Amniotic Products Market Report Scope & Overview:

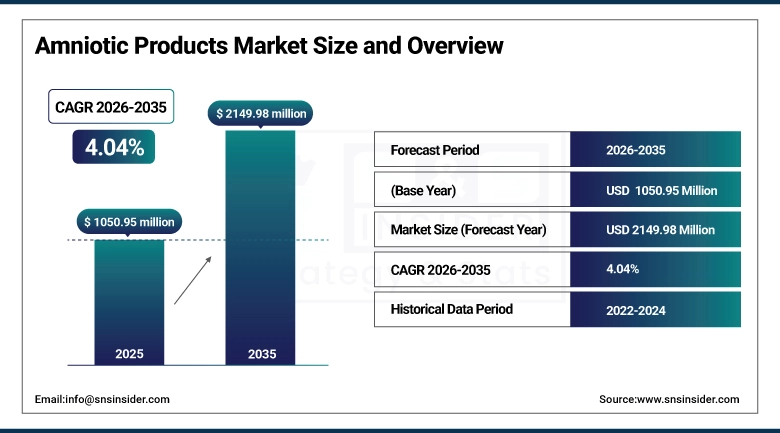

The Amniotic Products Market size was valued at USD 1050.95 Million in 2025 and is projected to reach USD 2149.98 Million by 2035, growing at a CAGR of 7.42% during 2026–2035.

Increased adoption of regenerative medicine and biologic therapies for wound care, ophthalmology, and orthopedic application is driving the growth of Amniotic Products Market. The therapeutic advantages of amniotic products, including increased healing, anti-inflammatory, and decreased scarring effects, are driving clinical demand and awareness of these products. Technological progress in cryopreservation and dehydration protocols, rising trend of outpatient procedures, expanding healthcare infrastructure in developing regions also boost the market growth during the forecast period of 2026–2035.

Amniotic Products Market Size and Forecast:

-

Market Size in 2025: USD 1050.95 Million

-

Market Size by 2035: USD 2149.98 Million

-

CAGR: 7.42% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Amniotic Products Market - Request Free Sample Report

Amniotic Products Market Key Trends:

-

The increasing adoption of regenerative medicine and biologic therapies is driving demand for advanced amniotic products across wound care, ophthalmology, and orthopedics.

-

Technological advancements in cryopreservation, dehydration, and lyophilization methods are improving product shelf life, clinical efficacy, and ease of use.

-

Collaborations between amniotic product manufacturers and hospitals or specialty clinics are enhancing market penetration and clinical awareness.

-

Growing focus on minimally invasive procedures and outpatient treatments is stimulating the development of suspension-based and ready-to-use amniotic products.

-

The expanding presence of distributors and healthcare networks in emerging regions is creating new market opportunities.

-

AI-driven product tracking, quality control, and supply chain optimization are revolutionizing operational efficiency and product deployment in the amniotic products market.

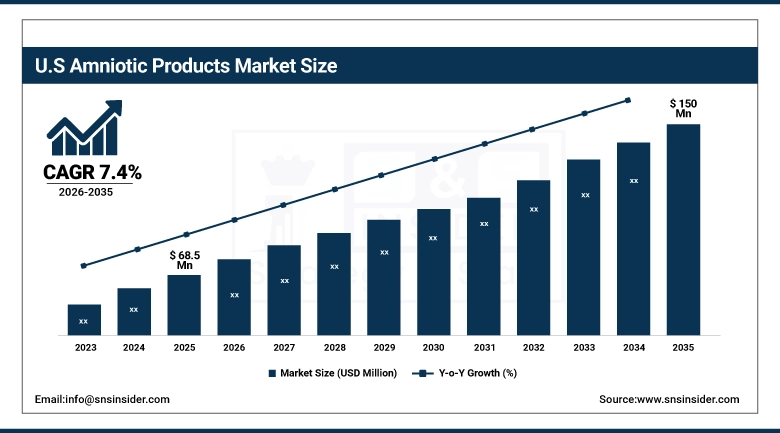

The U.S. Amniotic Products Market size was valued at USD 68.5 Million in 2025 and is projected to reach an estimated USD 150 Million by 2035, growing at a CAGR of 7.4% during 2026–2035. This reflects steady expansion driven by rising clinical adoption of regenerative therapies, increasing prevalence of chronic conditions, and growing procedural volumes within key therapeutic areas.

Amniotic Products Market Key Drivers:

-

Rising adoption of regenerative medicine and biologic therapies across wound care, ophthalmology, and orthopedics is boosting market demand.

Growth of Amniotic Products Industry is contributing with the rising clinical adoption as therapeutic benefits of advanced amniotic products for the treatment of various diseases and conditions are recognized. Focus on Increasing Incidence of Chronic Wounds, Ocular Disorders, and Orthopedic Conditions have urged the hospitals and specialty clinics towards procuring high performance amniotic solutions. Advancements in cryopreservation and dehydrated membranes, coupled with growing outpatient procedures and expanding infrastructure in developing regions is further widening market adoption and help sustain revenue growth.

Amniotic Products Market Key Restraints:

-

High costs, stringent regulatory approvals, and ethical considerations are constraining consistent growth of the Amniotic Products Market.

The major restraints for Amniotic Products Market are high cost of the product, complex and time-consuming regulatory pathways, and ethical concerns associated with use of human-derived tissues. Additionally, high price point can restrict access among other smaller healthcare facilities, while prolonged regulatory compliance requirements can postpone the ability of products to enter the market. Some regions also face further hurdles due to ethical and sourcing issues, preventing widespread acceptance. Steady growth is impeded by economic volatility coupled with reimbursement uncertainties, resulting in a climate in which manufacturers must tread carefully, balancing clinical, regulatory – and now operational – complexities.

Amniotic Products Market Key Opportunities:

-

Growing demand for minimally invasive procedures, advanced biologics, and outpatient treatments creates opportunities for market expansion.

The increasing demand for new, clinically proven, and easy to use amniotic products opens up the growth potential to the market. The shift towards therapies that promote healing, minimize scarring, and accelerate recovery is being embraced an increasing number of healthcare providers, which is a key factor driving uptake of amniotic suspensions that are pre-packaged for clinical use, and of dehydrated membranes. Combined with growing healthcare infrastructure, improving procedural volumes, and enhancing distribution networks, emerging regions are an ideal backdrop for market penetration. The manufacturers that prioritize product innovation and operational efficiency, while also engaging clinicians with their solution, will lead the way in gaining market share and subsequently, growing their practice.

Amniotic Products Market Segments:

-

By Type: In 2025, Cryopreserved dominated with 60% share; Dehydrated fastest growing segment during 2026–2035

-

By Product: In 2025, Membranes dominated with 65% share; Suspensions fastest growing segment during 2026–2035

-

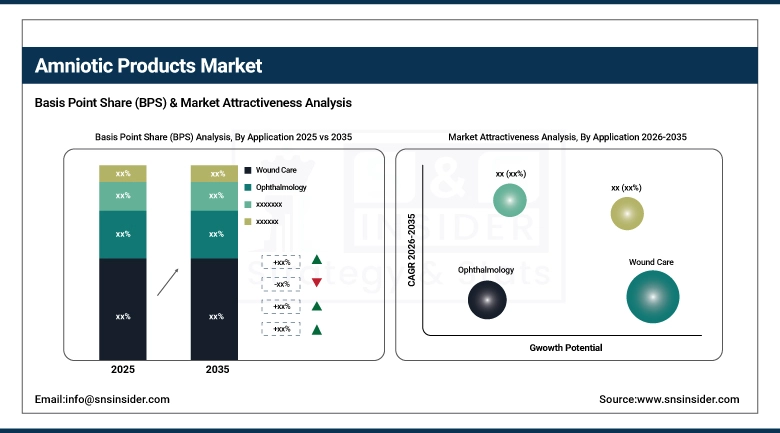

By Application: In 2025, Wound Care dominated with 50% share; Ophthalmology fastest growing segment during 2026–2035

-

By End User: In 2025, Hospitals dominated with 55% share; Ambulatory Surgical Centers fastest growing segment during 2026–2035

Amniotic Products Market Segment Analysis:

By Type, Cryopreserved Dominates While Dehydrated Expands Rapidly:

The cryopreserved segment led the market in terms of revenue share due to greater acceptance among clinicians, enhanced biological activity, and wider applications of the product in therapies. The promise of strong demand continues across its use in wound care, ophthalmology, and orthopedics. Cryopreserved product revenue was USD 630 million in 2025.

The largest growing segment is dehydrated, due to ease of storage and longer shelf life, with a growing outpatient market. Rising usage in ambulatory surgical centers and specialty clinics is driving growth. Dehydrated product revenue was USD 420 million in 2025.

By Product, Membranes Dominate While Suspensions Expand Rapidly:

Due to their reliable effectiveness in a number of surgical, wound care, and ophthalmic uses, membranes segment held the majority share of the market. The market value of Membranes covered USD 680 million in 2025.

Expanding product type in fast growth segment due to their use in minimally invasive procedures with ease of preparation for clinical application in practice Increasing penetration in outpatient procedures as well as regenerative therapy applications is leading the positive growth. Suspensions were only USD 370 million in 2025

By Application, Wound Care Dominates While Ophthalmology Expands Rapidly:

The market was dominated by Wound Care segment due to high incidence of chronic wounds, diabetic ulcers, and post-surgical wound management. It keeps market leadership with its broadest use of hospitals and specialty clinics. Wound Care application held USD 525 million in 2025.

The rapid growth of the ophthalmology segment is driven by a growing number of surgical and corneal therapy procedures, regulatory approvals of novel products, and rising patient awareness regarding the safety ands efficacy of contact lenses, eye myopia, and presbyopia. Growing awareness of amniotic therapies in relation to health of the eye is driving the market due to increased adoption. Ophthalmology applications were worth USD 310 million in 2025.

By End User, Hospitals Dominate While Ambulatory Surgical Centers Expand Rapidly:

The dominance of hospitals segment is attributed to higher budget allocation for advanced technologies, greater procedural volumes and integration of laser therapy into standard care pathways. Cryopreserved membranes and suspensions are in regular demand as hospitals continue to make use of them. Hospital & Professional Service Revenue was USD 580 million in 2025

Outpatient procedures and adoption of minimally invasive therapy will continue to elevate the prevalence of surgical centers to the fasted growing end user while easier integration of ready-to-use amniotic products operate on the same level as hospital environment will help grow market share. USD 210 million in revenue from Ambulatory Surgical Centers in 2025

Amniotic Products Market Regional Analysis:

North America Amniotic Products Market Insights:

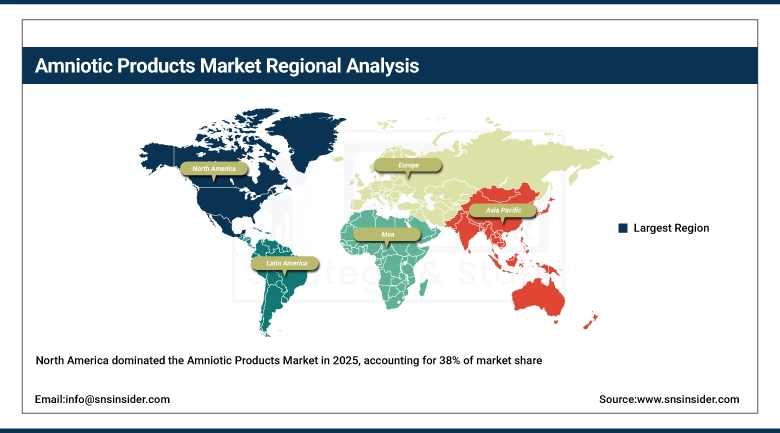

Amniotic Products Market by Region North America held the largest share of the overall Amniotic Products Market in 2020, 38% share, supported by developed healthcare infrastructure, large procedural volume, and increased adoption of regenerative medicine therapies in the region. The U.S. and Canada boast a high level of clinical awareiless, robust hospital networks, and accessible regenerative amniotic products, and will continue to lead the market. North America continues to dominate due to the rising demand for cryopreserved membranes and suspensions in wound care, ophthalmology, and orthopedic applications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific Amniotic Products Market Insights:

The fastest growing region is expected to be the Asia-Pacific region, which is expected to witness an impressive CAGR of 8.1% in 2026–2035. The expansion of healthcare infrastructure, increase in procedural volumes, favourable reimbursement scenario for regenerative medicine, growing awareness among end-users & patients, and increase in government initiatives to boost advanced medical technologies in China, Japan, India, and South Korea drive the market growth in Asia Pacific. The boom of the market in the region is attributed to fast urbanization, expanding hospital networks as well as the rise of local and international amniotic product providers.

Europe Amniotic Products Market Insights:

Europe contains the second largest share, aided through developed healthcare platforms, elevated clinical utilization and a powerful presence of key amniotic product manufacturers. Demand is high in Germany, the UK and France due to higher procedural volumes and increased investment in advanced wound care and ophthalmology therapies. Europe remains an attractive market supported by increasing demand for minimally invasive treateds, refined biologics, and integration of amniotic therapies into standard care pathways.

Latin America Amniotic Products Market Insights:

Latin America market is estimated to experience stable growth due to increasing healthcare spending, growing awareness about regenerative minute medicine, expanding hospitals and clinic infrastructure in Brazil, Mexico, and Argentina. Improved regulatory structures, clinical training, and partnerships with industry leaders have accelerated adoption of cryopreserved and dehydrated amniotic products. The growth of new emerging e-commerce and medical distribution channels is further enhancing the growth of the market.

Middle East & Africa (MEA) Amniotic Products Market Insights:

Increasing healthcare expenditure, rising procedural numbers, and growing awareness about regenerative medicine therapies in the UAE, Saudi Arabia, and South Africa are encouraging the MEA market growth. A robust hospital infrastructure, increasing disposable incomes, and collaboration with foreign amniotic product manufacturers are supporting adoption. This growth is being fueled by regulatory improvements and an increasing focus on advanced wound care and ophthalmic treatments in the region.

Amniotic Products Market Competitive Landscape:

MiMedx Group, Inc., based in Marietta, Georgia, is a global leader in placental biologics and regenerative medicine with a strong focus on advanced wound care, surgical recovery and chronic non‑healing wounds. The company develops and markets innovative placental tissue allografts derived from human amniotic membrane, umbilical cord and placenta using patented processing methods that preserve biological activity and healing potential.

-

In 2025, MiMedx advanced its clinical pipeline and reported increased adoption across wound and surgical care, highlighting its commitment to regenerative solutions and long‑term healing outcomes.

Organogenesis Holdings, Inc., headquartered in Canton, Massachusetts, is a leading regenerative medicine company specializing in advanced wound care, and surgical and sports medicine solutions. Its comprehensive product portfolio includes bioengineered therapies such as Apligraf and Dermagraft for chronic wounds, along with amniotic and placental tissue‑based products like Affinity, NuShield and NuCel that support healing across a spectrum of wound types and surgical applications.

-

Organogenesis continues to expand its regenerative offerings and production capabilities, reinforcing its position in the biologics market while supporting improved patient outcomes through innovative tissue solutions.

Amniotic Products Market Key Players:

-

MiMedx Group, Inc.

-

Organogenesis Holdings, Inc.

-

Integra LifeSciences Holdings Corporation

-

Smith & Nephew Plc

-

Stryker Corporation

-

BioTissue Holdings, Inc. (formerly TissueTech, Inc.)

-

Celularity Inc.

-

StimLabs LLC

-

Surgenex, LLC

-

Amnio Technology, LLC

-

Alliqua BioMedical Inc.

-

Applied Biologics LLC

-

Human Regenerative Technologies LLC

-

Skye Biologics Inc.

-

Amniox Medical Inc.

-

Katena Products Inc.

-

NuVision Biotherapies Ltd.

-

Merakris Therapeutics Inc.

-

VIVEX Biologics Inc.

-

LifeCell International Pvt. Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1050.95 Million |

| Market Size by 2035 | USD 2149.98 Million |

| CAGR | CAGR of 7.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Cryopreserved, Dehydrated) •By Product (Membranes, Suspensions) •By Application (Wound Care, Ophthalmology, Orthopedics, Others) •By End User (Hospitals, Specialized Clinics, Ambulatory Surgical Centers, Research Centers & Laboratory, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | MiMedx Group, Inc., Organogenesis Holdings, Inc., Integra LifeSciences Holdings Corporation, Smith & Nephew Plc, Stryker Corporation, BioTissue Holdings, Inc. (formerly TissueTech, Inc.), Celularity Inc., StimLabs LLC, Surgenex, LLC, Amnio Technology, LLC, Alliqua BioMedical Inc., Applied Biologics LLC, Human Regenerative Technologies LLC, Skye Biologics Inc., Amniox Medical Inc., Katena Products Inc., NuVision Biotherapies Ltd., Merakris Therapeutics Inc., VIVEX Biologics Inc., LifeCell International Pvt. Ltd. |

Frequently Asked Questions

Ans: The Amniotic Products Market is expected to grow at a CAGR of 7.42% during 2026–2035.

Ans: The Amniotic Products Market size was valued at USD 1050.95 Million in 2025 and is projected to reach USD 2149.98 Million by 2035.

Ans: The key drivers of the Amniotic Products Market include increasing adoption of regenerative medicine and biologic therapies, rising prevalence of chronic wounds and surgical procedures.

Ans: The Cryopreserved segment dominated the Amniotic Products Market.

Ans: North America dominated the Amniotic Products Market in 2025.

Get in Touch