Transmission Repair Market Report Scope & Overview:

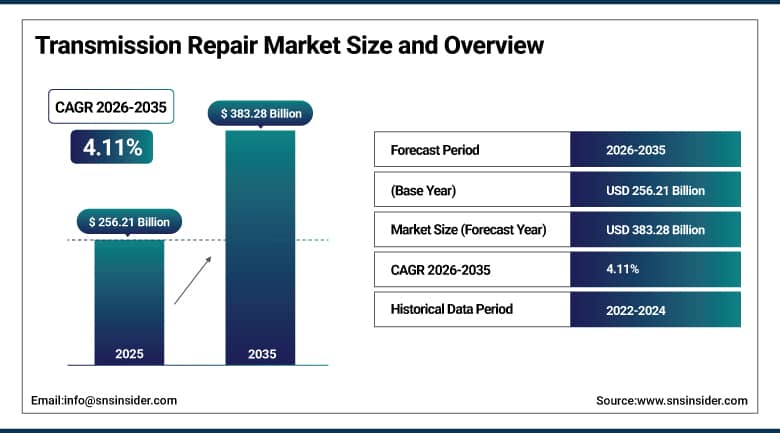

The Transmission Repair Market was valued at USD 256.21 Billion in 2025 and is expected to reach USD 383.28 Billion by 2035, growing at a CAGR of 4.11% from 2026–2035.

The global transmission repair market is driven by the expanding on-road vehicle fleet and the rising average age of vehicles worldwide. Over 65% of vehicles on the road exceeded 10 years of age in 2024, directly increasing demand for transmission maintenance and repair services. Automatic and hybrid transmission systems, which now account for approximately 55% of global service demand, require specialised repair expertise and diagnostic equipment that is creating a growing commercial market for professional service providers. The expansion of automotive service centres, rising consumer awareness of preventive maintenance, and the proliferation of commercial fleet operations across logistics and freight sectors are all contributing to steady and broad-based market growth across passenger and commercial vehicle segments.

In 2024, over 65% of vehicles on the road exceeded 10 years of age, driving a 24% increase in transmission repairs globally. Automatic and hybrid systems accounted for 55% of service demand, supported by a 30% rise in preventive maintenance uptake. These figures confirm that the ageing vehicle parc is the single most commercially reliable structural driver of transmission repair market demand, independent of new vehicle sales cycles or macroeconomic conditions.

Market Size and Forecast

-

Market Size in 2026E: USD 266.74 Billion

-

Market Size by 2035: USD 383.28 Billion

-

CAGR: 4.11% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Transmission Repair Market - Request Free Sample Report

Transmission Repair Market Trends

-

Growing adoption of advanced diagnostic tools and telematics-based predictive maintenance systems is enabling repair shops to identify transmission issues earlier.

-

Rising prevalence of automatic and hybrid transmissions in both passenger and commercial vehicles is increasing the technical complexity of repair requirements.

-

Increasing use of remanufactured and rebuilt transmission components is reducing repair costs for consumers while supporting sustainability goals.

-

Expanding mobile repair service offerings are bringing transmission servicing directly to fleet depots and commercial operators whose vehicle downtime costs make on-site repair commercially attractive relative to towing vehicles to fixed workshop locations.

-

Growing fleet electrification introducing EV-specific transmission and drivetrain service requirements is creating new service category development for repair providers investing in EV-compatible diagnostic and servicing infrastructure.

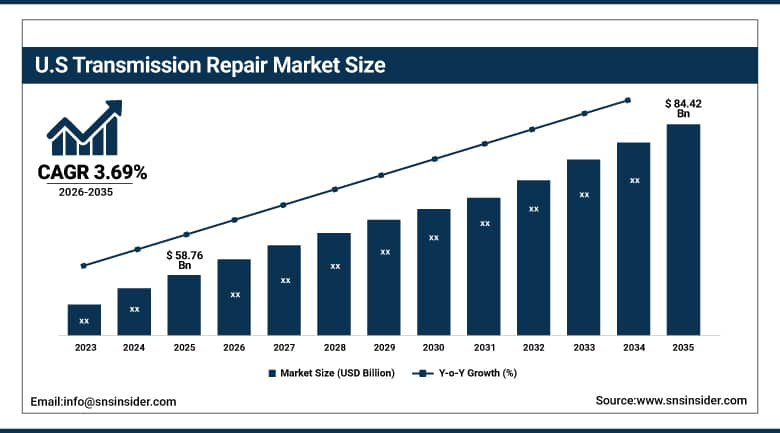

U.S. Transmission Repair Market Outlook

The U.S. Transmission Repair Market was valued at approximately USD 58.76 Billion in 2025 and is expected to reach approximately USD 84.42 Billion by 2035, growing at a CAGR of approximately 3.69%.

The United States is the world’s largest individual national transmission repair market, sustained by one of the world’s largest on-road vehicle fleets whose average age has risen consistently over the past decade as consumers extend vehicle ownership periods in response to elevated new vehicle prices and financing costs. The large base of ageing gasoline and light truck vehicles, combined with the widespread adoption of multi-speed automatic transmissions in American vehicles over the past two decades, creates a structurally reliable and geographically distributed demand for transmission repair and maintenance services that sustains both national franchise chains including AAMCO Transmissions and Midas and the independent repair shop ecosystem that serves local vehicle owners across suburban and rural markets. Rising fleet operations in last-mile delivery, ride-sharing, and logistics sectors whose commercial vehicle assets accumulate mileage at rates substantially above individual owner-operator vehicles are generating an above-average repair frequency commercial customer segment.

Schaeffler Group’s integration of predictive maintenance technology across its U.S. transmission repair service network demonstrates the commercial direction of the most technically sophisticated market participants, where data-driven diagnostics are moving the transmission repair relationship from reactive breakdown response toward scheduled preventive intervention that improves customer retention, reduces emergency repair cost, and allows service providers to maintain higher workshop utilisation rates through more predictable appointment scheduling across their service footprint.

Transmission Repair Market Segment Analysis

-

By Vehicle Type, Passenger Cars dominated with the largest revenue share in 2025, reflecting the sheer volume of passenger vehicles on global roads and the high frequency of automatic transmission service requirements; Commercial Vehicles are the fastest-growing vehicle type segment.

-

By Service Type, Transmission General Repair dominated the market with approximately 70% share in 2025 through its high frequency of demand across routine fault resolution including fluid leaks, solenoid failures, clutch adjustment, and gear synchronisation issues; Rebuilt and Remanufactured Transmission Services are the fastest-growing service type

-

By Component, Fluids dominated the market in 2025 as transmission fluid changes are the most frequently required and consistently performed transmission maintenance service across all vehicle types and transmission technologies; Filters are the fastest-growing component segment.

-

By End User, Independent Repair Shops dominated with approximately 38% revenue share in 2025 through their competitive pricing, localised customer relationships, and operational flexibility that attracts the majority of individual vehicle owner transmission repair demand; Mobile Repair Services are the fastest-growing end user segment.

By Vehicle Type, passenger cars dominate, commercial vehicles grow fastest

Passenger cars retained the dominant vehicle type position in the transmission repair market in 2025, a dominance that reflects the extraordinary global volume of passenger vehicles on the road whose combined automatic and manual transmission service requirements generate the majority of transmission repair shop workload by transaction count. The passenger car transmission repair segment is particularly robust in North American and European markets where the near-universal adoption of multi-speed automatic transmissions in the past two decades has created a large installed base of transmission-equipped vehicles approaching the service age where fluid degradation, wear, and electronic control unit issues create the repair demand that drives workshop revenue. The prevalence of continuously variable transmissions and dual-clutch automated manual transmissions in the passenger car fleet is also creating growing service demand for repair providers with the specific technical training and diagnostic software that these transmission technologies require.

Commercial vehicles are the fastest-growing vehicle type in the transmission repair market, driven by the extraordinary expansion of the global logistics and freight sector whose fleet vehicles accumulate annual mileage at rates two to five times those of typical private passenger cars, proportionally increasing the frequency of transmission service requirements per vehicle year of operation. The e-commerce-driven growth of last-mile delivery fleets operated by companies including Amazon, UPS, FedEx, and their regional logistics subcontractors is creating a structurally growing commercial vehicle transmission service demand that is geographically distributed across suburban and urban service markets and commercially concentrated in the fleet service provider relationships that major chains are building to serve these customers with scheduled, on-site, and mobile service options.

By Service Type, general repair dominates, rebuilt services grow fastest

Transmission General Repair retained the dominant service type position with approximately 70% of the transmission repair market in 2025, a commercial position that reflects both the high frequency of routine transmission faults across the global ageing vehicle fleet and the relative simplicity of general repair services compared to complete transmission rebuilds that require specialised equipment, extended workshop time, and higher parts cost. The general repair category encompasses the most commonly performed transmission services: fluid exchange and contamination correction, solenoid replacement for shift control failures, torque converter inspection and repair, gasket and seal replacement for leak resolution, and throttle cable adjustment for shift timing correction. These services collectively constitute the majority of transmission repair shop transactions by volume and define the recurring revenue base that sustains the commercial viability of both franchise and independent transmission repair businesses across all major markets.

Rebuilt and Remanufactured Transmission Services are the fastest-growing service type segment in the transmission repair market, driven by the growing consumer and fleet operator preference for factory-reconditioned transmission units that restore vehicle performance to near-original specification at a cost substantially below new OEM replacement while carrying quality warranties that increase buyer confidence relative to field-rebuilt alternatives. The remanufacturing sub-sector is benefiting from the standardisation of quality certification programmes by major automotive parts distributors including Genuine Parts Company and Auto Parts Holdings whose certified remanufactured transmission programmes provide both retail and trade customers with a commercially reliable alternative to new OEM components that is increasingly supported by national service centre chains seeking cost-competitive repair solutions for their price-sensitive customer segments.

By End User, independent repair shops dominate, mobile services grow fastest

Independent repair shops retained the dominant end user position with approximately 38% of the transmission repair market in 2025, a market leadership position that reflects their competitive advantages in price, flexibility, and localised customer knowledge that collectively make them the preferred service provider for the majority of individual vehicle owner transmission repair decisions in most major markets. Independent shops’ ability to negotiate competitive pricing for aftermarket parts, adapt their service offerings to local vehicle parc characteristics, and build long-term customer relationships through personalised service and community presence creates commercial resilience that franchise chain competitors with higher fixed overhead cannot always match at equivalent price points for the routine service and repair needs that represent the majority of transmission market transactions by volume.

Mobile Repair Services are the fastest-growing end user segment in the transmission repair market, driven by the commercial logic of fleet operators who recognise that the cost of having a non-operational commercial vehicle towed to a fixed workshop and remaining out of service during a conventional repair process substantially exceeds the marginal cost premium of on-site mobile service that returns the vehicle to operation within the same working day. The mobile transmission service model is particularly commercially viable for fluid change, filter replacement, and minor diagnostic and repair services that can be performed without workshop lifting equipment, creating a service capability that mobile operators including FleetPros and regional mobile service networks are building dedicated vehicle and tooling infrastructure to deliver across major metropolitan fleet operation zones.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Transmission Repair Market Insights

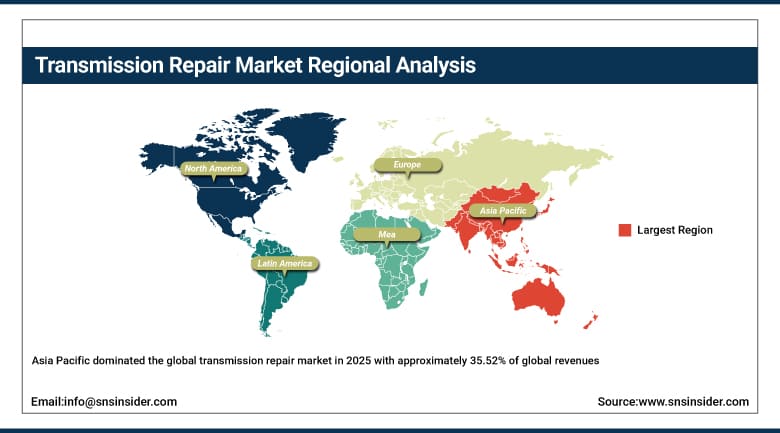

Asia Pacific dominated the global transmission repair market in 2025 with approximately 35.52% of global revenues and is simultaneously the fastest-growing region at a CAGR of approximately 5.54% through 2035. The region’s market leadership reflects the extraordinary scale of its vehicle fleet, which encompasses the world’s largest concentrations of passenger and commercial vehicles in China, India, Japan, and Southeast Asia, combined with rapidly improving automotive service infrastructure and growing consumer awareness of preventive transmission maintenance. China accounts for approximately 61.7% of Asia Pacific revenues through the scale of its domestic vehicle fleet, the rapid growth of its commercial logistics sector, and the progressive improvement of specialised automotive repair service quality in major urban and peri-urban vehicle service markets.

India represents the most commercially significant emerging growth opportunity within Asia Pacific as rising vehicle ownership, expanding highway freight logistics, and the increasing adoption of automatic transmissions in newly sold vehicles create a growing transmission service demand pool whose professional repair infrastructure is developing rapidly alongside rising consumer expectations for quality assured repair services. Japan and South Korea contribute sophisticated secondary markets whose high automatic transmission penetration, strong preventive maintenance culture, and dealer-maintained service quality standards generate premium transmission service demand that supports above-average per-vehicle service revenue for operators serving these markets.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Transmission Repair Market Insights

North America is the world’s second-largest transmission repair market, with the United States accounting for approximately 87.4% of North American revenues and representing the single most commercially valuable national transmission repair market by revenue concentration. The U.S. market’s commercial characteristics reflect a vehicle parc whose average age exceeds 12 years, an entrenched aftermarket service culture supported by national franchise chains and independent shops, and a commercial vehicle sector whose logistics and delivery fleet operations generate consistent high-volume transmission service demand. Canada contributes approximately 12.6% of North American revenues through its large vehicle fleet, strong preventive maintenance adoption, and commercial transportation sector whose cross-border freight operations between the U.S. and Canada sustain active heavy commercial transmission service demand at both domestic and cross-border service facilities.

Europe Transmission Repair Market Insights

Europe is a mature and technically sophisticated transmission repair market characterised by high vehicle quality standards, strong automotive aftermarket infrastructure, and growing regulatory pressure for vehicle maintenance compliance that is increasing consumer attention to transmission service frequency. Germany accounts for approximately 22.3% of European revenues as the region’s largest national market, anchored by its world-class automotive engineering culture, the high density of specialised automotive repair workshops serving both German and international vehicle brands, and a vehicle fleet whose above-average age combined with high-quality automatic transmission prevalence creates consistent professional transmission service demand that sustains premium workshop revenue per vehicle serviced.

The European market is also being shaped by the progressive electrification of the vehicle fleet, which is introducing new transmission and drivetrain service requirements for hybrid and electric powertrains alongside the established internal combustion engine transmission services that currently define the market’s revenue base. Forward-looking European transmission repair providers are investing in EV-specific service training, diagnostic equipment, and high-voltage system safety certification to position their workshops for the service requirements of the vehicle mix that will define European aftermarket repair demand through the second half of the forecast period.

MEA & Latin America Transmission Repair Market Insights

The Middle East and Africa and Latin America are growing transmission repair markets where expanding vehicle ownership, the prevalence of older imported vehicles requiring frequent maintenance, and the development of organised automotive service infrastructure are creating increasing market volumes. Saudi Arabia leads Middle East and Africa revenues at approximately 38.4% of the regional total through its large private vehicle fleet, substantial commercial logistics sector, and the development of a professional automotive service industry supported by Vision 2030’s economic diversification investment in service sector quality and technical training. Brazil leads Latin American revenues at approximately 44.2% of the regional total through its combination of the region’s largest vehicle fleet, a well-established independent automotive repair industry, and a commercial transportation sector whose domestic freight demand sustains active heavy commercial vehicle transmission service volume across the country’s extensive road network.

Market Dynamics

Growth Drivers: Rising average vehicle age driving repair frequency, growing automatic and hybrid transmission complexity creating specialised service demand

The primary structural growth driver for the transmission repair market is the rising average age of the global on-road vehicle fleet whose increasing age directly correlates with transmission wear, fluid degradation, and electronic control unit failure rates that collectively generate the repair demand that sustains the market. Consumers extending vehicle ownership periods in response to high new vehicle prices are sustaining a growing population of vehicles in the 8-to-15-year age bracket where transmission failure rates are highest and repair investment is most commercially justified relative to vehicle replacement cost. The progressive complexity of modern automatic, hybrid, and electric drivetrain transmission systems is simultaneously creating a growing market for specialised professional repair that general maintenance workshops cannot serve without specific technical training, certified diagnostic equipment, and access to the increasingly sophisticated parts supply that modern transmission technologies require.

Restraints: Skilled technician shortage limiting service capacity, electric vehicle transition reducing long-term ICE transmission service demand

A significant restraint on the transmission repair market is the chronic shortage of skilled transmission technicians whose specialised training in automatic, CVT, and dual-clutch transmission diagnostics and repair takes years to develop and is not being produced by vocational training institutions at a rate proportional to the market’s service demand growth. The electric vehicle transition represents a structural long-term restraint as battery electric vehicles without conventional transmissions progressively reduce the proportion of the vehicle fleet requiring automatic or manual transmission service, creating a demand reduction trajectory that will become commercially meaningful in markets with above-average EV penetration rates within the forecast period.

Opportunities: Predictive maintenance technology improving repair shop operational efficiency, mobile service model expansion serving fleet operators.

Predictive maintenance technology integrated with vehicle telematics is creating a commercial opportunity for transmission repair providers to offer subscription-based monitoring services that convert one-time repair customers into recurring maintenance programme participants whose predictable service schedules improve workshop planning, parts inventory management, and customer retention rates. Mobile service model expansion represents the most commercially innovative growth pathway in the transmission repair market, as purpose-equipped mobile workshop vehicles that serve fleet depots and commercial operators with scheduled on-site maintenance are demonstrating the ability to capture high-value commercial accounts that fixed workshop operators cannot serve with equivalent operational convenience.

Recent Developments:

-

2024: Volvo Group launched Volvo Dynamic Maintenance, an AI-driven predictive maintenance and repair optimisation platform for its Volvo Trucks, Renault Trucks, and Mack Trucks fleets, enabling data-driven transmission and drivetrain service scheduling that reduces unplanned breakdowns and improves fleet uptime for commercial customers globally.

-

2025: Daimler Truck introduced TruckForce, an AI-powered digital repair platform for its Freightliner, Mercedes-Benz Trucks, and Thomas Built Buses, providing service technicians with AI-assisted diagnostic guidance and parts sourcing that reduces average transmission repair diagnosis time and improves first-time fix rates across its dealer network.

-

2025: Allison Transmission expanded its certified remanufactured transmission programme, increasing the availability of factory-reconditioned automatic transmission units for the North American commercial vehicle aftermarket and providing fleet operators with a warranty-backed alternative to new OEM replacement that reduces total cost of ownership for high-mileage commercial vehicle transmissions.

-

2025: ZF Friedrichshafen launched an expanded aftermarket service training programme for technicians working on its 8-speed and 9-speed automatic transmission systems, addressing the skills gap in professional transmission repair and improving the quality and consistency of ZF transmission service delivery across its global authorised service network.

-

2025: AAMCO Transmissions accelerated its franchise expansion programme across the United States, adding new service centre locations in under-served suburban and secondary city markets to capture the growing transmission repair demand from ageing vehicle populations in communities that previously had limited access to specialised transmission repair services.

Transmission Repair Market Key Players

-

Schaeffler Group

-

Allison Transmission Holdings Inc.

-

BorgWarner Inc.

-

ZF Friedrichshafen AG

-

Continental AG

-

AAMCO Transmissions Inc.

-

Mister Transmission Ltd.

-

Lee Myles Autocare & Transmission

-

Aisin Seiki Co., Ltd.

-

Cottman Transmission and Total Auto Care

-

Midas Inc. (TBC Corporation)

-

Firestone Complete Auto Care (Bridgestone)

-

Genuine Parts Company (NAPA Auto Parts)

-

Advance Auto Parts Inc.

-

AutoZone Inc.

-

Driven Brands Holdings Inc.

-

Jiffy Lube International Inc.

-

Meineke Car Care Centers

-

Precision Industries Inc.

-

SunCoast Converters

Transmission Repair Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 256.21 Billion |

| Market Size by 2035 | USD 351.43 Billion |

| CAGR | CAGR of 4.11% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Transmission General Repair, Rebuilt & Remanufactured Transmission Services, Transmission Fluid Services, Others) • By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Others) • By Component (Fluids, Filters, Gaskets & Seals, Clutch Plates, Others) • By End User (Independent Repair Shops, Dealerships, Mobile Repair Services, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Schaeffler Group, Allison Transmission Holdings Inc., BorgWarner Inc., ZF Friedrichshafen AG, Continental AG, AAMCO Transmissions Inc., Mister Transmission Ltd., Lee Myles Autocare & Transmission, Aisin Seiki Co., Ltd., Cottman Transmission and Total Auto Care, Midas Inc. (TBC Corporation), Firestone Complete Auto Care (Bridgestone), Genuine Parts Company (NAPA Auto Parts), Advance Auto Parts Inc., AutoZone Inc., Driven Brands Holdings Inc., Jiffy Lube International Inc., Meineke Car Care Centers, Precision Industries Inc., SunCoast Converters |

Get in Touch