Celiac Disease Treatment Market Report Scope & Overview:

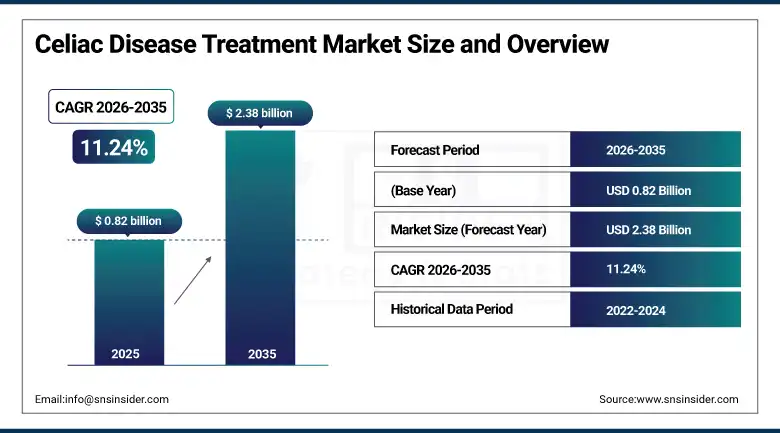

The Celiac Disease Treatment Market was valued at USD 0.82 Billion in 2025 and is expected to reach USD 2.38 Billion by 2035, growing at a CAGR of 11.24% from 2026 to 2035.

This is an autoimmune condition that affects about 1 percent of people across the world and is caused by ingestion of gluten in people who are predisposed and causes inflammation, atrophy of villi, and gradual absorption problems in the small intestines. In spite of its frequency, celiac is highly underdiagnosed around the world. According to World Gastroenterology Organization, more than 80 percent of the affected people are undiagnosed, resulting in a considerable patient population that could be targeted with increasing awareness in diagnostics and serological tests. There is a trend in the industry towards medication solutions rather than purely diet-based treatments. Enzyme replacement therapies, tight junction regulators, and novel immunomodulatory biologics are advancing through clinical development pipelines, with several Phase II and Phase III candidates targeting markets that currently have no approved pharmaceutical treatment option. This therapeutic gap represents one of the most commercially significant unmet medical needs in gastroenterology today.

Takeda Pharmaceutical received FDA Breakthrough Therapy designation for TAK-062, its engineered glutenase candidate designed to degrade immunogenic gluten peptides in the gastrointestinal tract before they trigger the autoimmune response characteristic of celiac disease. The designation accelerated the program's Phase II development timeline and validated the commercial hypothesis that a pharmacological adjunct to the gluten-free diet can be developed to address incomplete mucosal healing and inadvertent gluten exposure events that affect the majority of adherent celiac patients globally.

Market Size and Forecast

-

Market Size in 2026E: USD 0.91 Billion

-

Market Size by 2035: USD 2.38 Billion

-

CAGR: 11.24% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Celiac Disease Treatment Market - Request Free Sample Report

Celiac Disease Treatment Market Trends

-

Rising investment in next-generation enzyme replacement therapy and immunomodulatory drug candidates is expanding the celiac disease treatment pipeline beyond dietary management.

-

Improved serologic and genetic diagnostic tools are increasing the rate of confirmed celiac diagnosis globally, directly expanding the diagnosed patient population that constitutes the addressable commercial market.

-

Growing consumer and clinical awareness of non-classical celiac presentations including dermatitis herpetiformis, neurological manifestations, and silent celiac disease is broadening the patient identification funnel across specialty practice settings.

-

Digital health platforms and mobile applications enabling real-time gluten exposure tracking, dietary compliance monitoring, and symptom journaling are becoming commercially integrated components of comprehensive celiac management programs.

-

Regulatory frameworks across the FDA, EMA, and TGA are developing specific guidance for celiac disease drug development endpoints and trial design, reducing regulatory uncertainty for pharmaceutical sponsors advancing therapeutic candidates toward approval.

The U.S. Celiac Disease Treatment Market Outlook

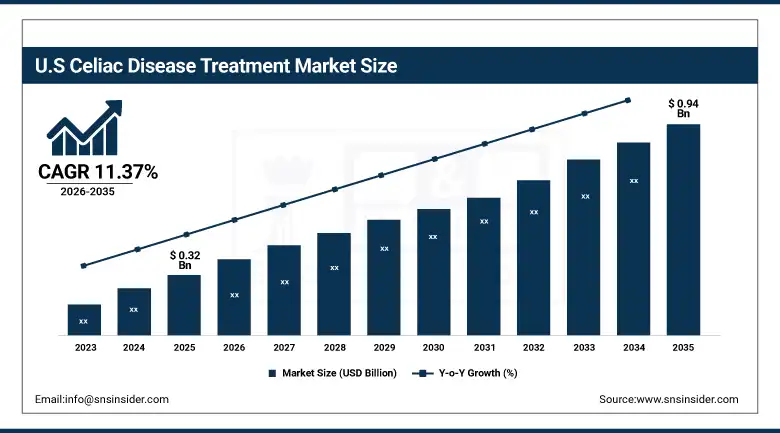

The U.S. celiac disease treatment market was valued at approximately USD 0.32 Billion in 2025 and is expected to reach approximately USD 0.94 Billion by 2035, growing at a CAGR of approximately 11.37%.

The United States is the world's most commercially developed celiac disease treatment market, supported by the highest absolute number of diagnosed celiac patients among major economies, a mature specialty gastroenterology infrastructure, and strong commercial adoption of premium gluten-free nutritional management products. The National Institutes of Health and the Celiac Disease Foundation have sustained research investment and patient advocacy programs that have progressively raised physician screening rates and public disease awareness over the past decade. FDA Breakthrough Therapy and Fast Track designations awarded to multiple pipeline candidates including larazotide acetate, nexvax2, and TAK-062 confirm the agency's recognition of the significant unmet need and its commitment to facilitating pharmaceutical development timelines for this historically underserved patient population. Major healthcare systems including the Cleveland Clinic and Mayo Clinic operate dedicated celiac disease centers whose clinical research programs are active trial enrollment sites for both domestic and international sponsors.

Dr. Schär, the global leader in gluten-free medical nutrition, launched a physician-directed celiac nutritional protocol programme in the United States in 2025, partnering with registered dietitians and gastroenterology practices to provide structured dietary management support as a complement to emerging pharmacological treatments. The programme addresses documented gaps in post-diagnosis nutritional counseling access that contribute to incomplete mucosal healing in a significant proportion of adherent gluten-free diet patients.

Celiac Disease Treatment Market Segment Analysis

-

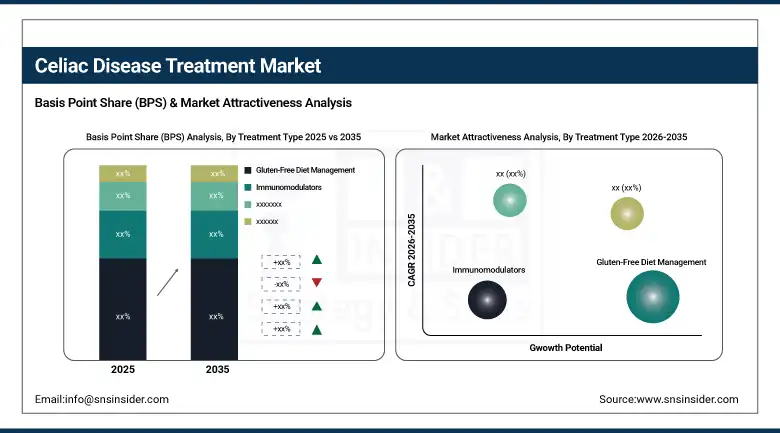

By Treatment Type, the gluten-free diet management segment dominated the market with 48.74% share in 2025, while the enzyme replacement therapy segment is the fastest growing during 2026 to 2035.

-

By Route of Administration, the oral segment dominated the market with 68.42% share in 2025, while the injectable segment is the fastest growing during 2026 to 2035.

-

By Drug Class, the nutritional supplements segment dominated the market with 52.36% share in 2025, while the biologics segment is the fastest growing during 2026 to 2035.

-

By End User, the hospitals & specialty clinics segment dominated the market with 58.47% share in 2025, while research centers are the fastest growing end user segment.

-

By Distribution Channel, the hospital pharmacies segment dominated the market in 2025, while online pharmacies are the fastest growing channel during 2026 to 2035.

By Treatment Type, gluten-free diet management dominates, enzyme replacement therapy grows fastest

Gluten-free diet management retained the dominant treatment position with 48.74% of market revenue in 2025. Gluten-free diet is currently the only treatment option for celiac disease recognized by international regulatory agencies as standard care for the condition. Patients must observe lifelong exclusion of wheat, barley, and rye from their diets altogether, ensuring continuous commercial opportunities for manufacturers of gluten-free foods, dietary supplements, and specialized treatment services delivered by dietitians. Compliance with dietary restrictions poses substantial limitations on patients’ lifestyle and social interactions, thus motivating sufferers to use any pharmaceutical treatments available that would alleviate the adverse effects of accidental gluten ingestion and enhance mucosal healing results in addition to existing dietary therapy. Enzyme therapy represents the most promising treatment segment, featuring a number of clinically developed products that include modified glutenase such as ALV003 and TAK-062. Successful Phase III completion for any enzyme therapy candidate would represent a market-defining approval event that would rapidly shift commercial spending toward pharmacological treatment options in the celiac management ecosystem.

By Route of Administration, oral dominates, injectable grows fastest

Oral drug delivery accounted for 68.42% of sales in 2025 due to the ease of administration in oral form, especially since the disease requires long-term therapy. The oral route of delivery is even more popular in the case of celiac disease owing to the complicated diet management practices which makes the patients sensitive to the complexity of further treatment. The highest growth rate was experienced by the injectable formulations in 2025, driven by the emerging pipeline products that aim at modulating immune responses to certain inflammation pathways. Refractory celiac disease type II, which carries significant malignancy risk, represents a small but high-value patient population where parenteral biologic intervention is the only potentially disease-modifying treatment option. Refractory celiac disease type II, which carries significant malignancy risk, represents a small but high-value patient population where parenteral biologic intervention is the only potentially disease-modifying treatment option. Regulatory designations awarded to injectable biologic candidates targeting this indication are establishing commercial precedent for premium pricing in refractory disease that will influence broader market pricing architecture.

By Drug Class, nutritional supplements dominate, biologics grow fastest

Nutritional supplements accounted for 52.36% of drug class revenue in 2025. Vitamins D and B12, iron, folate, calcium, and zinc supplementation address the nutrient malabsorption deficiencies that are near-universal in newly diagnosed celiac patients and persistent in a substantial minority even on strict dietary therapy. The nutritional supplement segment benefits from broad OTC accessibility and the growing consumer health awareness that has expanded supplement usage beyond physician-recommended patients to the large population of individuals with undiagnosed gluten sensitivity who self-manage with dietary modification and supplementation programmes without formal celiac disease diagnosis. Biologics represent the fastest-growing drug class as their potential to address the underlying immunopathology of celiac disease, rather than managing symptoms or supplementing nutritional deficits, positions them as the highest-commercial-value segment of the pipeline. Every biologic approval in celiac disease would establish a treatment category whose per-patient revenue contribution would substantially exceed the current nutritional supplement market average.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.42% |

|

Europe |

Germany |

28.73% |

|

Asia Pacific |

China |

34.82% |

|

Middle East & Africa |

Israel |

22.46% |

|

Latin America |

Brazil |

43.74% |

North America Celiac Disease Treatment Market Insights

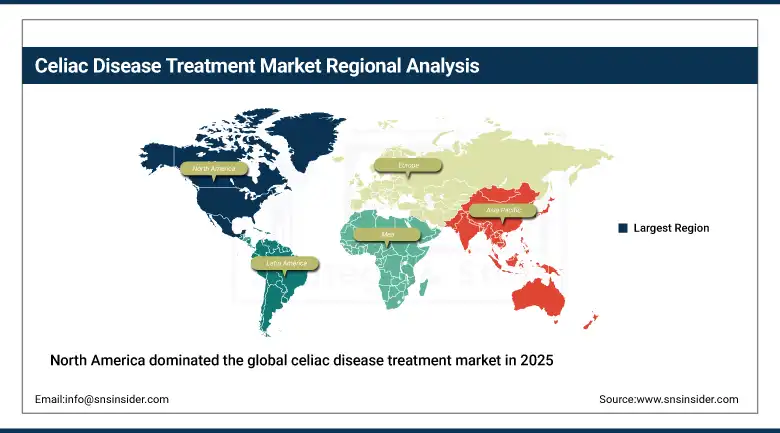

North America dominated the global celiac disease treatment market in 2025, holding approximately 42.84% of global revenues. The United States accounts for approximately 86.42% of regional revenue through its combination of the highest celiac diagnosis rate among major economies, the most commercially developed gluten-free nutritional products market, and the greatest concentration of Phase II and Phase III clinical trial activity globally. The Celiac Disease Foundation's sustained patient advocacy and physician education programs have measurably improved diagnosis rates and treatment adherence across the U.S. patient population. Canada contributes supplementary regional demand through its publicly funded gastroenterology specialist network and growing gluten-free product commercial infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Celiac Disease Treatment Market Insights

Europe held approximately 28.47% of global revenues in 2025. The European continent carries one of the world's highest documented celiac disease prevalence rates, with Sardinia, Finland, and Sweden recording particularly elevated population-level rates that have historically driven both clinical research leadership and commercial market development. The EMA's established rare and orphan disease regulatory pathways are providing development efficiency advantages to sponsors advancing celiac pharmaceutical candidates toward European approval. Germany accounts for approximately 28.73% of European revenues through its large diagnosed patient base, well-developed specialist gastroenterology network, and established reimbursement infrastructure for both medical nutrition and pharmaceutical therapies in autoimmune digestive conditions.

Asia Pacific Celiac Disease Treatment Market Insights

Asia Pacific is the fastest-growing regional market at a CAGR of approximately 12.84% through 2035. China and India each carry substantial but historically underdiagnosed celiac patient populations whose diagnosis rates are rising rapidly as genetic testing costs decline and physician awareness improves. Japan's advanced regulatory framework and established specialist gastroenterology infrastructure support growing clinical trial activity for international sponsors seeking Asia Pacific regulatory submissions. The progressive development of region-specific gluten-free food distribution infrastructure is creating the commercial foundation for both dietary management and future pharmacological treatment market development across the region's large and commercially underserved celiac patient populations.

MEA & Latin America Celiac Disease Treatment Market Insights

The Middle East and Latin America represent smaller but growing markets where improving medical infrastructure, rising physician awareness, and the progressive introduction of celiac screening programs into routine clinical practice are expanding the diagnosed patient base. Israel leads MEA revenues through its internationally recognized gastroenterology research centers whose academic-commercial partnerships support active clinical trial participation across both industry-sponsored and investigator-initiated celiac disease research programmes. Brazil leads Latin American revenues at approximately 43.74% of the regional total through its large population base, expanding specialist gastroenterology network in major urban centers, and a growing gluten-free food commercial market whose retail and foodservice development indirectly validates the widening celiac disease awareness that is progressively converting previously undiagnosed patients into active treatment market participants at both physician and consumer level.

Market Dynamics

Growth Drivers: Expanding pharmaceutical pipeline and rising global celiac diagnosis rates are creating sustained commercial demand growth.

The celiac disease treatment market's most commercially consequential structural driver is the progressive transition from a single-intervention market dominated by dietary management toward a multi-modal treatment landscape incorporating both nutritional management and pharmacological intervention. More than 25 pharmaceutical programs for celiac disease were in active clinical development as of 2025, representing the richest pipeline in the condition's treatment history and providing a forward revenue catalyst that is structurally independent of current standard of care revenue. Rising diagnostic rates driven by improved physician screening protocols, direct-to-consumer genetic testing adoption, and increasing public awareness campaigns are simultaneously expanding the patient population whose diagnosed status makes them a commercial addressable market for both existing and pipeline therapeutic products.

Restraints: Absence of approved pharmacological treatments and patient non-adherence to gluten-free diet create dual constraints on market.

The celiac disease treatment market operates in a paradoxical commercial environment where the only available standard of care requires no pharmaceutical prescription, limiting current market revenue to nutritional supplements and dietary management products whose per-patient economic value is modest relative to pharmacological alternatives in comparable chronic autoimmune conditions. Non-adherence to the gluten-free diet among diagnosed patients, estimated at 40 to 50% in adult populations, creates ongoing symptom burden that constitutes unmet need but does not currently generate pharmaceutical treatment revenue because no approved medication exists to address it. Clinical trial design complexity for celiac disease drug candidates, where mucosal healing and histological endpoints require lengthy and expensive endoscopic evaluation protocols, increases development costs and timelines that constrain pipeline investment.

Opportunities: First approved pharmacological treatment for celiac disease would represent a transformative commercial event.

Opportunity created by approval of the first non-dietary pharmacological agent for treatment of celiac disease:

Commercial potential for such a drug is enormous and is supported structurally, considering the prevalence, chronicity of the condition, and the ineffectiveness of purely dietary intervention as a total treatment solution to date. It has been forecasted that a first-to-market enzyme replacement therapy or an immunomodulator biological for celiac disease could tap into peak sales potential in excess of USD 1 billion annually, just within the United States, based on the patient population numbers and high prices for chronic autoimmune biologic drugs used for treatment of other diseases such as inflammatory bowel disease and rheumatoid arthritis. Global commercial potential will only increase, when accounting for international market development targeting other celiac disease populations in Europe, Australia, and Asia.

Recent Developments:

-

2025: Takeda Pharmaceutical advanced TAK-062 through Phase II clinical evaluation with promising interim data supporting dose selection for a Phase III registration trial, maintaining the program's FDA Breakthrough Therapy designation timeline and reinforcing market confidence in the near-term pharmacological treatment approval opportunity.

-

2024: ImmusanT completed Phase IIb enrollment for nexvax2, its gluten-specific peptide immunotherapy designed to induce tolerance to immunogenic gluten epitopes, with topline data anticipated to determine the program's path toward Phase III development and potential regulatory submission.

-

2024: Dr. Schär expanded its medical nutrition product portfolio with new physician-recommended gluten-free formulations specifically designed for newly diagnosed patients during the intestinal recovery phase, addressing documented nutritional gaps in the acute post-diagnosis management period that precede complete mucosal healing.

Celiac Disease Treatment Market Key Players are:

-

Takeda Pharmaceutical Company Ltd.

-

ImmusanT Inc.

-

Chugai Pharmaceutical Co. Ltd.

-

Alvine Pharmaceuticals Inc.

-

9 Meters Biopharma Inc.

-

GlaxoSmithKline PLC

-

Bioniz Therapeutics

-

Protagonist Therapeutics

-

Aimmune Therapeutics (Nestle Health Science)

-

Dr. Schär AG/SpA

-

Glutelief by Bioxcel Therapeutics

-

Cour Pharmaceutical Development

-

Artisan Biopharma

-

Bioatla LLC

-

Zealand Pharma A/S

-

Forte Biosciences Inc.

-

Celimmune LLC

-

Larazotide Acetate (9 Meters Bio)

-

Entasis Therapeutics

-

Intrexon Corporation

Celiac Disease Treatment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 0.82 Billion |

| Market Size by 2035 | USD 2.38 Billion |

| CAGR | CAGR of 11.24% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Type (Gluten-Free Diet Management, Enzyme Replacement Therapy, Immunomodulators, Steroids & Vitamins/Minerals Supplementation, Others) • By Route of Administration (Oral, Injectable, Others) • By Drug Class (Biologics, Small Molecules, Nutritional Supplements) • By End User (Hospitals & Specialty Clinics, Research Centers, Homecare Settings) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Takeda Pharmaceutical Company Ltd., ImmusanT Inc., Chugai Pharmaceutical Co. Ltd., Alvine Pharmaceuticals Inc., 9 Meters Biopharma Inc., GlaxoSmithKline PLC, Bioniz Therapeutics, Protagonist Therapeutics, Aimmune Therapeutics (Nestle Health Science), Dr. Schär AG/SpA, Glutelief by Bioxcel Therapeutics, Cour Pharmaceutical Development, Artisan Biopharma, Bioatla LLC, Zealand Pharma A/S, Forte Biosciences Inc., Celimmune LLC, Larazotide Acetate (9 Meters Bio), Entasis Therapeutics, Intrexon Corporation |

Frequently Asked Questions

North America dominated the celiac disease treatment market in 2025.

Gluten-free diet management dominated the celiac disease treatment market with 48.74% share in 2025.

The primary growth factors are the expanding pharmaceutical pipeline for non-dietary treatment options and rising global celiac disease diagnosis rates driven by improved screening and genetic testing accessibility.

The celiac disease treatment market was valued at USD 0.82 Billion in 2025.

The celiac disease treatment market is expected to grow at a CAGR of 11.24% from 2026 to 2035.

Get in Touch