Vaccine Adjuvants Market Report Scope & Overview:

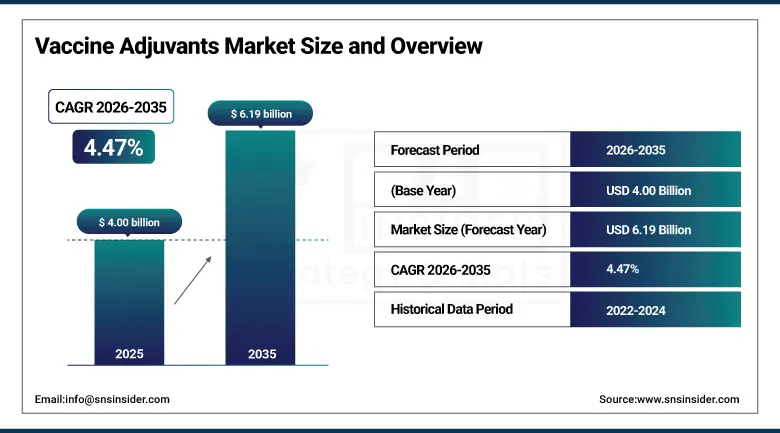

The Vaccine Adjuvants Market size was valued at USD 4.00 billion in 2025 and is expected to reach USD 6.19 billion by 2035, growing at a CAGR of 4.47% over the forecast period of 2025-2035.

Vaccine adjuvants market comprises products and techniques employed for boosting the efficacy of vaccines by stimulating the immunity of the body against antigens. Adjuvants are an integral part of the development process of vaccines since they boost immunogenicity, minimize antigen usage, and provide sustained immunity. The adjuvant technologies find extensive application in both prophylactic and therapeutic vaccines against various diseases such as infections, cancers, and others. The vaccine adjuvants market is on the rise because of the increasing emphasis on immunization worldwide. Constant innovations in vaccine development and the fast pace of development in biotechnology are driving the growth of next-generation adjuvant platforms. The rising popularity of recombinant, protein subunit, and nucleic acid vaccines is adding to the demand for advanced adjuvant systems that boost immune responses efficiently. Adjuvants with enhanced safety profiles, increased stability, and selective immune activation properties are being developed by manufacturers. Adjuvants based on nanotechnology and liposomes and combination adjuvants have become more prominent in contemporary vaccine development strategies. Moreover, increased public and private sector investment in pandemic readiness and vaccine innovation is paving the way for future market growth.

According to WHO, annual immunizations save 3.5-5 million lives each year; thus, the importance of technologies for improving vaccine efficacy like adjuvants cannot be overlooked. Studies conducted in clinical immunology indicate that use of new adjuvants allows enhancing the immune response 10-100 times as compared to conventional vaccines without adjuvants but allows decreasing the doses of antigens by 30-80%. According to CEPI, investments into vaccine research and development amount to more than USD 10 billion. Notably, most funds are devoted to developing novel vaccine platforms including mRNA and recombinant vaccines based on advanced adjuvants. Moreover, more than 40% of vaccines in the pipeline contain new adjuvants.

Market Size and Forecast

-

Market Size in 2026E: USD 4.18 Billion

-

Market Size by 2035: USD 6.19 Billion

-

CAGR: 4.47% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

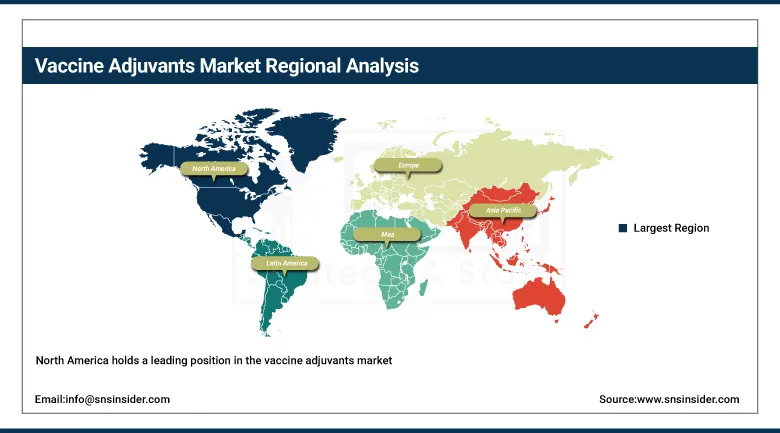

Largest Region: North America

To Get more information on Vaccine Adjuvants Market - Request Free Sample Report

Vaccine Adjuvants Market Trends

-

Enhanced uptake of nanoparticles and liposomal adjuvants has been increasing the efficacy of delivering antigens, activating the immune response, and resulting in increased durability of immunity among vaccine products against diseases, both infective and non-infective.

-

Increased focus on the use of combined adjuvants is leading to synergistic immunological reactions, increased potency of vaccines, and effective dose sparing in current vaccine development processes.

-

Increasing demand for vaccines such as mRNA and recombinant protein-based vaccines is increasing the adoption of more sophisticated adjuvants, guaranteeing better stability, selective immune responses, and increased efficiency of antigen expression.

-

Increased interest in the development of vaccines against cancers through immunotherapeutic means is boosting research in immunomodulating adjuvants to ensure selective immune activation and better response rates.

-

More investment in pandemic readiness is leading to increased studies on next generation adjuvants, which allow faster vaccine platforms, enhanced scalability, and rapid immunity from emerging disease outbreaks around the globe.

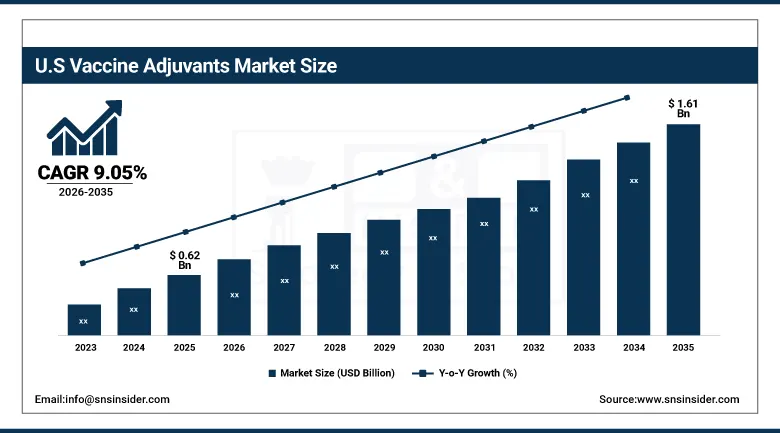

The U.S. Vaccine Adjuvants Market Size Outlook

The U.S. vaccine adjuvants market was valued at USD 0.62 billion in 2025 and is expected to reach USD 1.61 billion by 2035, growing at a CAGR of 9.05%.

The United States vaccine adjuvants market is driven by a highly advanced biopharmaceutical ecosystem, strong federal funding, and continuous vaccine innovation programs. Various entities, such as the NIH, BARDA, and the CDC, facilitate the development and testing of vaccines on a massive scale and prepare for any pandemics in the future. Among other countries, this nation has highly rated vaccine manufacturers and firms that concentrate on biotechnology. They invest a lot of money in incorporating the latest adjuvant technology in RNA vaccines, protein vaccines, and viral vaccines. This country is among those nations that have studied oncology vaccines. In the research, it was found out that oncology vaccines make use of immune system stimulators to increase tumor specificity and response. The next generation adjuvant technologies such as lipid nanoparticles and emulsions have been widely used to improve the efficacy and safety of the vaccines. There are also strict guidelines set by the FDA in the development and trials of adjuvants.

There are several aspects that significantly influence the growth of the U.S. vaccine adjuvants market, including federal support for biomedical research and vaccine development programs. In fact, government organizations, such as NIH, BARDA, and FDA, promote development and adoption of new vaccine technology in their research programs, which contributes to the growth of the discussed market. Due to immunization campaigns and pandemic readiness initiatives, there was an increased need for novel technologies that have become widely adopted within commercialized vaccines. Major pharmaceutical and biotechnological firms use new adjuvant technology in vaccines based on mRNA, recombinant proteins, and proteins.

Vaccine Adjuvants Market Segment Analysis

-

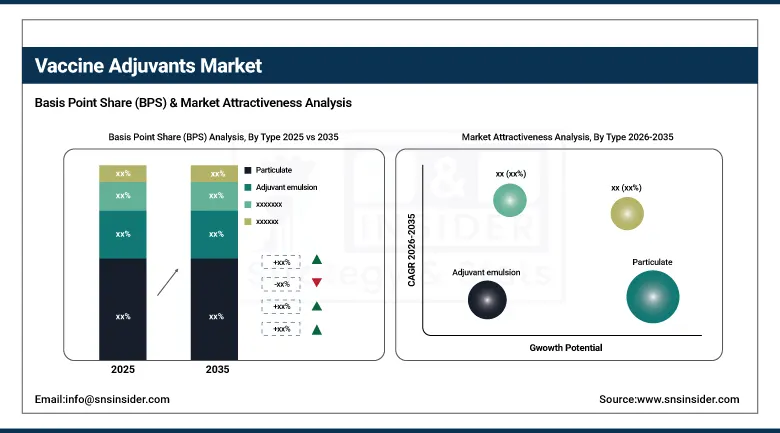

By Type, particulate dominated in 2025 with largest share, combination adjuvants growing rapidly.

-

By Application, infectious diseases dominated the market; cancer growing rapidly.

-

By Administration, intramuscular dominated; intradermal growing at above-average CAGRs.

By Type: particulate dominant, combination adjuvants grow fastest

Market leaders in the vaccine adjuvants industry for the year 2025 included particulate adjuvants on account of their efficient ability to activate the immune system as well as their safe nature as seen from their usage in commercial vaccines. Aluminum salts, emulsions, liposomes, and nanoparticles were some of the commonly used vaccines in the infectious diseases category due to their ability to facilitate antigen presentation and long-lasting immune responses. The use of these adjuvants was favored because of their scalability during manufacturing processes as well as regulatory acceptance.

Combination adjuvants are emerging very fast due to the increasing trend among vaccine developers to create effective and broad immunity by using innovative vaccine formulations. This type of technology utilizes several immunostimulant factors at once, which activates immune responses through diverse paths. With the increasing research on vaccines for cancer, pandemics, and future infectious diseases, there will be a great surge in the use of combination adjuvants, especially because of their potential in providing long-term immunity at lower doses.

By Administration, intramuscular dominated; intradermal growing at above-average CAGRs.

Regarding the vaccine adjuvants market, the segment related to intramuscular injection dominated in 2025 due to the popularity of this method in medical practice, the simplicity of its use, and its compatibility with various types of vaccine delivery systems, such as inactivated, protein-based, and mRNA-based. This type of administration ensures an effective stimulation of the immune response and is used on a large scale during various vaccination campaigns and routine vaccinations.

In contrast, the intradermal route is showing rapid growth on account of the dose sparing nature of this route of administration as well as the efficient immunogenicity that comes with it. The presence of antigen presenting cells in large numbers in the skin makes it possible to achieve immune responses through the use of small doses of antigens. It continues to gain popularity due to needle sparing technologies and advanced vaccine administration devices.

By Application, infectious diseases dominated the market; cancer growing rapidly.

Applications of adjuvants for infectious diseases were at the forefront in the global market in 2025 owing to the high demand for vaccines that can be used in various large-scale immunization programs around the world to combat conditions such as influenza, hepatitis, COVID-19, HPV, and pneumococcal diseases. Governments’ vaccination plans as well as investments made towards preparing for possible pandemics would continue to support robust growth in the demand for enhanced vaccines. Adjuvants facilitate efficient immunity while requiring less antigen usage.

Cancer vaccine applications are growing rapidly as immuno-oncology research advances and pharmaceutical companies accelerate development of therapeutic cancer vaccines. The use of adjuvants to evoke specific immune responses towards tumor-associated antigens is becoming more common. Market growth is being driven by investments made in personalized medicine, neoantigen-based vaccines, and combinations of treatment options. Participation in clinical trials and regulatory approval for innovative cancer treatments are other factors that are contributing to the rise in popularity. Higher prevalence of cancers across the globe guarantees business opportunities for innovative adjuvants in vaccine development.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87% |

|

Europe |

United Kingdom |

27% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

48% |

North America Vaccine Adjuvants Market Insights

North America holds a leading position in the vaccine adjuvants market due to strong biopharmaceutical R&D infrastructure, high healthcare spending, and early adoption of advanced vaccine technologies. The area enjoys substantial governmental investment from organizations such as NIH, BARDA, and CDC, which invests in the development of adjuvant-based vaccines and pandemic preparedness efforts. The influence of large pharmaceutical and biotech firms helps to develop new products related to vaccines based on adjuvants, especially mRNA technology, recombinant protein technology, and oncology indications. Excellent clinical trial infrastructure and solid regulatory structures in the U.S. FDA enable the fast but secure launch of innovative adjuvant vaccines. Increased interest in influenza vaccines, COVID-19 boosters, and cancer immunotherapies spurs market growth. At the same time, greater cooperation between academia and industry in research activities leads to innovations in adjuvant systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Vaccine Adjuvants Market Insights

Europe holds a significant share in the vaccine adjuvants market due to strong regulatory frameworks, advanced biotechnology capabilities, and robust government-supported vaccination programs. The European Medicines Agency (EMA) provides stringent assessment for vaccine safety and efficacy, thereby promoting the development of superior quality adjuvanted vaccines. Germany, France, and the UK are among the leading suppliers because of the presence of significant pharmaceutical research and development, along with collaboration with academia. The increasing significance of preparedness for pandemics and advances in immunotherapy will result in new developments in the coming generations of adjuvants, specifically cancer and infection vaccines. Increasing demand for mRNA vaccines and green manufacturing processes will further drive the market dynamics. Growth in the geriatric segment and vaccination campaigns during seasonal outbreaks will ensure steady demand in the region.

Asia Pacific Vaccine Adjuvants Market Insights

Asia Pacific is witnessing strong growth in the vaccine adjuvants market due to expanding immunization programs, rising infectious disease burden, and increasing vaccine manufacturing capacity. The nations like China and India are focusing a great deal on developing vaccines domestically and setting up mass production facilities. The government-led public health campaigns and innovations in biotechnology have increased the acceptance of state-of-the-art adjuvant systems. Cost-effective production centers and the involvement in international clinical trials increase the regional competitiveness further. The heightened awareness about preventive healthcare along with high demand for pediatric and adult vaccines are also important factors. In addition to this, the collaboration between multinational pharmaceutical companies and the local vaccine producers is helping to expedite the access to the next generation of vaccines.

MEA and Latin America Vaccine Adjuvants Market Insights

The Middle East & Africa market for vaccine adjuvants demonstrates consistent growth due to increasing vaccination programs, high prevalence of infections, and government health care initiatives. The countries within the Gulf region are building up their vaccine capabilities, whereas Africa is concentrating on massive health care campaigns with the help of international health agencies and making advancements in modern vaccines.

Latin America is witnessing moderate growth due to expanding vaccination coverage and increasing focus on infectious disease prevention programs. These two countries dominate in terms of demand because of their strong public health programs and production of vaccines. Through the use of international collaborations and better access to health care facilities, there is an increasing acceptance of advanced adjuvant vaccines despite the challenges associated with research and development.

Market Dynamics

Growth Drivers: Rising global immunization demand and next-generation vaccine development driving sustained vaccine adjuvants market growth globally

The market is experiencing high growth due to rising vaccination initiatives globally for infectious diseases, cancers, and emerging diseases. There is increasing interest in preventive medicine, and preparations are being made for potential pandemics. This has resulted in heavy investment in vaccine development from large drug makers and biotechnology companies. The rapid adoption of advanced generation vaccines such as mRNA, recombinant protein, and viral vector vaccines has increased the need for efficient adjuvants. Advancements in vaccine formulations in terms of nanoparticles, emulsions, and combination adjuvants are driving vaccine potency, dosing, and immunogenicity.

Restraints: High development complexity and stringent regulatory approval requirements constraining vaccine adjuvants market expansion globally

There are several major growth barriers in vaccine adjuvants market owing to the complicated process involved in developing the adjuvants as well as stringent regulatory guidelines in respect of safety and efficacy of vaccines. There must be extensive clinical testing to ensure that adjuvants are safe for biological use, which results in long development periods and increased costs for research and development. Regulatory agencies such as the FDA and EMA have stringent requirements for the approval of adjuvants, particularly novel or combinations of adjuvants, making the commercialization process difficult. Variation in the immune response among populations is also an issue. Moreover, difficulties in scaling up new adjuvant technology as well as safety issues like reactogenicity are further constraints to market growth.

Opportunities: Expanding oncology vaccines and next-generation immunotherapy platforms creating high-value opportunities in vaccine adjuvants market globally

The vaccine adjuvants market presents strong opportunities driven by the rapid expansion of cancer immunotherapy and personalized vaccine development. Growing emphasis on cancer therapy vaccines is fueling the need for next-generation adjuvants that can increase the efficiency of cancer-related immune responses and develop immune memory. The trend towards precision medicine and biomarker-targeted vaccine development is also driving increased acceptance of customized adjuvants. Furthermore, growing funding for RNA-based vaccines and next-generation infectious disease vaccines provides opportunities in the realm of innovative adjuvants. Moreover, emerging regions characterized by developing healthcare facilities and high vaccine coverage levels represent promising growth opportunities. Ongoing innovations in nanoscale delivery systems and combined adjuvants will create new possibilities, providing many years of commercial success for pharmaceutical companies worldwide.

Recent Developments:

-

2026: GSK expanded next-generation adjuvant optimization programs focused on enhancing AS01 and AS03 platforms for mRNA and protein subunit vaccines, achieving improved antigen dose-sparing effects and stronger T-cell mediated immune responses in late-stage clinical trials across infectious disease pipelines.

-

2026: Novavax advanced global commercialization of its Matrix-M adjuvant through expanded licensing partnerships with regional vaccine manufacturers, increasing adoption in influenza and pandemic preparedness vaccines while demonstrating improved durability of antibody response and enhanced cross-protection in updated clinical datasets.

-

2026: Dynavax Technologies accelerated adoption of its CpG 1018 TLR9 agonist adjuvant across combination vaccine candidates, with increased regulatory approvals in adult immunization programs and broader integration into next-generation hepatitis and oncology vaccine platforms targeting long-term immune memory enhancement.

Vaccine Adjuvants Market key players are:

-

CSL Limited

-

GlaxoSmithKline plc

-

Novavax, Inc.

-

Dynavax Technologies Corporation

-

Agenus, Inc.

-

Adjuvance Technologies, Inc.

-

InvivoGen

-

Phibro Animal Health Corporation

-

Brenntag Biosector

-

SPI Pharma

-

SEPPIC

-

Croda International plc

-

OZ Biosciences

-

Aurorium

-

Hawaii Biotech Inc.

-

Sanofi

-

Merck & Co., Inc.

-

Pfizer Inc.

-

Johnson & Johnson

-

3M Health Care

Vaccine Adjuvants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.00 Billion |

| Market Size by 2035 | USD 6.19 Billion |

| CAGR | CAGR of 4.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Adjuvant emulsion, Pathogen, Combination, Particulate, and Others) • By Administration (Oral, Intramuscular, Intradermal, Intranasal, and Others) • By Application (Cancer, Infectious diseases, and Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | CSL Limited, GlaxoSmithKline plc, Novavax, Inc., Dynavax Technologies Corporation, Agenus, Inc., Adjuvance Technologies, Inc., InvivoGen, Phibro Animal Health Corporation, Brenntag Biosector, SPI Pharma, SEPPIC, Croda International plc, OZ Biosciences, Aurorium, Hawaii Biotech Inc., Sanofi, Merck & Co., Inc., Pfizer Inc., Johnson & Johnson, 3M Health Care |

Frequently Asked Questions

Ans: The Vaccine Adjuvants Market was valued at USD 4.00 billion in 2025.

Ans: Asia Pacific is the fastest growing; North America holds a significant position.

Ans: Infectious Diseases dominated the market and Cancer growing rapidly.

Ans: Particulate dominated the market in 2025; Combination Adjuvants is growing at the fastest CAGR.

Ans: The Vaccine Adjuvants Market is expected to grow at a CAGR of 4.47% from 2026 to 2035.

Get in Touch