Tremfya Market Report Scope & Overview:

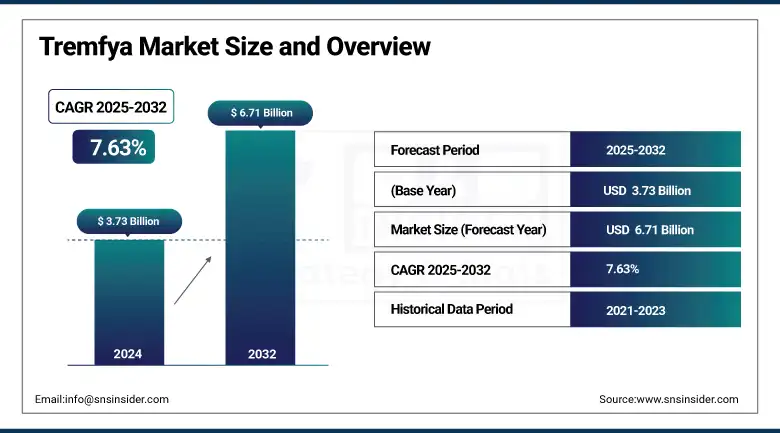

The Tremfya market size was valued at USD 3.73 billion in 2024 and is expected to reach USD 6.71 billion by 2032, growing at a CAGR of 7.63% over 2025-2032.

The global tremfya market is increasing due to a growing case of autoimmune diseases such as plaque psoriasis and psoriatic arthritis. A preferred relatively newer biologic, tremfya (guselkumab), a biologic modulating IL-23, has the advantage of its specificity, a good safety profile, and long-term retention of efficacy. Rising incidence of disease, higher rate of diagnosis, and preference for individualized immuno therapies will create demand for next-generation, targeted biologics. With regulatory approvals and other such developments from the likes of the FDA and EMA still forthcoming, there is still plenty to drive the tremfya market, and label expansions have recently made it available for more extensive use.

To Get more information On Tremfya Market - Request Free Sample Report

In June 2024, Janssen launched a phase III clinical trial to evaluate Tremfya in axial spondyloarthritis, which could broaden its label far beyond psoriasis and psoriatic arthritis.

Growing R&D budget for immunology by Tremfya companies, including Janssen Pharmaceuticals (Johnson & Johnson), the key contributor of IL-23 research, provides significant support to the demand for the market. J&J invested more than USD 15 billion in R&D in 2023 alone, much of that money going into the field of immunology. In addition, favorable reimbursement and increasing physician preference for IL-23 inhibitors over TNF and IL-17 agents will drive demand. Tremfya market share is poised to grow based on current clinical trials of new indications as supply stabilizes and global manufacturing capacity increases, which will improve product availability in developing areas. In addition, the ongoing updating of treatment guidelines favoring IL-23 inhibitors is supporting the Tremfya market, driving prescription expansion.

In March 2024, Janssen issued positive real-world data in more than 20,000 patients demonstrating sustained clearance and long-term remission with Tremfya, bolstering its clinical and commercial claim in the Tremfya market analysis.

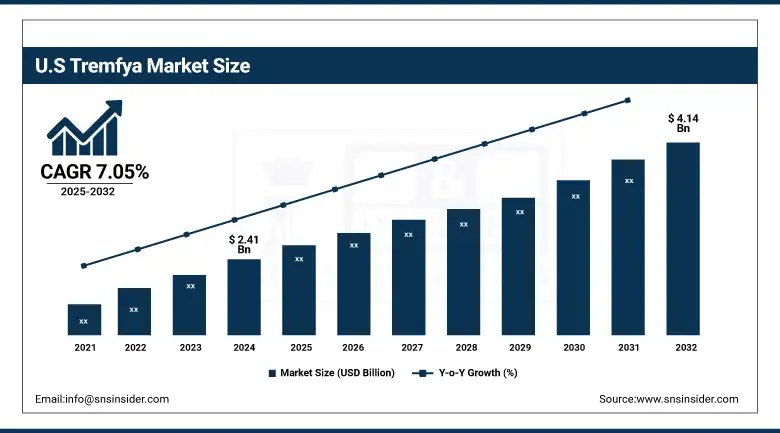

The U.S. Tremfya market size was valued at USD 2.41 billion in 2024 and is expected to reach USD 4.14 billion by 2032, growing at a CAGR of 7.05% over 2025-2032. The U.S. has also gained a leadership position in the region due to a high patient pool, early availability of biologics, and strong R&D activities of major pharmaceutical players such as Johnson & Johnson. Psoriasis Over 7.5M Americans were diagnosed with psoriasis in 2023, and treatment needs are very substantial. Moreover, supportive reimbursement in the form of diagnostic implementation and relatively high-level physician awareness result in solid adoption. In Canada, the business is going up gradually with the government’s rising support for specialty drug coverage and the rise in awareness among dermatologists. Mexico, though lagging overall in development of the biologics market compared to the United States and Canada, is growing due to public-private investment, biologics on the national formulary, and urban domiciling of the patient.

Market Dynamics:

Drivers:

-

The Tremfya Market is Being Propelled by Rising Disease Burden, Increasing Biologics Preference, Robust R&D Investments, and Evolving Treatment Guidelines

The Tremfya market is expanding on the back of the growing global burden of moderate-to-severe plaque psoriasis and psoriatic arthritis. Estimates by the National Psoriasis Foundation indicate that over 8 million Americans suffer from psoriasis, driving the need for a long-term solution in the market. As an IL-23 inhibitor, Tremfya provides long-term remission with fewer side effects than the older biologics. Another major driver is the rapid transformation of clinical practice toward targeted biologics, in particular for patients who do not respond to TNF-alpha or IL-17 inhibitors.

ABBV, LLY, and Eli Lilly have been growing their R&D efforts, and as the company behind Tremfya invests in continuing to innovate IL-23, there are now over 100 clinical trials underway researching different IL-23 pathways. Expectation of making approvals on biologicals, such as fast-track and expanding labels, has boosted market confidence. In addition, biosimilar competition is still light here, so there is still pricing power and profit in the segment. Both AAD and EULAR clinical guidelines have reiterated IL-23 inhibitors as first-line treatment for long-term disease control, in turn giving a lift to the Tremfya market growth. Increasing patient awareness, doctor training, and payer adoption of premium treatment options echo strong positive growth in the tremfya market trends.

Restraints:

-

The Tremfya Market Faces Pricing Pressures, Biosimilar Threats, and Access Limitations That May Hinder Long-Term Growth

The biggest constraint is the high cost of treatment, with the cost of annual therapy often rising above USD 60,000, which restricts access of uninsured or under-insured patients to treatment. Though biologics like Tremfya are reimbursed in developed markets, high out-of-pocket (OOP) costs and significant prior authorization steps hold back adoption. And in lower-income markets, affordability is still a significant obstacle. Furthermore, the supply chain for biologics, including cold chain considerations and manufacturing capacity, particularly in times of geopolitical challenges, can become a barrier to widespread global accessibility.

Only 45% of new biologics are available in low- and middle-income countries within three years of launch, according to IQVIA. A further restraint is the nascent biosimilar pipeline, while IL-23 drugs are yet to hit the market, potentially enabling a price war from the early 2030s due to regulatory incentives and patent expirations. Furthermore, the approval delays or recalls could be a threat to the continuous flow of the market, if a tough regulatory environment and batch-to-batch variation issues are considered. In addition, patient compliance problems associated with needle phobia and the desire for oral therapy are hindering growth in certain segments. All of these influences taken together result in limiting the Tremfya market share expansion, even if it does have an impressive efficacy.

Segmentation Analysis:

By Application

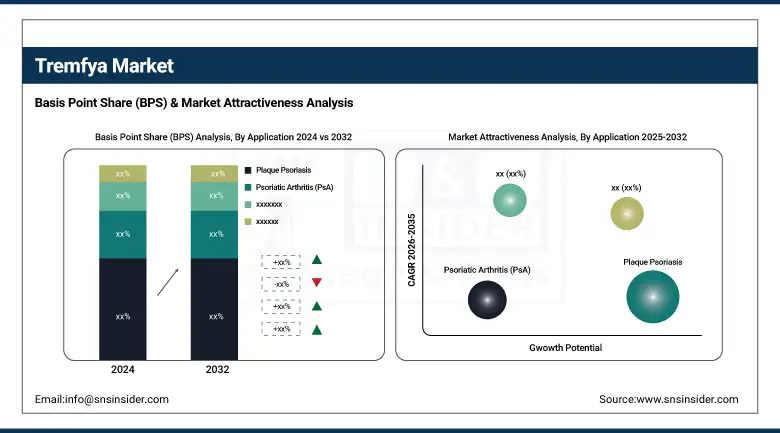

In 2024, the largest revenue share of 87.03% was captured by the plaque psoriasis segment on the Tremfya market, owing to the high prevalence of plaque psoriasis moderate-to-severe patients across the globe and robust clinical outcomes delivered by IL-23 inhibitors, including Tremfya. Uptake was also supported by the growing rate of diagnosis and heightened patient knowledge of biologic medicines. KOLs’ preference for IL-23 inhibitors as a preferred choice for long-term disease control was also a key driver of demand. Conversely, the psoriatic arthritis (PsA) category is expected to achieve the strongest growth, maintained by the growing body of clinical data supporting Tremfya’s efficacy in joint inflammation and stiffness. An approved indication for PsA and increasing rheumatologist uptake mean that use outside of dermatology settings is increasing.

By Distribution Channel

The hospital pharmacies segment was the leader in 2024, which accounted for 51.23% of the revenue share of the Tremfya market. Reasons for this domination are the high extent of hospital-based biologics initiation, especially in moderate-to-severe cases, and facilitated ordering procedures in special therapeutic agents through institutional purchasing. On the contrary, online pharmacies are anticipated to be the fastest-growing segment. This growth is being fueled by increasing adoption of digital health, increased convenience of home delivery of biologics, increased patient confidence in regulated e-pharmacies, and wider direct-to-consumer models post-pandemic.

Regional Analysis:

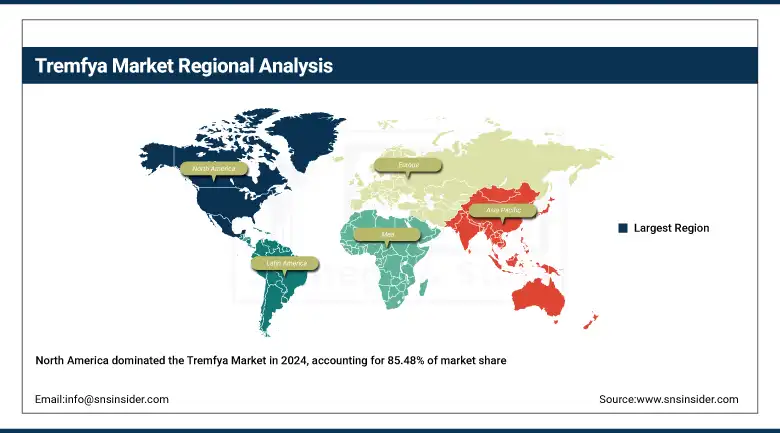

North America held the largest revenue share in the global Tremfya market in 2024, accounting for 85.48% of global revenue. During the forecast period, owing to a high prevalence of plaque psoriasis and psoriatic arthritis, robust uptake of biologics, and well-established healthcare infrastructure.

Get Customized Report as per Your Business Requirement - Enquiry Now

The tremfya market in Europe is still seeing steady growth as the biologic pool widens and psoriasis increases. General adoption of IL-23 inhibitors in guidelines and greater interest in novel treatments are driving forces. Germany is the largest country in the region due to the early adoption of biologics, a pharmaceutical R&D base, and a favorable reimbursement environment. Biologics like Tremfya are covered by public health insurance in Germany, which makes it accessible to more people. The UK is among the fastest-growing in Europe, driven by NHS access initiatives and growing clinical preference for IL-23 inhibitors. France and Italy are also major contributors on the back of a highly aged population and high psoriasis diagnosis rate, and Poland and Turkey are emerging with better outcomes through healthcare reforms and growing regulatory approvals on novel biologics.

The Asia Pacific Tremfya market is anticipated to witness maximum growth during the forecast period, owing to growing disease awareness, better healthcare infrastructure in emerging economies such as India and China, and huge investment in developing immunology. Japan is the leading country in the region with a high-quality healthcare system, high penetration of biologics, and an ageing population. Japan has one of the broadest coverage of AT, including Tremfya, and provides substantial reimbursement. China is quickly becoming a new growth driver due to the growth of the middle class, an increasing prevalence of psoriasis (projected > 6 M cases), and most importantly, improving regulatory timelines for biologics. In addition, China’s NMPA is fast-tracking drug approvals via its priority review system. India and South Korea are also achieving growth driven by improved access to biosimilars and government health schemes targeting chronic skin and joint diseases.

Key Players:

Leading tremfya company in the market landscape is Johnson & Johnson Services, Inc.

Recent Developments:

-

In June 2024, Johnson & Johnson announced encouraging results from a clinical study showing that Tremfya significantly improved symptoms in patients with active psoriatic arthritis (PsA), supporting its efficacy in joint symptom management alongside skin clearance.

-

In March 2025, the U.S. FDA approved Tremfya (guselkumab) as the first and only IL-23 inhibitor offering both subcutaneous and intravenous induction options for adults with moderately to severely active Crohn’s disease, enhancing treatment flexibility and patient access.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.73 billion |

| Market Size by 2032 | USD 6.71 billion |

| CAGR | CAGR of 7.63% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Plaque Psoriasis, Psoriatic Arthritis (PsA), and Others) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Johnson & Johnson Services, Inc. |

Frequently Asked Questions

Tremfya is well-positioned as a first-in-class IL-23 inhibitor with subcutaneous and IV dosing flexibility, making it a preferred choice for long-term disease control.

Major competitors include AbbVie (Skyrizi), Eli Lilly (Taltz), Novartis (Cosentyx), Amgen, and UCB, which offer similar biologics in the IL-23, IL-17, and TNF spaces.

North America dominates the Tremfya market with over 85% share in 2024, followed by Europe, due to early approvals, high diagnosis rates, and broad insurance coverage.

Key growth drivers include rising prevalence of autoimmune conditions, increasing demand for IL-23 inhibitors, favorable clinical outcomes, and strong regulatory support for label expansion.

Over the past five years, the Tremfya market has grown steadily due to expanded indications, wider geographic access, and its strong safety-efficacy profile compared to older biologics.

Get in Touch