of 9.5% in the forecast period of 2025 to 2032, fueled by 100% solids high-performance resins. The need for chemically resistant, non-permeable bonding in humid environments in areas such as commercial kitchens, laboratories, and healthcare has driven development within the tile and marble adhesives industry. Manufacturers such as LATICRETE and ARDEX unveiled high-performance epoxy-based products with fast cure times and exceptional adhesion. This is a part of the larger movement towards special adhesives with excellent hygiene and durability for the stronger market growth of tile adhesives and stone adhesives.

By Construction Type

New construction dominated with 63% of the market, driven by new housing starts in the United States, which had 1,029,000 single-family completions as of March 2025, according to the U.S. Census Bureau. The rise in new residential and commercial construction projects has driven demand for high-performance adhesives that provide long-lasting strength. In this category, the new residential ground-up construction was the major shareholder because of the strong builder confidence and promotion activity for the energy efficient construction, making new construction’s tile adhesives & stone adhesives market share in the lead.

Repairs & Renovation is projected to have the fastest growth in the market by 2024. These included spending on home improvement, which rose to $567 billion in 2022, 24 percent more than in 2019, the Harvard Joint Center for Housing Studies found. Fast-setting, easy-to-use, high-performance adhesive is the preferred for DIY and professional ceramic jobs. Tile adhesives & stone adhesives manufacturers responded with specialized renovation grade products that have extended open times and better bond strengths to aged substrates, due to a trend towards refurbishment over new build, with new home builds becoming very expensive.

By End-use

The residential segment dominated, accounting for over 53% of the market share in 2024, mainly due to the single-family place’s installation.

According to the U.S. Census Bureau announced 1.44 million privately-owned housing units were authorized in June 2023, illustrating strong residential construction.

The continual rise in homeowners’ demand for high-end tile finishes in kitchens and bathrooms has long pushed the needle in the tile adhesives market, as cementitious thin sets have generally had that one covered in terms of dependability. This preference for residential design in turn drives demand for tile adhesives and stone adhesives as formulation and aesthetics become more important for living spaces where durability is paramount.

Commercial end-use emerged as the fastest-growing segment, with the highest CAGR for the 2025-2032 period, due to the increasing renovations of retail and office spaces requiring fast-curing, high-strength adhesives.

According to U.S. Census data in February 2025, private non-residential construction spending was up by 2.9% for the 12 months ending.

The commercial sector of the tile stone adhesive market gains from construction projects that demand the least downtime while placing tight demands on performance. Companies manufacturing tile adhesives & stone adhesives are introducing fast-setting and polymer-modified products suitable for the installation of large-format tiles at high-traffic commercial spaces, underpinning rapid commercial applications.

Regional Analysis

North America is projected to be the fastest-growing region due to the rise in the overall renovation activities in residences and nonresidences during the forecast period. According to the U.S. Census Bureau, more than 1 million private housing completions were projected to be reported in Q1 2025, which would substantially affect tile adhesive demand. The U.S. commands the field with innovations from companies like LATICRETE, ARDEX Americas, and Custom-Building Products. Canada is next with investments in urban infrastructure and green buildings. The trend of tile adhesives in the market in this region includes low-emission materials (low-VOC) and stronger adhesives for large-size tiles.

Asia Pacific dominated and accounted for the major market share of 42.0%, due to rapid urbanization and government-supported housing schemes. China is the leading contributor, and its Ministry of Housing data shows more than 6 million affordable homes have been completed in 2023, helping to grow the market. Also, the Indian government has been heavily investing in urban infrastructure under the Smart Cities Mission, which has led to higher consumption of tiles in the public as well as private projects. In addition, tourism-related development is booming in Southeast Asia, particularly Vietnam and Indonesia. Local firms are benefiting from moisture-resistant, quick-setting adhesives targeting tropical and high-humidity areas.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe, with a 12.9% share of the tile adhesives & stone adhesives market, is driven by stringent environment regulations and the development of green construction materials. Germany is a frontrunner in the region in the adoption of eco-labeled adhesives certified by the Blue Angel program, in line with EU green objectives. Post-Brexit recovery and the U.K.’s public investment in healthcare facilities have also helped spur demand. The demand for epoxy and water-resistant adhesives for wet-area tiling is increasing in France, Spain, and Italy, marking climate-protective restorations and energy-efficient homes as a significant trend in the tile adhesives market in these countries.

The Middle East & Africa hold a significant growth for tile stone adhesive due to mega-projects including the NEOM of Saudi Arabia and the Expo 2020 developments in Dubai. Government contracts spur growth in large-format tile as Saudi Arabia keeps investing in residential and hospitality construction. Adhesives are being sought that can withstand heat and humidity, especially in South Africa and the UAE, for luxury and retail projects. There’s steady growth in Latin America, higher urbanization, and renovation work in Brazil and Mexico. Both its ceramic tiles and Mexico’s swelling demand for adhesives are being driven by labor costs and middle-class housing expectations.

Key Players

The major competitors in the market include MAPEI S.p.A., LATICRETE International, Inc., ARDEX Group, Saint-Gobain Weber, Pidilite Industries Limited, TERRACO Group, Fosroc International Limited, Custom Building Products, Norcros Adhesives, and Magicrete Building Solutions.

Recent Developments

-

In June 2024, Nuvoco Vistas launched its "Zero M" tile and stone fixing solutions, offering specialized adhesives and grouts meeting global standards, designed for diverse surfaces and construction needs.

-

In November 2024, Nuvoco introduced Zero M Tile Adhesive T5, a high-performance epoxy-polyurethane adhesive suitable for challenging substrates, offering chemical resistance and durability for interior and exterior tile applications.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 5.53 billion |

| Market Size by 2032 | USD 10.22 billion |

| CAGR | CAGR of 7.99% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Chemistry (Cementitious, Epoxy, Others) •By Construction Type (New Construction, Repairs & Renovation) •By End-use (Residential, Commercial, Institutional) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | MAPEI S.p.A., LATICRETE International, Inc., ARDEX Group, Saint-Gobain Weber, Pidilite Industries Limited, TERRACO Group, Fosroc International Limited, Custom Building Products, Norcros Adhesives, Magicrete Building Solutions |

Frequently Asked Questions

Ans: Major players in the Tile Adhesives & Stone Adhesives Market include MAPEI, LATICRETE, ARDEX, Saint-Gobain Weber, and Pidilite Industries.

Ans: Epoxy adhesives are the fastest-growing in the Tile Adhesives & Stone Adhesives Market, favored for use in healthcare and wet environments.

Ans: Cementitious adhesives dominate the Tile Adhesives & Stone Adhesives Market due to their cost-effectiveness, ease of use, and ANSI standard compliance.

Ans: The Tile Adhesives & Stone Adhesives Market is driven by urban infrastructure growth, home renovations, and increased use of large-format tiles.

Ans: The Tile Adhesives & Stone Adhesives Market was valued at USD 5.53 billion in 2024 and is projected to reach USD 10.22 billion by 2032.

Get in Touch