Trade Finance Market Report Scope & Overview:

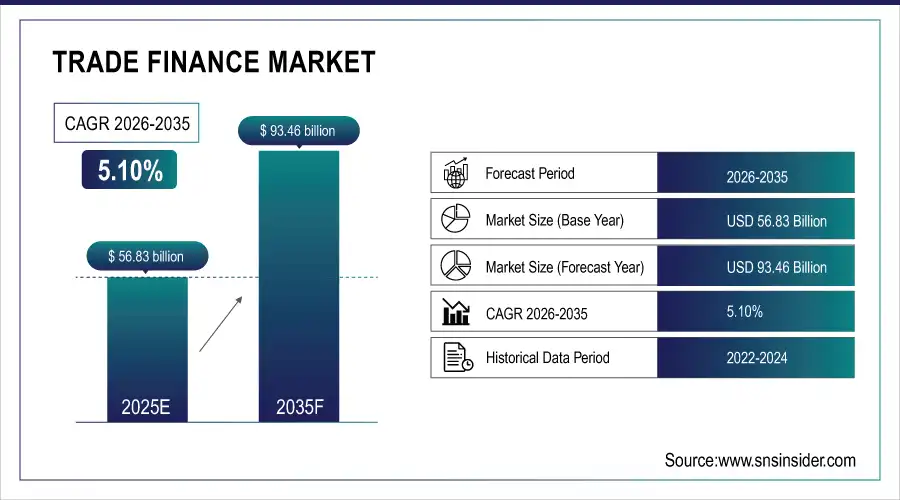

Trade Finance Market was valued at USD 56.83 billion in 2025 and is expected to reach USD 93.46 billion by 2035, growing at a CAGR of 5.10% from 2026-2035.

The growth of the Trade Finance Market is driven by increasing globalization, which has expanded cross-border trade and heightened the need for secure financing mechanisms. Rising demand for supply chain financing among SMEs and large enterprises is enhancing market activity. The adoption of digital platforms, blockchain, and automation is streamlining operations, reducing documentation errors, and accelerating transaction speeds. According to the U.S. International Trade Administration, digitization is helping SMEs streamline trade finance by improving access to working capital, lowering costs, and accelerating processes.

The U.S. Quadrennial Supply Chain Review (2025) further underscores investments in digital infrastructure, automation, and supply chain finance tools to enhance resilience against disruptions such as pandemics or trade shocks. The shift toward paperless trade and compliance with international trade regulations is further boosting efficiency, transparency, and trust, supporting the sustained growth of the trade finance ecosystem.

Trade Finance Market Size and Forecast

-

Market Size in 2025: USD 56.83 Billion

-

Market Size by 2035: USD 93.46 Billion

-

CAGR: 5.10% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Trade Finance Market - Request Free Sample Report

Trade Finance Market Trends

-

Rising global trade and cross-border transactions are driving the trade finance market.

-

Growing adoption of digital platforms, blockchain, and AI-based solutions is boosting efficiency and transparency.

-

Expansion across SMEs, large enterprises, and emerging markets is fueling market growth.

-

Increasing focus on risk mitigation, fraud prevention, and regulatory compliance is shaping adoption trends.

-

Advancements in automated document processing, smart contracts, and real-time payment tracking are enhancing operations.

-

Rising demand for working capital optimization and supply chain financing is supporting market expansion.

-

Collaborations between banks, fintechs, and trade organizations are accelerating innovation and global adoption.

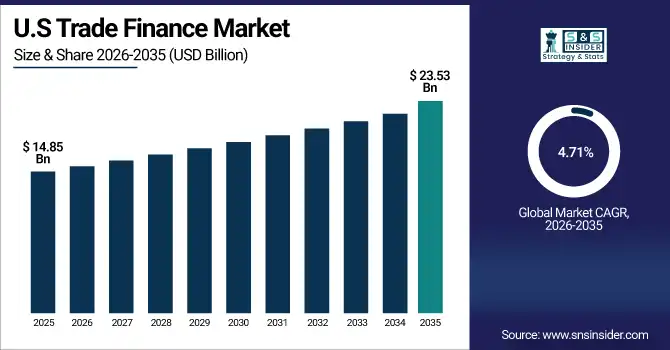

U.S. Trade Finance Market was valued at USD 14.85 billion in 2025 and is expected to reach USD 23.53 billion by 2035, growing at a CAGR of 4.71% from 2026-2035.

The U.S. Trade Finance Market is growing due to increased international trade activity, rising adoption of digital financing platforms, greater demand for supply chain financing, and enhanced regulatory frameworks that promote transparency, risk mitigation, and efficiency in trade-related financial transactions.

Trade Finance Market Growth Drivers:

-

Digital transformation and automation are accelerating trade finance operations with improved efficiency, transparency, and faster transaction processing.

Growing adoption of blockchain, AI, and cloud platforms is revolutionizing trade finance by streamlining document handling and reducing manual errors. Automation enhances speed and accuracy while cutting operational costs. This digital shift is especially vital for global trade participants seeking real-time updates, end-to-end visibility, and secure transaction tracking. Technologies like smart contracts and e-invoicing are replacing paper-based systems, minimizing fraud and compliance risks. Financial institutions are increasingly investing in digital trade platforms to meet the evolving demands of cross-border commerce and facilitate seamless financing for exporters and importers across global markets.

-

The 2024 U.S.–EU Joint Statement outlines that increasing the use of digital technologies including e‑invoicing, AI, and cloud platforms simplifies trade for SMEs, reducing regulatory friction and overall trade-related costs.

Trade Finance Market Restraints

-

Complex regulatory compliance requirements across borders hinder trade finance accessibility and increase operational costs for stakeholders.

Trade finance is heavily regulated, involving strict anti-money laundering (AML), know-your-customer (KYC), and counter-terrorism financing (CTF) protocols that vary across jurisdictions. This complexity burdens financial institutions with significant administrative tasks, often resulting in delayed processing and limited service access for SMEs. Regulatory fragmentation increases legal uncertainty, deterring new market entrants and complicating international trade flows. Moreover, evolving global sanctions and compliance audits require constant system updates, training, and legal oversight. The lack of harmonized standards across nations adds cost and inefficiency, discouraging smaller institutions from actively participating in global trade finance networks.

Trade Finance Market Opportunities

-

Integration of fintech innovations in trade finance is transforming access, speed, and risk management for global stakeholders.

Fintech firms are modernizing trade finance through digital tools like blockchain, APIs, and AI-driven credit assessments, enhancing transparency and reducing fraud. These innovations simplify onboarding, automate document verification, and lower operational costs. Collaborative ecosystems between banks and fintechs are unlocking capital access for underserved businesses. Digital marketplaces and platforms offer real-time tracking, instant payment settlement, and streamlined compliance checks. As digital trade infrastructure scales, more exporters and importers particularly SMEs can access affordable financing solutions. This digital disruption positions fintech as a strategic partner in bridging global trade finance gaps and boosting financial efficiency.

-

Over 60% of banks worldwide have implemented or are in the process of adopting digital technologies to modernize trade finance operations, including fintech tools like APIs, blockchain, and AI-based verification though only 9% have so far realized measurable cost or time savings. Meanwhile, 65% have reduced the use of paper in documentation/advising and settlement; yet 52% still rely on paper for document verification.

Trade Finance Market Challenges

-

Cybersecurity threats and digital fraud risks present growing concerns as trade finance moves toward fully digital ecosystems.

The digitization of trade finance exposes financial institutions and businesses to sophisticated cyberattacks, phishing scams, and data breaches. Given the high transaction values and sensitive documentation involved, any breach can lead to significant financial and reputational losses. Hackers increasingly target trade systems, exploiting vulnerabilities in APIs, blockchain networks, or third-party platforms. Regulatory bodies are demanding tighter cybersecurity protocols, raising compliance costs. Maintaining digital trust requires continuous investment in cybersecurity tools, employee training, and multi-layered defenses. Ensuring data integrity, identity verification, and system resilience remains an ongoing challenge in digital trade finance transformation.

Trade Finance Market Segments

By Trade

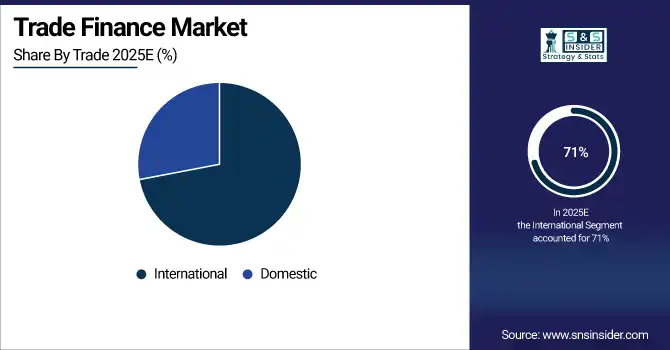

The international segment dominated the Trade Finance Market with a 71% revenue share in 2025 due to the rising complexity and volume of cross-border transactions. Global trade expansion, demand for secure payment mechanisms, and involvement of multiple currencies, jurisdictions, and intermediaries contributed to the high reliance on international trade finance services. Banks and financial institutions prioritized these transactions to mitigate credit risk and ensure timely settlement of global commerce.

The domestic segment is expected to grow at the fastest CAGR of 6.66% from 2026 to 2035, driven by the surge in intra-country trade activities and growing participation of local SMEs in supply chains. Simplified regulatory requirements and increased digitization are making domestic trade finance more accessible. Governments and financial institutions are promoting localized credit facilities to stimulate internal economic growth and strengthen the resilience of national supply networks.

By Enterprise Size

Large enterprises dominated the Trade Finance Market in 2025 with a 64% revenue share due to their frequent involvement in high-value international transactions. These firms typically have stronger credit ratings, enabling easier access to structured finance products like letters of credit and export credit. Their global presence, robust compliance mechanisms, and established relationships with financial institutions further strengthen their ability to leverage trade finance tools efficiently.

SMEs are expected to grow at the fastest CAGR of 6.16% from 2026 to 2035, as fintech-driven innovations and government support programs improve access to trade finance. Increasing integration of SMEs into global supply chains and adoption of digital platforms are enabling quicker onboarding, credit assessment, and financing. These trends are closing the historic financing gap and empowering SMEs to expand their trade activities both domestically and internationally.

By Vertical

The construction segment led the Trade Finance Market in 2025 with a 20% revenue share owing to its capital-intensive nature and long project cycles. Projects often involve multiple contractors, imports of raw materials, and high-value cross-border transactions requiring structured financing solutions. Trade finance ensures timely procurement of supplies and effective cash flow management, which is critical for meeting deadlines and minimizing risks in large-scale infrastructure and development projects.

Shipping & logistics is projected to grow at the fastest CAGR of 7.87% from 2026 to 2035 due to the sector's increasing digitization and central role in global e-commerce. As global trade grows, logistics companies need flexible, real-time financing to manage complex delivery networks. Trade finance helps optimize working capital, streamline cross-border operations, and improve inventory cycles, making it a critical enabler for growth in the highly dynamic logistics environment.

By Instrument

The letter of credit segment dominated with a 36% revenue share in 2025 due to its wide use in mitigating non-payment risks in cross-border trade. It provides a secure payment mechanism between buyers and sellers who may lack a prior relationship, especially in high-risk markets. Banks guarantee the buyer’s payment upon compliance with documentary terms, making it a preferred tool for ensuring transaction trust and financial security in global trade.

Receivables financing/invoice discounting is expected to grow at the fastest CAGR of 7.97% from 2026 to 2035 due to its increasing use among SMEs seeking faster liquidity. By converting unpaid invoices into working capital, companies can maintain cash flow and avoid credit constraints. The rise of digital platforms that automate invoice processing and risk assessment has made this financing method more accessible, efficient, and attractive across various sectors and enterprise sizes.

By Service Provider

Banks held the largest revenue share of 52% in the Trade Finance Market in 2025, supported by their global networks, capital reserves, and regulatory experience. Their long-standing relationships with traders, ability to underwrite large transactions, and robust compliance frameworks make them the preferred providers of trade finance instruments such as letters of credit and bank guarantees. Their role in enabling cross-border trust further reinforces their dominance in the sector.

Financial institutions are projected to grow at the fastest CAGR of 7.11% from 2026 to 2035, driven by increased involvement of fintechs, trade finance platforms, and non-bank lenders. These entities offer faster, more flexible, and tech-enabled solutions that appeal to SMEs and underserved markets. As traditional banks face regulatory pressure and capacity limits, alternative financial institutions are stepping in to close funding gaps and deliver innovative trade finance products.

By End Use

Importers led the Trade Finance Market with a 48% revenue share in 2025, owing to their need to manage payment risk, currency exposure, and supplier relationships in international procurement. Importers rely on trade finance tools such as letters of credit and import loans to ensure timely goods delivery and to optimize working capital. Their dependency on overseas sourcing and complex logistics makes trade finance critical to operational efficiency.

Trade intermediaries are expected to grow at the fastest CAGR of 8.01% from 2026 to 2035, as they play a crucial role in facilitating global commerce for multiple parties. These intermediaries such as agents, brokers, and third-party logistics providers increasingly use trade finance to manage risk, secure inventory, and coordinate international transactions. Digitization and platform-based trade models are further enhancing their ability to access, utilize, and scale financing solutions effectively.

Trade Finance Market Regional Analysis

North America Trade Finance Market Insights

North America dominated the Trade Finance Market with a 37% revenue share in 2025 due to its well-established financial infrastructure, strong presence of multinational corporations, and advanced regulatory frameworks. The region’s mature banking sector supports high volumes of cross-border trade, especially between the U.S., Canada, and Mexico. Robust technological integration and widespread adoption of digital trade finance tools further reinforced North America's leadership in facilitating secure and efficient international transactions.

Get Customized Report as per Your Business Requirement - Enquiry Now

The United States is dominating the Trade Finance Market in North America due to its strong banking infrastructure and high volume of international trade activities.

Asia Pacific Trade Finance Market Insights

Asia Pacific is expected to grow at the fastest CAGR of 6.87% from 2026 to 2035, driven by rapid economic development, export-led growth strategies, and expanding intra-regional trade. Countries like China, India, Vietnam, and Indonesia are witnessing a surge in manufacturing and global supply chain integration. Supportive government trade policies, infrastructure investments, and growing fintech ecosystems are also enhancing access to trade finance, especially for small and medium-sized enterprises in the region.

China is dominating the Trade Finance Market in Asia Pacific due to its massive export volume, manufacturing strength, and government-backed trade finance initiatives.

Europe Trade Finance Market Insights

Europe holds a significant share in the Trade Finance Market due to its strong intra-regional trade, advanced banking systems, and export-driven economies like Germany and France. Harmonized regulatory frameworks and cross-border financial integration further enhance market efficiency and growth potential.

Germany is dominating the Trade Finance Market in Europe due to its strong export-oriented economy, advanced manufacturing sector, and robust trade finance infrastructure.

Middle East & Africa and Latin America Trade Finance Market Insights

The Middle East & Africa region is witnessing growing trade finance demand due to infrastructure development and increased export activities, particularly in oil and minerals. Latin America is expanding steadily, supported by regional trade agreements, agricultural exports, and improving access to financial services.

Trade Finance Market Competitive Landscape:

Standard Chartered PLC

Standard Chartered PLC is a multinational banking and financial services company focused on Asia, Africa, and the Middle East. The bank provides trade finance, corporate banking, and sustainable financing solutions. Its strategy emphasizes integrating environmental, social, and governance (ESG) standards into trade capital deployment, supporting exporters, and promoting global sustainable trade initiatives through partnerships with international organizations like the ICC and IFC.

-

2025: Standard Chartered adopted the ICC Sustainable Trade Finance Principles, becoming the first global bank fully aligned with international sustainable trade standards.

-

2025: The bank and IFC launched a USD 400M risk participation facility for exporters in Pakistan, expanding short-term trade finance access.

-

2025: Standard Chartered arranged the world’s first syndicated sustainable trade finance guarantee exceeding USD 300M for Envision Group’s wind power equipment sales.

BNP Paribas

BNP Paribas is a leading international bank providing corporate and institutional banking, trade finance, and sustainable finance solutions. The bank emphasizes responsible banking practices and environmental stewardship across its financing portfolio. BNP Paribas actively participates in international initiatives to standardize sustainable trade finance, enabling clients to access green capital efficiently while supporting compliance with ESG and global environmental standards.

-

2025: BNP Paribas endorsed the ICC Principles for Sustainable Trade Finance, joining other global banks to advance standardized sustainable trade finance guidelines across major markets.

Citigroup Inc.

Citigroup Inc. is a global financial services leader providing trade finance, corporate banking, and digital financial solutions. Citi focuses on accelerating cross-border commerce through innovative technology, enhancing operational efficiency for exporters and importers. Its digital trade and receivables solutions aim to reduce transaction times, streamline working capital, and integrate risk management, helping multinational corporations and SMEs optimize trade finance processes.

-

2024: Citi launched the Citi Digital Bill, a digital trade receivables finance solution that reduces monetization time from weeks to under an hour, enhancing cross-border trade efficiency.

Rabobank Group

Rabobank Group is a Dutch multinational bank specializing in food and agribusiness financing, corporate banking, and sustainable trade solutions. It focuses on supporting clients with ESG-aligned finance while promoting environmental stewardship across its lending and trade portfolios. Rabobank actively engages with international frameworks to standardize sustainable trade finance, ensuring that agricultural and global trade transactions meet environmental and social responsibility benchmarks.

-

2025: Rabobank endorsed the ICC Principles for Sustainable Trade Finance, joining leading global banks to promote environmental criteria and standardized sustainable trade finance practices.

Key Players

-

Standard Chartered PLC

-

BNP Paribas

-

TD Bank

-

UBS

-

Arab Bank

-

DBS Bank Ltd

-

JPMorgan Chase & Co.

-

Santander Bank / Banco Santander S.A.

-

Deutsche Bank AG

-

Bank of America Corporation

-

HSBC Holdings plc

-

Morgan Stanley

-

Mitsubishi Corporation

-

ANZ Bank

-

Rabobank Group

-

SunTrust Bank Holding Company

-

UniCredit S.p.A

-

Wells Fargo & Company

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 56.83 Billion |

| Market Size by 2035 | USD 93.46 Billion |

| CAGR | CAGR of 5.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Instrument (Letter of Credit, Supply Chain Financing, Documentary Collections, Receivables Financing/Invoice Discounting, Others) • By Service Provider (Banks, Financial Institutions, Trading Houses, Others) • By Trade (Domestic, International) • By Enterprise Size (Large Enterprises, SMEs) • By Vertical (BFSI, Construction, Wholesale/Retail, Manufacturing, Automobile, Shipping & Logistics, Others) • By End Use (Importer, Exporter, Trade Intermediaries) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Standard Chartered PLC, BNP Paribas, Citigroup Inc., TD Bank, UBS, Arab Bank, DBS Bank Ltd, JPMorgan Chase & Co., Santander Bank / Banco Santander S.A., Deutsche Bank AG, Bank of America Corporation, HSBC Holdings plc, Commerzbank AG, Morgan Stanley, Mitsubishi Corporation, ANZ Bank, Rabobank Group, SunTrust Bank Holding Company (now Truist Financial Corporation), UniCredit S.p.A, Wells Fargo & Company |

Get in Touch