Skill Gaming Market Report Scope & Overview:

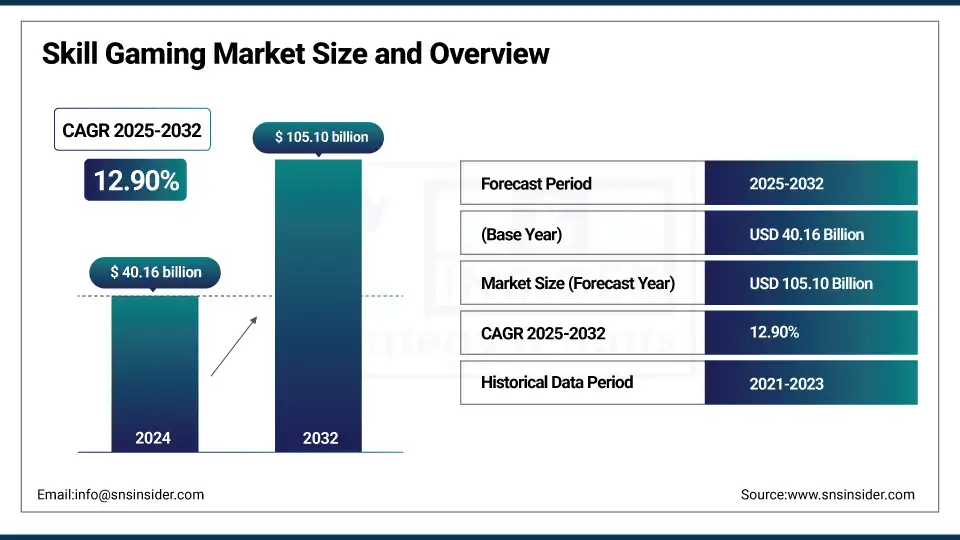

The Skill Gaming Market was valued at USD 40.16 billion in 2024 and is expected to reach USD 105.10 billion by 2032, growing at a CAGR of 12.90% from 2025-2032.

The growth of the Skill Gaming Market is driven by increasing smartphone penetration, rising internet accessibility, and growing interest in competitive and reward-based gaming. Millennials and Gen Z are actively engaging in skill-based games that offer real money or prizes, fueling demand. The integration of advanced technologies like AI, AR/VR, and blockchain enhances user experience, fairness, and transparency. Additionally, regulatory clarity in several regions and the emergence of eSports culture contribute to widespread adoption. Monetization models such as entry fees, in-game purchases, and advertising are also boosting revenue potential, attracting investors and developers to expand offerings and scale operations.

To Get more information On Skill Gaming Market - Request Free Sample Report

-

As per the American Gaming Association (AGA), of the 38 U.S. jurisdictions permitting regulated gaming, 28 reported record-breaking revenue in 2024, including newly regulated states like North Carolina and Vermont.

-

Skillz Inc. (USA), a leading skill-based gaming platform, reported managing over 2 billion tournament entries for 30 million mobile players globally, distributing more than $60 million in monthly prizes across its platform.

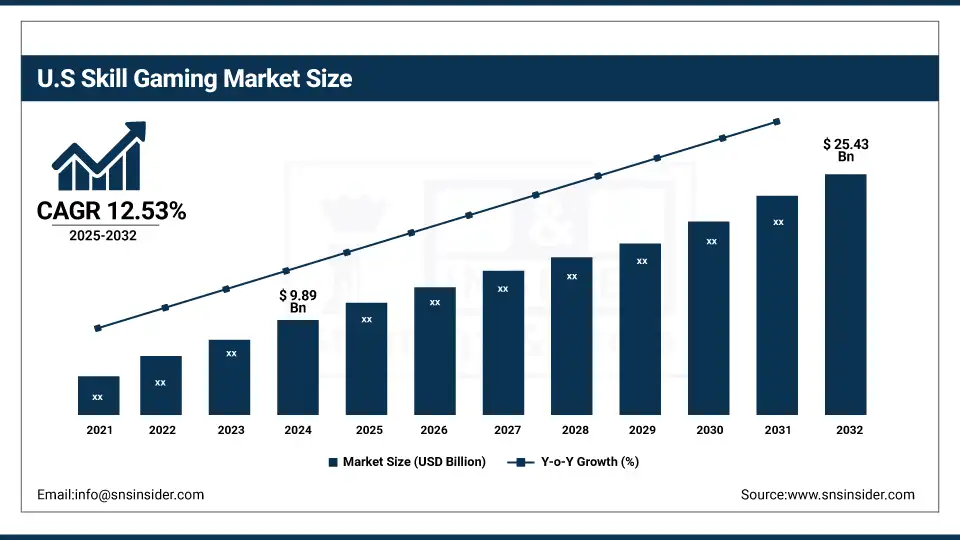

The U.S. Skill Gaming Market was valued at USD 9.89 billion in 2024 and is expected to reach USD 25.43 billion by 2032, growing at a CAGR of 12.53% from 2025-2032.

The U.S. Skill Gaming Market is growing due to increasing demand for interactive entertainment, the rise of mobile gaming, and growing acceptance of real-money skill-based competitions. Favorable legal frameworks in several states support market expansion, while technological advancements enhance gameplay and user engagement. The popularity of eSports, streaming platforms, and monetization models like entry fees and in-game rewards further contribute to the market’s robust growth trajectory.

Market Dynamics

Drivers

-

Rising smartphone penetration and internet connectivity is making skill-based gaming widely accessible to younger, mobile-first global audiences.

The rapid increase in smartphone usage and improved internet access across developing and developed regions is significantly fueling the adoption of skill-based gaming platforms. Mobile-first consumers, especially millennials and Gen Z, are actively engaging with gaming apps that offer competitive, skill-oriented experiences. This shift is allowing platforms to monetize through in-app purchases, ads, and entry fees. As the digital infrastructure matures further, rural and underpenetrated regions are becoming lucrative new markets. The growing ease of access, low-cost data, and affordable smartphones are expanding the user base for skill gaming exponentially.

Restraints

-

Ambiguity in legal and regulatory frameworks continues to hinder growth and investor confidence in skill gaming markets globally.

The lack of standardized and transparent legal definitions distinguishing skill-based gaming from gambling poses significant operational and reputational risks. Countries have inconsistent rules, with some banning real-money gaming outright, while others impose stringent licensing norms. This regulatory fragmentation deters foreign investment, creates compliance burdens, and restricts platform scalability across borders. Uncertainty over taxation, jurisdiction, and player protection laws further complicates expansion. These unresolved legal gray areas increase the risk of sudden platform shutdowns, user attrition, or legal penalties, thereby slowing overall growth momentum and innovation in the global skill gaming industry.

Opportunities

-

Integration of emerging technologies like blockchain, AI, and AR is transforming gameplay mechanics and transparency in skill gaming.

Next-generation technologies are opening up new frontiers in the skill gaming experience. Blockchain is enabling transparent prize pools and fraud-proof gameplay, building user trust in outcomes. Artificial Intelligence is personalizing gameplay, optimizing matchmaking, and detecting cheating in real time. Augmented Reality (AR) is making games more immersive, blending physical and digital environments. These innovations not only enhance user engagement but also differentiate platforms in a competitive market. Additionally, tech integration supports cross-device compatibility, driving higher usage. As consumer expectations rise, companies leveraging these technologies can capture a tech-forward audience and improve monetization.

Challenges

-

Cybersecurity threats and data privacy risks are undermining trust and operational continuity in real-money skill gaming platforms.

With sensitive user data and financial transactions at stake, skill gaming platforms are prime targets for hacking, fraud, and data breaches. Players' concerns over identity theft, rigged outcomes, or wallet tampering can damage trust and cause attrition. Furthermore, inadequate data encryption or compliance failures with privacy laws like GDPR or India’s DPDP Act expose platforms to heavy penalties. Cyber incidents not only result in financial loss but also tarnish brand reputation and invite regulatory scrutiny. Ensuring 24/7 cybersecurity, anti-fraud systems, and regulatory compliance has become a critical but challenging necessity for platforms operating at scale.

Segment Analysis

By Skill Type

Physical segment dominated the Skill Gaming Market with the highest revenue share of about 77% in 2024 due to the widespread popularity of real-money skill games involving physical reflexes and motor coordination, such as e-sports, shooting games, and action-based arcade formats. These games attract a massive user base driven by competitive dynamics, fast-paced gameplay, and audience appeal through streaming platforms, making them highly monetizable and engaging across multiple age groups.

Mental segment is expected to grow at the fastest CAGR of about 15.43% from 2025–2032 owing to increasing demand for brain-training games, trivia, and logic-based challenges among students, professionals, and older adults. Rising awareness about cognitive fitness, stress relief through mental gaming, and the growing integration of AI for personalized mental exercises are fueling adoption. Mental skill games also see strong uptake in educational and gamified learning contexts.

By Genre

Card-Based segment dominated the Skill Gaming Market with the highest revenue share of about 31% in 2024 because of the enduring popularity of traditional and digital card games like poker, rummy, and blackjack that combine strategy, probability, and user skill. These games are deeply embedded in user behavior, offer legal clarity in several regions, and facilitate real-money competition, attracting high repeat engagement and generating stable, high-value revenue streams for platforms.

Puzzle Games segment is expected to grow at the fastest CAGR of about 14.87% from 2025–2032 due to rising interest in mobile-friendly, low-bandwidth, and solo-play gaming experiences that engage users intellectually. The appeal of short, repeatable game sessions makes puzzle formats ideal for casual gamers. Enhanced personalization, mental stimulation, and the ease of in-app monetization through hints or level-unlocks are driving rapid adoption in diverse demographic segments.

By Gaming Platform

Desktop segment dominated the Skill Gaming Market with the highest revenue share of about 43% in 2024 due to the platform's superior graphics capabilities, processing power, and longstanding dominance in e-sports, card games, and PC-based competitive gaming. Desktop environments allow for more immersive gameplay, stable connectivity, and better user controls, making them the preferred choice for serious gamers and high-stakes tournaments, thereby attracting higher revenues and longer session durations.

Virtual Reality (VR) segment is expected to grow at the fastest CAGR of about 17.78% from 2025–2032 owing to increasing affordability and adoption of VR headsets, along with rising consumer demand for immersive, lifelike gaming experiences. VR skill games offer unique engagement through motion tracking, 3D environments, and realistic interaction, appealing to tech-savvy users and creating premium monetization avenues for developers experimenting with next-generation gameplay.

By Revenue Model

Entry Fees segment dominated the Skill Gaming Market with the highest revenue share of about 36% in 2024 due to the direct monetization model that rewards users for participation and incentivizes regular gameplay. This model ensures platform liquidity and sustainability by enabling prize pools and competitive matchmaking. Entry fee-based tournaments also appeal to users confident in their skills, driving high repeat engagement and forming a core revenue stream for skill gaming platforms.

In-Game Purchases segment is expected to grow at the fastest CAGR of about 14.57% from 2025–2032 because of the shift toward freemium gaming models where users pay to enhance gameplay. Microtransactions for power-ups, cosmetic upgrades, hints, and level unlocks are becoming popular, especially among casual gamers. Platforms are increasingly optimizing purchase mechanics through gamification, behavioral analytics, and dynamic pricing, making in-game purchases a rapidly growing revenue channel in the skill gaming space.

Regional Analysis

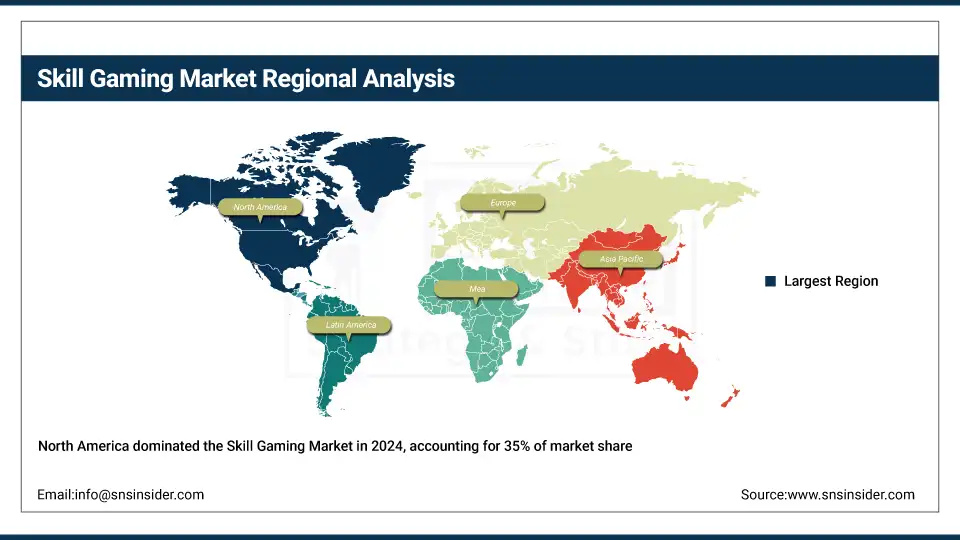

North America dominated the Skill Gaming Market with the highest revenue share of about 35% in 2024 due to mature digital infrastructure, high smartphone penetration, and strong consumer spending on real-money gaming. Favorable regulatory frameworks in the U.S. for skill-based formats, coupled with the popularity of e-sports and online card games, have attracted major investments and consistent player engagement, making the region the leading contributor to global market revenues.

Get Customized Report as per Your Business Requirement - Enquiry Now

The United States is dominating the skill gaming market in North America due to high user engagement, strong digital infrastructure, and favorable regulatory clarity.

Asia Pacific is expected to grow at the fastest CAGR of about 14.77% from 2025–2032 driven by a massive, youthful population, growing internet connectivity, and rapid smartphone adoption across emerging economies. Increasing interest in mobile gaming, local-language content, and culturally adapted skill-based formats are expanding user bases. Governments are gradually easing restrictions, and regional developers are innovating rapidly, positioning Asia Pacific as the most dynamic and scalable market in the global skill gaming ecosystem.

China is dominating the Asia Pacific skill gaming market due to its massive user base, advanced mobile ecosystem, and strong demand for competitive gaming experiences.

Europe holds a strong position in the Skill Gaming Market due to increasing internet penetration, rising smartphone usage, and favorable regulatory support. The region shows high engagement in online competitions, real-money gaming, and skill-based formats across diverse age groups.

The United Kingdom is dominating the European skill gaming market due to strong online gaming culture, mature regulations, and high consumer spending on digital entertainment.

Middle East & Africa and Latin America are emerging markets in the Skill Gaming space, driven by growing mobile penetration, young tech-savvy populations, and rising interest in competitive gaming. Economic development and digital access are expanding regional gaming participation.

Key Players

Skillz, DraftKings, FanDuel, Zynga (Take-Two Interactive), Supercell, Tencent Games, Scopely, Dream11, Mobile Premier League (MPL), WorldWinner (GSN Cash Games), Bet365, GameDuell, WinZO Games, Gameloft, King (part of Activision Blizzard), Riot Games, Square Enix, Valve Corporation, Sega, Netmarble.

Recent Developments:

-

2025: Skillz unveiled its Web SDK (v2025.0.37) enabling browser‑based play via Skillz.com without downloads, expanding reach to web users

-

2025: FanDuel Casino, part of Flutter, launched “Calling All Thrillionaires,” a new creative marketing platform spotlighting its Jackpot experiences across TV, digital, and retail channels.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 40.16 Billion |

| Market Size by 2032 | USD 105.10 Billion |

| CAGR | CAGR of 12.90% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Genre (Card-Based, Puzzle Games, Tile-Based, Board-Based, Word or Number-Based, Dice-Based, Others) • By Skill Type (Physical, Mental) • By Gaming Platform (Desktop, Mobile, Console, Virtual Reality (VR), Augmented Reality (AR)) • By Revenue Model (Entry Fees, Subscription Fees, In-Game Purchases, Advertising, Other Revenue Models) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Skillz, DraftKings, FanDuel, Zynga (Take-Two Interactive), Supercell, Tencent Games, Scopely, Dream11, Mobile Premier League (MPL), WorldWinner (GSN Cash Games), Bet365, GameDuell, WinZO Games, Gameloft, King (part of Activision Blizzard), Riot Games, Square Enix, Valve Corporation, Sega, Netmarble |

Frequently Asked Questions

North America led the Skill Gaming Market in 2024 with a 35% revenue share, supported by mature infrastructure and favorable regulatory conditions.

The Physical segment dominated the market with a 77% revenue share in 2024, due to demand for reflex-driven and action-based gaming experiences.

Increasing smartphone penetration, fast internet access, and the rising popularity of competitive, real-money gaming among Gen Z and millennials are major growth drivers.

In 2024, the Skill Gaming Market was valued at USD 40.16 billion, reflecting strong demand for competitive, reward-based digital gaming experiences.

The Skill Gaming Market is expected to grow at a CAGR of 12.90% from 2025 to 2032, driven by technology and user engagement.

Get in Touch