Video Management Software Market Report Scope & Overview:

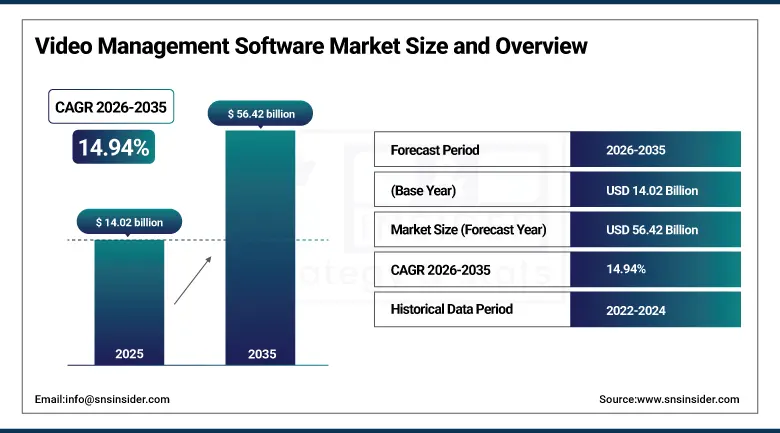

The Video Management Software Market was valued at USD 14.02 billion in 2025 and is expected to reach USD 56.42 billion by 2035, growing at a CAGR of 14.94% from 2026-2035.

The Video Management Software market growth is propelled by the high demand for advanced surveillance systems, growing security threats, and increased adoption of AI-based video analysis software. The increasing number of smart city initiatives, growing installation of IP-based cameras, and rising requirements for real-time surveillance in both government and private organizations are contributing to the growth of the market. Advancements in technologies such as cloud computing, edge computing, and cybersecurity software solutions are improving the efficiency of these systems.

The U.S. National Institute of Standards and Technology (NIST) reports increasing adoption of AI-based video analytics in surveillance systems, including facial recognition, object detection, and anomaly detection, driven by advancements in machine learning and enhanced real-time monitoring capabilities.

The U.S. Department of Justice (DOJ) continues to support funding initiatives for public safety, including the deployment of surveillance infrastructure in cities and the implementation of advanced crime prevention technologies to strengthen law enforcement and security operations.

Market Size and Forecast

-

Market Size in 2025: USD 14.02 Billion

-

Market Size by 2035: USD 56.42 Billion

-

CAGR: 14.94% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Video Management Software Market - Request Free Sample Report

Video Management Software Market Trends

-

Rising demand for advanced surveillance and real-time video monitoring is driving the video management software (VMS) market.

-

Growing adoption across government, transportation, retail, and commercial sectors is boosting market growth.

-

Expansion of smart cities, critical infrastructure security, and public safety initiatives is fueling deployment.

-

Increasing focus on centralized video storage, analytics, and remote accessibility is shaping adoption trends.

-

Advancements in AI-powered video analytics, cloud-based VMS platforms, and edge computing are enhancing efficiency and intelligence.

-

Rising need for cybersecurity, compliance, and scalable surveillance systems is supporting market expansion.

-

Collaborations between security solution providers, hardware manufacturers, and enterprises are accelerating innovation and global adoption.

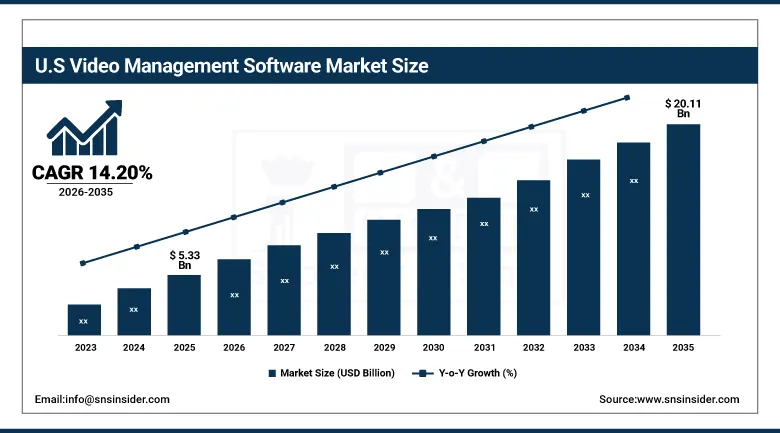

U.S. Video Management Software Market was valued at USD 5.33 billion in 2025 and is expected to reach USD 20.11 billion by 2035, growing at a CAGR of 14.20% from 2026-2035.

The growth in U.S. Video Management Software market is attributed to growing security issues, increasing use of artificial intelligence in video surveillance systems, and rise in smart city projects. High demand from government, transport, and commercial applications, coupled with fast adoption of cloud-based video management solutions, is aiding market growth.

Video Management Software Market Segment Highlights

-

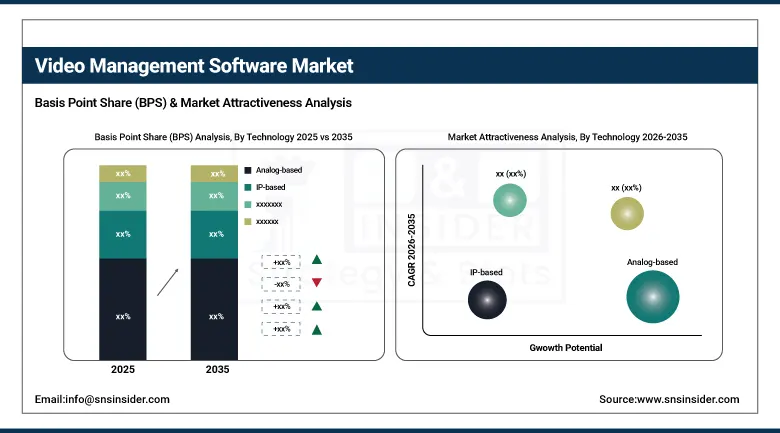

By Technology, Analog-based segment dominated the Video Management Software Market in 2025 with approximately 68% share; IP-based segment fastest growing (CAGR).

-

By Deployment, On-premises segment dominated the Video Management Software Market in 2025 with approximately 71% share; Cloud segment fastest growing (CAGR).

-

By Application, Video Analytics segment dominated the Video Management Software Market in 2025 with a significant share; Remote Monitoring segment fastest growing (CAGR).

-

By Vertical, Retail & E-commerce segment dominated the Video Management Software Market in 2025 with a significant share; Healthcare segment fastest growing (CAGR).

Video Management Software Market Segment Analysis

By Technology, Analog-based segment dominates the Video Management Software Market, IP-based segment expected to grow fastest

Analog-based Segment led the Video Management Software Market in 2025 owing to its large number of installations, low implementation cost, and continued dependence on old CCTV system in both commercial and public areas. Many businesses use analog systems in simple surveillance operations when financial issues do not allow them to switch fully to digital solutions. The simplicity of maintenance and compatibility with current installations continue to drive usage in cost-sensitive applications and slower adoption markets.

IP-based Segment is expected to grow at the highest CAGR driven by rising need for high definition video surveillance and scalable architectures. IP-based solutions offer better access and management through remote monitoring and integration of AI-based software. The rapid adoption of smart city solutions and enterprise digitalization along with improvement in network infrastructure continues to fuel the move from analog to IP-based solutions.

By Deployment, On-premises segment dominates the Video Management Software Market, Cloud segment expected to grow fastest

The on-premises segment led the Video Management Software Market in 2025 owing to the presence of high demands for data security, regulatory compliances, and complete control over the surveillance system. Companies in the critical industry segment have a preference for storing their data locally to mitigate any risks associated with cyber-attacks and maintain operational autonomy. Existing IT infrastructures and concerns regarding data exposure to third parties are also driving their adoption. The on-premises segment is still highly preferred by government, critical infrastructures, and large enterprises.

The cloud segment is the fastest-growing (CAGR) owing to the increasing demand for flexible, scalable, and economical video management software solutions. Cloud deployment allows organizations to monitor remotely and integrate easily with sophisticated analytical and artificial intelligence tools. Subscription-based pricing and low infrastructure costs are making organizations adopt this segment irrespective of their size. Digital transformation programs, remote working, and real-time surveillance requirements at different locations are adding to the adoption rate.

By Application, Video Analytics segment dominates the Video Management Software Market, Remote Monitoring segment expected to grow fastest

The Video Analytics segment dominated the Video Management Software Market in 2025 due to high demand for smart video surveillance systems that have the ability to offer real-time insights and threat detection with the help of AI technology. The increasing use of analytics for facial recognition, behavior analysis, and anomaly detection for making the security process more efficient and effective. This shift from the traditional surveillance to security management is fueling the growth of the market.

The Remote Monitoring segment is the fastest-growing segment (CAGR). The high growth of this segment can be attributed to the rising need for centralized surveillance in various locations. The rising demand for remote monitoring to enhance efficiency, cut down on cost, and offer real-time incident response is driving the growth of this segment. The increasing adoption of IP-based cameras and cloud connectivity will boost the growth of this segment in the coming years.

By Vertical, Retail & E-commerce segment dominates the Video Management Software Market, Healthcare segment expected to grow fastest

The Retail & E-commerce segment was the leader in the Video Management Software Market in 2025 owing to the increased demand for security against theft, analysis of customer behavior, and improved operational efficiency both in the physical and e-commerce retail environments. Video management software is employed by retailers to increase security and efficiency and improve customers' shopping experience. Increasing adoption of omnichannel retailing practices and the focus on loss prevention and inventory security further drive the demand.

The Healthcare segment is the fastest growing (CAGR) owing to the increasing demand for patient security, regulatory compliance, and advanced monitoring solutions. Hospitals and healthcare facilities are increasingly adopting video management software for enhanced security, protection of assets, and operational efficiency. The rising investments in smart hospital infrastructure and digital transformation of the healthcare industry further drive the adoption of video management software. The growing need for a secure environment and effective monitoring of patients and facilities boosts the demand.

Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

92.6% |

|

Europe |

United Kingdom |

25.8% |

|

Asia Pacific |

Australia |

8.2% |

|

Middle East & Africa |

UAE |

14.1% |

|

Latin America |

Brazil |

51.3% |

North America Video Management Software Market Insights

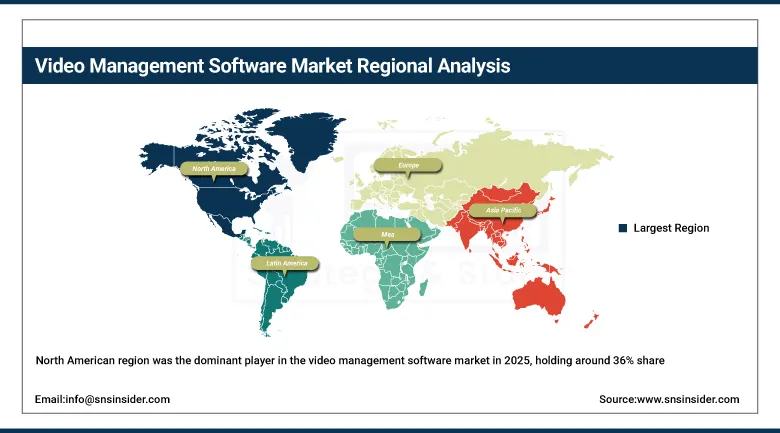

The North American region was the dominant player in the video management software market in 2025, holding around 36% of the overall market revenue share. Adoption of advanced surveillance solutions, use of IP-based security solutions, and fast integration of AI-powered video analytics solutions have driven the growth of the market. Demand from government, transport, and commercial end-user segments has also aided growth in the market. Factors such as availability of leading technology vendors, digital infrastructure development, and rising smart city and public safety initiatives have further helped in driving regional dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Video Management Software Market Insights

Asia Pacific region will register the fastest growth during the forecast period on account of the fast digitalization process, development of urban infrastructure, and deployment of surveillance technology. Investments in smart cities, public safety initiatives, and video analytics through artificial intelligence will drive growth in the video management systems market. In addition, demand from different end-user industries such as commercial, industrial, and government will encourage adoption of video management systems. Furthermore, high internet penetration, use of cloud computing, and government support will drive the growth of the video surveillance market.

Europe Video Management Software Market Insights

Europe holds a significant share in the video management software market because of stringent security measures, digital infrastructure, and the presence of intelligent surveillance systems. The rising use of AI-based video analytics, cloud-based surveillance systems, and integrated security systems is fueling the growth of the market. There is rising demand for video management software from governments, transportation companies, retailers, and BFSI companies that are driving market growth. Ongoing investments in smart cities and public safety programs, along with technological advancements and high-level security, are boosting the regional market scenario.

Middle East & Africa and Latin America Video Management Software Market Insights

The Middle East & Africa region and Latin America are new markets for video management solutions, which are being backed up by urbanization trends and investments in security infrastructures. The increasing demand for security systems in public spaces, traffic control systems, and security systems in businesses is creating opportunities for adoption. There are also significant investments by governments in smart city concepts and digital transformations aimed at ensuring greater security and efficiency. The increased use of IP-based surveillance systems and cloud technologies is helping to fuel growth. Growth is still in its early stages but is expected to continue in the future.

Market Growth Drivers:

Rising demand for advanced surveillance systems and intelligent security infrastructure across commercial and public safety environments globally: There are growing worries about security problems that are arising in business organizations, transportation sectors, smart cities, and various other infrastructures; such concerns are driving the need for video management software solutions. Businesses are increasingly investing in sophisticated surveillance systems to enhance their surveillance, incident detection, and security operations. Urbanization and infrastructural developments are contributing to the increasing demand for central video management systems. The integration of artificial intelligence, face recognition technology, and real-time surveillance features is enhancing efficiency of these systems. The growing use of IP cameras and other similar devices is also increasing the demand. There are ongoing developments in security systems in businesses and government institutions.

Market Restraints:

Data privacy concerns and cybersecurity risks restricting seamless deployment of cloud-based video surveillance systems globally: The increasing use of cloud video management software creates issues with respect to data security, data privacy, and the potential for unauthorized access to confidential surveillance footage. The issue of cyberattacks that can compromise the security of surveillance networks presents dangers of data theft and system manipulation. The stringent data protection laws in different geographical locations present a challenge for implementation in a global setting. Companies involved in managing confidential data of public and enterprise nature have challenges in securing their video contents. This is being hampered by the fear of misuse of surveillance cameras.

Market Opportunities:

Integration of artificial intelligence and advanced video analytics creating new opportunities for intelligent surveillance and automation systems: The integration of AI technology within video management software systems will lead to features like facial recognition, behavior analysis, and predictive threat detection becoming a reality. Decision making through analytics becomes more efficient due to AI integration while improving the accuracy of real-time surveillance. There are huge opportunities being created by rising demands for automated security systems in smart cities, retail and transportation. With edge computing and machine learning technology, video processing efficiency and speed continue to be enhanced. Investment in smart infrastructure is driving the adoption of intelligent surveillance systems. Innovation in technology is set to drive new applications and growth areas.

Recent Developments:

-

2026: Axis upgraded Camera Station Pro with natural language video search, allowing operators to retrieve footage using conversational queries, improving investigation speed and reducing manual video review time.

-

2026: Bosch launched IQSIGHT intelligence-first video platform, designed to integrate with leading VMS platforms such as Genetec and Milestone, enhancing AI-driven surveillance analytics and scalable cloud video deployments.

-

2025: Eagle Eye Networks launched AI-powered Remote Video Monitoring integrated into its cloud VMS platform, enabling real-time threat detection, automated alerts, and hybrid human-AI surveillance response systems.

-

2024: Motorola Solutions enhanced Avigilon Unity Video VMS with cloud-connected deployment options, improved AI-powered video search, and unified interface combining video analytics, access control, and incident management workflows.

Video Management Software Market Key Players

-

Genetec Inc.

-

Milestone Systems

-

Axis Communications

-

Bosch Security Systems

-

Honeywell International Inc.

-

Motorola Solutions (Avigilon)

-

Hanwha Vision

-

Hikvision

-

Dahua Technology

-

Qognify

-

Verint Systems

-

Pelco

-

Exacq Technologies

-

AxxonSoft

-

Vivotek

-

Eagle Eye Networks

-

Cisco Systems

-

Axon Enterprise

-

Kedacom

-

BriefCam

|

Report Attributes |

Details |

|---|---|

| Market Size in 2025 | USD 14.02 Billion |

| Market Size by 2035 | USD 56.42 Billion |

| CAGR | CAGR of 14.94% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (IP-based, Analog-based) • By Deployment (Cloud, On-premises) • By Application (Video Analytics, Access Control Integration, Cloud Storage & Management, Perimeter Protection, Remote Monitoring, Others) • By Vertical (Retail & E-commerce, Government & Law Enforcement, BFSI, Transportation & Logistics, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Genetec Inc., Milestone Systems, Axis Communications, Bosch Security Systems, Honeywell International Inc., Motorola Solutions, Hanwha Vision, Hikvision, Dahua Technology, Qognify, Verint Systems, Pelco, Exacq Technologies, AxxonSoft, Vivotek, Eagle Eye Networks, Cisco Systems, Axon Enterprise, Kedacom, BriefCam |

Frequently Asked Questions

Ans: North America dominated the Video Management Software Market in 2025.

Ans: The Analog-based segment dominated the Video Management Software Market in 2025.

Ans: Rising demand for advanced surveillance systems and intelligent security infrastructure across commercial and public safety environments globally.

Ans: The Video Management Software Market was valued at USD 14.02 billion in 2025.

Ans: The Video Management Software Market is expected to grow at a CAGR of 14.94% from 2026 to 2035.

Get in Touch