Traumatic Brain Injury Biomarkers Market Report Scope & Overview:

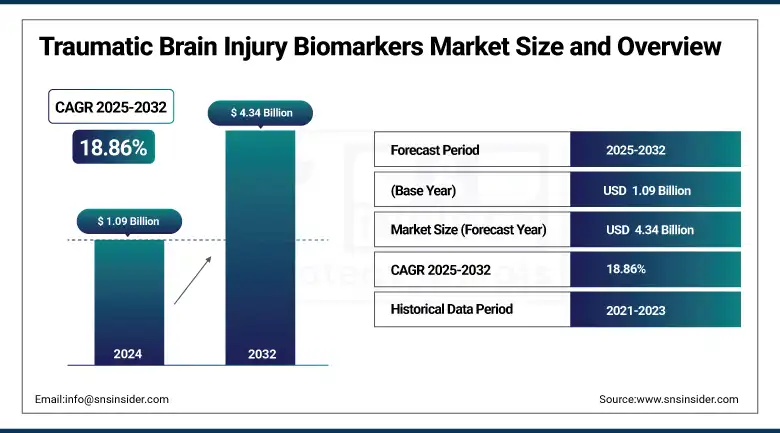

The traumatic brain injury biomarkers market size was valued at USD 1.09 billion in 2024 and is expected to reach USD 4.34 billion by 2032, growing at a CAGR of 18.86% over 2025-2032.

The traumatic brain injury (TBI) biomarkers market is also growing due to the increasing prevalence of TBI amongst sportspeople, military personnel, and road accident victims. The CDC reports that 1.5 million Americans sustain a TBI each year, driving an increasing need for tools for early diagnosis and treatment. There is rapidly increasing R&D activity in the global traumatic brain injury biomarkers market, able to improve the diagnostic accuracy with the discovery and establishment of blood-based, CSF, and imaging biomarkers.

To Get more information On Traumatic Brain Injury Biomarkers Market - Request Free Sample Report

In March 2025, Quanterix introduced a new-generation biomarker platform, which can detect NfL and GFAP at levels five times lower; the device has set a new standard in the traumatic brain injury biomarkers market.

Companies such as Abbott, Quanterix, and BioDirection are leading the way, including through FDA EUA approval of rapid assay solutions such as Abbott´s i-STAT Alinity platform. Growing government funding and institutional support, including the U.S. Department of Defense funding for biomarker-based detection tools, are boosting the TBI biomarkers market growth. Increased clinical trials and biotech company/research institutions collaborations are indicating a robust supply-side activity as well.

Regulatory initiatives such as those drafted by the FDA and EMA that are centered on precision diagnostics are shaping product development times. This demand is further accelerated due to rising adoptions of non-invasive tests and the rising elderly population, who are predisposed to falls and injuries. On the back of record-high R&D expenditure in neurodiagnostics worldwide, the traumatic brain injury biomarkers market study depicts a transition towards personalized and preventive care for neurological conditions.

In April 2025, Abbott declared its growing tests for a blood-based, portable diagnostic system designed for point-of-care TBI testing in an effort to meet an increasing worldwide demand as well as to raise the traumatic brain injury biomarkers market share.

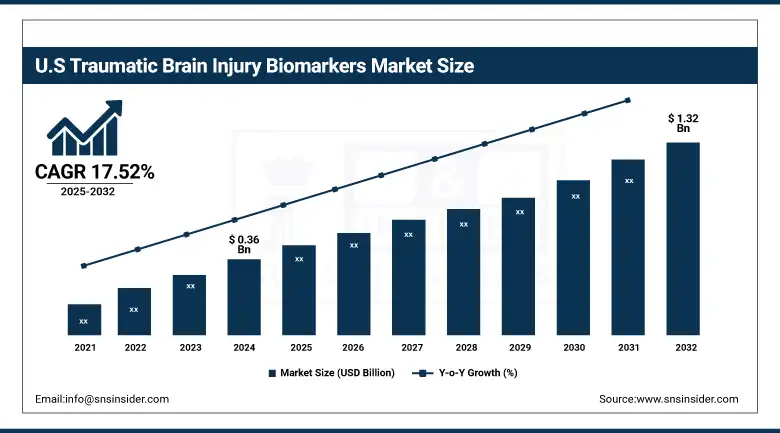

The U.S. traumatic brain injury biomarkers market size was valued at USD 0.36 billion in 2024 and is expected to reach USD 1.32 billion by 2032, growing at a CAGR of 17.52% over 2025-2032. The United States is the major market in this region owing to stringent regulations, a large number of biomarker-based diagnostic tests adopted in trauma centers, and a large number of R&D initiatives funded by both government and commercial players. Since 2020, biomarker research related to TBI with U.S. Department of Defense /funding has exceeded USD 200 million. There is increasing clinical trial activity and use of POC testing in Canada, particularly in rural and emergency areas. Mexico is becoming a regional epicenter in part because of better access to sophisticated diagnostics and efforts by the government to modernize trauma care. Mature reimbursement systems and early FDA approvals in the region have made it a center for innovation and deployment.

Market Dynamics:

Drivers:

-

Increasing Prevalence of Traumatic Brain Injuries, Rising Demand for Non-Invasive Diagnostics, And Growing R&D Spending Are Fueling Market Growth

The traumatic brain injury biomarkers market is primarily driven by growth in the burden of TBIs, which are being caused by traffic accidents, sports injuries, military action, and natural resource mining or construction. Road traffic accidents are the 8th cause of death globally, and TBIs are an important fraction of this cause. Increased public awareness and clinical demands for early and reliable diagnosis now drive a focus on blood-based biomarkers, including UCH-L1, Tau, and S100B. The supply side is being boosted substantially by public and private investment – literally (such as the over USD 550 million that the US National Institutes of Health has earmarked for brain injury research as part of its BRAIN Initiative). Furthermore, the growing use of AI for biomarker discovery and Neuroimaging analysis helps to simplify diagnostic pathways.

Regulatory encouragement has played an important role as well; The FDA granted Breakthrough Device Designation to BrainScope AI-Machine Learning Assisted EEG-Based assessment tool for TBI in 2023, reflecting increased regulatory confidence in biomarker innovation. Rising Focus on Multiplex Assays and High-Throughput Screening: The prevalence of high-throughput screening technologies and multiplex assays is also bolstering the expansion of the product lines among the landscape of the traumatic brain injury biomarkers players. With the growing need in emergency, military, and sports medicine applications, the global traumatic brain injury biomarkers market remains poised to witness further innovation and commercialization.

Restraints:

-

Limited Biomarker Specificity, Regulatory Challenges, And High Development Costs Are Hindering the Pace of Market Expansion

The traumatic brain injury biomarkers market analysis clearly identifies challenges that hinder broader adoption. Most detrimental to the field is the lack of biomarker specificity – several proteins, including GFAP and Tau, are elevated in various neuropathologies, making it challenging to identify TBI-specific markers free from confounds. This overlap in diagnostics hampers clinical utility and hinders regulatory approval. Furthermore, the strict regulations set forth by institutions such as the FDA and EMA call for elaborate validation of the sensitivity, reproducibility, and population-specific usage, again generating the need for long and expensive clinical studies.

High development costs also present challenges; the development of a single biomarker-based test can exceed USD 100 million, due to preclinical and human testing, manufacturing, and quality control considerations. Supply-side barriers, such as restricted availability of large-scale and related biobanks in TBI samples, have compounded the delayed delivery of discovery and validation. Furthermore, inequities in health care infrastructure, coupled with the expensive nature of sophisticated diagnostic platforms, reduce implementation at resource-poor sites. All these factors cumulatively are restraining the product innovation and commercial scalability and hindering the growth of the traumatic brain injury biomarkers market.

Segmentation Analysis:

By Type

The protein biomarkers segment was the highest contributor to the traumatic brain injury biomarkers market in 2024, accounting for more than half of the revenue share, as these biomarkers are widely used for early disease diagnosis and disease monitoring. Proteins, including GFAP, UCH-L1, and S100B, have been well validated for the detection of TBI because of their rapid increase after injury. Their commercial and clinical validation, simplicity of integration into blood-based diagnostics, and increasing FDA favor for protein-based assays have resulted in their market leadership.

Metabolomic biomarkers are anticipated to experience the fastest growth as metabolomics provides a fuller perspective of the biochemical alterations following injury. The proliferation of high-throughput metabolism platforms and systems biology methods has facilitated the discovery of novel metabolic markers associated with TBI on a faster time scale, and has fueled the interest in both research and clinical diagnostics.

By Sample Type

Blood-based biomarkers were the largest market segment in 2024, accounting for over 63.6% of the revenue share. They dominate because they are non-invasive and have a fast turnaround time, and when combined with point-of-care (POC) diagnostics. Recent developments in microfluidics and miniaturized biosensors have extended the potential usefulness of blood-based biomarker tests at the point-of-care in the field of emergency medicine. This market is also expected to exhibit the fastest growth during the forecast period, as there is a growing preference for minimally invasive diagnostic procedures, and high-throughput screening can be easily scaled up.

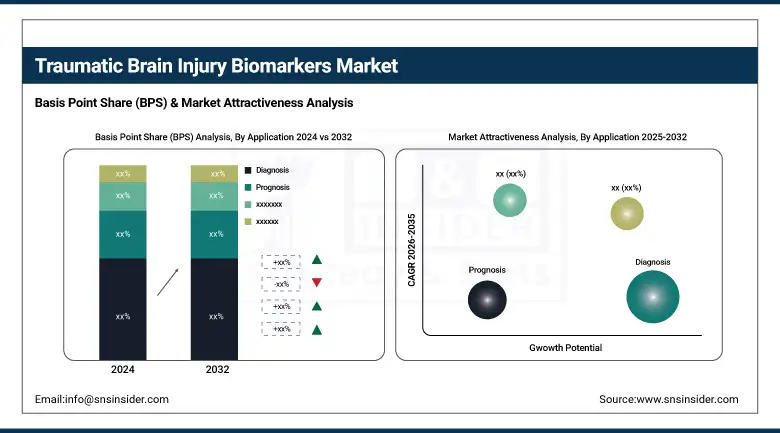

By Application

Diagnosis was the largest segment in 2024, accounting for a revenue share of 55.9% in 2024 due to the need for prompt and accurate detection of TBI patients in emergency departments and trauma centers. Early diagnosis is important for the prevention of secondary brain damage, and the panel of biomarkers provides more specificity than imaging alone.

Monitoring treatment response is expected to expand most rapidly as the system moves toward personalized medicine. Real-time assessment of the therapy response is provided by ongoing monitoring using biomarkers, contributing to improved patient outcomes and adaptive treatment design.

By End Use

Research institutes were the largest end user in 2024, accounting for 39% of the revenue. This prevalence reflects the intense scientific and clinical research aimed at discovering and confirming new TBI biomarkers. Significant government investment and joint efforts with biotech companies have made the institutes focal points of the biomarker development pipeline.

On the other hand, hospitals and clinics are expected to register the fastest CAGR, as there is a rising number of point-of-care (PoC) installed biomarker-based diagnostic tools, which facilitate better clinician decision-making and reduce dependence on image-based evaluations.

Regional Analysis:

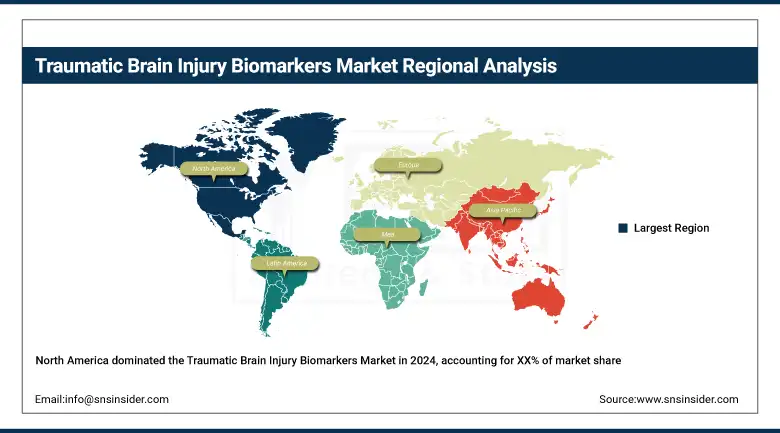

By region, North America led the global traumatic brain injury biomarkers market in 2024 with the presence of a high number of TBI cases, great investment in healthcare, and developed diagnostics.

Get Customized Report as per Your Business Requirement - Enquiry Now

Traumatic Brain Injury Biomarkers Market in Europe is the second-highest growing regional market due to excellent regulatory policies and the development of sports and geriatric-based TBIs. In Europe, the UK is the leader, as the National Health Service (NHS) incorporates biomarker testing into concussion protocols for athletes and elderly adults. Germany and France are also important contributors, fuelled by powerful biomedical R&D bases and links between academic institutions and the med-tech industry. In 2023, the EU introduced a EUR 75 million programme of research under Horizon Europe devoted to neurodegenerative and traumatic brain injuries, driving biomarker advancement. A sales acceptance and more startups for diagnostics, accompanied by pan-European aided funding, add to the acceleration of the market growth in the region.

The APAC region is expected to witness the highest growth in the traumatic brain injury biomarkers market during the forecast period, owing to the high rate of road traffic accidents, growth in the healthcare infrastructure, and significant public awareness. Regional Analysis China leads the regional market due to investments in neurological diagnostics, a huge patient population, and an increase in collaborations between global biotech companies and local hospitals. Brain health and precision medicine have also been prioritized in the Chinese government’s 14th Five-Year Plan. The fast Indian subcontinent is transitioning; the trauma to the head that afflicts the brain is a gigantic public health problem and an increasing academic-intuitive partnership for the development of diagnostic equipment.

Key Players:

Leading traumatic brain injury biomarkers companies operating in the market comprise Quanterix, Banyan Biomarkers, Abbott, Siemens Healthineers, GE Healthcare, Koninklijke Philips, Fujirebio, Thermo Fisher Scientific, Randox Laboratories, Immunarray, Oculogica, NeuroTrauma Sciences, BRAINBox Solutions, bioMérieux, Myriad Genetics, QIAGEN, F. Hoffmann-La Roche, and Abcam.

Recent Developments:

-

In February 2025, Quanterix partnered with Neurogen Biomarking to integrate its Simoa antibody technology into an at-home blood test for early dementia and mild cognitive impairment detection.

-

In April 2024, Abbott secured FDA clearance for a whole-blood rapid test on its iSTAT Alinity system, enabling concussion assessment at the bedside with results in just 15 minutes.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.09 billion |

| Market Size by 2032 | USD 4.34 billion |

| CAGR | CAGR of 18.86% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Protein Biomarkers, Genetic Biomarkers, and Metabolomic Biomarkers) •By Sample Type (Blood-Based, Cerebrospinal Fluid (CSF)-Based, and Urine-Based) •By Application (Diagnosis, Prognosis, and Monitoring Treatment Response) •By End Use (Hospitals & Clinics, Diagnostic Laboratories, and Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Quanterix, Banyan Biomarkers, Abbott, Siemens Healthineers, GE Healthcare, Koninklijke Philips, Fujirebio, Thermo Fisher Scientific, Randox Laboratories, Immunarray, Oculogica, NeuroTrauma Sciences, BRAINBox Solutions, bioMérieux, Myriad Genetics, QIAGEN, F. Hoffmann-La Roche, and Abcam. |

Frequently Asked Questions

North America dominated the Traumatic Brain Injury Biomarkers market.

Limited biomarker specificity, regulatory challenges, and high development costs are hindering the pace of market expansion.

The traumatic brain injury biomarkers market is primarily driven by growth in the burden of TBIs, which are being caused by traffic accidents, sports injuries, military action, and natural resource mining or construction.

The market is expected to reach USD 4.34 billion by 2032, increasing from USD 1.09 billion in 2024.

The Traumatic Brain Injury Biomarkers market is anticipated to grow at a CAGR of 18.86% from 2025 to 2032.

Get in Touch