Thermoplastic Elastomers Market Size & Trends

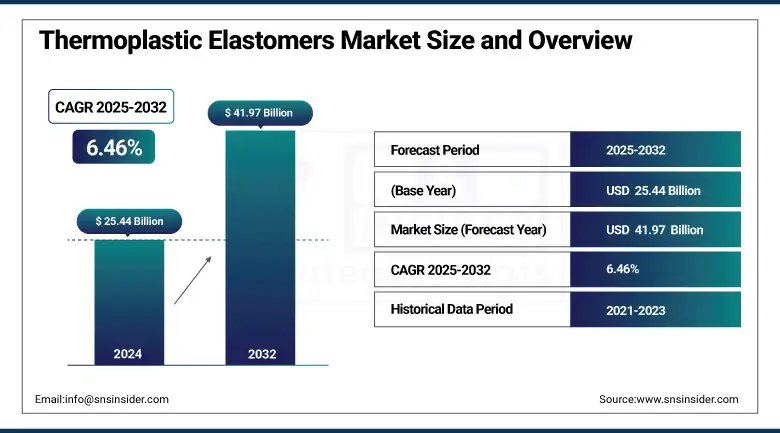

The thermoplastic elastomers market size was valued at USD 25.44 billion in 2024 and is expected to reach USD 41.97 billion by 2032, growing at a CAGR of 6.46% over the forecast period of 2025-2032.

The thermoplastic elastomers market analysis, one of the main markets driving demand for lightweight and fuel-efficient components, is the transportation sector, particularly the automotive industry. Automotive manufacturers are constantly on the lookout for stable, weight-saving materials to help them meet stringent fuel economy regulations and virtually eliminate carbon emissions. Thermoplastic elastomers (TPEs) answer to this demand very well, replacing denser conventional materials like metal and thermoset rubber in many car parts, from bumpers and seals to gaskets, interior trims, and under-the-hood parts. These things also make them very peculiar for the automotive design concerning EV and hybrid vehicles, where keeping weight to a minimum is a key factor as well, given their flexibility, recyclability, and ease of processing. This increasing dependence on TPEs for automotive applications is driving the thermoplastic elastomers market growth.

As per the U.S. Department of Energy, a reduction of 10% in the vehicle weight provides a fuel economy improvement of 6–8%. Additionally, DOE analysis also suggests a 10 percent reduction in weight using lightweight materials on one-quarter of the U.S. vehicle fleet could lead to more than 5 billion gallons of fuel savings by 2030.

Thermoplastic Elastomers Market Size and Forecast:

-

Market Size in 2024: USD 25.44 Billion

-

Market Size by 2032: USD 41.97 Billion

-

CAGR: 6.46% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2022–2023

To Get more information On Thermoplastic Elastomers Market - Request Free Sample Report

Thermoplastic Elastomers Market Trends:

-

Increasing adoption of lightweight TPE materials in automotive and EV manufacturing

-

Rising demand for medical-grade, latex-free, and sterilizable TPEs in healthcare applications

-

Growing shift toward bio-based and recyclable thermoplastic elastomers to support sustainability goals

-

Expanding use of TPEs in building & construction for weather-resistant and low-VOC applications

-

Rapid advancements in TPU and SBC materials for high-performance industrial and consumer products

-

Capacity expansions and strategic partnerships among key manufacturers to meet rising global demand

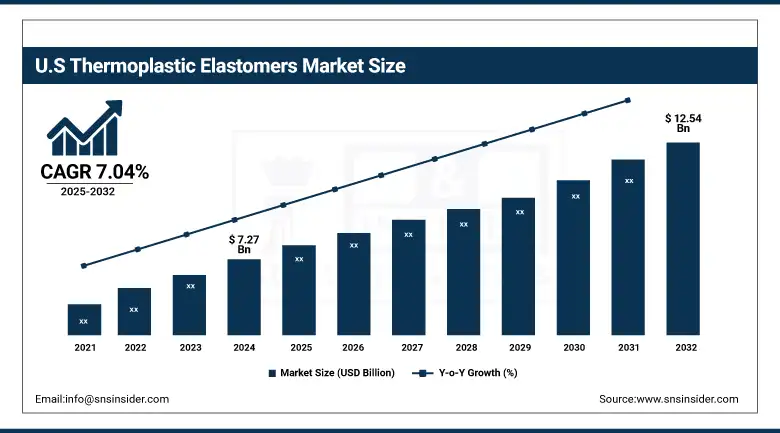

The U.S. thermoplastic elastomers market size was USD 7.27 billion in 2024 and is expected to reach USD 12.54 billion by 2032 and grow at a CAGR of 7.04% over the forecast period of 2025-2032. The consumption of TPE in the country is one of the major factors driving the regional growth, as it informs the lightweight and high-performance materials required for automotive, medical, and consumer applications. Since the U.S. is a cradle for most innovation worldwide, the majority of TPE innovations and patents originate from U.S.-based companies. Demand is also being stoked by growing adoption in electric vehicles, consumer electronics, and 3D printing. In addition, manufacturers are shifting from LSRs to TPEs to make the manufacturing process much more eco-friendly as they are now being encouraged by government fuel-efficiency standards and various sustainability initiatives.

Thermoplastic Elastomers Market Drivers

-

Increasing Use of TPEs in Medical Devices and Healthcare Applications Drives the Market Growth

Thermoplastic elastomers are being increasingly used in the healthcare sector as they possess good flexibility, great chemical resistance, and sterilizable properties. TPEs are also latex-free and phthalate-free compared to traditional rubber, so they hold less potential to trigger allergic reactions, allowing for their use in more sensitive products. They have many applications in terms of medical tubing, catheters, syringe tips, masks, IV components, and seals. The 3D printing industry is evolving with the increasing use of single-use, as well as disposable and wearable medical devices (primarily in diagnostics and chronic disease management), which is driving demand for safe, compliant, and high-performance materials. Additionally, ageing populations and global healthcare infrastructure development are expanding the scope of TPEs in the medical product manufacturing.

In March 2024, Teknor Apex expanded its U.S. Medalist medical-grade TPE line to meet the increasing need for soft-touch, latex-free alternatives in medical tubing and connected healthcare devices. This expansion provides compliance with FDA and ISO 10993 requirements.

Thermoplastic Elastomers Market Restrain

-

Fluctuations in Raw Material Prices May Hamper the Market Growth

One of the most considerable challenges in the TPE market is the fluctuating absolute costs of petrochemical-based feedstocks like styrene, olefins, and urethane precursors. TPE manufacturing has a high dependency on oil and gas markets; therefore, crude oil supply disruption caused by geopolitical instability, trade restrictions, or energy policy changes can have an instantaneous impact on raw material costs. Such fluctuations not only pressure profit margins for manufacturers but also downstream automotive, electronics, and consumer goods pricing. Additionally, fossil-fuel-derived feedstocks are facing growing suspicion on sustainability grounds, rendering the supply chain more vulnerable to environmental regulations and the market.

Thermoplastic Elastomers Market Opportunities

-

Rising Demand for Sustainable and Bio-Based TPEs Creates an Opportunity in the Market

Increased focus on sustainability and environmentally friendly product development is opening up growth avenues for bio-based and recyclable thermoplastic elastomers. With origins in renewable resources such as plant oils or starches, these materials also typically have a lower carbon footprint. Bio-based TPEs are becoming popular for automotive interiors, consumer packaging, footwear, and medical products as industries move towards circular economy models. Moreover, brands are facing pressure to comply with environmental regulations, RoHS, REACH, and low VOC, which promote green alternatives. There is ongoing R&D in this space, focused on better mechanical performance, lower cost, and being compatible with current molding technologies, which drive the thermoplastic elastomers market trends.

Arkema, in 2023, widened its output of biobased thermoplastic elastomers (TPEs) with Pebax Rnew made with castor oil derivatives at its French plant. These environmentally friendly elastomers are now also found in sports gear, medical tubing, and automotive interiors with lifecycle emission reductions of more than 30% versus petroleum-based TPEs.

Thermoplastic Elastomers Market Segmentation Analysis

By Type

Styrenic block copolymer held the largest thermoplastic elastomers market share, around 32%, in 2024. This is because of its versatility, simplicity of processing, and cost-effectiveness over a wide range of applications. SBCs offer unrivaled elasticity, flexibility, and clarity, which makes them suitable for packaging films, adhesives, sealants, footwear, and personal care applications. They enhance sustainable production by mimicking rubber-like properties, but thermoplastic ally processable, using less energy than shaping rubber or solidifying it to manufacture. On top of that, SBCs are generally utilized in medical and consumer goods due to their soft nature, biocompatibility, and low toxicity. The recyclability and versatility of the material in a variety of compounding methods make them unrivaled in the market for high-volume consumer applications requiring efficient, cost-balanced performance.

Thermoplastic Polyurethane held a significant thermoplastic elastomers market share. It is owing to its excellent combination of mechanical strength, abrasion resistance and elasticity. The TPU is medium-transparent, durable, and resistant to oil, chemicals, and both high and low-temperature extremes in a very broad and extensive range of high-performance applications including automotive, electronics, industrial tools, footwear, and medical devices. Processed via injection molding, extrusion, or 3D printing, the polymer gives manufacturers versatility in design and production. TPU also combines well with more recyclable systems and it also has a good use in flexible electronics and wearable technology, making it more modern for the tech-driven market.

By End Use

The automotive segment held the largest market share, around 28%, in 2024. It is owing to the continuous transformation of the industry towards lightweight, durable, and recyclable materials. Because of their versatility and durability, coupled with heat and chemical resistance, TPEs are widely used in automotive interiors, exteriors, and under-the-hood and other components. They play a major role in reducing vehicle weight (and cost), improving fuel economy, and helping manufacturers meet stringent emission norms by replacing conventional rubber and metal components. TPE usage includes wire and cable jacketing, seals and gaskets, and vibration-damping components in electric and hybrid vehicles, providing noise reduction and energy savings.

Building & Construction holds a significant market share in the thermoplastic elastomers market. It is due to the increasing demand for flexible, durable, and weather-resistant materials across modern infrastructure projects. Owing to their superior elasticity, UV resistance, and thermal stability, TPEs are commonly used in waterproof membranes, expansion joints, sealants, adhesives, roofing elements, and flooring systems. This unique characteristic of maintaining performance through changing environmental conditions makes them the ultimate solution for both residential and commercial construction. In addition, the increased awareness of sustainable building practices and green construction has led to accelerated penetration of recyclable and low-VOC TPE compounds consumption.

Thermoplastic Elastomers Market Regional Insights

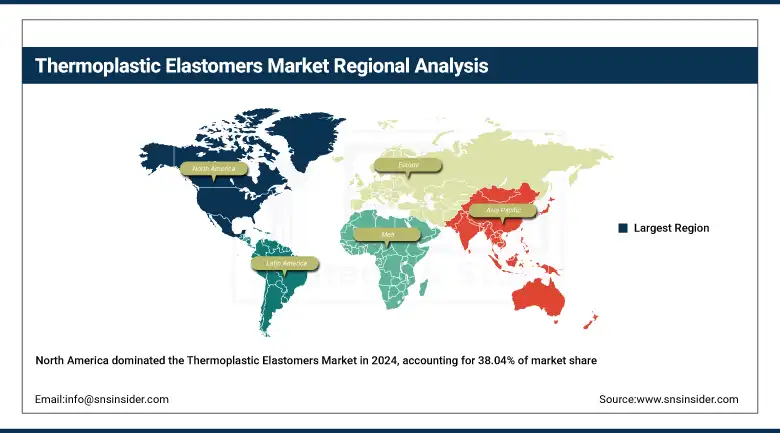

North America held the largest market share of thermoplastic elastomers market, around 38.04%, in 2024. It is owing to the mature manufacturing ecosystem, well-established automotive and healthcare sectors, and dynamic material science innovations. Stringent energy efficiency norms and lightweight materials demand from key end-use industries such as automotive and packaging boost market growth in the region. The country is majorly dominating the region, and loads the market revenue organic pipeline comprising global TPE manufacturers and good R&D capabilities. Applications of TPEs in durable consumer goods, electronics, and infrastructure projects are still growing.

Get Customized Report as per Your Business Requirement - Enquiry Now

In August 2023, LyondellBasell announced a 30% capacity expansion for TPE production at its La Porte, Texas, plant to cater to the growing demand from medical and industrial packaging sectors.

In 2024, more U.S. automotive OEMs will apply TPE for EV components, including interior trims and under-the-hood parts, to meet fuel economy standards and minimize complete vehicle mass.

Asia Pacific thermoplastic elastomers market held a significant market share and is the fastest-growing segment in the forecast period. It is due to the growing automotive production in the Asia Pacific region, along with rapid urban infrastructure development and increasing electronics and footwear industry, has propelled thermoplastic elastomers in this region, making it the fastest growing market for thermoplastic elastomers. Notably, China, India, Japan, and South Korea drive the progress, with China dominating thanks to a massive manufacturing industry and supportive government policies encouraging sustainable lightweight materials. Furthermore, low raw material prices and labor costs play a significant role in increasing the efficiency of TPE production in this region. The growth of the market is also supported by increasing consumer demand for high-performance and environmentally friendly products.

In November 2023, Kraton Corporation introduced a new G2100 series in Asia, focusing on the automotive and electronics industries, with heat resistance and durability improvements in Styrenic Block Copolymers (SBCs).

Europe held a significant market share in the forecast period. It is owing to stringent environmental regulations, a mature automotive market, and increasing medical applications. Germany, France, and Italy are in particular the main consumer countries for ceramics in the automotive and healthcare industries. Increasing cry of circular economy, and lower carbon footprint, both at the local and global level, are bringing newer recyclable, and bio-based thermoplastic elastomers into wider acceptance among producing nations, mostly in the EU. In addition, an increase in the geriatric population throughout the region is supporting the demand for medical-grade TPE from low blood pressure controlling devices, such as tubing, catheters, and wearables.

In 2023, German pharmaceutical manufacturers initiated the utilization of pheno-based TPE compounds in medical production lines due to changes in EU sustainability targets and an increase in performance features from product lines.

Thermoplastic Elastomers Market Key Players

-

BASF SE

-

Arkema S.A.

-

DuPont

-

Evonik Industries

-

LG Chem

-

Kraton Corporation

-

Huntsman Corporation

-

Teknor Apex Company

Recent Development in the Thermoplastic Elastomers Market

-

In April 2024, Lubrizol Corporation and Eastman Chemical joined forces to reinforce the adhesion of TPEs over-molded onto Eastman's Tritan copolyester, supporting the next generation of sustainable, performance-driven materials.

-

In March 2024, Kraiburg TPE Americas announced its partnership with APTA Resinas to provide expanded distribution of TPE in Brazil and throughout South America in order to enhance local accessibility and market coverage.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 25.44 Billion |

| Market Size by 2032 | USD 41.97 Billion |

| CAGR | CAGR of 6.46% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Styrene Block Copolymer, Thermoplastic Polyurethane, Thermoplastic Polyolefin, Thermoplastic Vulcanizate, Polyether Block Amide Elastomer, and Copolyester Ether Elastomer) • By End Use (Automotive, Building & Construction, Footwear, Wires & Cables, Medical, Engineering, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | BASF SE, Arkema S.A., DuPont, Covestro AG, Evonik Industries, LG Chem, Kraton Corporation, Lubrizol Corporation, Huntsman Corporation, Teknor Apex Company |

Frequently Asked Questions

Ans: The top leading key players in the Thermoplastic Elastomers market include BASF SE, Dow Inc., Kraton Corporation, Arkema S.A., Covestro AG, Lubrizol Corporation, SABIC, Teknor Apex, Evonik Industries, and KRAIBURG TPE.

Ans: Technology is enhancing the Thermoplastic Elastomers market by enabling advanced formulations with improved durability, flexibility, and recyclability. Innovations like 3D printing, bio-based TPEs, and smart processing techniques are expanding application areas across industries.

Ans: North America currently dominates the Thermoplastic Elastomers market, while Asia Pacific is the fastest-growing region due to infrastructure investments.

Ans: Increasing Use of TPEs in Medical Devices and Healthcare Applications Drives the Market Growth.

Ans: The Thermoplastic Elastomers Market was valued at USD 25.44 billion in 2024.

Get in Touch