Cellular IoT Market Report Scope & Overview:

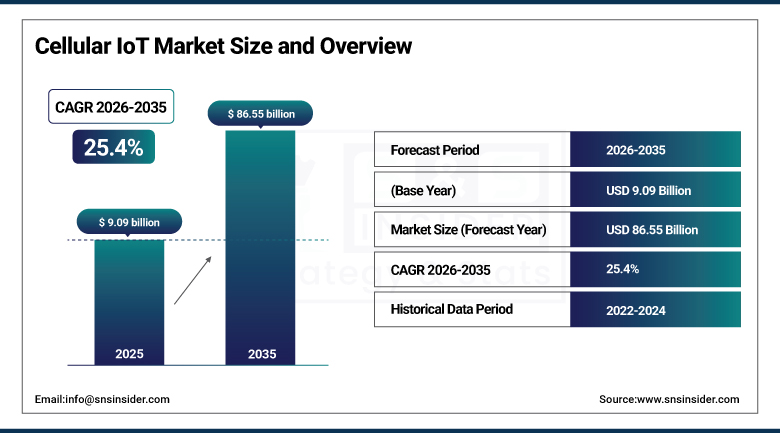

The Cellular IoT Market was valued at USD 9.09 Billion in 2025 and is expected to reach USD 86.55 Billion by 2035, growing at a CAGR of 25.4% from 2026 to 2035.

The cellular IoT market is expected to grow significantly owing to the widespread use of 5G and LPWANs that include both NB-IoT and LTE-M, as well as the introduction of edge computing solutions within businesses looking for real-time monitoring, automation, and data exchanges. Cellular IoT uses licensed spectrum cellular networks that deliver reliable and robust connectivity for IoT devices in various fields and distinguishes itself from both Wi-Fi or Bluetooth IoT in terms of wide-area coverage, carrier-grade security, and stable performance for mobility solutions. The market provides real-time monitoring, automation, and data exchange services in areas such as smart cities, health care, and automation. The government promotes the growth of this market by updating its smart grid, and the telecommunication companies promote the deployment of the NB-IoT and LTE-M networks.

In October 2024, Cisco Systems collaborated with T-Mobile to prepare for the commercial release of devices using RedCap, a 5G specification designed specifically for IoT devices including wearables and industrial sensors. RedCap offers a lower bandwidth version of 5G that provides simpler and more power-efficient connectivity than full 5G while delivering substantially better performance than NB-IoT, creating a new technology tier that bridges the gap between LPWA and broadband IoT application requirements.

Market Size and Forecast

-

Market Size in 2026E: USD 11.39 Billion

-

Market Size by 2035: USD 86.55 Billion

-

CAGR: 25.4% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Cellular IoT Market - Request Free Sample Report

Cellular IoT Market Trends

-

5G RedCap commercialization is bridging the gap between LPWA and full 5G connectivity by offering lower power consumption, reduced costs, and higher bandwidth for mid-tier IoT applications.

-

eSIM and iSIM adoption is accelerating global IoT deployments through remote provisioning, simplified connectivity management, and enhanced network flexibility.

-

Satellite-cellular hybrid connectivity is expanding IoT coverage into remote and underserved locations, enabling reliable monitoring across agriculture, maritime, and industrial sectors.

-

Private 5G network deployment is increasing in industrial environments, driven by demand for ultra-low latency, network security, and improved operational control.

-

AI-enabled IoT platforms are enhancing predictive analytics, anomaly detection, and automated decision-making capabilities across connected device ecosystems.

The U.S. Cellular IoT Market Outlook

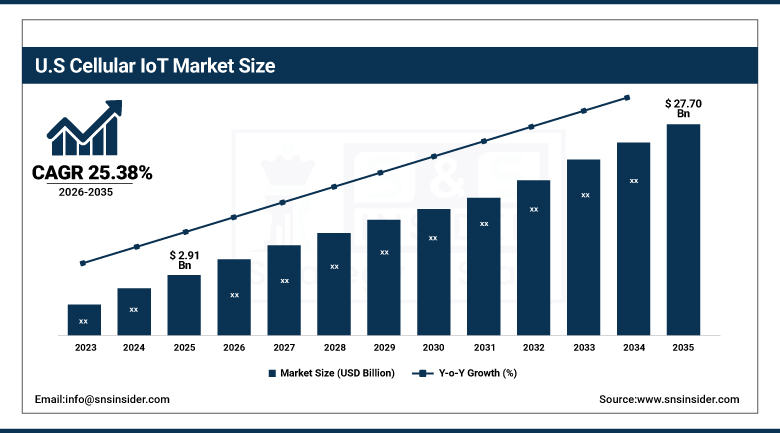

The U.S. Cellular IoT Market was valued at approximately USD 2.91 Billion in 2025 and is expected to reach approximately USD 27.70 Billion by 2035, growing at a CAGR of approximately 25.38%.

The U.S. is the most commercially innovative cellular IoT market within North America's dominant regional position. AT&T, Verizon, T-Mobile, Qualcomm, Ericsson, and Cisco collectively define the domestic cellular IoT commercial landscape. AT&T emerged as a global leader in IoT connectivity according to the 2025 Transforma Insights IoT Peer Benchmarking Report, leveraging innovations including Global SIM Advanced and IoT Console Single Pane of Glass to reduce operational complexity for enterprise IoT customers. The U.S. telecommunications carriers’ substantial 5G standalone network investment, the government's smart infrastructure funding programmes, and the manufacturing sector's Industry 4.0 adoption collectively sustain above-average cellular IoT procurement growth across the forecast period.

In June 2024, AT&T launched the first commercial 5G RedCap network in Dallas, allowing chipset vendors to certify devices on a live 5G standalone network and confirming power consumption reductions of approximately 65% compared to LTE Cat-4 modules. The launch demonstrates the commercial materialisation of 5G RedCap's IoT device efficiency promise and creates the network infrastructure foundation on which cellular IoT device manufacturers can validate and commercially launch RedCap-enabled products for wearables, industrial sensors, and other mid-tier IoT applications.

Cellular IoT Market Segment Analysis

-

By Component, the hardware segment dominated the cellular IoT market with the largest revenue share in 2025, while the software segment is the fastest growing.

-

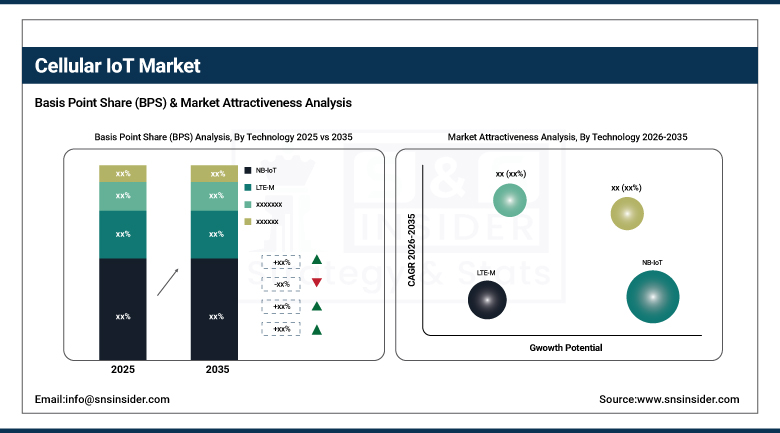

By Technology, the NB-IoT and LTE-M (Massive IoT/LPWAN) segment dominated the cellular IoT market with the largest combined revenue share in 2025, while the 5G segment is the fastest growing.

-

By Application, the smart manufacturing segment dominated the cellular IoT market with the largest revenue share in 2025, while the smart cities segment is the fastest growing.

-

By Vertical, automotive & transportation segment dominated the cellular IoT market with approximately 24.23% share in 2025, while the healthcare vertical is the fastest growing.

By Technology, NB-IoT and LTE-M dominate, 5G grows fastest

NB-IoT and LTE-M collectively retained the dominant technology position with the largest revenue share of the cellular IoT market in 2025. The LPWA technologies’ commercial primacy reflects the extraordinary volume of low-power IoT application deployments whose smart metering, asset tracking, environmental monitoring, and agricultural sensor use cases require cellular connectivity that battery-powered devices can sustain for years without charging. NB-IoT’s 36.2% market share demonstrates the technology’s role as the dominant deployed LPWA standard across smart utility metering programmes, building automation systems, and environmental monitoring networks where established operator infrastructure, low module pricing below USD 4, and decade-long device battery life create compelling deployment economics. China's NDRC guidelines in May 2024 requiring NB-IoT deployments in metering and environmental monitoring created the most commercially significant single-market LPWA mandate, sustaining NB-IoT’s leadership.

5G is the fastest growing technology because the commercial deployment of 5G standalone networks, the RedCap specification’s 65% energy efficiency improvement over LTE, and the industrial automation and autonomous vehicle application requirements whose ultra-low latency and high bandwidth demand 5G capabilities are collectively creating above-average 5G IoT module procurement growth. AT&T’s June 2024 RedCap commercial launch and Qualcomm’s September 2024 acquisition of Sequans’ 4G IoT technology portfolio demonstrate the commercial investment in 5G IoT module development that sustains the technology’s fastest-growing designation.

By Vertical, automotive dominates, healthcare grows fastest

Automotive and transportation retained the dominant vertical position with approximately 24.23% of the cellular IoT market in 2025. Connected vehicle telematics whose cellular data transmission for vehicle location, diagnostics, driving behaviour analytics, and over-the-air software update delivery creates per-vehicle recurring connectivity revenue that aggregates across global vehicle production volumes of 80 to 90 million units annually. Each new vehicle model that mandates cellular connectivity for eCall emergency response, stolen vehicle tracking, or remote diagnostics creates automotive cellular IoT hardware and connectivity procurement whose commercial aggregate grows with global vehicle production volume and connectivity feature content per vehicle. Fleet telematics deployment across commercial trucking, logistics, and public transportation creates the most commercially concentrated single-segment cellular IoT procurement within the automotive vertical.

Healthcare is the fastest growing vertical because digital health investment, remote patient monitoring adoption, and connected medical device deployment are creating above-average cellular IoT procurement growth whose regulatory compliance, patient outcome improvement, and healthcare system cost reduction motivations sustain investment independent of pure commercial ROI calculation. Each remote patient monitoring programme that connects cardiac monitoring, glucose sensing, or oxygen saturation devices through cellular creates recurring connectivity and data management service procurement. The global ageing population’s growing chronic disease management requirement creates structural demand for remote monitoring systems that sustain healthcare cellular IoT procurement growth through demographic expansion of the addressable patient population.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Cellular IoT Market Insights

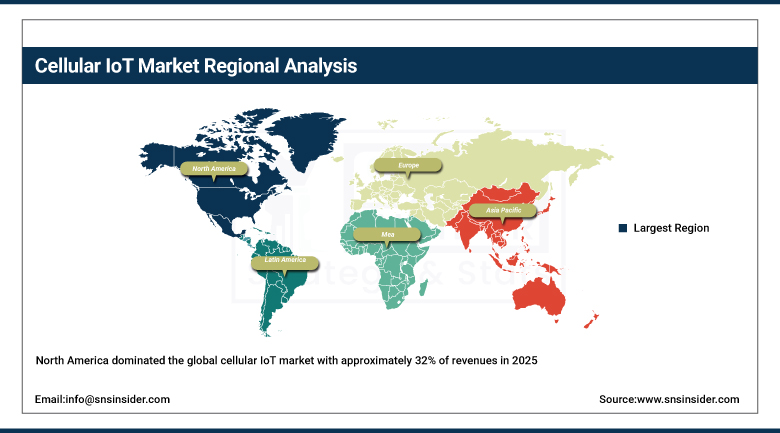

North America dominated the global cellular IoT market with approximately 32% of revenues in 2025, supported by advanced 4G and 5G network infrastructure, widespread enterprise cloud adoption, and the concentration of major cellular IoT vendors including Qualcomm, AT&T, Ericsson, and Cisco. The United States accounts for approximately 87.4% of North American revenues through its extraordinary IoT ecosystem concentration and 5G SA network investment.

Canada contributes through its telecommunications sector’s NB-IoT and LTE-M network deployment, the utilities sector’s smart metering investment, and the manufacturing sector’s cellular IoT adoption for Industry 4.0 applications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cellular IoT Market Insights

Europe is a technically sophisticated cellular IoT market where EU smart meter directives, NIS2 IoT security requirements, and the industrial automation sector’s cellular connectivity investment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its manufacturing sector’s private 5G deployment, Deutsche Telekom’s NB-IoT smart metering network, and the automotive industry’s connected vehicle platform investment.

The United Kingdom, France, and Nordics are significant secondary markets where Vodafone’s NB-IoT deployment, Ericsson’s European private 5G projects, and smart city investment across major European cities create consistent cellular IoT procurement. Ericsson’s Swedish headquarters and Nokia’s Finnish base sustain European cellular IoT technology leadership.

Asia Pacific Cellular IoT Market Insights

Asia Pacific is the fastest growing regional cellular IoT market, driven by China’s extraordinary NB-IoT deployment scale, India’s smart city investment, Japan’s industrial IoT adoption, South Korea’s 5G infrastructure, and Southeast Asia’s growing IoT ecosystem investment. China accounts for approximately 44.8% of Asia Pacific revenues through its government-mandated NB-IoT metering deployment, Huawei and Quectel’s module manufacturing dominance, and the extraordinary scale of Chinese smart city and industrial IoT programmes.

India represents the most commercially dynamic emerging market within Asia Pacific where the government’s smart cities mission, the utilities sector’s smart metering rollout, and the manufacturing sector’s Industry 4.0 investment create above-average cellular IoT procurement growth from a rapidly expanding connectivity infrastructure base.

MEA & Latin America Cellular IoT Market Insights

The UAE leads MEA revenues through its smart city investment in Dubai and Abu Dhabi, DEWA’s smart metering deployment, and the government’s advanced infrastructure digitalisation creating above-average cellular IoT procurement. Saudi Arabia’s Vision 2030 smart city investment adds substantial complementary Gulf demand. Brazil leads Latin American revenues at through its growing cellular IoT ecosystem, the utilities sector’s smart metering adoption, and the manufacturing sector’s connectivity investment. Mexico’s manufacturing sector and Colombia’s smart city programmes collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: 5G network deployment enabling new application categories and government smart infrastructure investment creating structured cellular IoT procurement

5G network deployment is the cellular IoT market’s most commercially transformative structural growth driver, creating application categories that previous cellular generations could not support. The ultra-low latency, massive device density support, and network slicing capability of 5G standalone networks enable autonomous vehicle coordination, real-time industrial control, and ultra-reliable sensor networks that 4G LTE cannot provide with adequate performance consistency. Each new 5G standalone network deployment creates a platform on which private 5G networks, RedCap device certifications, and mission-critical IoT applications can develop commercial deployments whose aggregate creates above-market revenue growth in the 5G IoT segment.

Government smart infrastructure investment through smart city programmes, smart grid modernisation, and industrial digitisation mandates creates the most commercially certain near-term cellular IoT procurement. China’s NDRC NB-IoT metering mandate, the EU’s smart meter directive, and India’s smart cities mission collectively represent public sector investment whose procurement scale sustains market growth independent of private sector adoption rate variation.

Restraints: High deployment costs for 5G IoT and spectrum availability constraints in emerging markets

High deployment costs for 5G IoT infrastructure including private 5G network capital expenditure, advanced module pricing, and integration engineering costs create adoption barriers for small enterprises and emerging market operators whose budget constraints favour lower-cost NB-IoT or LTE-M alternatives even where 5G provides superior performance. Each industrial facility whose private 5G business case cannot demonstrate sufficient ROI within acceptable payback periods creates a market segment where 5G IoT adoption is delayed relative to the technology's capability.

Spectrum availability constraints in emerging markets where cellular frequency allocations prioritised mobile broadband over dedicated IoT bands create deployment complexity that moderates LPWA network expansion pace in markets outside the major operator network investment zones. Each market where NB-IoT and LTE-M spectrum remains unallocated creates a cellular IoT deployment barrier that sustains reliance on 2G or 3G connectivity alternatives despite their inferior IoT performance and energy efficiency.

Opportunities: Satellite-cellular hybrid connectivity and AI-powered IoT platform development

Satellite-cellular hybrid IoT connectivity represents the most commercially transformative emerging opportunity whose extension of cellular IoT coverage beyond terrestrial network footprints into agricultural, maritime, offshore, and remote industrial monitoring applications creates new market categories previously un-addressable by cellular IoT solutions. Qualcomm and Skylo’s NTN chipset collaboration and Semtech’s HL7900 5G LPWA module with NTN fallback demonstrate the commercial progress of hybrid satellite-cellular that creates an addressable market substantially larger than terrestrial cellular coverage alone.

AI-powered IoT platform development whose predictive analytics, autonomous optimization, and intelligent orchestration of cellular IoT device networks creates software and services revenue above connectivity alone represents the most commercially premium cellular IoT market expansion opportunity. Each IoT platform deployment that transforms cellular connectivity data into operational intelligence creates subscription revenue whose commercial value substantially exceeds the underlying connectivity cost.

Recent Developments:

-

2025: AT&T and Thales launched a next-generation eSIM solution for IoT devices in October 2025 based on the GSMA SGP.32 standard, enabling enterprises to remotely manage large fleets of connected devices securely with improved automation and cybersecurity compliance.

-

2024: Cisco Systems collaborated with T-Mobile in October 2024 to prepare for the commercial release of 5G RedCap devices for wearables and industrial IoT sensors, validating the technology's power efficiency improvements of approximately 65% versus LTE Cat-4.

-

2024: AT&T launched the first commercial 5G RedCap network in Dallas in June 2024, allowing cellular IoT chipset vendors to certify devices on a live 5G standalone network and confirming the energy efficiency and performance characteristics of RedCap for commercial IoT deployments.

Cellular IoT Market Key Players are:

-

Qualcomm Technologies Inc.

-

Ericsson AB

-

Huawei Technologies Co. Ltd.

-

Quectel Wireless Solutions Co. Ltd.

-

Fibocom Wireless Inc.

-

AT&T Inc.

-

Verizon Communications Inc.

-

T-Mobile US Inc.

-

Cisco Systems Inc.

-

Nordic Semiconductor ASA

-

Semtech Corporation

-

Telit Cinterion

-

MediaTek Inc.

-

UNISOC (Shanghai) Technologies Co. Ltd.

-

Thales Group SA

-

Sierra Wireless (Semtech)

-

u-blox Holding AG

-

Murata Manufacturing Co. Ltd.

-

Sunsea AIoT Technology Co. Ltd.

-

Intel Corporation

Cellular IoT Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.09 Billion |

| Market Size by 2035 | USD 86.55 Billion |

| CAGR | CAGR of 25.4% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Technology (2G, 3G, 4G/LTE, LTE-M, NB-IoT, 5G) • By Application (Smart Manufacturing, Smart Cities, Smart Metering, Connected Healthcare, Asset Tracking & Fleet Management, Wearables, Others) • By Vertical (Automotive & Transportation, Healthcare, Manufacturing & Industrial, Energy & Utilities, Retail, Agriculture, Smart Cities, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Qualcomm Technologies Inc., Ericsson AB, Huawei Technologies Co. Ltd., Quectel Wireless Solutions Co. Ltd., Fibocom Wireless Inc., AT&T Inc., Verizon Communications Inc., T-Mobile US Inc., Cisco Systems Inc., Nordic Semiconductor ASA, Semtech Corporation, Telit Cinterion, MediaTek Inc., UNISOC (Shanghai) Technologies Co. Ltd., Thales Group SA, Sierra Wireless (Semtech), u-blox Holding AG, Murata Manufacturing Co. Ltd., Sunsea AIoT Technology Co. Ltd., and Intel Corporation |

Frequently Asked Questions

North America dominated the Cellular IoT Market with approximately 32% of revenues in 2025.

NB-IoT and LTE-M (Massive IoT/LPWAN technologies) collectively dominated the Cellular IoT Market in 2025.

The Cellular IoT Market is expected to grow at a CAGR of 25.4% from 2026 to 2035.

The Cellular IoT Market was valued at USD 9.09 Billion in 2025.

5G network deployment enabling new application categories including autonomous vehicles, industrial automation, and smart cities, and government smart infrastructure investment mandating cellular IoT adoption in smart metering.

Get in Touch