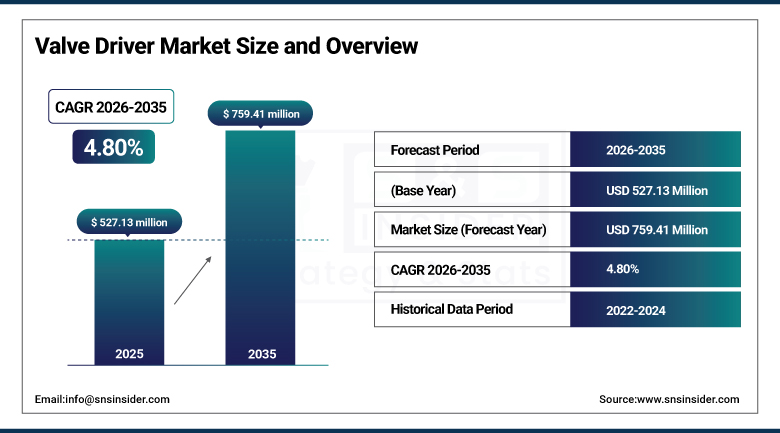

Valve Driver Market Report Scope & Overview:

The Valve Driver Market was valued at USD 527.13 Million in 2025 and is expected to reach USD 759.41 Million by 2035, growing at a CAGR of 4.80% from 2026 to 2035.

The growth drivers of the market include the increased adoption of advanced valve control technologies such as digital valve drivers for enhanced automation capabilities and remote monitoring functions. Growing trends towards energy efficiency among industries are another factor driving the growth of the market as there is increased demand for energy efficient valve control mechanisms. Increasing integration of valve drivers in predictive maintenance systems with the help of IoT and AI is adding to the rising demand for valve drivers due to cost savings and system reliability. Valves control technology innovation and regulation/standards compliance requirements also serve as growth drivers of the market.

In 2024, Emerson Electric Co. introduced new connectivity capabilities in its Fisher FIELDVUE digital valve controller platform to allow real-time monitoring of valve performance as well as predictive maintenance alerts in industrial process control applications. This innovation reflects the commercial trend of the valve driver market towards connected intelligent valves creating service-based value beyond mere transaction of the product purchase for industrial clients.

Market Size and Forecast

-

Market Size in 2026E: USD 552.44 Million

-

Market Size by 2035: USD 759.41 Million

-

CAGR: 4.80% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Valve Driver Market - Request Free Sample Report

Valve Driver Market Trends

-

Increasing adoption of digital valve drivers enabling greater automation and remote monitoring is accelerating market growth as industrial operators seek real time visibility into valve performance across complex process control systems.

-

Integration of valve drivers with IoT and predictive maintenance systems is boosting demand by reducing unplanned downtime and maintenance costs, with connected valve drivers providing continuous performance data that enables condition based servicing.

-

Rising demand for proportional valve drivers offering precise, variable flow control is growing in hydraulic and pneumatic systems across manufacturing, automotive, and aerospace applications where on off solenoid functionality is insufficient.

-

Growing emphasis on energy efficiency in commercial HVAC and industrial process control applications is driving adoption of electronically controlled valve drivers that optimize fluid and gas flow to minimize energy consumption.

-

Expansion of renewable energy infrastructure including wind turbines and solar thermal systems is creating new valve driver application categories where precise fluid control is critical for system performance and longevity.

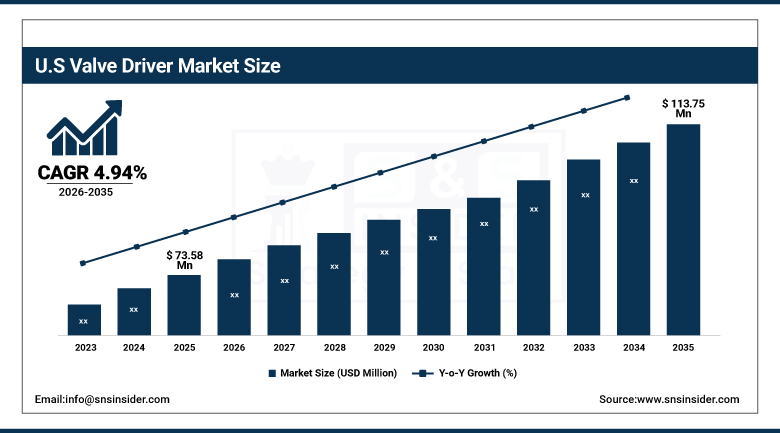

U.S. Valve Driver Market Outlook

The U.S. Valve Driver Market was valued at approximately USD 73.58 Million in 2023 and is expected to reach approximately USD 113.75 Million by 2032, growing at a CAGR of approximately 4.94%.

The U.S. market is advantageous because it boasts a robust industrial infrastructure, high adoption of process automation solutions, and stringent energy efficiency and safety standards, which increase the need for valve control technologies. In addition, the availability of valve driver vendors and system integrators, along with steady investments in the construction of oil and gas facilities, chemicals industry, and power generation infrastructure, ensures structural procurement need in both replacement and new installations. Integration with the predictive maintenance system that uses IoT and AI solutions is especially relevant in the U.S. market, where efficiency and lack of downtime have an obvious financial benefit.

In 2023, Carel Industries S.p.A. launched an enhanced electronic expansion valve driver series for commercial refrigeration and HVAC applications, offering improved control algorithms and communication protocols compatible with modern building management systems. The product launch demonstrates the ongoing commercial evolution of the expansion valve driver segment, where building energy management requirements and refrigerant transition obligations are creating structured demand for electronically controlled valve solutions with enhanced communication and monitoring capability.

Valve Driver Market Segment Analysis

-

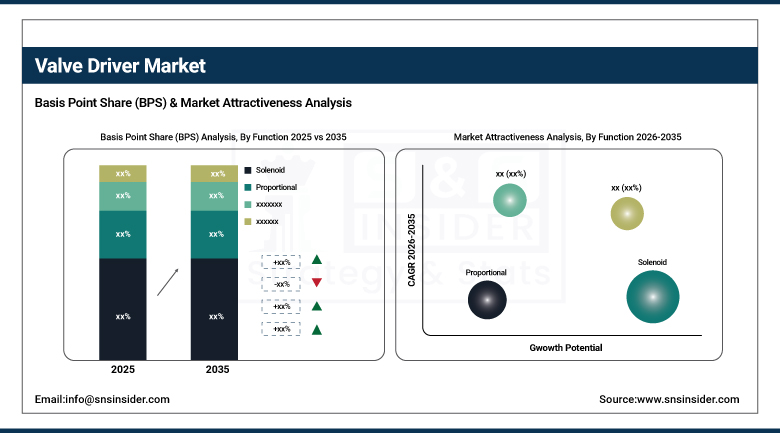

By Function, the Solenoid segment dominated the Valve Driver Market in 2025 and captured approximately 51.00% of total market share, while the Proportional segment is expected to be the fastest growing during the forecast period.

-

By Valve Type, the Conventional Control Valve segment dominated the Valve Driver Market with approximately 58.00% share in 2025, while the Expansion Valve segment continues to gain traction across HVAC and refrigeration applications.

-

By End User, the Industrial segment dominated the Valve Driver Market with approximately 72.00% share in 2025, while the Commercial and Residential segment continues growing with increasing adoption of smart HVAC and building automation systems.

By Function, solenoid dominates, proportional grows fastest

The solenoid type of valve drivers had the highest share in the valve driver market in 2025, accounting for 51%. This particular component finds wide application in controlling the movement of fluids in numerous industrial applications due to its highly efficient operation and reliability. One of the benefits of using solenoid valves in valve drivers is that they allow one to have a precise on-off control over the valve, thus making solenoid valves ideal for such industries as oil and gas, automotive, water treatment, and HVAC. Moreover, the main characteristics of solenoid valves include high speed and high durability.

In 2026 to 2035, the proportional segment will become the fastest-growing segment of the valve driver market. Proportional valve drivers enable users to have precise variable control over flow rates and pressures. Therefore, proportional valve drivers are required when an operator needs not only on and off control but also a variable control over the output flow rate and pressure. Such industries as mobile hydraulics, industrial automation, and precise fluid control utilize such valve drivers. Every time there is an industrial system that has performance requirements greater than those of a binary valve driver, proportional valve driver purchase is made.

By Valve Type, conventional control valve dominates, expansion valve grows

Conventional control valves retained the dominant valve type position in the valve driver market in 2025. Their widespread use across oil and gas, petrochemical, power generation, and water treatment industries reflects these sectors' dependence on reliable, durable flow regulation for safety critical and production critical process control applications. Each process plant and utility installation whose operation requires precise throttling of liquid, gas, or steam flow creates conventional control valve driver procurement whose commercial aggregate across the global industrial process sector sustains this valve type's commanding market position.

Expansion valves are primarily used in refrigeration and HVAC systems to control the flow of refrigerant, ensuring optimal cooling efficiency. The increasing need for energy efficiency and climate control solutions is contributing to this segment's expansion. The global transition from HFC refrigerants to lower GWP alternatives is also creating structured replacement demand for expansion valve and driver systems in existing refrigeration and HVAC installations, adding structured near term commercial momentum to the segment's underlying growth trajectory.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

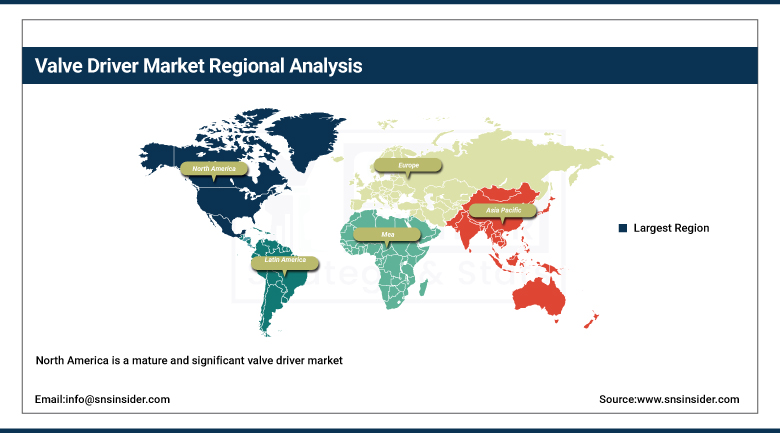

North America Valve Driver Market Insights

North America is a mature and significant valve driver market, driven by a strong industrial base, widespread adoption of process automation technologies, and stringent energy efficiency regulations. The United States accounts for approximately 87.4% of North American revenues through Emerson Electric, Eaton Corporation, Parker Hannifin, and other major industrial technology companies whose valve driver commercial operations sustain regional market leadership.

Canada contributes complementary North American revenue through its oil sands and natural gas processing industries that create structured demand for advanced valve control solutions across complex fluid management applications.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Valve Driver Market Insights

Europe is a technically sophisticated valve driver market where EU energy efficiency directives and process safety regulations create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its strong automotive and chemical manufacturing base and high industrial automation adoption that creates consistent valve driver procurement across process and discrete manufacturing applications.

The United Kingdom and France are significant secondary markets where established oil and gas and chemical industries and growing HVAC system modernization investment create consistent procurement. Bosch Rexroth's German operations and other European automation manufacturers sustain regional commercial supply.

Asia Pacific Valve Driver Market Insights

Asia Pacific is expected to witness the fastest CAGR during the forecast period, driven by rapid industrialization, increasing infrastructure projects, and growing adoption of automation technologies in countries like China, India, and Japan. Rapid urbanization and rising construction of commercial and industrial facilities are creating growing demand for valve driver solutions across HVAC, water treatment, and process control applications. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary industrial manufacturing scale.

India represents the most commercially dynamic emerging market within Asia Pacific where growing manufacturing automation investment and expanding infrastructure development create above average regional valve driver procurement growth, with the country's increasing focus on water treatment infrastructure adding structured demand for solenoid and control valve driver solutions.

MEA & Latin America Valve Driver Market Insights

Valves in Saudi Arabia dominate MEA revenues due to their huge processing capacity for oil and gas needing sophisticated valve controls. Increasing industrial and construction activities in the UAE add to this regional market development. In Latin America, valves in Brazil dominate the regional revenue generation due to the presence of large scale oil & gas and chemicals production activities demanding continuous procurement of valve drivers. Increased activities in Mexico's manufacturing sector and water/wastewater infrastructure, as well as growth in Argentina's energy sector, ensure market development till 2035.

Market Dynamics

Growth Drivers: Industrial automation expansion and IoT-enabled predictive maintenance

The development of industrial infrastructures in oil and gas, automotive, and chemical industries keeps expanding and there is a growing demand for more sophisticated valve control systems due to the increasing complexity of the processes involved. The industries require very efficient valve drivers to ensure optimal production, safety and compliance with strict regulations. As the pace of the infrastructure development rises, including in developing countries, the demand for more sophisticated valve control solutions grows resulting in the growth of the market. Valve drivers are used to control the flow of fluid and gas, and therefore are very important in large-scale operations.

IoT technology in valve drivers transforms industries due to the possibility of remote monitoring and automation as well as predictive maintenance. Valve drivers with IoT capabilities can be integrated into industrial and building control systems and automate the flow of fluids and gases. With IoT, the predictive maintenance becomes possible which results in lower downtimes because of the identification of equipment deterioration before it fails. Automation and remote control capabilities significantly cut down costs of operation, while increased safety and accuracy make IoT valve drivers productivity multipliers in industrial process applications.

Restraints: Legacy system integration complexity

The introduction of valve drivers with already existing systems, especially legacy systems, poses many difficulties. Many old systems did not have any provision for incorporating any sort of digital systems. Therefore, the incorporation of new digital valves would require a lot of modification to be done. Incompatibilities of valve drivers with other control systems and sensors may pose problems.

Many companies experience problems in integrating valve drivers with their already existing control systems. It becomes difficult because legacy systems do not have any standard and hence the problem of integration of valve drivers. Such problems arise especially during retrofit projects where legacy distributed control systems become an obstacle for valve drivers installation.

Opportunities: Smart building and energy efficiency mandates

The integration of valve drivers with IoT and smart technologies presents significant market opportunity. As industries across sectors like oil and gas, manufacturing, and automotive evolve, there is increasing demand for specialized valve solutions tailored to unique operational needs. The growing commercial and residential construction market creates rising demand for intelligent HVAC valve control solutions that reduce energy consumption and improve building performance against increasingly stringent energy efficiency standards.

Energy efficiency trends are pushing manufacturers to develop valve driver solutions that minimize energy consumption without compromising performance. Each building or industrial facility whose energy management program identifies valve control optimization as a lever for consumption reduction creates structured procurement for advanced electronically controlled valve drivers. Government energy efficiency mandates and utility incentive programs further accelerate this market opportunity across both developed and emerging economies.

Recent Developments:

-

2024: Emerson Electric Co. expanded its Fisher FIELDVUE digital valve controller platform in 2024 with enhanced IoT connectivity for real time valve performance monitoring and predictive maintenance alerts.

-

2023: Carel Industries S.p.A. launched an enhanced electronic expansion valve driver series in 2023 for commercial refrigeration and HVAC applications with improved control algorithms and BMS communication protocols.

-

2024: Parker Hannifin Corporation expanded its proportional valve driver product range in 2024 with new high force solenoid valve drivers targeting mobile hydraulics and industrial automation applications.

-

2023: Eaton Corporation expanded its AxisPro proportional valve driver platform in 2023 with enhanced diagnostic and condition monitoring features for hydraulic machine tool and press applications.

-

2024: Bosch Rexroth AG introduced new smart electronics for proportional directional valve control in 2024, incorporating enhanced condition monitoring and fieldbus communication protocols for Industry 4.0 integration.

Valve Driver Market Key Players

-

Emerson Electric Co.

-

Eaton Corporation plc

-

Parker Hannifin Corporation

-

Bosch Rexroth AG

-

Danfoss A/S

-

Carel Industries S.p.A.

-

Clippard Instrument Laboratory Inc.

-

Applied Processor and Measurement Inc.

-

Bucher Hydraulics Inc.

-

Fluidotronica SL

-

IMI plc

-

SMC Corporation

-

Festo AG & Co. KG

-

Asco Numatics (Emerson)

-

Honeywell International Inc.

-

Siemens AG

-

ABB Ltd.

-

Norgren Ltd. (IMI)

-

Metal Work S.p.A.

-

Koganei Corporation

Valve Driver Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 527.13 Million |

| Market Size by 2035 | USD 759.41 Million |

| CAGR | CAGR of 4.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Function (Solenoid, Proportional) • by Valve Type (Conventional Control Valve, Expansion Valve) • by End User (Commercial, Residential, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Emerson Electric Co., Eaton Corporation plc, Parker Hannifin Corporation, Bosch Rexroth AG, Danfoss A/S, Carel Industries S.p.A., Clippard Instrument Laboratory Inc., Applied Processor and Measurement Inc., Bucher Hydraulics Inc., Fluidotronica SL, IMI plc, SMC Corporation, Festo AG & Co. KG, Asco Numatics (Emerson), Honeywell International Inc., Siemens AG, ABB Ltd., Norgren Ltd. (IMI), Metal Work S.p.A., Koganei Corporation |

Frequently Asked Questions

North America is a dominant and mature valve driver market, while Asia Pacific is expected to witness the fastest CAGR driven by rapid industrialization and growing automation adoption.

The Valve Driver Market is expected to grow at a CAGR of 4.80% from 2026 to 2035.

Industrial expansion across oil and gas, automotive, and chemical industries driving demand for advanced valve control systems to manage increasingly complex processes, and the integration of IoT and predictive maintenance technologies enabling remote monitoring, automation, and condition based servicing that reduces operational costs.

The Solenoid segment dominated the Valve Driver Market in 2025 with approximately 51% of total market share, while the Proportional segment is expected to be the fastest growing segment.

Get in Touch