Veterinary CRO and CDMO Market Report Scope & Overview:

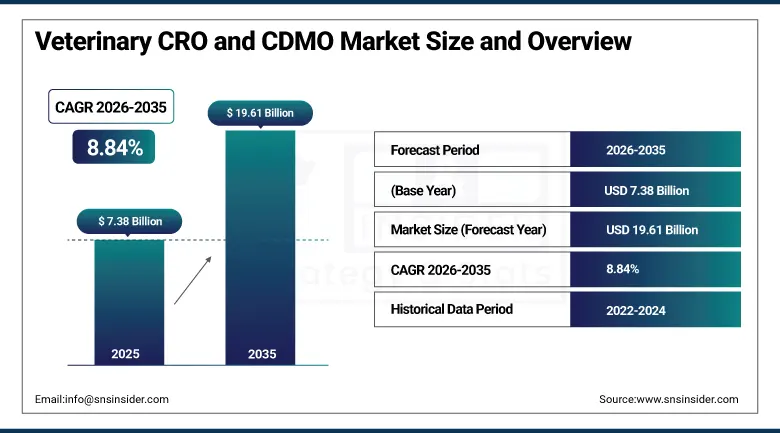

The Veterinary CRO and CDMO Market was valued at USD 7.38 Billion in 2025 and is expected to reach USD 19.61 Billion by 2035, growing at a CAGR of 8.84% from 2026–2035.

The global veterinary CRO and CDMO market is growing at a sustained and commercially significant pace. Veterinary contract research organizations (CROs) specialize in conducting preclinical and clinical trials, regulatory support, pharmacokinetics studies, and data management for animal health products, while veterinary contract development and manufacturing organizations (CDMOs) focus on drug formulation, process optimization, analytical method development, and scalable production of veterinary pharmaceuticals while maintaining regulatory compliance. The market is driven by increasing prevalence of diseases in animals such as cancer and zoonotic infections, increased focus on pet healthcare and the rising livestock population.

In May 2023, WuXi AppTec announced a partnership with Bayer to provide integrated drug development and manufacturing services for veterinary products, creating an end-to-end outsourcing relationship that covers preclinical development, analytical testing, and commercial-scale veterinary pharmaceutical manufacturing for Bayer’s animal health product pipeline. The partnership reflects the commercial recognition that integrated CRO-CDMO service provision accelerates veterinary pharmaceutical development timelines by eliminating inter-organization handoff complexity whose management creates delay and coordination cost.

Market Size and Forecast

-

Market Size in 2026E: USD 8.03 Billion

-

Market Size by 2035: USD 19.61 Billion

-

CAGR: 8.84% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Veterinary CRO and CDMO Market - Request Free Sample Report

Veterinary CRO and CDMO Market Trends

-

Adoption of integrated CRO-CDMO service models is increasing as animal health companies seek streamlined partners that can provide end-to-end development, regulatory, and manufacturing support

-

Growing demand for veterinary biologics and vaccines is driving investment in specialized CDMO capabilities, including advanced vaccine production and biologics manufacturing

-

The pet humanization trend is increasing demand for high-quality veterinary pharmaceuticals, supporting greater outsourcing of clinical research, testing, and regulatory services

-

Expansion of zoonotic disease surveillance and One Health initiatives is creating additional opportunities for veterinary CROs through government-funded and public health research programs

-

Rapid growth of the aquaculture industry is generating demand for veterinary drug and vaccine development services focused on fish health management and disease prevention programs

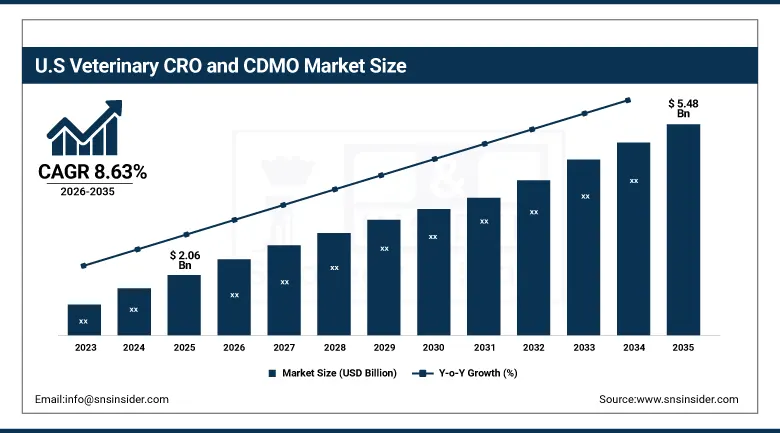

U.S. Veterinary CRO and CDMO Market Outlook

The U.S. Veterinary CRO and CDMO Market was valued at approximately USD 2.06 Billion in 2025 and is expected to reach approximately USD 5.48 Billion by 2035, growing at a CAGR of approximately 8.63%.

The U.S. is the most commercially significant veterinary CRO and CDMO market within North America’s dominant position. Charles River Laboratories, Covance (Labcorp), MPI Research (Inotiv), and WuXi AppTec’s U.S. operations collectively serve the domestic veterinary pharmaceutical and biotech outsourcing market. The USDA’s APHIS veterinary biologics regulatory framework, FDA’s Center for Veterinary Medicine’s drug approval pathway, and the extraordinary concentration of animal health company headquarters in the U.S. create the world’s most commercially significant national veterinary CRO and CDMO market. Major animal health companies including Zoetis, Merck Animal Health, Elanco, and Boehringer Ingelheim Vetmedica’s domestic outsourcing programme sustains consistent commercial demand.

Zoetis expanded its CDMO outsourcing programme in 2024 with new manufacturing partnerships for its veterinary mRNA vaccine pipeline, targeting novel RNA-based vaccines for influenza and other respiratory diseases in swine and poultry whose commercial production requires specialized lipid nanoparticle formulation CDMO capability. The outsourcing expansion reflects Zoetis’ commercial conviction that mRNA veterinary vaccine’s development timeline and manufacturing complexity create structured CDMO partnership motivation whose integrated service sustains pipeline velocity.

Veterinary CRO and CDMO Market Segment Analysis

-

By Service Type, the CDMO Services segment dominated the Veterinary CRO and CDMO Market with 85.5% share in 2025, while the CRO Services segment is the fastest growing.

-

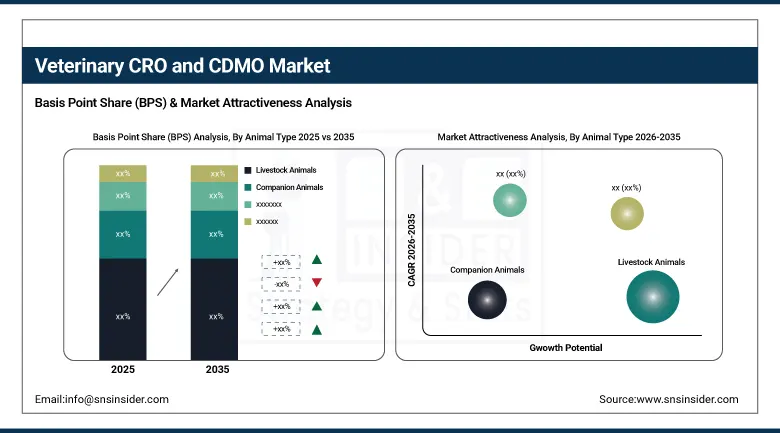

By Animal Type, the Livestock Animals segment dominated the Veterinary CRO and CDMO Market with 63% share in 2025, while the Companion Animals segment is the fastest growing.

-

By Application, the Medicine/Pharmaceuticals segment dominated the Veterinary CRO and CDMO Market with the highest market share in, while the Biologics/Vaccines & Immunologics segment is the fastest growing.

-

By End User, the Pharmaceutical & Biotech Companies segment dominated the Veterinary CRO and CDMO Market with approximately 58% share in 2025, while the Animal Health Companies segment is the fastest growing.

By Service, CDMO dominates, CRO grows fastest

CDMO services retained the dominant position with 85.5% of the veterinary CRO and CDMO market in 2025. CDMO’s extraordinary commercial dominance reflects the veterinary pharmaceutical industry’s structural preference for outsourced manufacturing whose capital intensity, regulatory complexity, and species-specific formulation expertise create consistent outsourcing motivation. Each veterinary pharmaceutical company whose product pipeline requires formulation development, process optimization, analytical method validation, and commercial-scale manufacturing creates CDMO procurement whose per-programme service value reflects the drug development stage’s complexity. The veterinary CDMO’s role in managing the most capital-intensive phase of drug development creates commercial relationships whose multi-year duration sustains consistent revenue.

CRO services are the fastest-growing segment because increasing prevalence of animal diseases, expanding companion animal oncology and specialty medicine therapeutic areas, and growing regulatory emphasis on veterinary drug safety evidence create growing clinical trial and research service demand. Each new veterinary therapeutic area that requires clinical efficacy and safety evidence creates CRO procurement whose regulatory requirement sustains service demand independently of sponsor R&D budget discretion.

By Animal Type, livestock dominates, companion animals grow fastest

Livestock animals retained the dominant position with 63% of the veterinary CRO and CDMO market in 2025. Livestock’s commercial primacy reflects the food production sector’s scale whose cattle, poultry, and swine health management creates the most commercially significant veterinary pharmaceutical procurement by value. Each new vaccine, antiparasitic, or growth promotion product for the global livestock sector creates CDMO manufacturing procurement whose per-batch commercial value reflects the production scale required for food-animal application. India’s 239.30 million tons of milk production in 2023-24 and global livestock expansion collectively create the scale motivation that sustains livestock’s dominant segment position.

Companion animals are the fastest-growing animal type because pet humanization’s progressive elevation of veterinary healthcare standards creates growing demand for premium pharmaceutical development across oncology, dermatology, cardiology, and neurology therapeutic areas. Each companion animal oncology programme that develops targeted cancer therapy creates CRO clinical trial and CDMO manufacturing procurement whose premium specialization reflects the therapeutic complexity. The extraordinary companion animal healthcare spending growth, driven by the pet owner’s willingness to invest in evidence-based veterinary medicine, creates commercial demand that sustains above-livestock segment growth rate.

By Application, medicine dominates, biologics grow fastest

Medicine and pharmaceuticals retained the dominant application position in the veterinary CRO and CDMO market in 2025. The veterinary pharmaceutical sector’s established antiparasitic, anti-infective, and anti-inflammatory product portfolios create consistent CDMO manufacturing procurement whose commodity character sustains volume-based commercial relationships. Each established veterinary pharmaceutical manufacturer’s product line renewal, line extension, and generic entry creates CDMO formulation and manufacturing procurement whose aggregate across the global veterinary pharmaceutical industry creates commercial scale. The large-volume livestock antiparasitic and vaccine manufacturing’s commercial scale creates CDMO relationship value.

Biologics including vaccines and immunologic are the fastest-growing application because veterinary mRNA vaccine technology’s commercial adaptation following COVID-19’s human mRNA vaccine success creates above-average new biologic development procurement. Each new veterinary vaccine programme that requires lipid nanoparticle formulation, cold chain manufacturing, and mRNA stability optimization creates specialized CDMO procurement whose technical complexity sustains premium commercial relationships. The animal health industry’s progressive adoption of monoclonal antibody, recombinant protein, and gene therapy creates biologics CDMO demand that compounds with biologic therapy’s therapeutic evidence development.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

South Africa |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Veterinary CRO and CDMO Market Insights

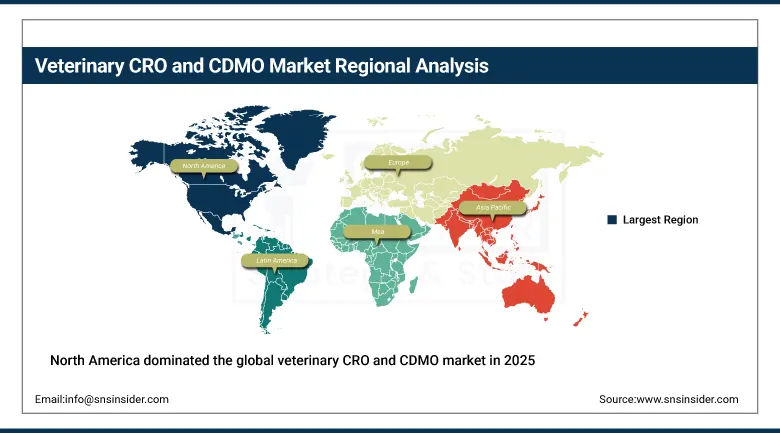

North America dominated the global veterinary CRO and CDMO market in 2025 as the most commercially mature veterinary pharmaceutical outsourcing market. The United States accounts for approximately 87.4% of North American revenues through Charles River Laboratories, Covance, MPI Research, and WuXi AppTec’s domestic operations, sustained by Zoetis, Merck Animal Health, Elanco, and Boehringer Ingelheim Vetmedica’s outsourcing programmes.

Canada contributes approximately 12.6% of North American revenues through its veterinary research institutions, the animal health industry’s outsourcing procurement, and the government’s animal disease surveillance research programme.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Veterinary CRO and CDMO Market Insights

Europe is a technically sophisticated veterinary CRO and CDMO market where EMA’s veterinary medicinal product regulatory framework, Boehringer Ingelheim Vetmedica’s German commercial leadership, and the European animal health industry’s outsourcing culture create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through Boehringer Ingelheim Vetmedica’s domestic outsourcing, EUROVET’s CRO service provision, and the pharmaceutical sector’s veterinary CDMO procurement.

France, the United Kingdom, and the Netherlands are significant secondary markets where MSD Animal Health, Ceva Sante Animale, and Virbac’s outsourcing programmes create consistent veterinary CRO and CDMO procurement.

Asia Pacific Veterinary CRO and CDMO Market Insights

Asia Pacific is the fastest-growing regional veterinary CRO and CDMO market, driven by China’s expanding animal health industry, India’s extraordinary livestock production scale, Japan’s advanced veterinary pharmaceutical market, and the region’s growing zoonotic disease research programme. China accounts for approximately 44.8% of Asia Pacific revenues through its domestic animal health company’s CDMO outsourcing, the government’s food safety programme’s veterinary research investment, and the growing companion animal healthcare market.

India’s extraordinary livestock scale creating vaccine and pharmaceutical demand, Japan’s advanced veterinary pharmaceutical regulatory framework, and South Korea’s growing companion animal market create significant secondary markets.

MEA & Latin America Veterinary CRO and CDMO Market Insights

South Africa leads MEA revenues at approximately 31.2% through its advanced veterinary research infrastructure, the livestock sector’s disease management programme, and the growing companion animal healthcare market. Brazil leads Latin American revenues at approximately 44.2% through its extraordinary livestock production scale—the world’s largest beef exporter—whose vaccine and antiparasitic procurement sustains consistent veterinary CDMO demand.

Market Dynamics

Growth Drivers: Increasing animal disease prevalence and pet humanization driving veterinary pharmaceutical development

Increasing prevalence of diseases in animals such as cancer and zoonotic infections is the veterinary CRO and CDMO market’s most commercially certain structural growth driver. The WHO’s one-health framework’s recognition that zoonotic disease prevention requires veterinary pharmaceutical investment creates government-funded animal health research that sustains CRO procurement beyond commercial pharmaceutical company outsourcing. Each new zoonotic pathogen surveillance programme creates CRO service demand whose public health motivation sustains investment. The growing livestock population’s disease burden creates vaccine and therapeutic development whose CDMO manufacturing requirement creates consistent commercial procurement.

Pet humanization’s progressive elevation of companion animal healthcare quality creates growing companion animal pharmaceutical and biologic development procurement. Each new companion animal oncology therapy, monoclonal antibody treatment, and specialty veterinary diagnostic creates CRO clinical trial and CDMO manufacturing procurement whose premium therapeutic complexity creates above-average per-programme commercial value.

Restraints: High R&D costs and stringent regulatory challenges for smaller veterinary companies

Veterinary drug development’s high R&D cost, encompassing animal safety studies, efficacy trials across target species, and multi-region regulatory submission, creates financial barriers for smaller animal health companies whose limited development budget constrains CRO and CDMO engagement. Each smaller veterinary pharmaceutical developer whose capital constraint creates development prioritization creates market limitation that moderates outsourcing adoption below the technically available opportunity.

Regulatory complexity across multiple USDA, FDA-CVM, and EMA veterinary medicinal product frameworks creates compliance investment that creates development cost overhead whose recovery requires pricing premium above commodity generic animal health product economics.

Opportunities: mRNA veterinary vaccine CDMO and aquaculture pharmaceutical development

mRNA veterinary vaccine manufacturing represents the most commercially transformative near-term CDMO opportunity whose lipid nanoparticle formulation, cold chain manufacturing, and mRNA stability management create premium specialized capability whose limited supply of qualified CDMO partners creates above-commodity pricing. Each new mRNA veterinary vaccine programme creates CDMO procurement whose technical complexity sustains long-term exclusive partnership relationships.

Aquaculture pharmaceutical and vaccine development creates a rapidly expanding new CRO and CDMO market whose fish health management requirement creates structured procurement from the growing global aquaculture production industry whose 90-million-tonne annual production creates disease management motivation.

Recent Developments:

-

2023: WuXi AppTec announced a partnership with Bayer in May 2023 to provide integrated drug development and manufacturing services for veterinary products, creating end-to-end outsourcing covering preclinical development, analytical testing, and commercial-scale veterinary pharmaceutical manufacturing.

-

2024: Zoetis expanded its CDMO outsourcing programme in 2024 with new manufacturing partnerships for its veterinary mRNA vaccine pipeline targeting novel RNA-based vaccines for swine and poultry respiratory diseases requiring specialized lipid nanoparticle CDMO capability.

-

2024: Charles River Laboratories expanded its veterinary CRO capabilities in 2024 with new large animal facility investment targeting cattle, swine, and equine clinical study services for companion animal oncology and livestock vaccine efficacy trials.

Veterinary CRO and CDMO Market Key Players

-

Zoetis Inc.

-

Merck Animal Health

-

Elanco Animal Health Inc.

-

Boehringer Ingelheim Vetmedica GmbH

-

Ceva Santé Animale

-

Charles River Laboratories International Inc.

-

Covance Inc.

-

WuXi AppTec Co., Ltd.

-

MPI Research

-

Pharmacyclics

-

EUROVET Animal Health BV

-

Virbac S.A.

-

Phibro Animal Health Corporation

-

Vetoquinol S.A.

-

Kindred Biosciences

-

Neogen Corporation

-

Bio Pharma Services Inc.

-

Absorption Systems

-

Bioxcel Therapeutics

-

Pacific Biotech International

Veterinary CRO and CDMO Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 7.38 Billion |

| Market Size by 2035 | USD 19.61 Billion |

| CAGR | CAGR of 8.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Service Type (CDMO Services/Drug Development & Manufacturing, CRO Services/Contract Research & Clinical Trials) • by Animal Type [Livestock Animals (Cattle, Poultry, Swine, Aquaculture), Companion Animals (Dogs, Cats, Horses, Others)] • by Application (Medicine/Pharmaceuticals, Biologics/Vaccines & Immunologics, Feed Additives, Diagnostics, Others) • by End User (Pharmaceutical & Biotech Companies, Veterinary Research Institutions, Government & Regulatory Bodies, Animal Health Companies, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Zoetis Inc., Merck Animal Health, Elanco Animal Health Inc., Boehringer Ingelheim Vetmedica GmbH, Ceva Santé Animale, Charles River Laboratories International Inc., Covance Inc., WuXi AppTec Co., Ltd., MPI Research, Pharmacyclics, EUROVET Animal, Health BV, Virbac S.A., Phibro Animal Health Corporation, Vetoquinol S.A., Kindred, Biosciences, Neogen Corporation, Bio Pharma Services Inc., Absorption Systems, Bioxcel Therapeutics, Pacific Biotech International |

Frequently Asked Questions

The Veterinary CRO and CDMO Market is expected to grow at a CAGR of 8.84% from 2026 to 2035.

The Veterinary CRO and CDMO Market was valued at USD 7.38 Billion in 2025.

Increasing prevalence of diseases in animals such as cancer and zoonotic infections creating advanced veterinary pharmaceutical demand, and increased focus on pet healthcare and rising livestock population driving innovative treatment development outsourced to specialized CROs and CDMOs.

CDMO Services dominated the Veterinary CRO and CDMO Market with 85.5% share in 2025 as confirmed by SNS Insider, while CRO Services is the fastest growing segment.

Livestock Animals dominated the Veterinary CRO and CDMO Market with 63% share in 2025 as confirmed by SNS Insider, while Companion Animals is the fastest growing segment.

Get in Touch