Histology and Cytology Market Report Scope & Overview:

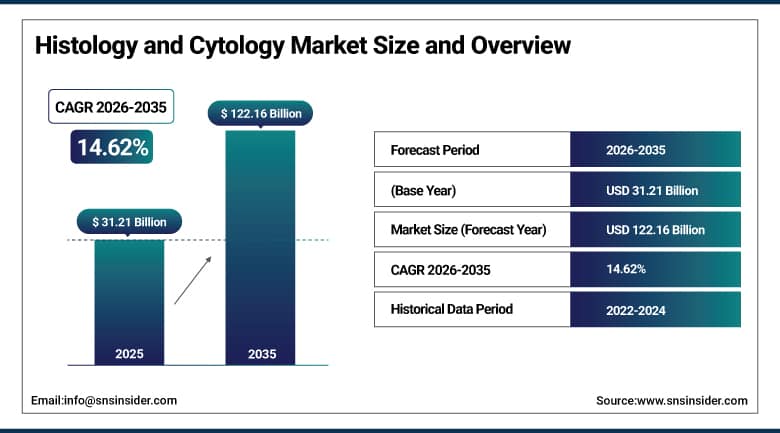

The Histology and Cytology Market was valued at USD 31.21 billion in 2025 and is expected to reach USD 122.16 billion by 2035, growing at a CAGR of 14.62% from 2026-2035.

The growth in the histology and cytology market is fueled by the increasing incidences of cancers and other chronic diseases globally, leading to an increase in the demand for diagnosis. The expanding health care infrastructure and the adoption of modern technologies such as digital pathology, artificial intelligence technology-based imaging, and automation in laboratories are some factors that are driving the market growth. Moreover, increasing awareness about the importance of detecting diseases at an early stage among both patients and health care professionals is adding to increased testing. Furthermore, research and development activities and the application of histology and cytology for drug discovery and diagnostics are playing a crucial role in the expansion of the market.

According to the World Health Organization (WHO), cancer is responsible for approximately 10 million deaths annually worldwide, making it one of the leading drivers of histopathology and cytology testing demand across healthcare systems globally.

Market Size and Forecast

-

Market Size 2026E: USD 35.77 Billion

-

Market Size 2035: USD 122.16 Billion

-

CAGR (2026-2035): 14.62%

-

Fastest Growing Market: Asia Pacific

-

Largest Market: North America

To Get More Information On Histology and Cytology Market - Request Free Sample Report

Histology and Cytology Market Trends

-

Rising prevalence of cancer and other chronic diseases is driving the histology and cytology market.

-

Growing demand for accurate disease diagnosis and early detection is boosting market growth.

-

Expansion of diagnostic laboratories, hospitals, and research institutes is fueling adoption of advanced diagnostic techniques.

-

Increasing focus on personalized medicine and precision diagnostics is shaping adoption trends.

-

Advancements in digital pathology, automated staining systems, and AI-assisted image analysis are enhancing diagnostic accuracy and efficiency.

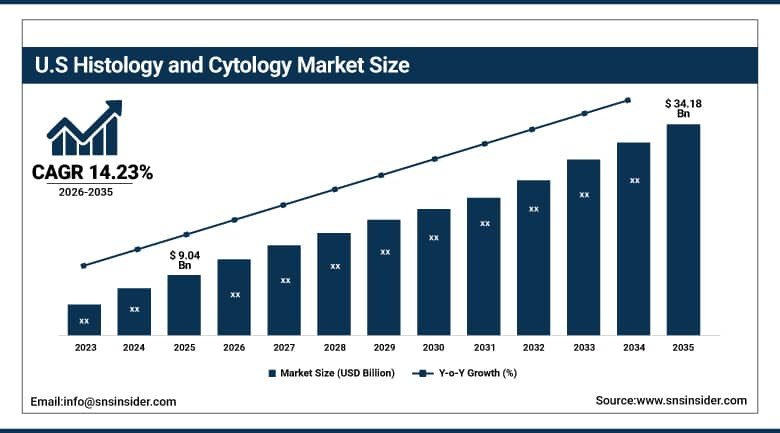

U.S. Histology and Cytology Market Size Outlook

The U.S. Histology and Cytology Market was valued at USD 9.04 billion in 2025 and is expected to reach USD 34.18 billion by 2035, growing at a CAGR of 14.23% from 2026-2035.

The growth of the U.S. histology and cytology market is fueled by increasing incidences of cancer and chronic diseases, resulting in the need for effective diagnosis using high-quality diagnostic techniques. The use of modern technology has been highly adopted by the market due to their ability to make diagnostic processes faster and more accurate. This is supported by improvements in healthcare infrastructure, increase in healthcare spending, and presence of state-of-the-art diagnostic labs.

Histology and Cytology Market Segment Analysis

-

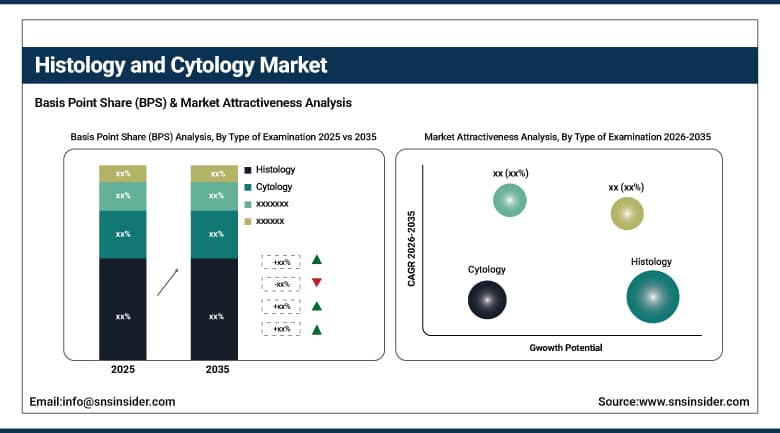

By Type of Examination, histology segment dominated the histology and cytology market in 2025 with 58% share; cytology segment is the fastest growing segment.

-

By Product, consumables and reagents segment dominated the market in 2025 with 61% share; instruments and analysis software system segment is the fastest growing segment.

-

By Application, clinical diagnostics segment dominated the market in 2025 with 52% share; drug discovery & designing segment is the fastest growing segment.

-

By End User, hospitals and clinics segment dominated the market in 2025 with 67% share; academic and research institutes segment is the fastest growing segment.

By Type of Examination, histology segment dominates the histology and cytology market, cytology segment is the fastest growing

The histology segment dominated the histology and cytology market because of the wide utilization of histology in disease diagnostics for identifying any abnormalities in tissues as well as diagnosing cancer cases. Histology is commonly used in clinical practice because it offers comprehensive details of the structure of tissues. Moreover, increased incidence rates of chronic diseases and cancer have augmented the importance of histology among patients as well as physicians. Improvements in various histology techniques and equipment, along with improvements in laboratory facilities, are contributing to the increasing usage of histology in clinics around the world.

The cytology segment is the fastest growing in the histology and cytology market owing to the increasing preference for minimal invasive diagnostic procedures and disease screening. Cytology involves analyzing individual cells and hence is highly beneficial in detecting cancers such as cervical and lung cancers at an early stage. Growing popularity of screening programs and increased awareness about preventive healthcare measures are driving the growth in the cytology market. Furthermore, developments in liquid cytology and cell analysis technologies are adding fuel to the growth of the cytology segment.

By Product, consumables and reagents segment dominates the histology and cytology market, instruments and analysis software systems segment is the fastest growing.

The consumables and reagents segment dominated the histology and cytology market owing to their regular need in lab processes and their importance in diagnosis. Products like staining dyes, fixatives, antibodies, and slides are regularly needed to process samples in the labs. The high volume of tests and rising demand for diagnostics in various healthcare facilities have further helped in maintaining their dominance in the histology and cytology market. Moreover, since these products belong to the category of consumables, they are responsible for bringing in significant income in the market.

The instruments and analysis software systems segment is the fastest growing in the histology and cytology market owing to a fast adoption rate of digital and automated pathology solutions. The use of advanced imaging systems and slide scanners together with diagnostic software powered by artificial intelligence has greatly improved processes in laboratories. Moreover, there has been an increasing need for high-throughput diagnoses and remote pathology. The use of artificial intelligence also contributes to the fast growth of this market segment.

By Application, clinical diagnostics segment dominates the histology and cytology market, drug discovery & designing segment is the fastest growing

The clinical diagnostics segment dominated the histology and cytology market because of its extensive usage in disease diagnosis, surveillance, and treatment planning. Both histological and cytological examination are necessary for disease diagnosis, especially for infections, inflammation, and cancer. Increase in patient population coupled with chronic diseases has increased demand for diagnostic procedures in hospital and laboratory settings. Furthermore, developments in the healthcare industry along with increased knowledge on the importance of disease diagnosis have enabled clinical diagnostics to become the dominating application area within the histology and cytology market.

The drug discovery & designing segment is the fastest growing in the histology and cytology market owing to increased usage of cellular and tissue analysis in pharmaceutical industry. Both histological and cytological methods are important in assessing the effectiveness of drugs as well as their toxic effects on tissues. The rising investments in the biotechnological and pharmaceutical research sector has increased usage of sophisticated technologies like high-content screening along with advancements in AI technology.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

93.8% |

|

Europe |

United Kingdom |

26.4% |

|

Asia Pacific |

China |

57.2% |

|

Middle East & Africa |

UAE |

14.1% |

|

Latin America |

Brazil |

52.6% |

North America Histology and Cytology Market Insights

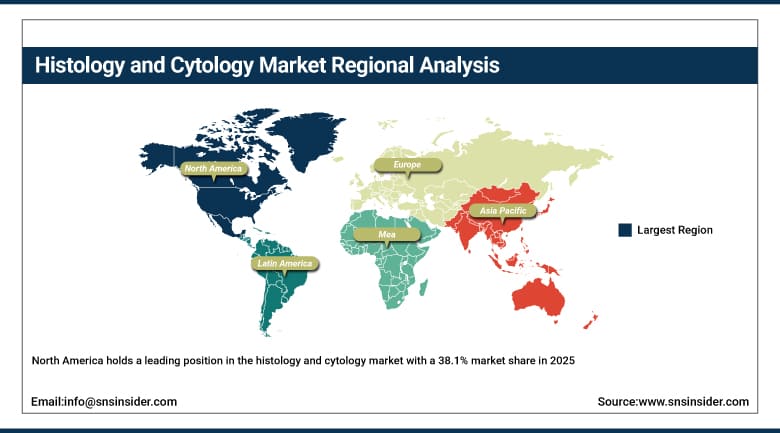

North America holds a leading position in the histology and cytology market with a 38.1% market share in 2025, owing to an excellent healthcare system and the presence of advanced diagnostics. Factors that drive market growth in North America include an efficient pathology laboratory, increased cancer screening tests, and rising awareness regarding early diagnosis. Technological advancements in digital pathology and laboratory automation also contribute to market growth. Rising healthcare expenditure and favorable reimbursement practices along with emphasis on precision medicine are additional factors enabling the dominance of the region in the global histology and cytology market.

In North America, diagnostic demand is strongly supported by high cancer incidence. The U.S. Centers for Disease Control and Prevention (CDC) reports that there are approximately 1.7 million new cancer cases diagnosed annually in the United States, driving large-scale adoption of histology, biopsy analysis, and cytology-based screening programs.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Histology and Cytology Market Insights

Europe histology and cytology market is fueled by efficient healthcare facilities, increasing cancer screening initiatives, and increased adoption of sophisticated diagnostic techniques. Growing instances of chronic ailments coupled with the importance of early disease diagnosis will increase the demand for histopathological analysis. Europe has an advantage in terms of its robust laboratory facilities and stringent regulatory policies to guarantee precise diagnoses. Moreover, the increasing application of digital pathology, laboratory automation, and artificial intelligence-enabled diagnostic procedures is increasing efficiency.

In Europe, the burden remains significant. The European Commission’s Joint Research Centre (JRC) estimates ~2.7 million new cancer cases annually in the EU, reinforcing strong utilization of pathology diagnostics, tissue analysis, and laboratory-based screening systems across public healthcare networks.

Asia Pacific Histology and Cytology Market Insights

The Asia Pacific region is the fastest growing region in the histology and cytology market with a 15.20% CAGR, owing to investments in healthcare and infrastructure development. Factors such as higher incidences of cancer, increased awareness about disease prevention and detection, and greater access to medical facilities have been driving the market towards growth. Urbanization, high disposable incomes, and hospitals' presence play a crucial role in enhancing the demand for histology and cytology. Moreover, the rise in digital pathology, government initiatives to upgrade their healthcare sector, and availability of diagnostic laboratories have been contributing towards the growth of the market.

In Asia Pacific, the disease burden is the highest globally. The WHO International Agency for Research on Cancer (IARC) reports that the region accounts for over 50% of global cancer cases, with China and India contributing a large share due to population size and rising chronic disease prevalence.

Middle East & Africa and Latin America Histology and Cytology Market Insights

Middle East & Africa and Latin America Histology and Cytology Market sees slow but steady growth owing to improved infrastructure in the healthcare sector and increased knowledge on early diagnosis of diseases. Increase in the number of cancer cases is also fueling demand for diagnostic tests. Increase in hospital network along with investments made towards building up laboratories is also contributing to the growth of the market. Lack of sophisticated technology and availability of professionals, however, hampers faster adoption. Nevertheless, government measures to improve healthcare systems and rising use of diagnostics are likely to drive market growth.

In Latin America, cancer incidence continues to rise. The Pan American Health Organization (PAHO) reports approximately 1.5 million new cancer cases annually in the region, increasing demand for diagnostic pathology services and laboratory expansion across public and private healthcare systems.

In the Middle East & Africa (MEA), diagnostic infrastructure is expanding rapidly. The WHO African Region highlights that cancer cases are expected to rise significantly due to population growth and late-stage diagnosis patterns, with sub-Saharan Africa projected to see a near doubling of cancer cases by 2040, driving demand for improved histology and cytology services.

Market Dynamics

Growth Drivers: Rising global cancer burden and increasing demand for early and accurate diagnostic testing solutions

The increased incidence of cancer in the world is one factor behind rising demand for histology and cytology tests. Increased incidence of cancers like cervical cancer, breast cancer, lung cancer, and other types of cancers is forcing health care facilities to employ advanced technologies to diagnose patients early and correctly. Increasing awareness among both patients and health care practitioners about the need for early diagnosis is adding to the growth of the market. Technological developments in pathology systems, imaging, and molecular diagnostics have helped increase efficiency and accuracy of tests. Improved health care facilities and more screening programs in developing and developed countries are leading to increased testing.

In 2025, the American Cancer Society estimates that approximately 2.04 million new cancer cases and 618,120 deaths in the U.S. will occur, with approximately 5,600 new cases per day, on average.

Restraints: High cost of advanced diagnostic systems and laboratory infrastructure limiting adoption in low-resource settings

Implementation of histology and cytology products is hampered by expensive investments in complex instruments and diagnostic reagents. In small medical centers and laboratories, there is always an issue of funding to enable investment in costly pathology systems. Operation and maintenance cost increases the cost further, especially in developing countries. Also, the need for highly trained staff to run complicated diagnosis machinery results in additional expenditure. Moreover, lack of good remuneration strategies for diagnosis in certain medical care systems limits implementation of histology and cytology products. These economic limitations hinder widespread adoption of histology and cytology innovations in low-income areas. Healthcare systems still rely on older diagnostic techniques due to such economic challenges.

Opportunities: Rising focus on personalized medicine and targeted cancer therapies boosting diagnostic demand

Growing focus on personalized medicines will open up immense potential for cytology and histology solutions. Proper cell analysis plays an important role in developing effective treatments that will be tailored to individual patients. Growing application of companion diagnostics within the field of oncology will further increase demand for precise histopathological testing. There is a growing trend among pharmaceuticals and biotech companies that are focusing extensively on conducting studies and drug development activities, which will fuel the uptake of both histology and cytology services. Increasing clinical trials and biomarkers research will add to the growth in demand for such diagnostic solutions. Moreover, growing cooperation between diagnostic labs and research institutes will help create new avenues in cancer treatment.

Recent Developments:

-

2026: Roche acquired PathAI in 2026 to integrate AI-driven digital pathology into Ventana systems, enabling automated histology slide interpretation, improving cancer tissue diagnosis workflows and expanding AI-assisted pathology decision support across clinical laboratories globally.

-

2026: Danaher expanded Leica Biosystems Aperio digital pathology platform with AI-enabled whole-slide imaging updates, improving histology slide scanning speed, enabling remote pathology diagnosis and enhancing automated cancer tissue analysis in clinical laboratory environments.

-

2025: Thermo Fisher launched upgraded AutoStainer platform for histology laboratories in 2025, improving tissue staining consistency, automating slide preparation, and increasing throughput for cancer diagnostics and cytology sample processing workflows in clinical labs.

-

2025: BD introduced updated SurePath liquid-based cytology system enhancements in 2025, improving cervical cancer screening accuracy, reducing sample contamination, and increasing automated cytology slide preparation efficiency in diagnostic laboratories globally.

-

2025: Agilent launched upgraded Dako Omnis immunohistochemistry platform in 2025, improving automated staining of tissue samples, enhancing biomarker detection accuracy, and increasing standardization of histopathology workflows in cancer diagnostic laboratories.

Histology and Cytology Market Key Players are:

-

Abbott Laboratories

-

Becton, Dickinson and Company (BD)

-

F. Hoffmann-La Roche Ltd. (Roche Diagnostics)

-

Thermo Fisher Scientific

-

Danaher Corporation

-

Hologic

-

Merck KGaA

-

Agilent Technologies

-

Bio-Rad Laboratories

-

PerkinElmer

-

Sysmex Corporation

-

Trivitron Healthcare

-

Sakura Finetek Japan

-

Carl Zeiss AG

-

Koninklijke Philips N.V. (Philips)

-

Olympus Corporation

-

Promega Corporation

-

Oxford Gene Technology (OGT)

-

CellPath

-

STRATEC Biomedical Systems

Histology and Cytology Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 31.21 Billion |

| Market Size by 2035 | USD 122.16 Billion |

| CAGR | CAGR of 14.62% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type of Examination (Histology, Cytology) • By Product (Instruments and Analysis Software System, Consumables and Reagents) • By Application (Drug Discovery & Designing, Clinical Diagnostics, Research) • By End User (Hospitals and Clinics, Academic and Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, Becton, Dickinson and Company (BD), F. Hoffmann La Roche Ltd. (Roche Diagnostics), Thermo Fisher Scientific, Danaher Corporation, Hologic, Merck KGaA, Agilent Technologies, Bio Rad Laboratories, PerkinElmer, Sysmex Corporation, Trivitron Healthcare, Sakura Finetek Japan, Carl Zeiss AG, Koninklijke Philips N.V. (Philips), Olympus Corporation, Promega Corporation, Oxford Gene Technology (OGT), CellPath, STRATEC Biomedical Systems |

Frequently Asked Questions

North America dominated the Histology and Cytology Market in 2025.

The Histology segment dominated the Histology and Cytology Market in 2025.

Rising global cancer burden and increasing demand for early and accurate diagnostic testing solutions.

The Histology and Cytology Market was valued at USD 31.21 billion in 2025.

The Histology and Cytology Market is expected to grow at a CAGR of 14.62% from 2026 to 2035.

Get in Touch