Value-Based Healthcare Services Market Report Scope & Overview:

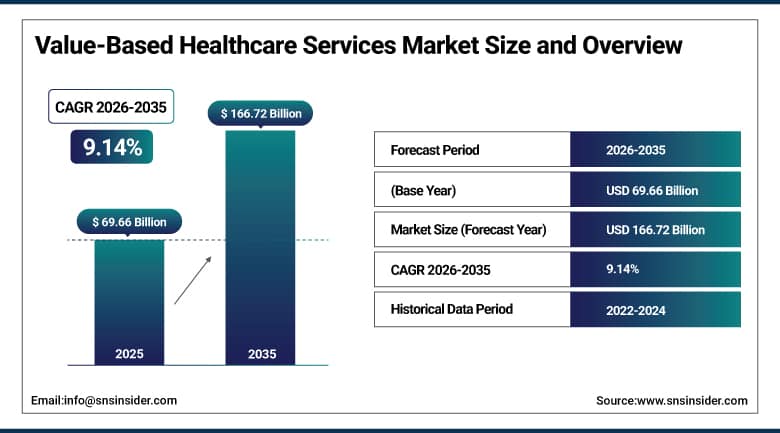

The Value-Based Healthcare Services Market was valued at USD 69.66 billion in 2025 and is expected to reach USD 166.72 billion by 2035, growing at a CAGR of 9.14% from 2026–2035.

The value-based healthcare services market is witnessing strong growth in the global market owing to the increasing shift toward outcome-based reimbursement models and quality driven care delivery systems. The rising prevalence of chronic diseases and aging population is promoting the adoption of care coordination, patient engagement, and population health management solutions across healthcare systems. Investments made by healthcare providers and payers in digital health technologies, data analytics, and electronic health records are contributing to market growth. Increasing developments in telemedicine, wearable health devices, and health information exchange are playing a major role in driving the demand for services. Growth in healthcare spending and regulatory reforms focused on cost efficiency are fueling the demand for market.

As per the OECD Health System and the U.S. Centers for Medicare & Medicaid Services for value-based care for 2025, over 60% of Medicare payments are currently based on other payment methods, such as accountable care organizations and bundling programs. According to WHO Global Health Observatory data, over 70% of nations have instituted nationally-based quality-driven systems in their health sectors, which have patient results, readmissions, and preventative care under consideration.

Market Size and Forecast:

-

Market Size 2026E: USD 75.89 billion

-

Market Size 2035: USD 166.72 billion

-

CAGR (2026 - 2035): 9.14%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Value-Based Healthcare Services Market - Request Free Sample Report

Value-Based Healthcare Services Market Trends:

-

Digital health ecosystems expand rapidly, enabling integrated value-based healthcare services through connected platforms, real time monitoring, and data exchange systems.

-

Artificial intelligence adoption grows in predictive analytics, supporting early disease detection and improving clinical decision-making accuracy across healthcare systems.

-

Telemedicine usage increases significantly, improving access to care in remote regions and reducing dependency on physical hospital visits globally.

-

Wearable health devices become widely adopted, enabling continuous patient monitoring and supporting preventive care and chronic disease management.

-

Population health management systems expand to reduce hospital readmissions, improve coordination, and optimize long term healthcare outcomes efficiently.

-

Insurance providers increasingly promote preventive care models, encouraging cost reduction strategies and supporting value-based healthcare service adoption globally.

U.S. Value-Based Healthcare Services Market Size Outlook:

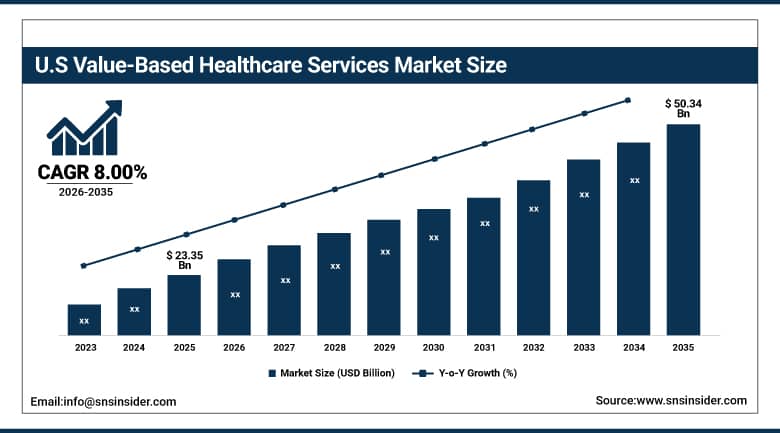

The U.S. Value-Based Healthcare Services Market was valued at USD 23.35 billion in 2025 and is expected to reach around USD 50.34 billion by 2035, growing at a CAGR of 8.00% from 2026–2035.

The U.S. value-based healthcare services market is growing consistently owing to increased shift toward outcome-based reimbursement models and coordinated care delivery systems. The usage of value-based healthcare services in hospitals, physicians, and outpatient care centers has contributed to market growth in a consistent manner. Increased spending in healthcare digitalization and population health management adoption has generated an increase in demand for integrated care solutions. Development of telemedicine, electronic health records, and predictive data analytics is further driving the demand for this market.

According to the Centers for Medicare & Medicaid Services 2025 Quality Payment Program performance, over 90% of Medicare payments are now tied to value-based care arrangements, including alternative payment models and quality reporting systems. The U.S. Health Resources and Services Administration also reports that more than 50% of primary care practices are engaged in accountable care organization structures, reflecting continued expansion of value-based healthcare service adoption in 2025.

Value-Based Healthcare Services Market Segment Analysis:

-

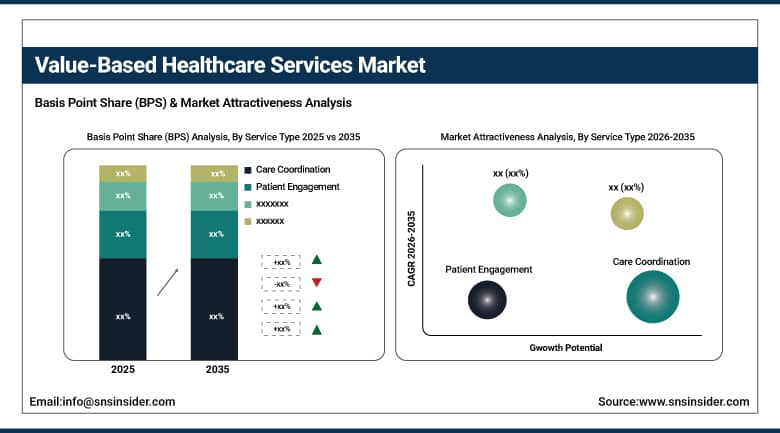

By Service Type, care coordination dominated the market with 38.50% share in 2025; while patient engagement is the fastest growing segment with CAGR of 11.46% during 2026 to 2035.

-

By Technology, electronic health records dominated the market with 42.80% share in 2025; while telemedicine is the fastest growing segment with CAGR of 12.56% during 2026 to 2035.

-

By Payer Type, private insurance dominated the market with 41.80% share in 2025; while public insurance is the fastest growing segment with CAGR of 11.14% during 2026 to 2035.

-

By Provider Type, hospitals dominated the market with 46.70% share in 2025; while physicians are the fastest growing segment with CAGR of 11.84% during 2026 to 2035.

By Service Type, care coordination dominated the value-based healthcare services market, while patient engagement is the fastest growing segment.

The Care Coordination segment led the value-based healthcare services market with the dominated revenue share in 2025. This is due to increased usage of coordinated care models and growing emphasis on avoiding readmissions. The adoption of coordinated processes by hospitals, physicians, and payers has become a priority in enhancing efficiency. In addition, growing cases of chronic diseases and the need for coordinated care programs add to its dominant position in the market.

The Patient Engagement segment is forecasted to witness the fastest growth during the forecast period 2026 to 2035 because of the rise in digital health applications and mobile applications. Increased patient awareness about self-management and preventive healthcare adds to the growth of this segment. The use of telehealth technology, wearables, and communication technologies boosts patient engagement. Efforts made by healthcare organizations to improve their satisfaction score have led to the fast growth of this segment.

By Technology, electronic health records dominated the value-based healthcare services market, while telemedicine is the fastest growing segment.

Electronic Health Records segment ruled the market with the dominated revenue share in 2025. The high revenue share was attributed to the increasing digital revolution in the healthcare industry along with the use of standardized patient record keeping. Electronic health records were used by hospitals and physicians to manage and monitor healthcare services. Other factors that helped boost its revenue share were interoperable solutions and supportive government policies. Analytics and reimbursements were other factors that boosted its leadership.

Telemedicine segment would show the fastest CAGR during the forecast period owing to the growing demand for accessing remote healthcare and virtual consultations. The increasing burden of chronic diseases and the shortage of healthcare professionals would further accelerate its adoption. Patient preference for cost-effective, convenient, and time-saving models of care would help its growth. Development of digital healthcare infrastructure and mobile health technologies would boost its performance in the coming years.

By Payer Type, private insurance dominated the value-based healthcare services market, while public insurance is the fastest growing segment.

Private insurance sector accounted for the dominated share of revenues in the value-based healthcare services market in 2025. This is due to the wide use of the value-based reimbursement approach. The fast adoption of performance-based payments systems is being witnessed among private insurers. Their main aim is to ensure that they reduce avoidable hospital admissions and increase better patient outcomes. Financial stability and the incorporation of digital health technology increase the adoption rate. Employer sponsored health insurance programs also contribute to the sector's dominance.

Public insurance sector will witness the fastest CAGR between 2026 and 2035. This will be fueled by increasing governmental reforms within the health sector and the rising need to control costs. Increasingly, there will be more implementation of the value-based care approach. This will be driven by growing chronic diseases and an aging population. Investments are made in digital health facilities and preventive measures. The expansion of universal healthcare also speeds up adoption.

By Provider Type, hospitals dominated the value-based healthcare services market, while physicians are the fastest growing segment.

Hospitals were the leading segment in the Value Based Healthcare Services market, generating the dominated market share in terms of revenue in 2025. This leadership was a result of the high adoption rates of the value-based reimbursement model. Hospitals need complex care delivery systems that deal with large amounts of patients. The use of electronic health records and data analytics improves treatment results. Government programs and changes in the insurance landscape have made hospitals more inclined towards implementing population health management systems.

Physicians segment is projected to register the fastest CAGR from 2026 to 2035 owing to the increasing trend towards outpatient and primary based value care systems. There is a rise in the number of physicians who opt for telemedicine and digitized healthcare options. An emphasis on prevention of diseases and their management increases the uptake rate. Practices of physicians adopt decision-making approaches based on data analysis.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

86.40% |

|

Europe |

Germany |

27.50% |

|

Asia Pacific |

China |

38.00% |

|

Middle East & Africa |

UAE |

18.50% |

|

Latin America |

Brazil |

47.50% |

North America Value-Based Healthcare Services Market Insights.

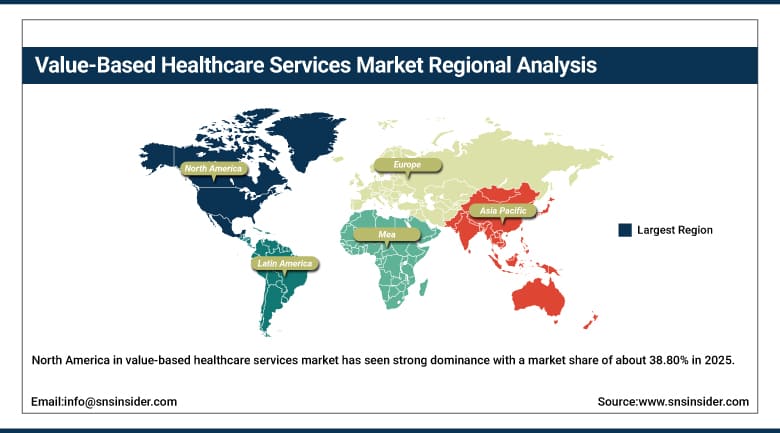

North America in value-based healthcare services market has seen strong dominance with a market share of about 38.80% in 2025 due to advanced healthcare infrastructure and high adoption of outcome-based reimbursement models. The region benefits from strong demand in care coordination, population health management, and data analytics solutions. Increasing demand for chronic disease management and preventive healthcare services is driving market expansion across the United States and Canada. Rising adoption of digital health platforms and telemedicine is further supporting market leadership. Strong policy support is strengthening value-based care transformation.

According to the Centers for Medicare & Medicaid Services 2025 value-based care performance data, over 51% of traditional Medicare payments in the United States are now tied to alternative payment models, including accountable care organizations and bundled payment arrangements. As per CMS Quality Payment Program reporting, approximately 88% of eligible clinicians participated in either Advanced Alternative Payment Models or Merit-based Incentive Payment System frameworks in 2024.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Value-Based Healthcare Services Market Insights.

The Europe value-based healthcare services market shows strong presence in 2025 due to strict healthcare regulations and increasing focus on cost efficient care delivery systems. Countries like Germany, France, United Kingdom, and Italy are key contributors to demand. High focus on aging population care, chronic disease management, and hospital efficiency is supporting steady market growth across the region. Increasing adoption in electronic health records, integrated care systems, and telemedicine is further strengthening service utilization. Expanding digital health frameworks are driving advanced value-based healthcare adoption.

According to the OECD health system performance 2025, unnecessary hospitalizations in relation to chronic ailments like diabetes and asthma in well-performing EU countries have been reported at reductions up to 25%-40%. Moreover, over 95% of European Union populations are covered by universal health care plans, thus providing an organized approach to performance-related payments.

Asia Pacific Value-Based Healthcare Services Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the value-based healthcare services market during the forecast period with a market share of about 11.34% in 2025. Rapid healthcare infrastructure expansion and increasing digital health adoption are driving strong demand across China, Japan, India, South Korea, and Southeast Asia. Expanding hospital networks, rising patient population, and growing focus on preventive care are significantly boosting adoption. Rising demand for affordable healthcare delivery models is further accelerating market growth across the region. Large scale government healthcare reforms support strong regional demand outlook.

According to the WHO and the OECD Health at a Glance Asia/Pacific 2025, there is an increase in the adoption of value-based care within the Asia-Pacific region, with over 27 countries adopting performance measurement systems that link outcomes to services. According to WHO Western Pacific regional policy guidelines, more than 60 percent of national health policies in the region adopt people-centered health care and outcome-based primary health care indicators.

Middle East & Africa and Latin America Value-Based Healthcare Services Market Insights.

The Middle East & Africa and Latin America value-based healthcare services market is witnessing steady growth due to rising healthcare modernization and increasing adoption of digital health systems. Countries like Brazil, Mexico, UAE, Saudi Arabia, and South Africa are emerging as key demand centers. Increasing investments in hospital infrastructure, outpatient care, and health insurance systems are supporting market expansion. Growing need for efficient care delivery and chronic disease management is further boosting service adoption. Rising healthcare access and government reforms strengthen long term demand outlook across both regions.

According to the World Health Organization 2025 Global Health Expenditure and Service Delivery Monitoring Framework and Universal Health Coverage by the World Bank, the Middle East and North African region show UHC service coverage index values between around 54 and 78, while the Latin America and Caribbean region show values between 66 and 82.

As per WHO–World Bank UHC monitoring updates, the financial protection gap is high as out-of-pocket spending for health services constitutes more than 25% of health expenditure in many countries, and around 4.6 billion people around the globe have no full coverage of essential health services.

Market Dynamics:

Growth Drivers: Increasing Burden of Chronic Diseases and Aging Population Driving Demand for Coordinated Care Systems

There is an increase in the number of chronic diseases like diabetes, heart disease, and respiratory problems. The need for proper coordination of healthcare services arises because of the aging population that requires monitoring and management. Health organizations make use of population health management system so as to minimize re-admission in hospitals. Decision-making is data based in order to make proper diagnosis and plan for treatment. Telemedicine and remote patient monitoring increase accessibility. Insurance companies embrace preventive medicine approach due to reduction in costs.

As per the WHO & Global Health Estimates 2025, NCDs make up 74% of all deaths worldwide, whereas just cardiovascular diseases make up around 32%. As stated in the OECD Health Statistics 2025, more than 60% of the member countries have introduced value-based care or coordinated care pilots aimed at the management of chronic diseases. This indicates the growing presence of integrated healthcare delivery systems due to aging population and increasing prevalence of diseases.

Restraints: Data Privacy Concerns and Lack of Standardized Healthcare Data Integration Systems

Growing use of digital healthcare solutions poses risks with regards to the privacy and security of patient data. Data breaches and potential data leaks threaten the integrity of confidential information of patients. There is an absence of a standardized system for data exchange, thereby limiting interoperability among payers and providers of healthcare services. The healthcare IT ecosystem poses issues related to efficiency. There is no uniform health information exchange system which results in inefficient use of data in real-time. Cybersecurity threats pose risks to digital health solutions.

Opportunities:Expansion of Digital Health Ecosystems and Artificial Intelligence Driven Healthcare Analytics Adoption

Fast-growing digital health ecosystems provide great prospects for value-based healthcare services' adoption. Artificial intelligence is applied to enable predictive analysis and early disease detection. Data-driven decision-making processes are employed by health care facilities. Telemedicine platforms facilitate access to services in remote locations. Wearable health devices ensure patients' monitoring and real-time health assessment. Health information management systems based on cloud technologies provide more efficient exchange of data. Investment in health care IT infrastructure stimulates innovations. All of these improvements greatly contribute to better care coordination and treatment results worldwide.

According to the Health by OECD 2025 and WHO Global Health Observatory Database, in excess of 90% of countries belonging to the Organization for Economic Co-operation and Development have established national digital health strategies incorporating electronic health records and information sharing mechanisms, thus providing the foundations for value-based care frameworks.

According to WHO Digital Health Adoption Indicators 2025, more than 60% of the nations have adopted the use of artificial intelligence-supported decision-making aids in their clinical operations. The US CDC indicate the penetration rate of EHRs in healthcare facilities above 95%, whereas CMS value-based payment initiatives account for over 50% of payments from Medicare.

Recent Developments:

-

2026: Elevance Health accelerated enterprise AI deployment strategy including agentic AI expansion plans across claims, benefits, and care management workflows.

-

2025: Oracle Corporation launched AI-powered EHR and payer-provider interoperability tools to improve value-based care coordination and reduce administrative burden.

-

2025: CVS Health expanded Aetna cost management initiatives while improving pharmacy services integration across retail clinics and insurance-linked care delivery systems.

-

2024: UnitedHealth Group addressed Change Healthcare cyberattack impacts while accelerating Optum technology resilience and digital claims processing restoration efforts.

Value-Based Healthcare Services Market Key Players are:

-

UnitedHealth Group

-

CVS Health

-

Cigna Group

-

Humana Inc.

-

Elevance Health

-

Centene Corporation

-

Kaiser Permanente

-

Teladoc Health

-

Oracle Corporation

-

Epic Systems Corporation

-

Siemens Healthineers

-

GE HealthCare

-

Koninklijke Philips

-

Medtronic

-

Abbott Laboratories

-

Microsoft Corporation

-

Alphabet Inc.

-

Amazon.com Inc.

-

IBM

-

McKesson Corporation

Value-Based Healthcare Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 69.66 Billion |

| Market Size by 2035 | USD 166.72 Billion |

| CAGR | CAGR of 9.14% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Care Coordination, Patient Engagement, Data Analytics, Population Health Management) • By Technology (Electronic Health Records, Telemedicine, Wearable Health Devices, Health Information Exchange) • By Payer Type (Private Insurance, Public Insurance, Government Programs, Self-Pay) • By Provider Type (Hospitals, Physicians, Outpatient Care Centers, Long-term Care Facilities) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | UnitedHealth Group, CVS Health, Cigna Group, Humana Inc., Elevance Health, Centene Corporation, Kaiser Permanente, Teladoc Health, Oracle Corporation, Epic Systems Corporation, Siemens Healthineers, GE HealthCare, Koninklijke Philips, Medtronic, Abbott Laboratories, Microsoft Corporation, Alphabet Inc., Amazon.com Inc., IBM, McKesson Corporation |

Frequently Asked Questions

The value-based healthcare services market is expected to grow at a CAGR of 9.14% from 2026 to 2035.

The value-based healthcare services market was valued at USD 69.66 billion in 2025.

Major growth factors include shift to outcome-based reimbursement, chronic disease rise, aging population, and digital health technology adoption globally.

Care coordination segment dominated the market in 2025 due to increasing adoption of integrated care models improving outcomes and reducing readmissions.

North America dominated the value-based healthcare services market due to advanced healthcare infrastructure, strong reimbursement adoption, and digital health penetration.

Get in Touch